Developed Countries

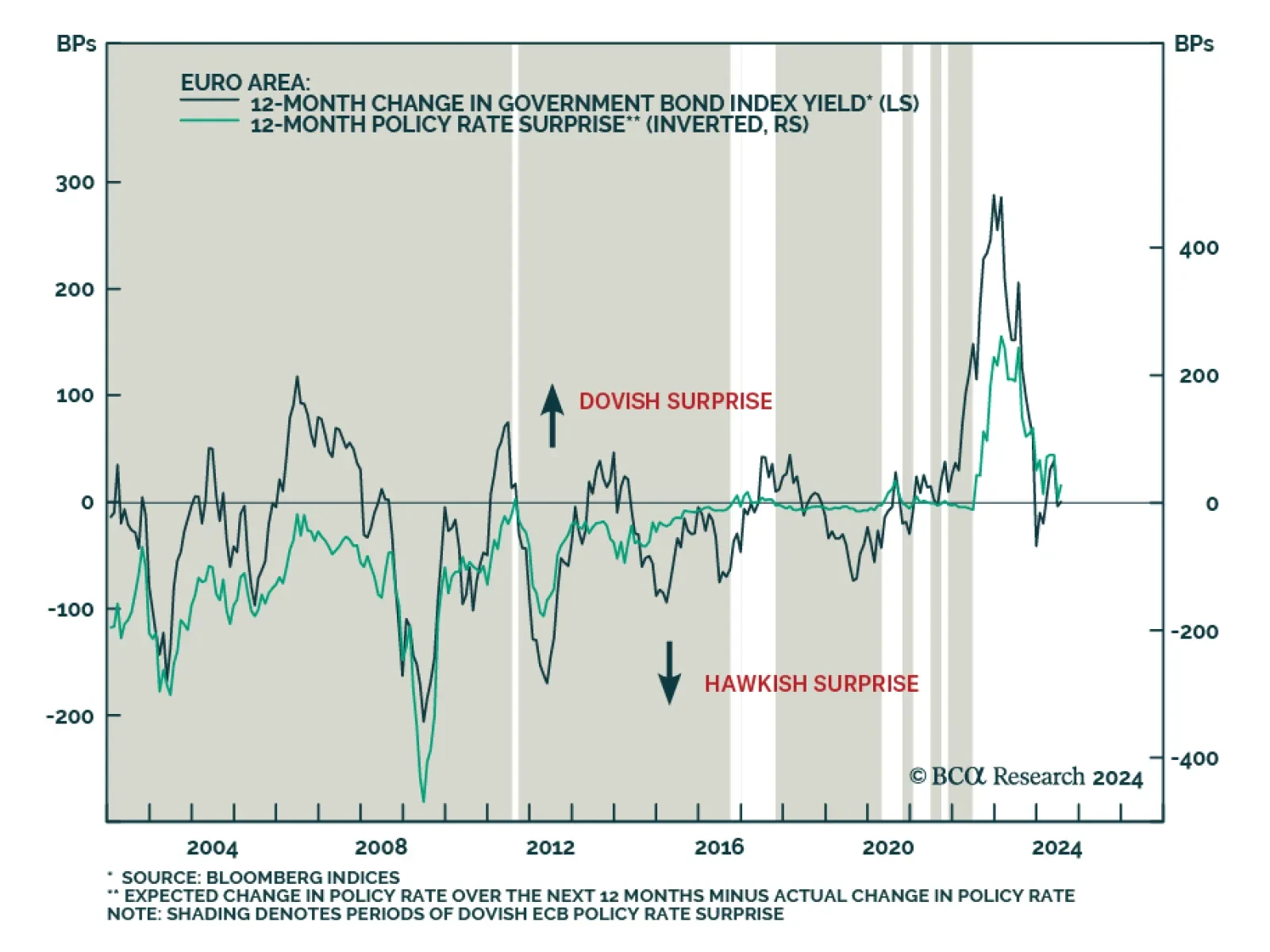

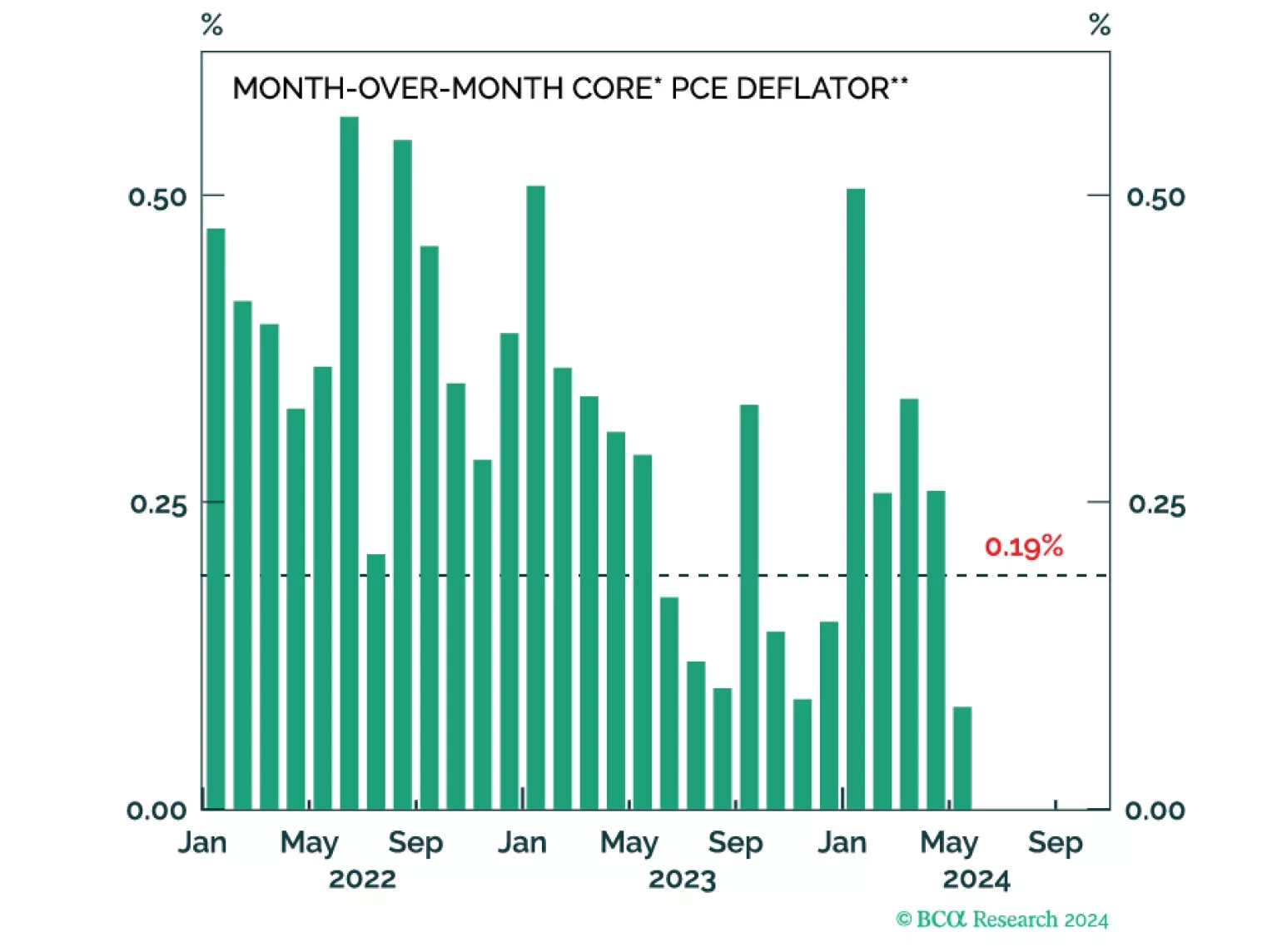

Eurozone headline inflation slowed from 2.6% y/y to 2.5% in June. Germany, its largest economy, saw price pressures ease from 2.4% to 2.2%, below expectations of 2.3% (or from 2.8% to 2.5% on an EU-Harmonized basis). However, Euro Area core inflation…

