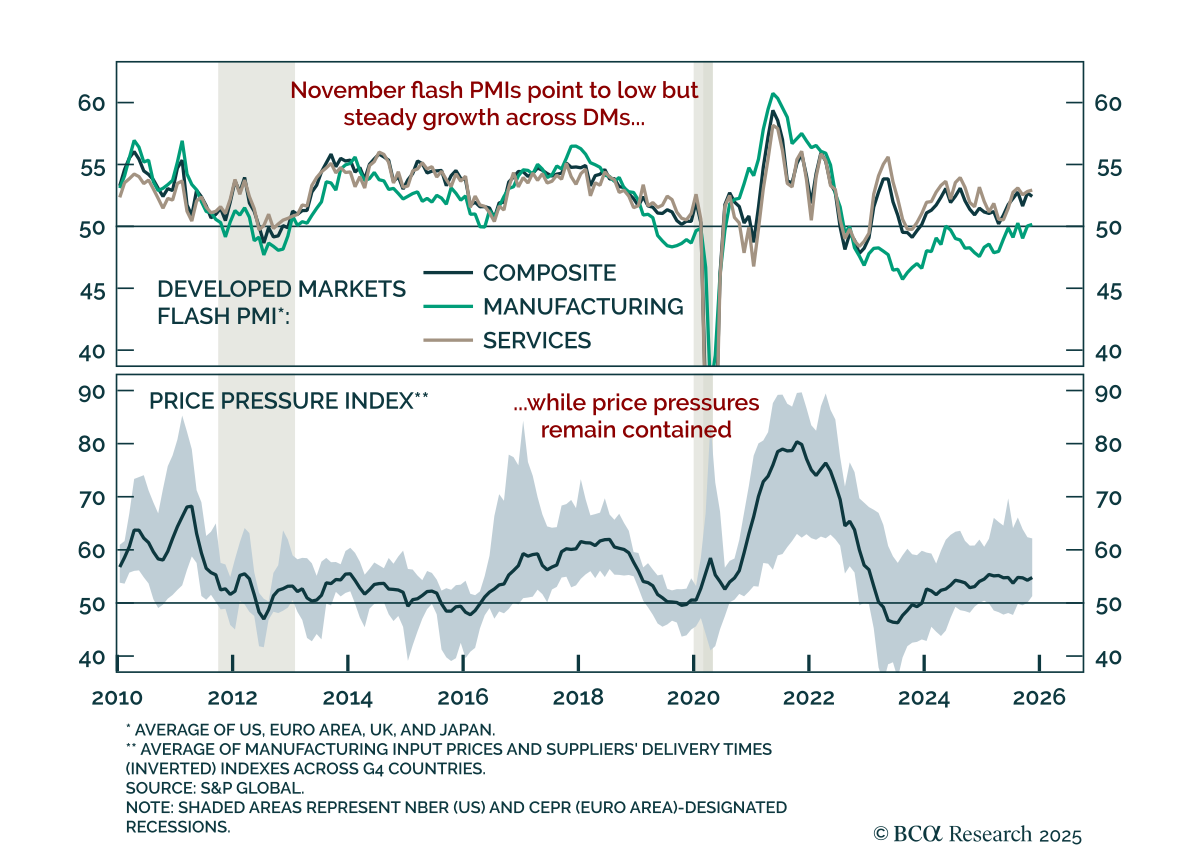

Developed Countries

We present our five key views for global fixed income markets in 2026. A year that will see the global easing cycle come to an end.

