Developed Countries

Our Portfolio Allocation Summary for October 2025.

This week’s US Bond Strategy Special Report takes a look at the two most provocative papers presented at last month’s Jackson Hole conference.

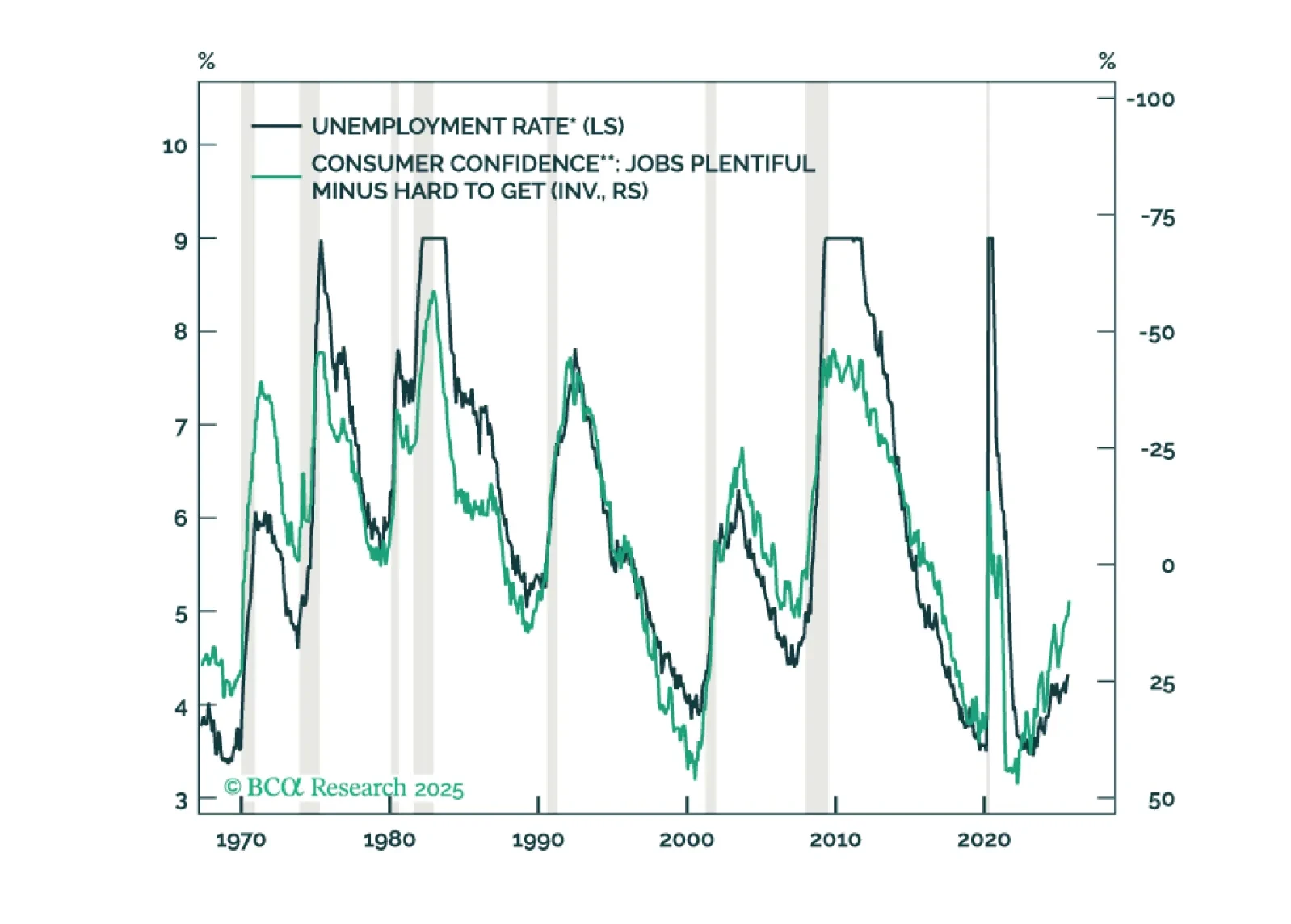

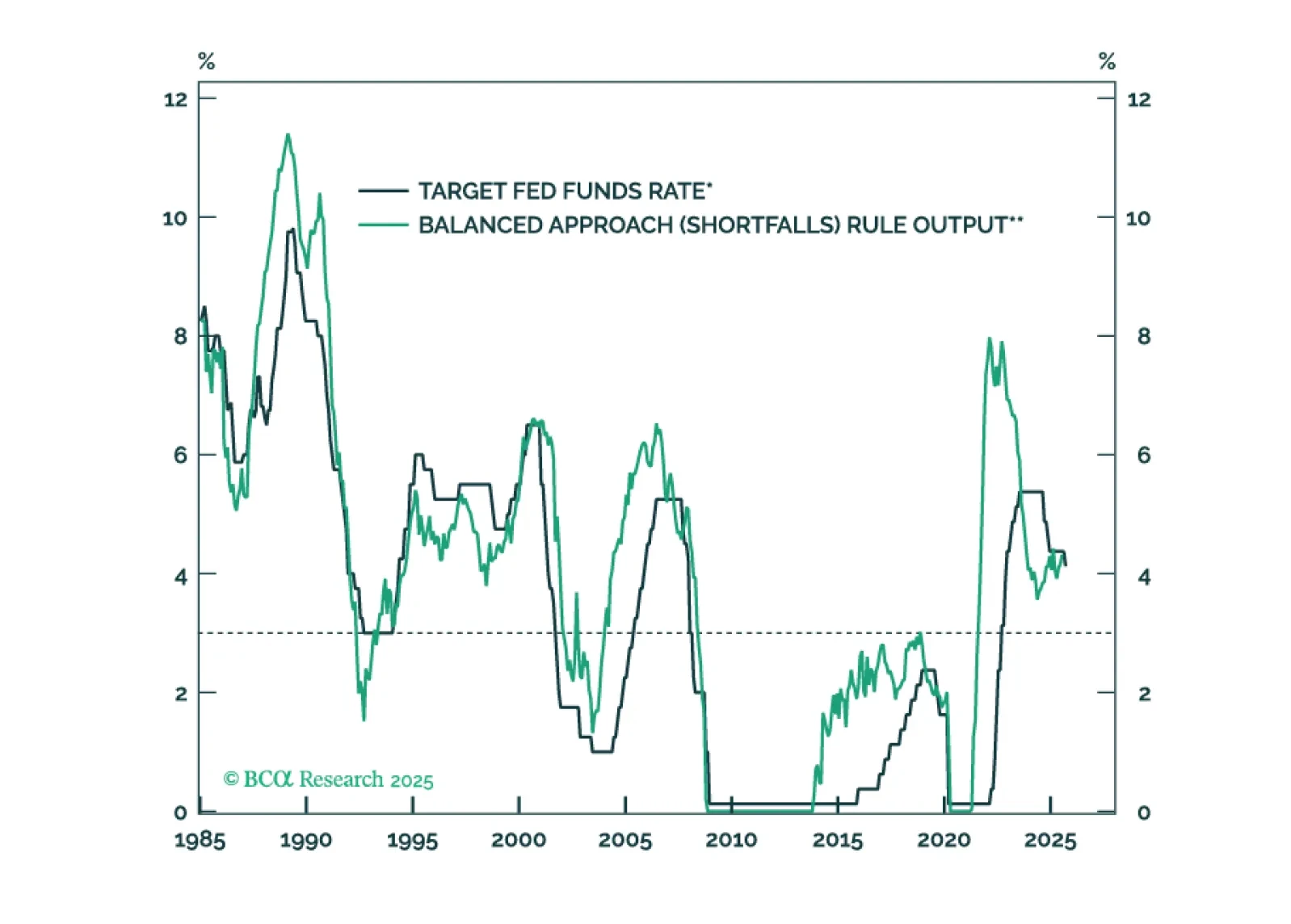

