Developed Countries

At its October meeting, the Reserve Bank Of New Zealand (RBNZ) cut the Official Cash Rate by 50 bps to 4.75%. The decision was not accompanied by an updated economic forecast or press conference and the latest forecast in August expected inflation to fall to…

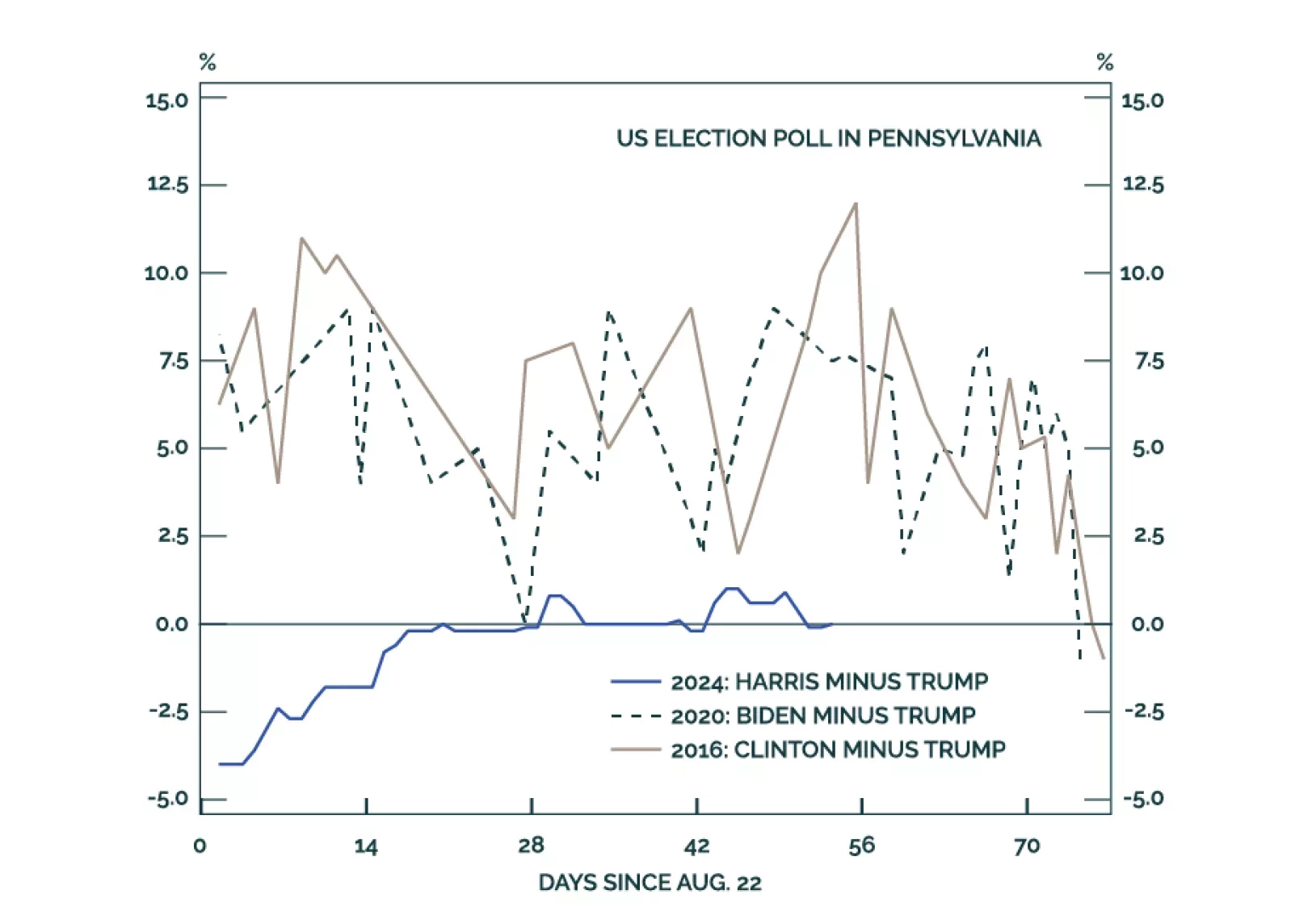

According to BCA Research’s US Political Strategy service, the important election takeaway for investment strategy comes from the Senate. The Senate is highly likely to fall to Republicans. They are nearly certain to win West Virginia and very likely to…

The NFIB Small Business Optimism index was mostly flat in September, ticking a mere 0.3 points higher to 91.5 in September, below expectations of a more meaningful improvement to 92.0. The NFIB Small Business Optimism has oscillated in a tight range since…

Consumer credit growth slowed in August, rising by USD 8.9 bn (to USD 5,097.6 bn outstanding) from USD 26.6 bn, disappointing expectations of a USD 12 bn monthly increase. Notably, revolving credit (which includes credit cards) declined by USD 1.4 bn over the…

The month of October ahead of a US general election tends to be a volatile month with negative outcome for equities. As such, it is prudent to remain on the sidelines until after the election.