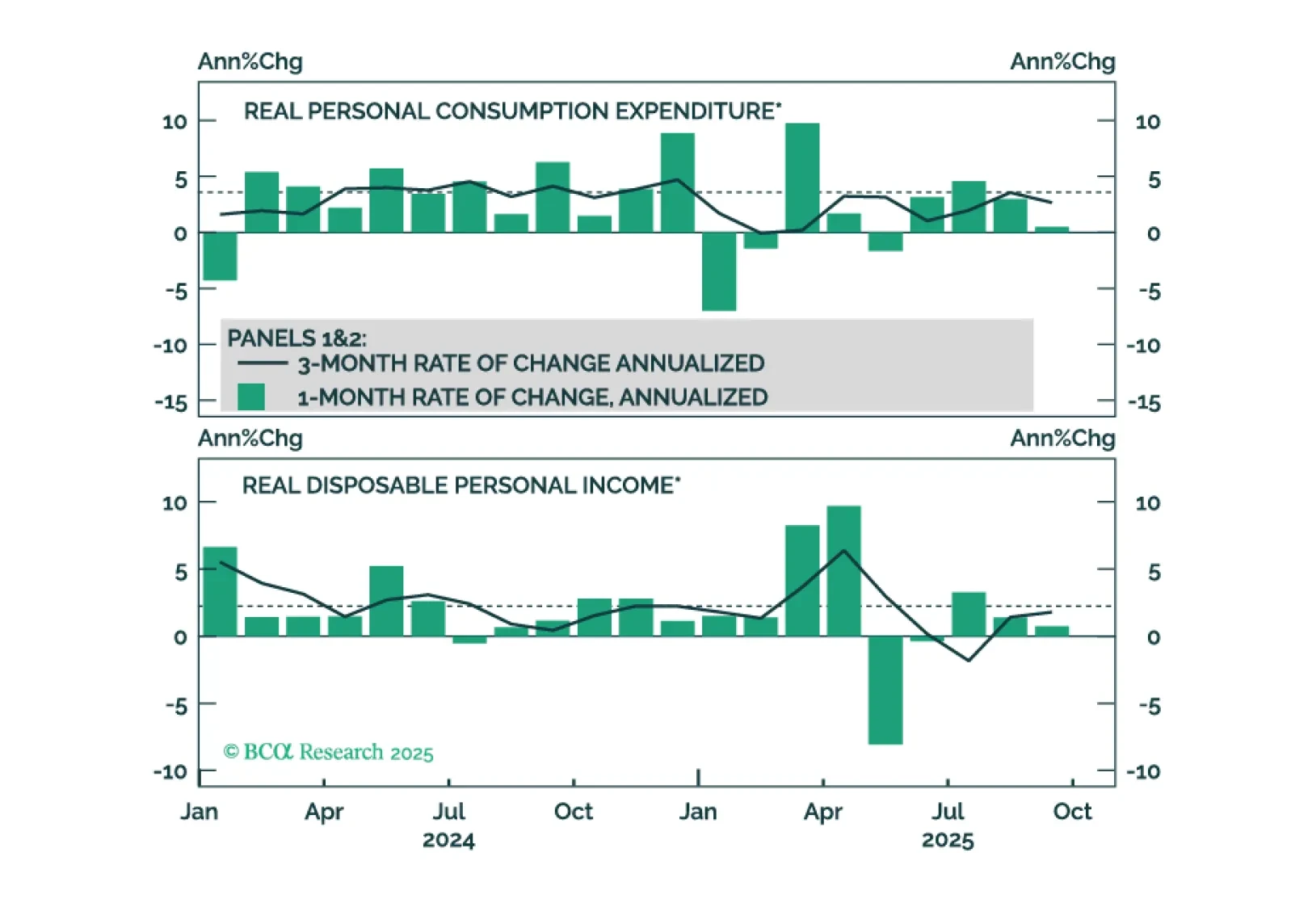

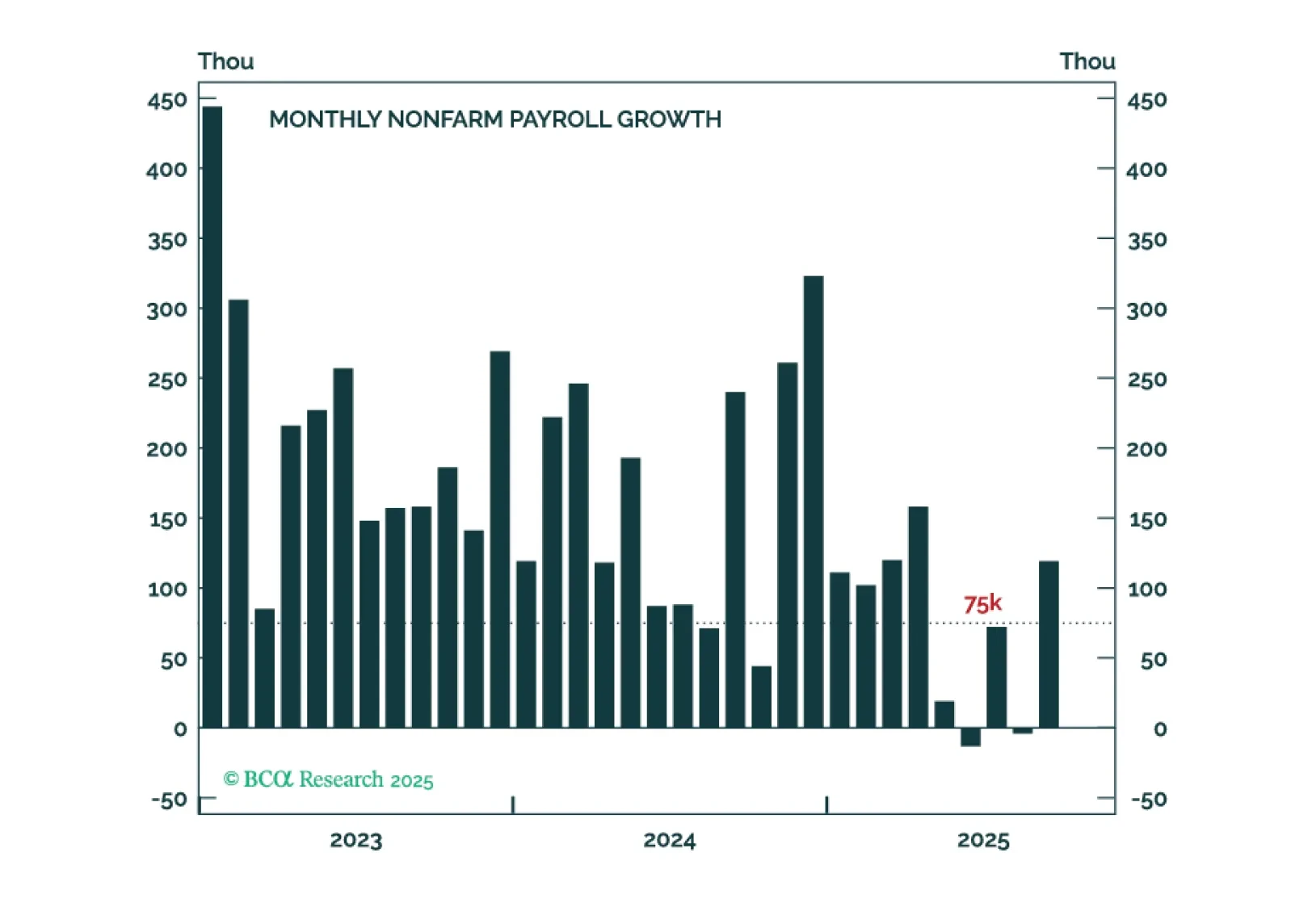

September’s weak consumer spending data challenge the K-shaped recovery narrative and suggest that spending will slow to match already-weak employment growth.

Our Portfolio Allocation Summary for December 2025.