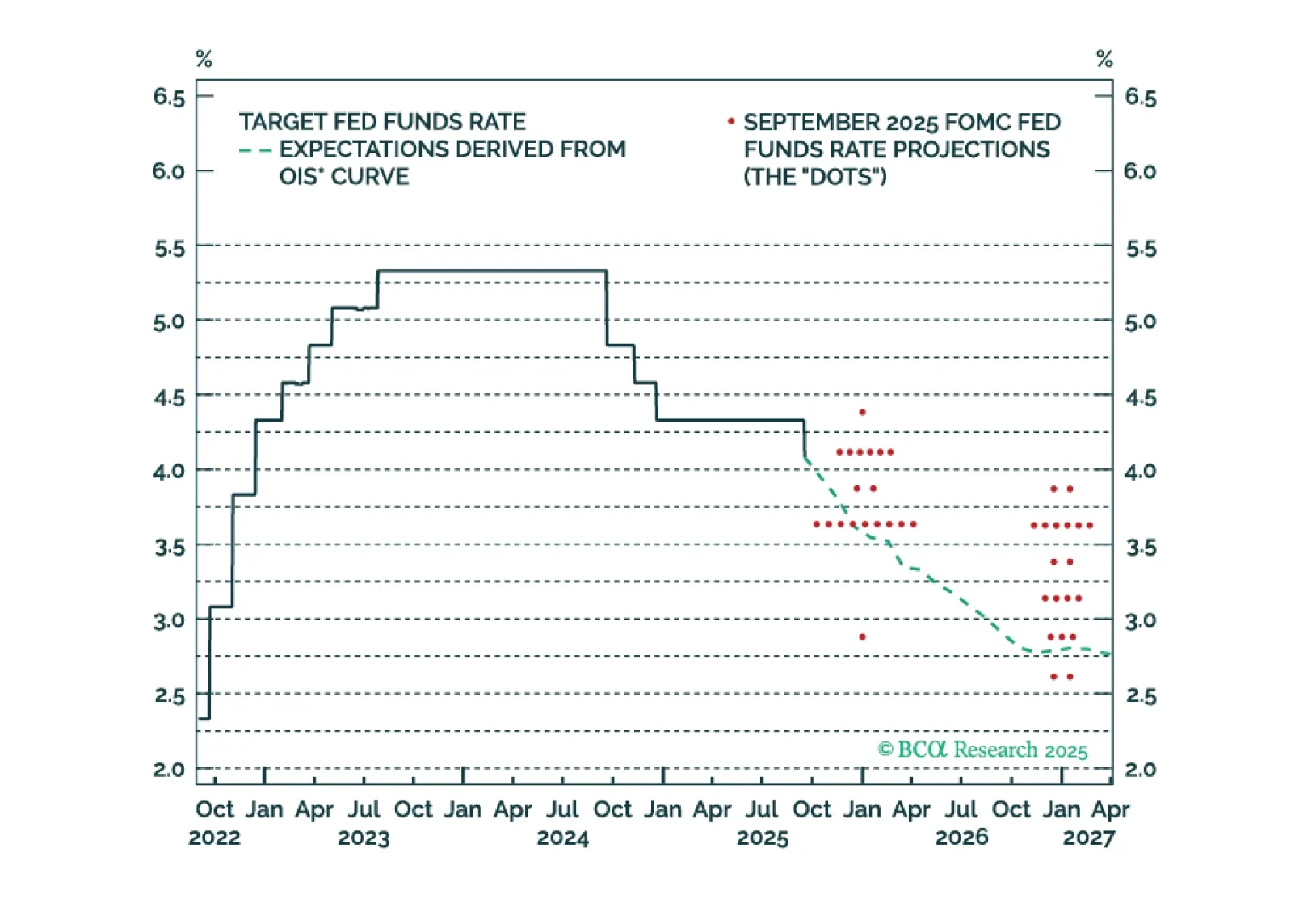

Median Fed unemployment rate projections are overly optimistic. The Fed will end up cutting more in 2026 than it currently anticipates.

