Developed Countries

At first glance, France has moved to the far left. However, this coalition is fragile, and Macron’s allies still hold the balance of power. What are the assets that will benefit from this new political setup, and those that will not?

Although we ticked a second box on our checklist, the incoming data still do not indicate that a recession is imminent. We remain tactically equal weight equities with a strong bias to underweight them, but we’re not exiting the party just yet.

In this week's report, we review the impact of political developments, as well as incoming fundamental data, on our positioning.

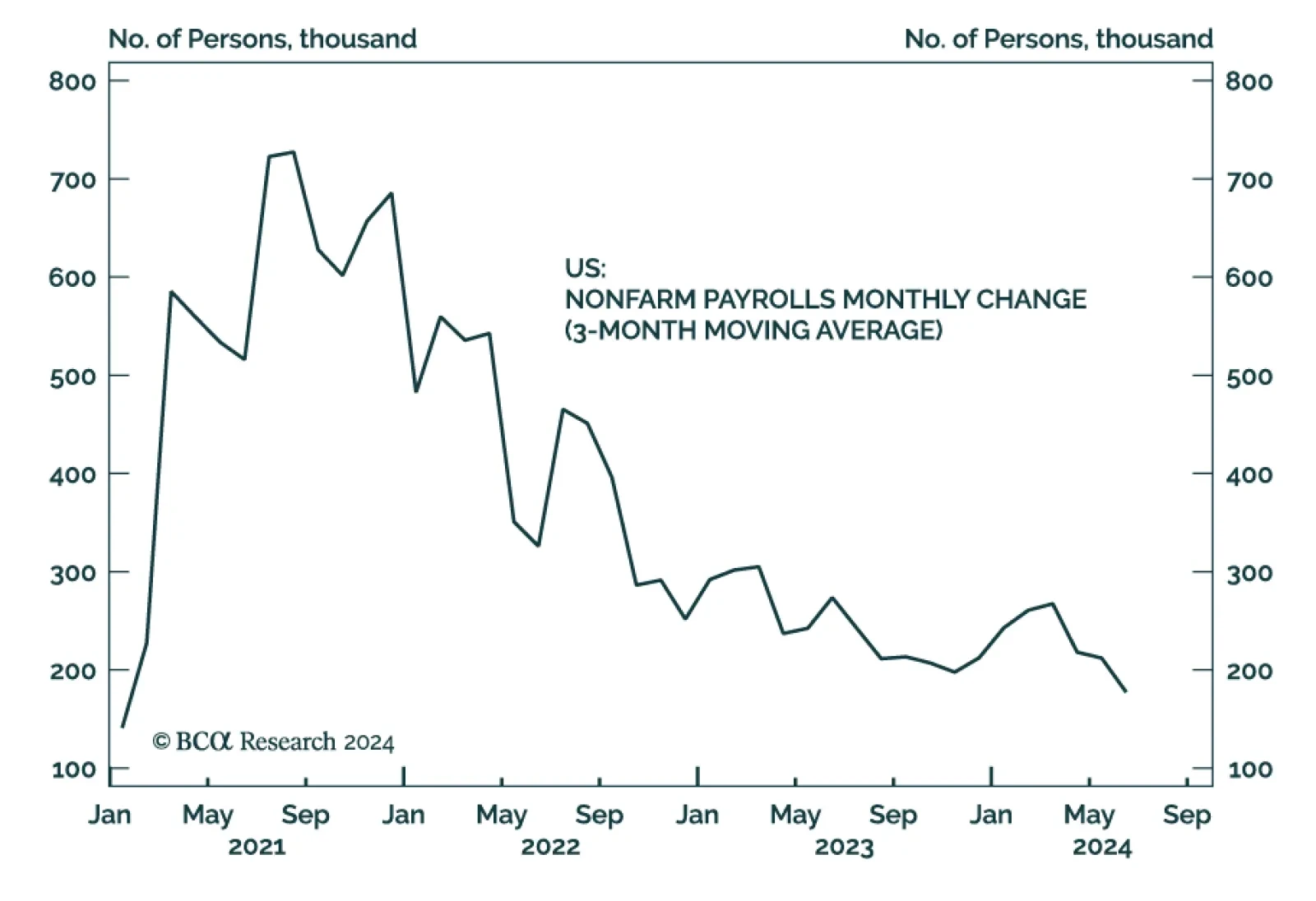

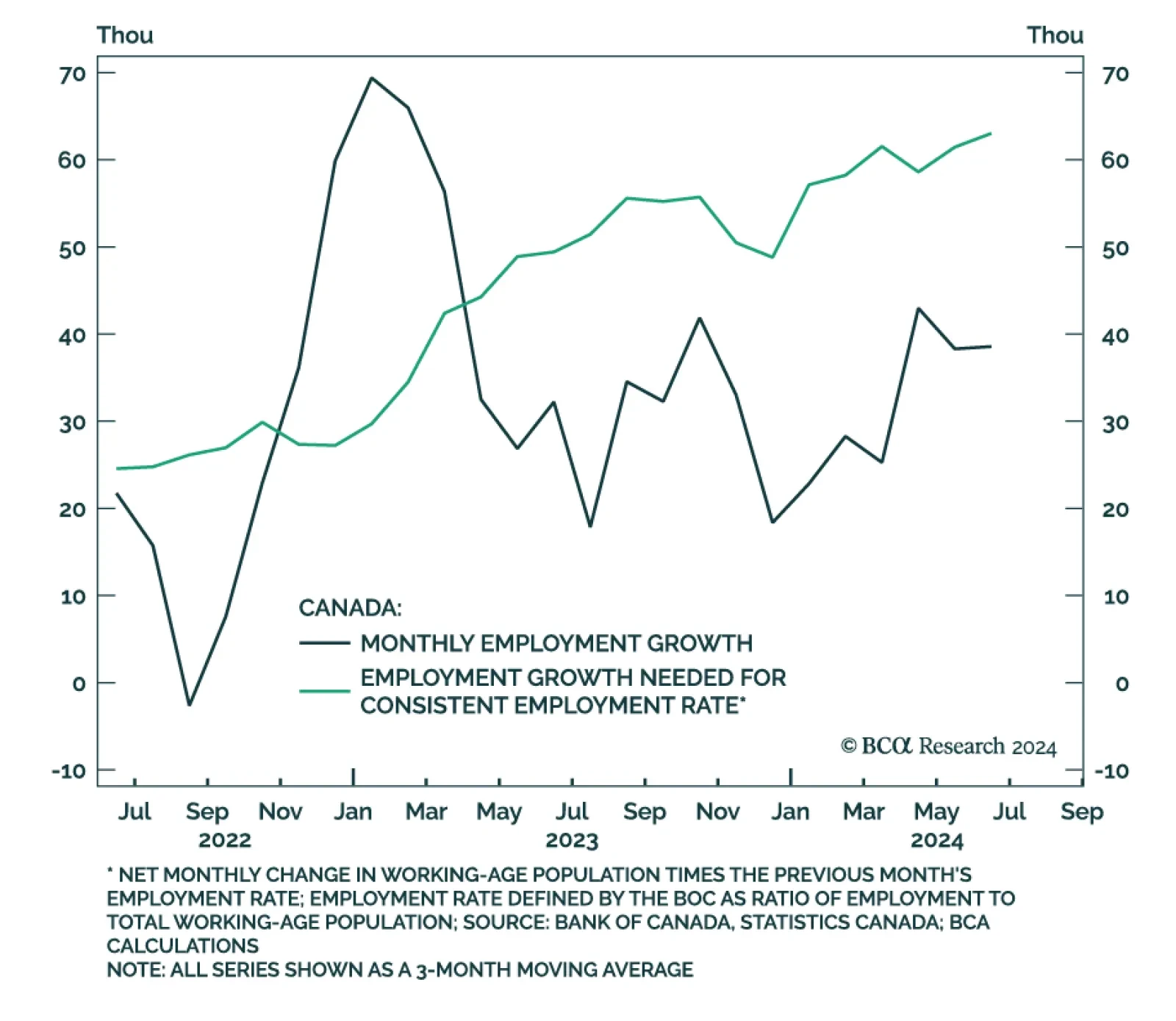

Our labor market indicators have softened meaningfully during the past month but aren’t yet signaling an imminent recession. That said, the Fed can no longer ignore the labor market with the unemployment rate above 4% and rising.