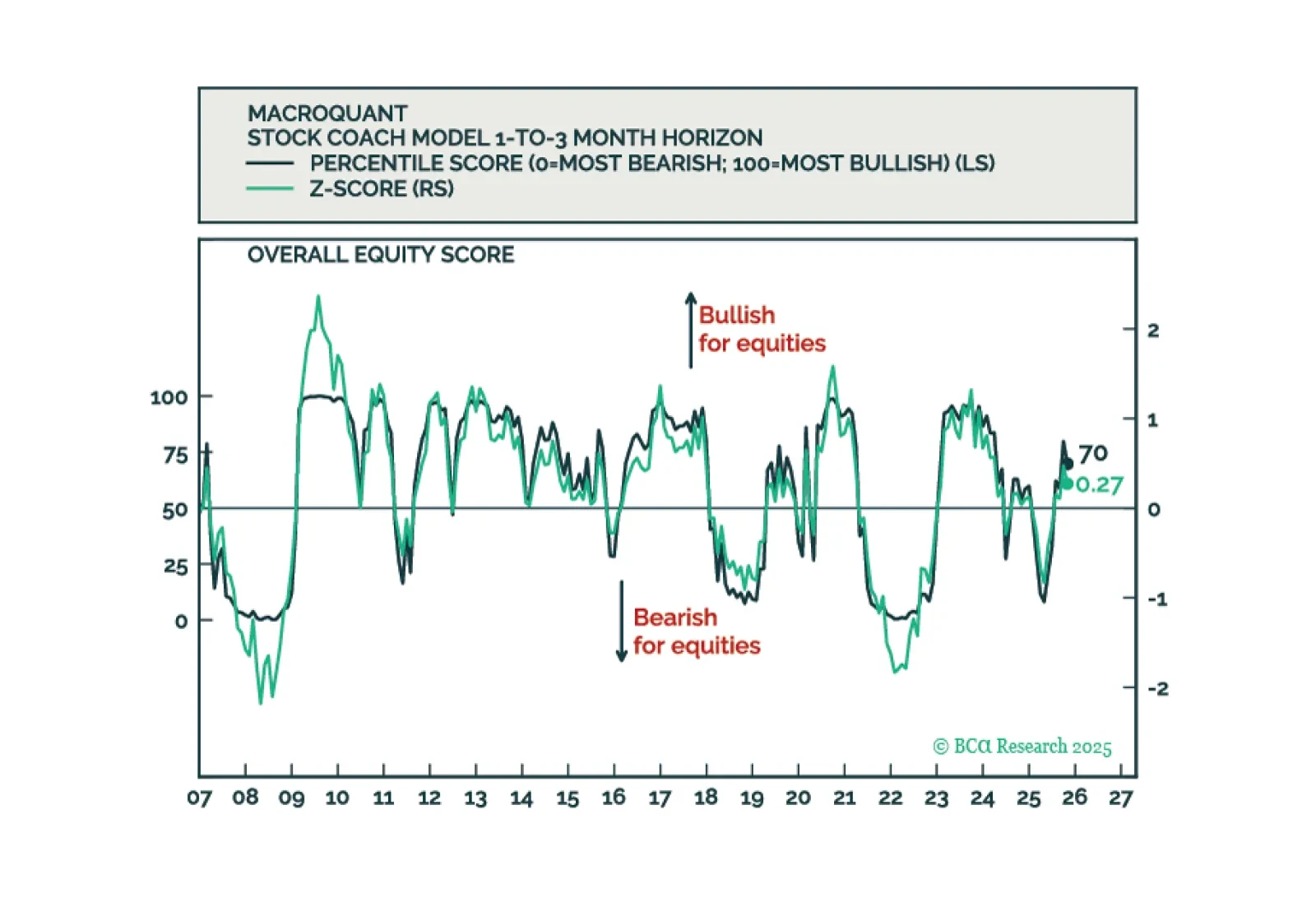

MacroQuant remains tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold.