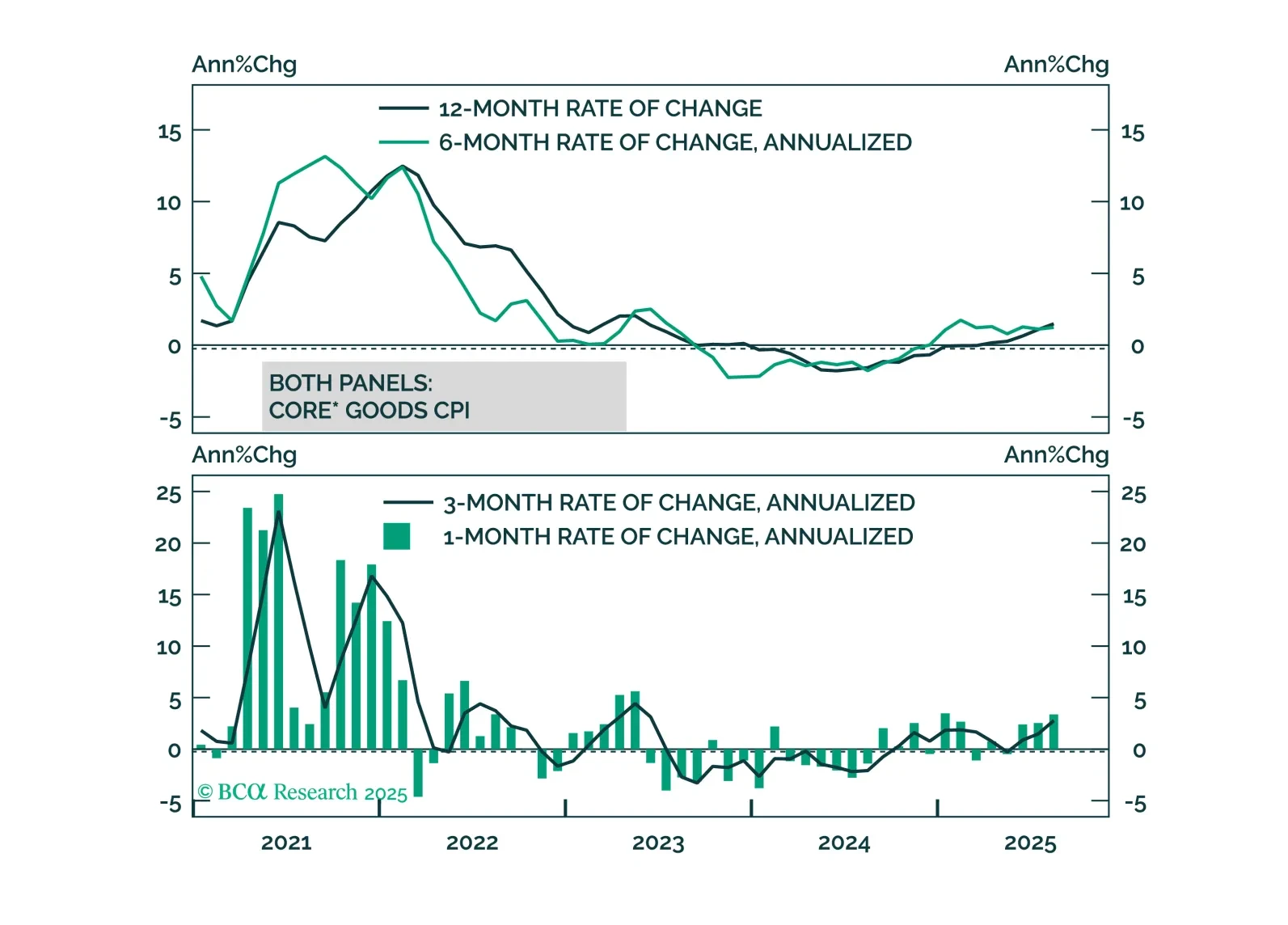

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

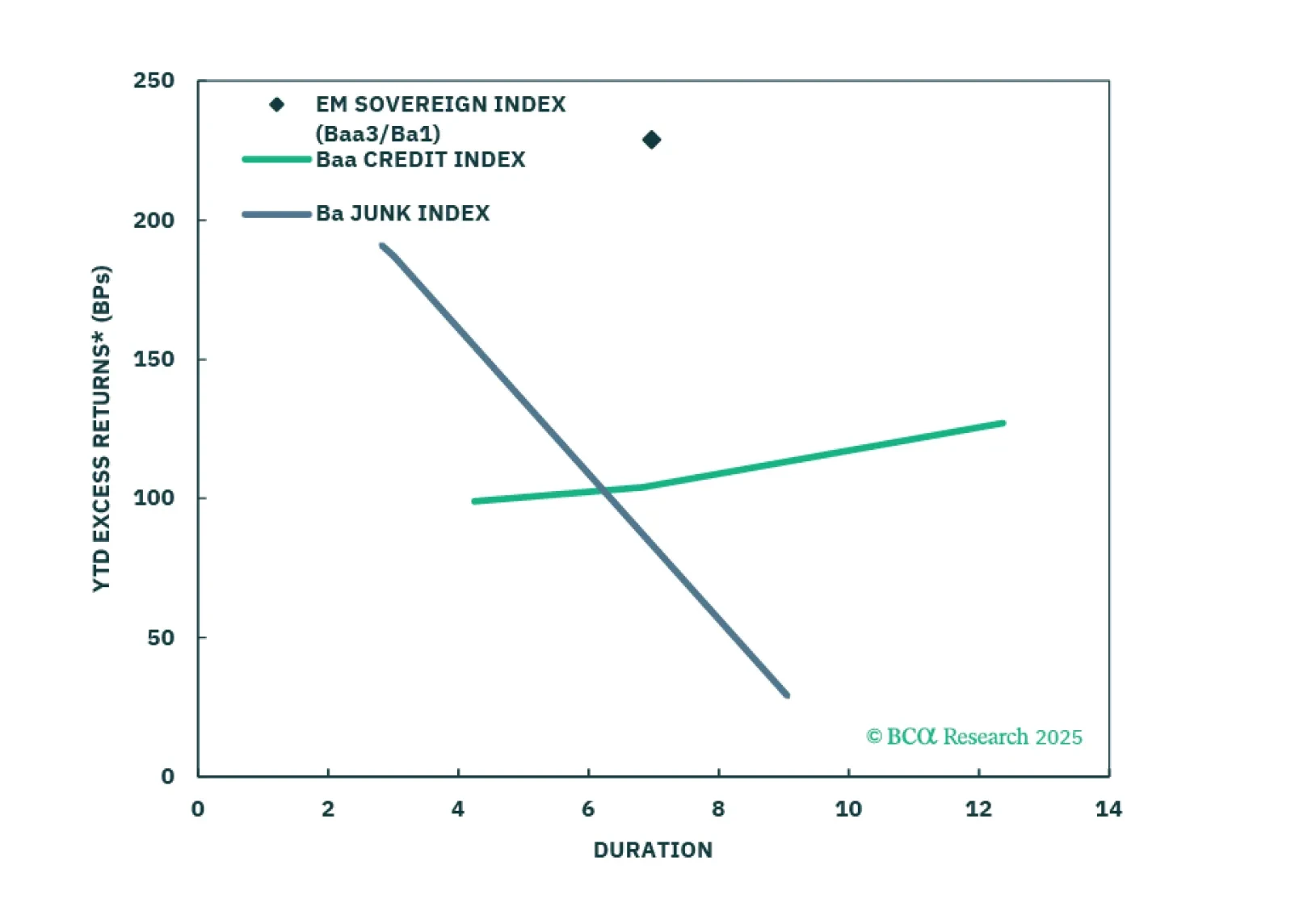

USD-denominated Emerging Market bonds have been outperforming US corporates for the past year. We don’t think the rally is exhausted yet.