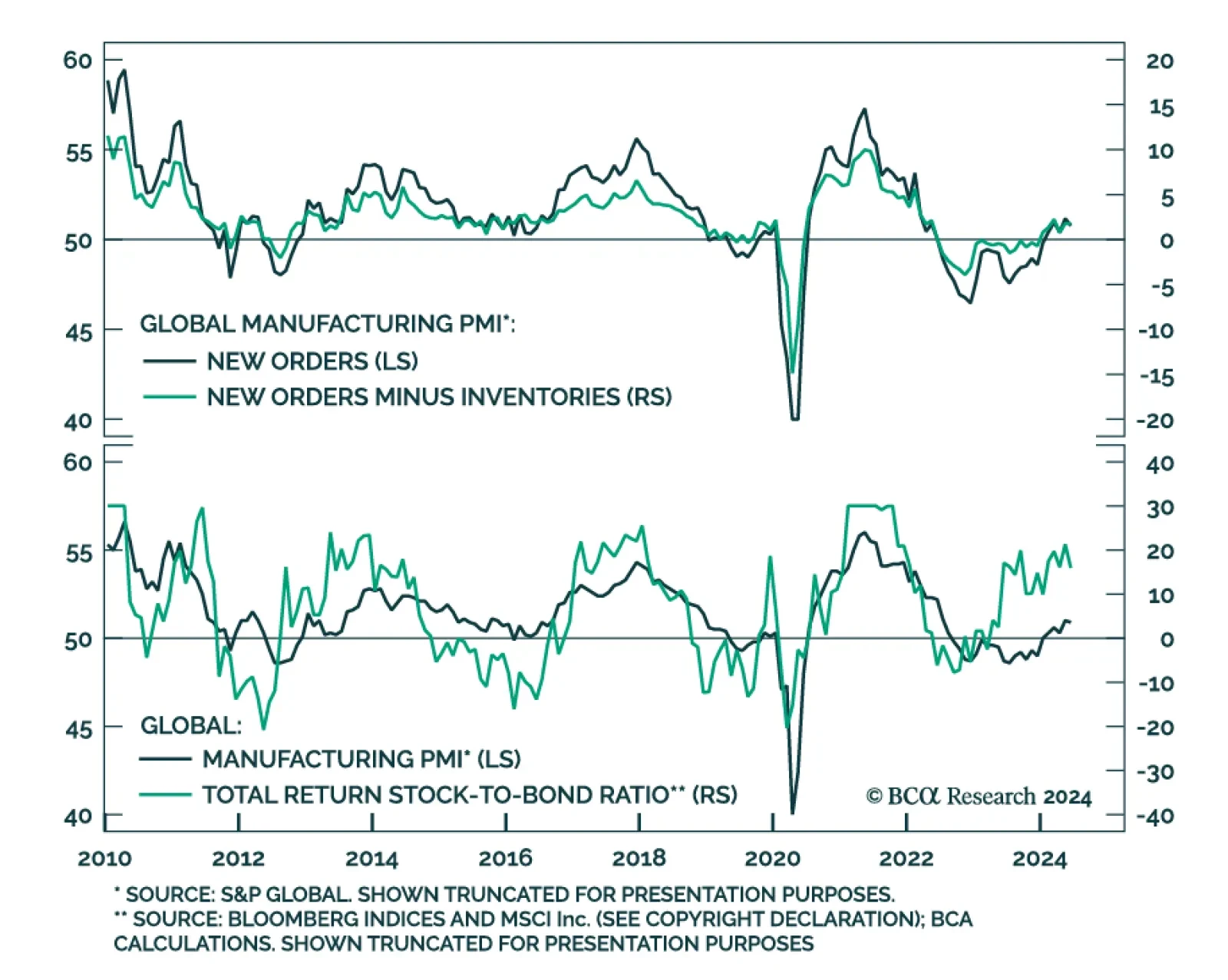

The stabilization in global growth continued in June. The JPM Global Manufacturing PMI came in at 50.9, nearly in line with May’s 22-month high. However, international trade flows deteriorated notably. The new export orders component started contracting in…