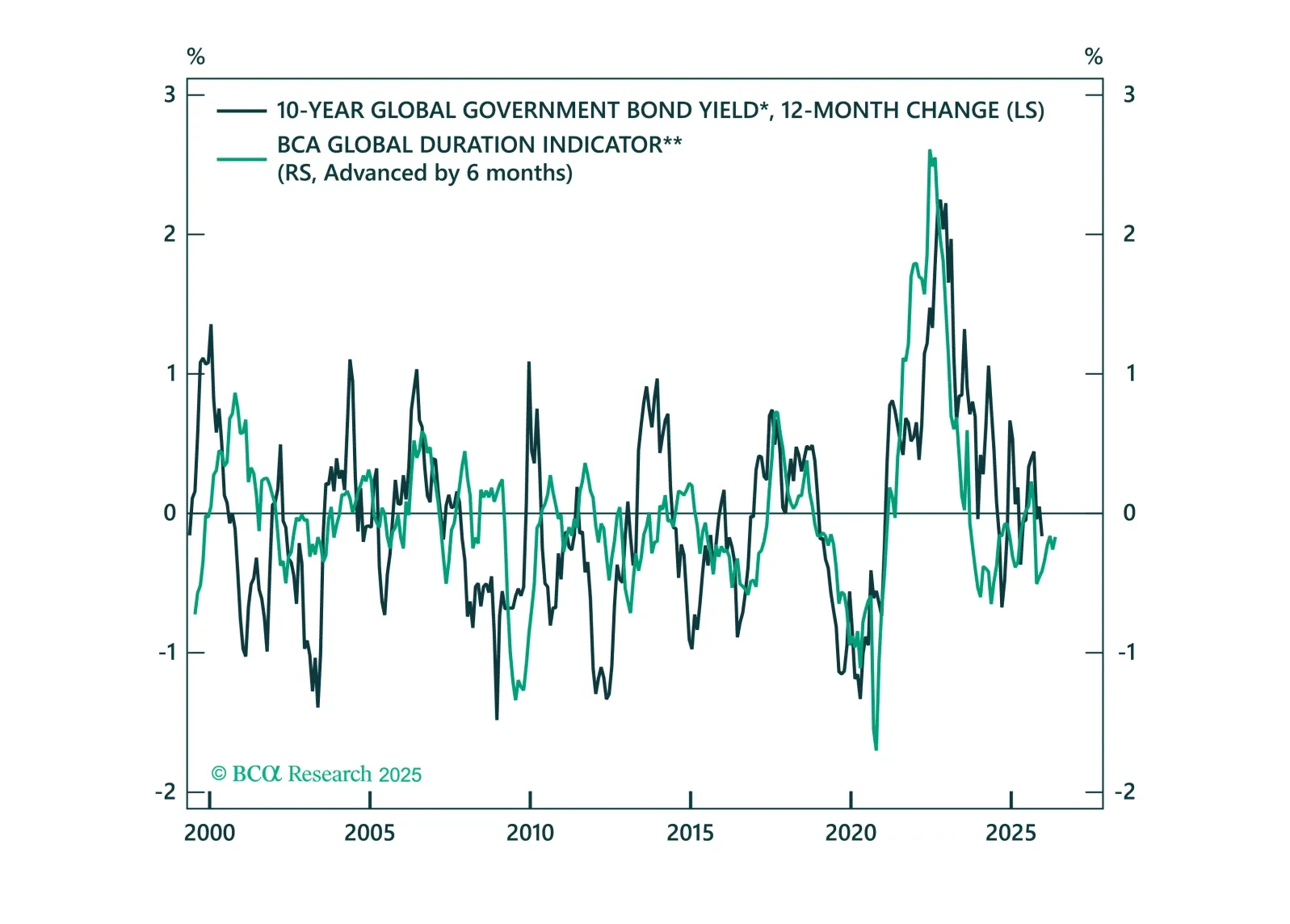

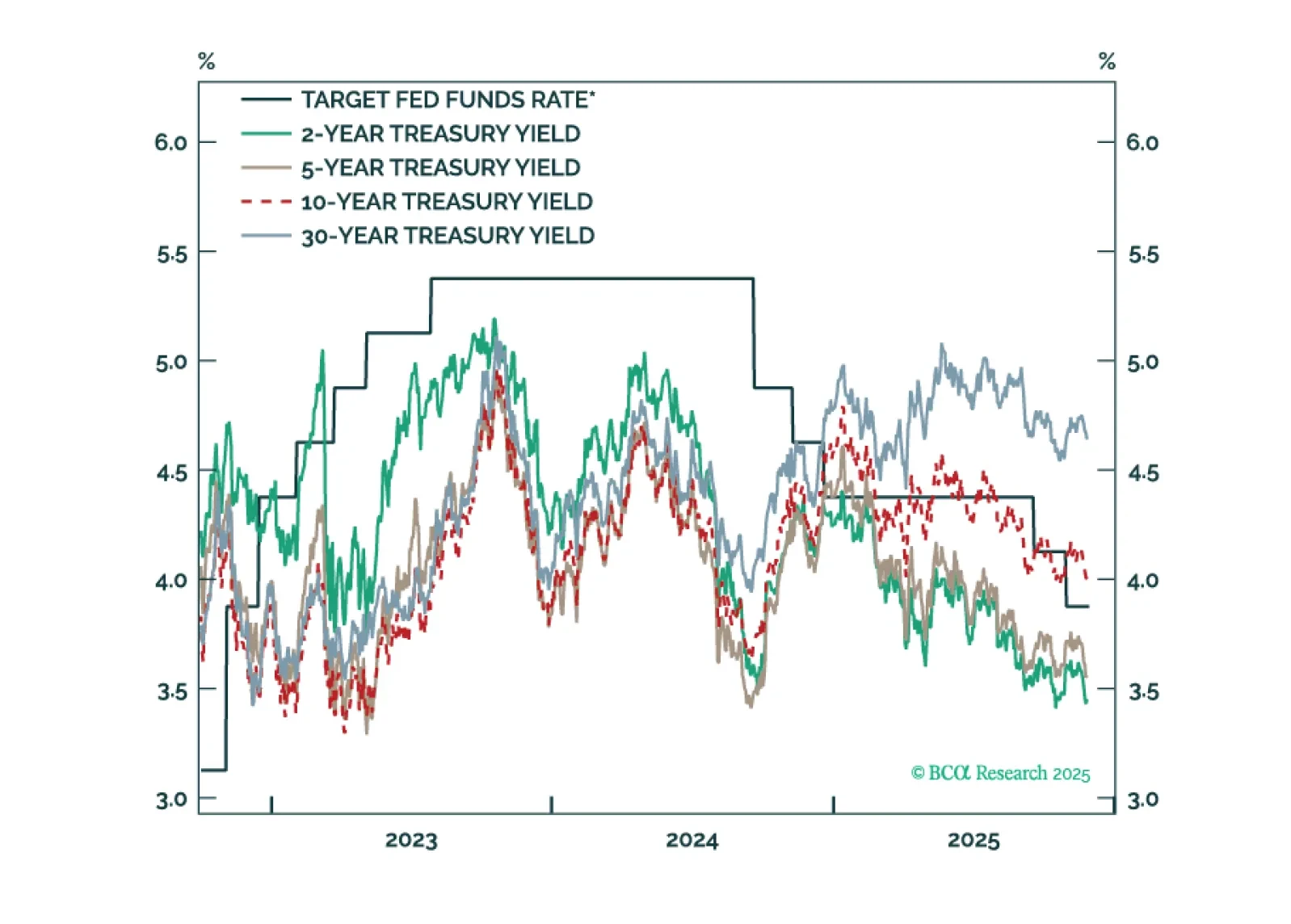

Our key US fixed income views for 2026.