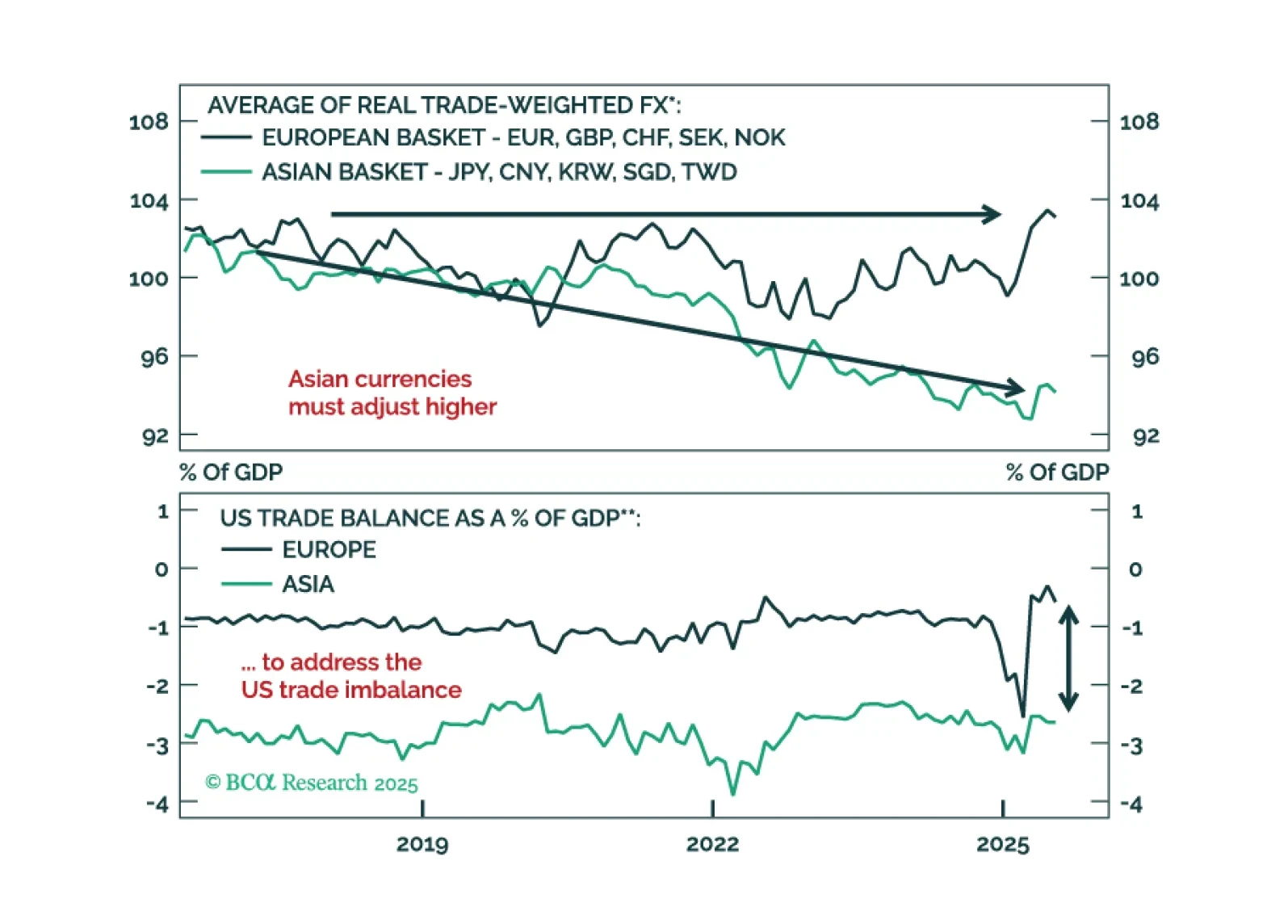

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

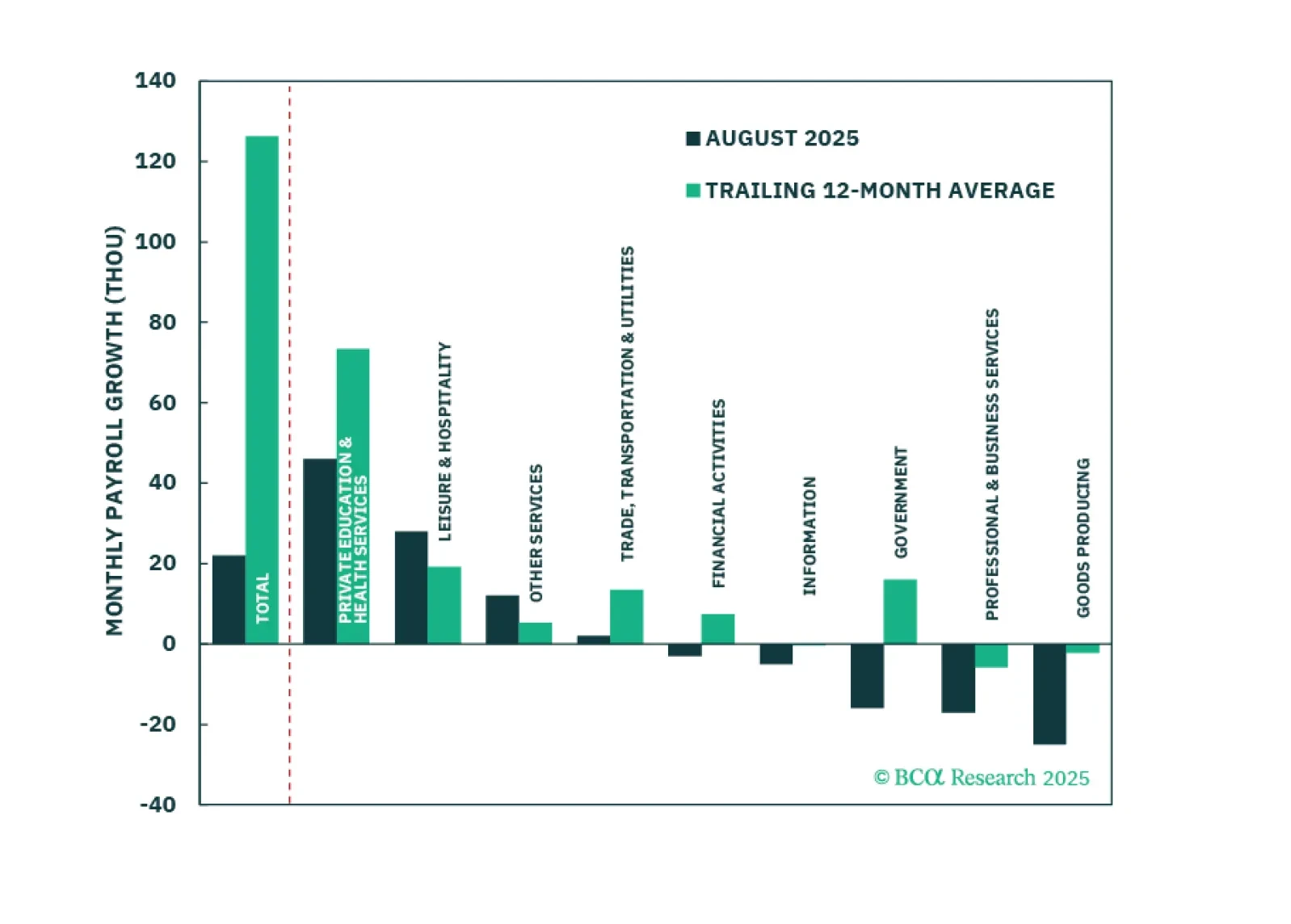

The August employment report showed a modest increase in labor market slack, enough to cement a 25-basis-point rate cut this month.

Our Portfolio Allocation Summary for September 2025.

