Developed Countries

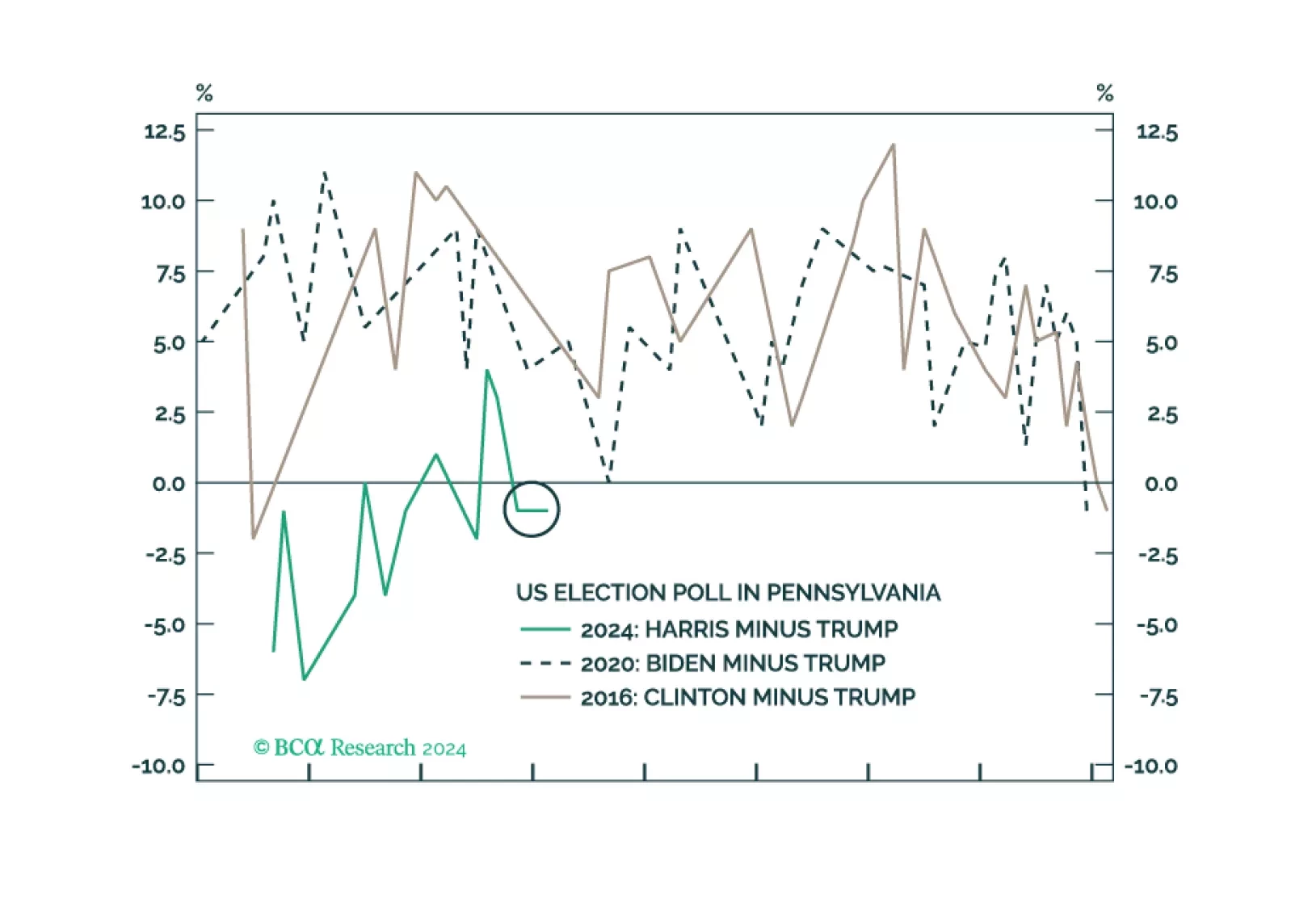

According to BCA Research’s Geopolitical Strategy service, the logic of pursuing one’s interest against US interests in the final hours of the election mostly applies to states that will suffer a significant loss to their strategic security if the…

The Bureau of Labor Statistics (BLS) revised down the number of workers on payrolls by 818 thousand over the twelve months period ending March 2024. This largest downward revision since 2009 thus implies that the labor market has been far less resilient than…

We’ve highlighted that continued deterioration in consumer fundamentals will tip the US economy into a recession. Slower compensation growth, tighter lending standards for consumer loans and dwindling excess savings will constrain spending in an economy where…

According to Goldman Sachs’ Financial Conditions Index (FCI) financial conditions have become considerably more supportive since the fall of 2023. More recently, the index ticked noticeably lower from 99.4 earlier in August to 98.8. US equities have indeed…

The DXY hit a 2024 low on Wednesday. The decline which totaled nearly 5% from its April highs, gathered pace this month (a 3% decline in August) when labor market worries spooked markets. The Fed had already telegraphed it was getting closer to cutting…

According to BCA Research’s Foreign Exchange Strategy service, the domestic economy does not really explain the recent weakness in the Norwegian krone. Some of this weakness can be attributed to structural and idiosyncratic factors, one being persistent…

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.

Canadian headline CPI decelerated from 2.7% y/y to 2.5% in July, the slowest pace in over 3 years. Notably, core median and trimmed-mean CPI eased further than expected, to 2.4% and 2.7% y/y respectively, 0.1 ppt below anticipations. Lower prices for…

In a widely expected move, the Riksbank lowered its policy rate from 3.75% to 3.5% in August. It had kept rates on hold in June, after having led many other major DM central banks in easing policy in May. The Riksbank also signaled it could cut as many as…

It didn't take long for markets to utterly shrug off the surprise rise in July's unemployment rate. On Tuesday, the S&P 500 closed higher than it was the day before the July Employment Situation report was released. The Russell 2000 gained 5.2% since…