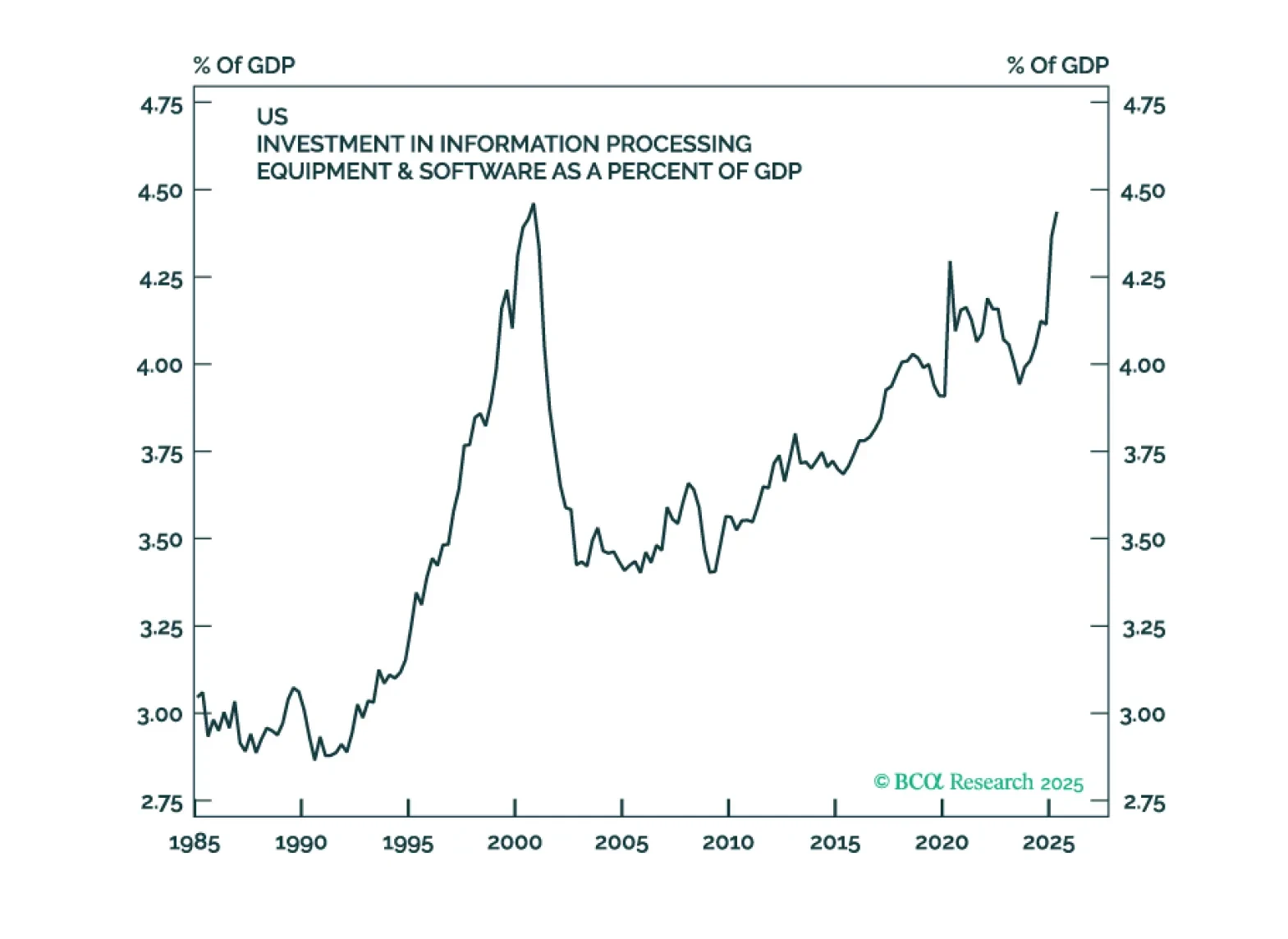

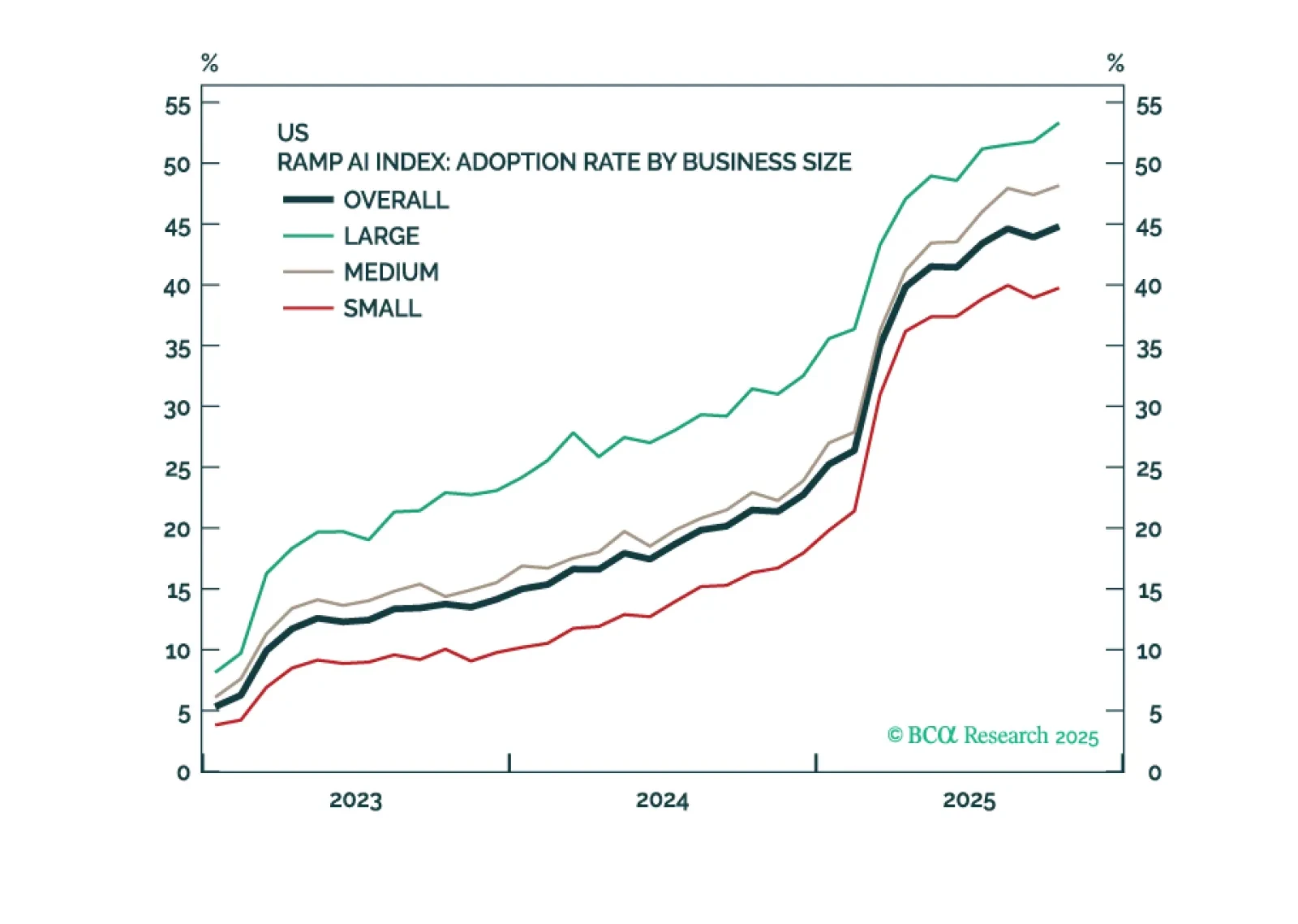

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.