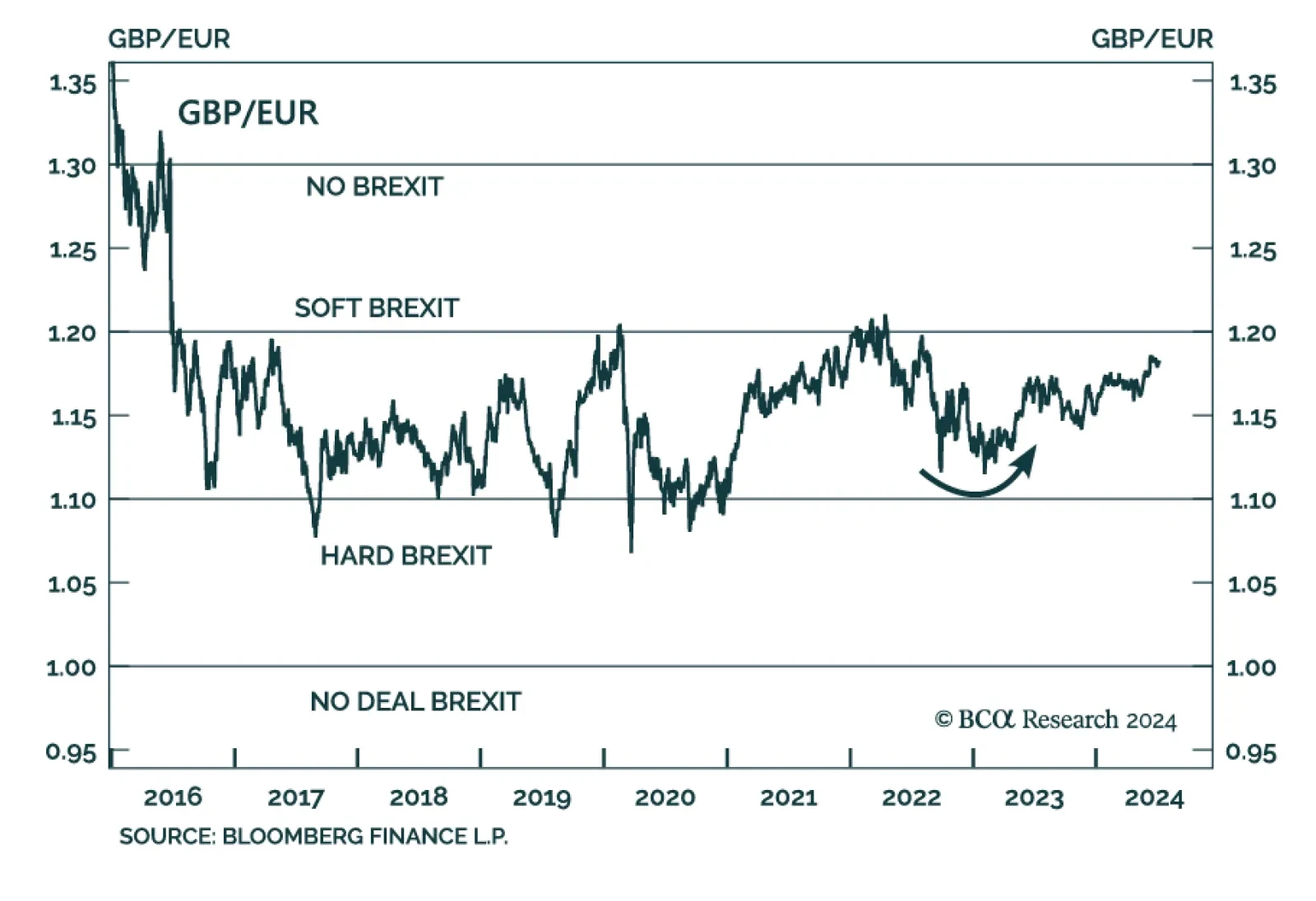

The new Labour government will have flexibility to respond to macro shocks, which is positive for the UK in general, namely GBP-EUR, and also gilts in absolute terms. But over the long run, tax hikes will likely surprise to the upside, which poses a risk to corporate earnings.