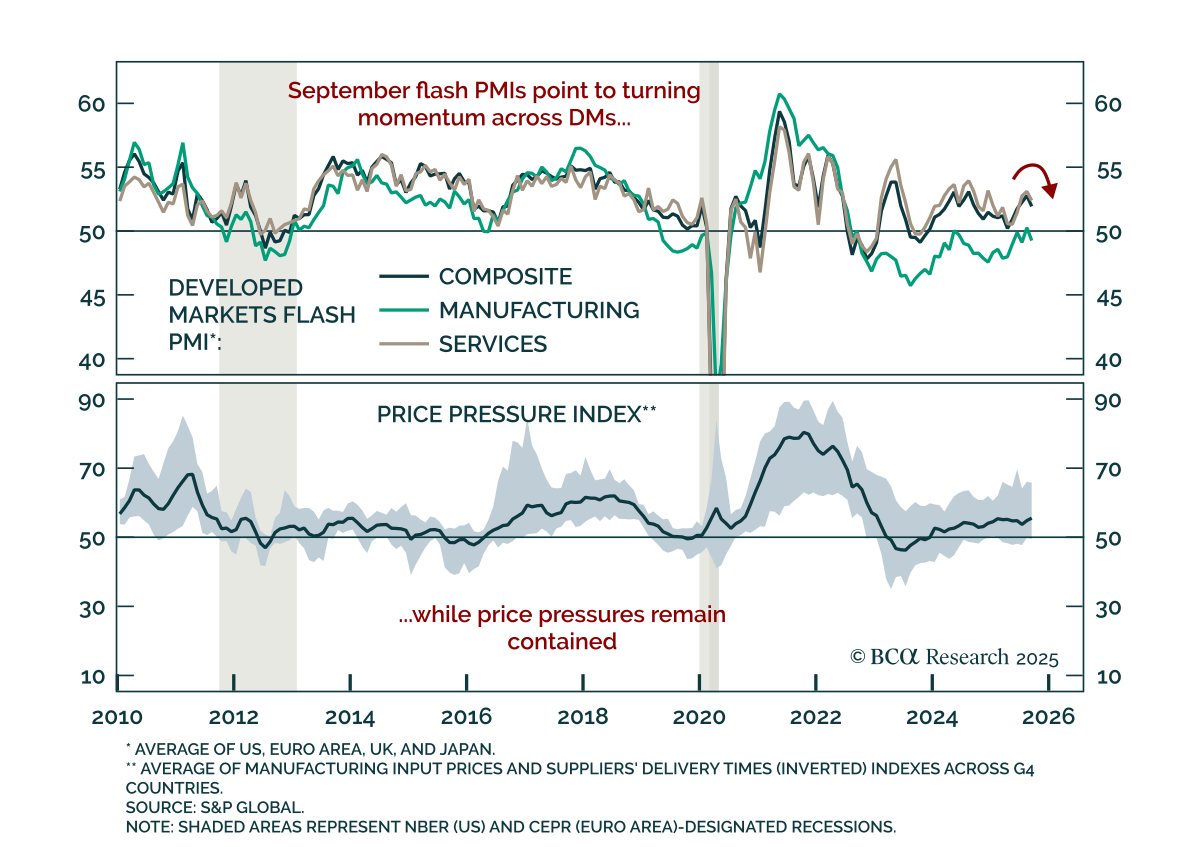

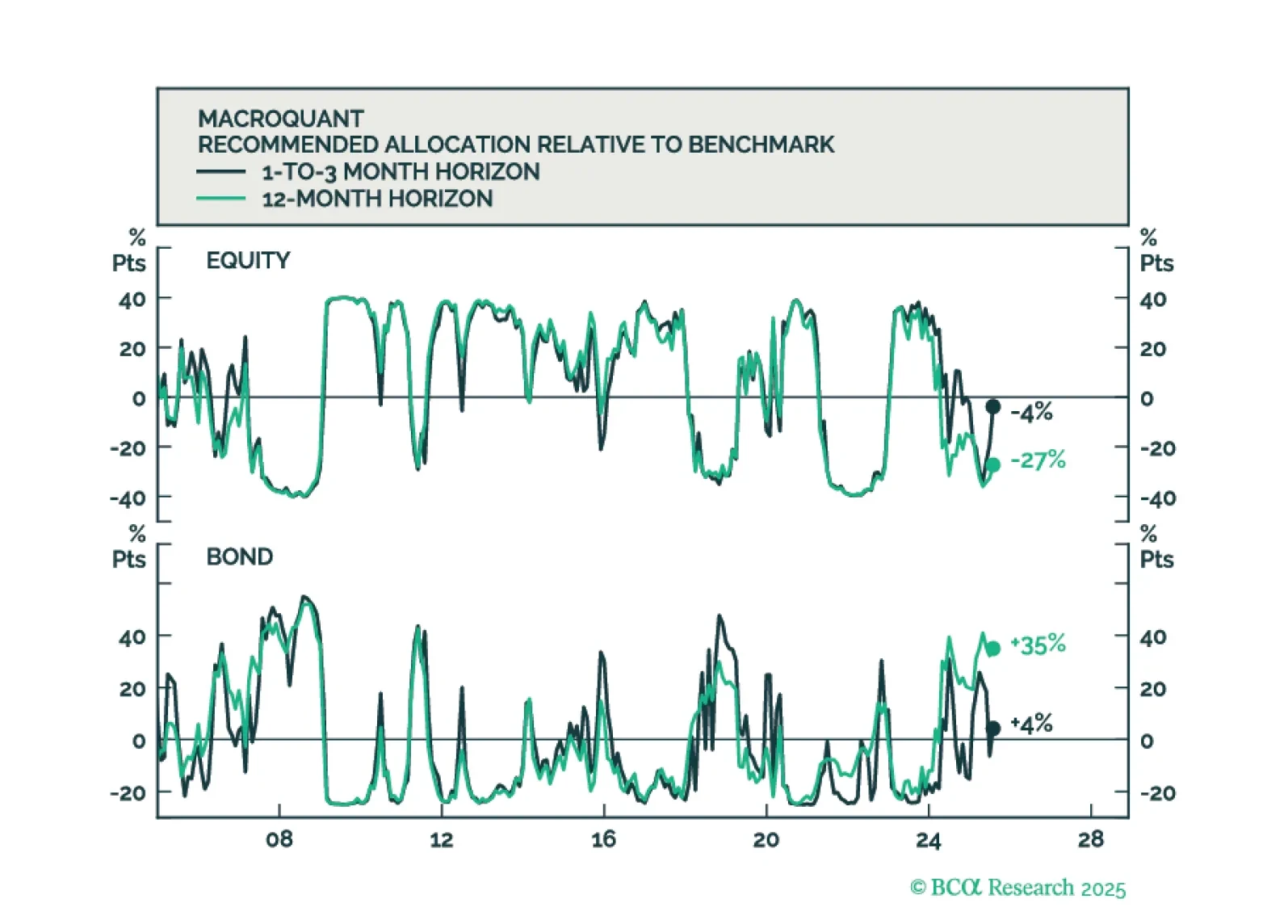

MacroQuant sees downside risks to stocks over a long-term horizon but is not yet saying that we are at imminent risk of an equity bear market.