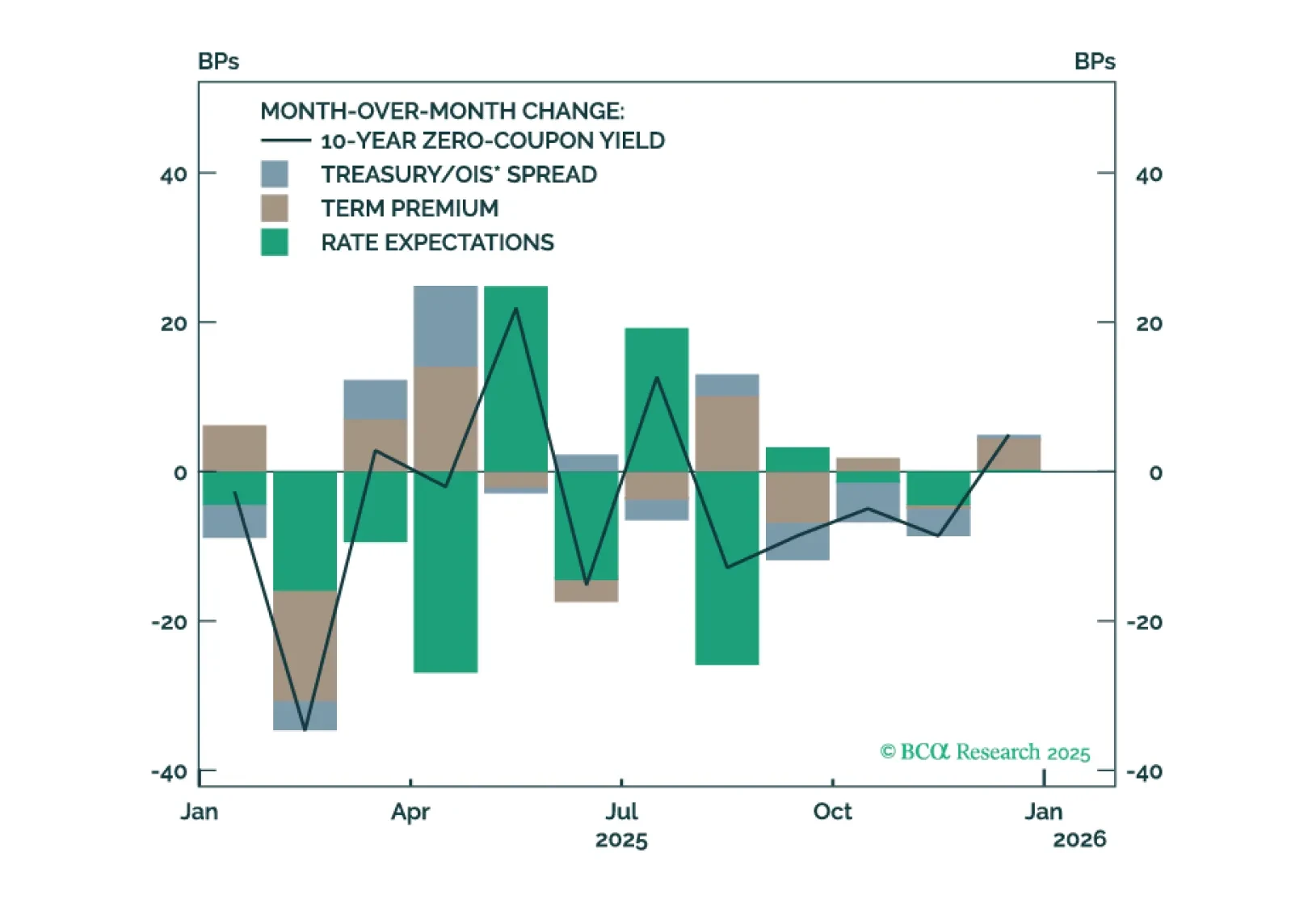

The September employment report probably won’t convince enough hawks to vote for a rate cut in December.