The US election underscores three long-term trends of Generational Change, Peak Polarization, and Limited Big Government. Investors should expect more volatility around the election and should assess the results before adding more risk. While we predicted the October surprise from the Middle East, more surprises are coming before the final vote is cast.

German factory orders contracted by a larger-than-anticipated 5.8% m/m (3.9% y/y) in August, from a 3.9% expansion (4.6% y/y). Domestically, Germany is constitutionally bound to maintain a balanced budget. The emergency pandemic funds disbursed in 2020 are…

The Swiss KOF Barometer is a composite leading indicator of the Swiss economy. It surprised to the upside in September coming in at 105.5 against expectations of 101.0. The August reading was also significantly revised higher, from 101.6 to 105.0. …

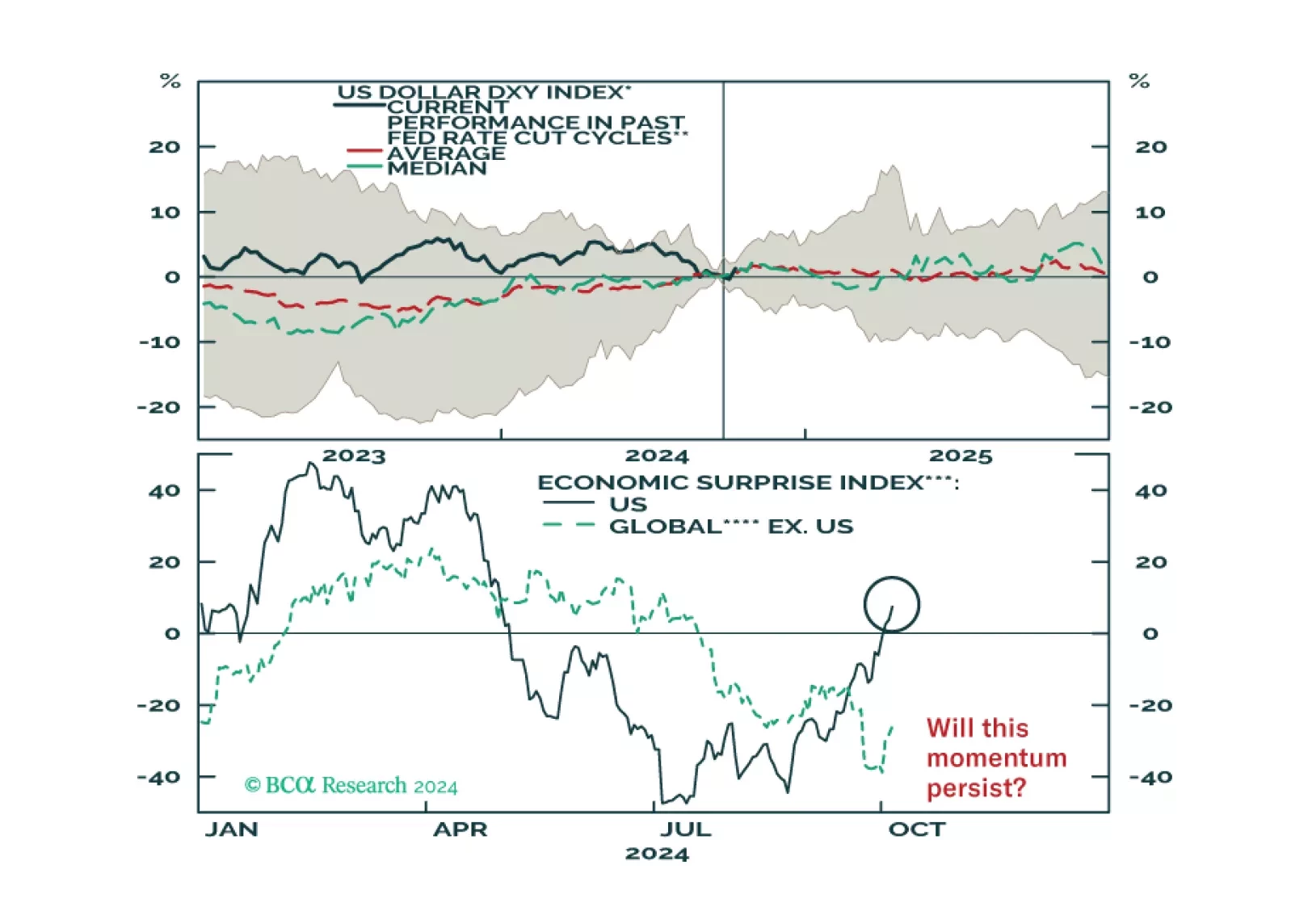

The dollar had erased all of its 2024 gains going into the fall, as markets prepared for Fed rate cuts. After a nearly 6% drawdown over the spring and summer, last week’s DXY rally brought the dollar back into the black YTD. Can these gains continue now…

This report looks at the likely path for the dollar and bond yields over the next 6-to-12 months.