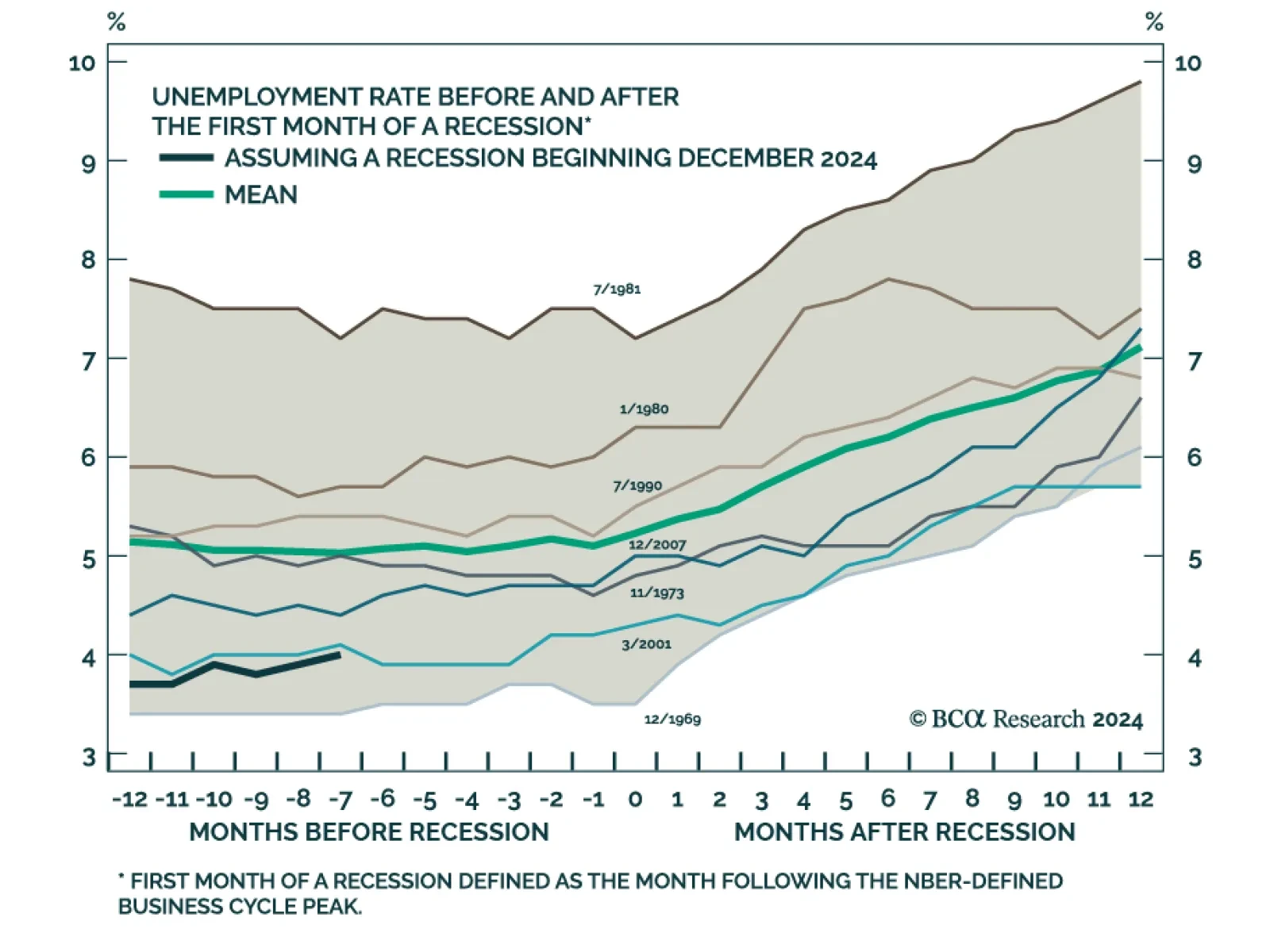

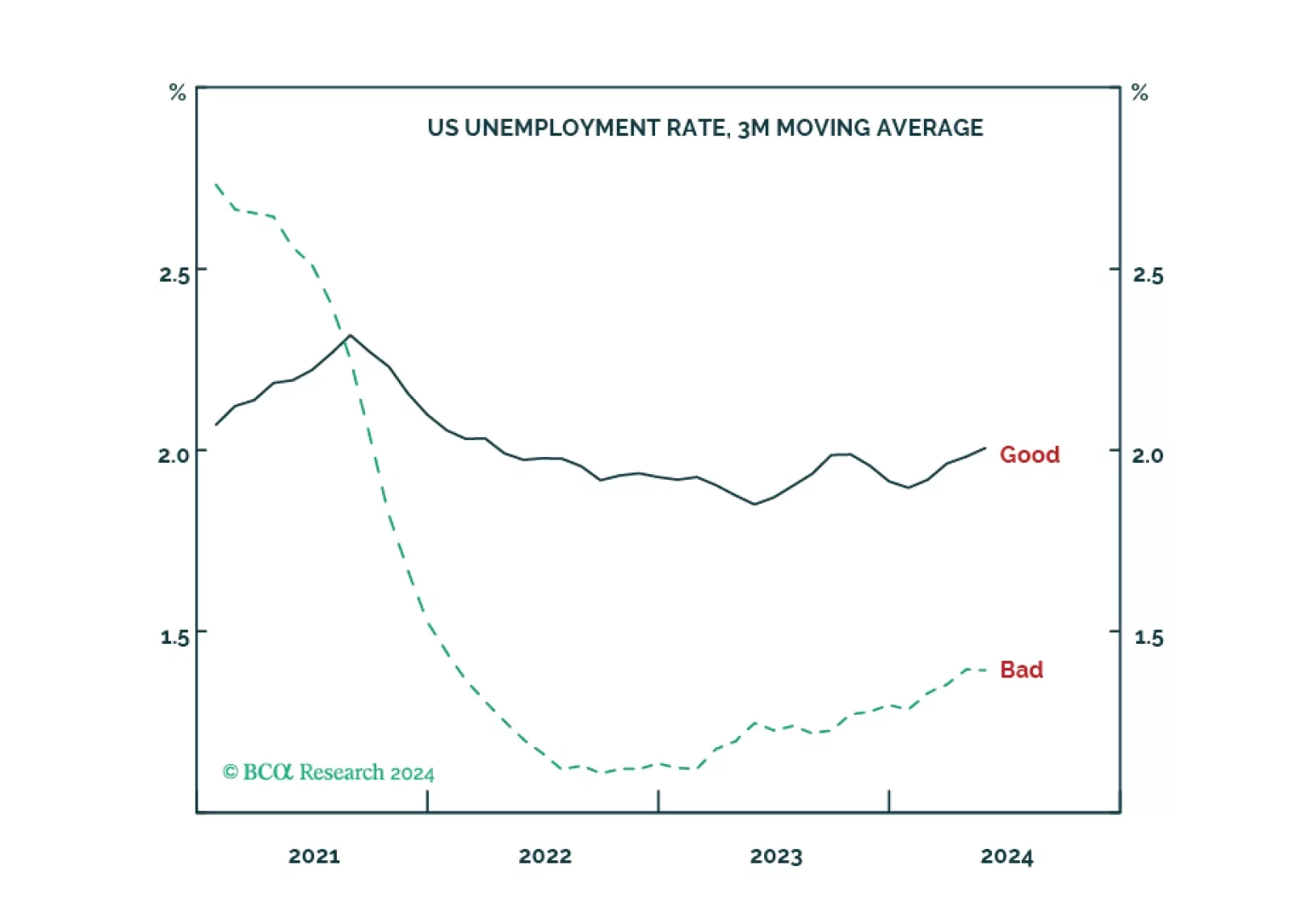

The US unemployment rate stands at just 4.0% today following 27 consecutive sub-4% readings. Does this low unemployment rate guarantee a soft landing in the US economy? Our Global Investment Strategy (GIS) team’s base case is that the US economy will fall…

The ISM Services PMI largely disappointed in June. The headline index plunged from 53.8 to 48.8, its fastest pace of contraction since May 2020, far below expectations of 52.7. This series can be noisy and the June update merely reversed a surprise surge…

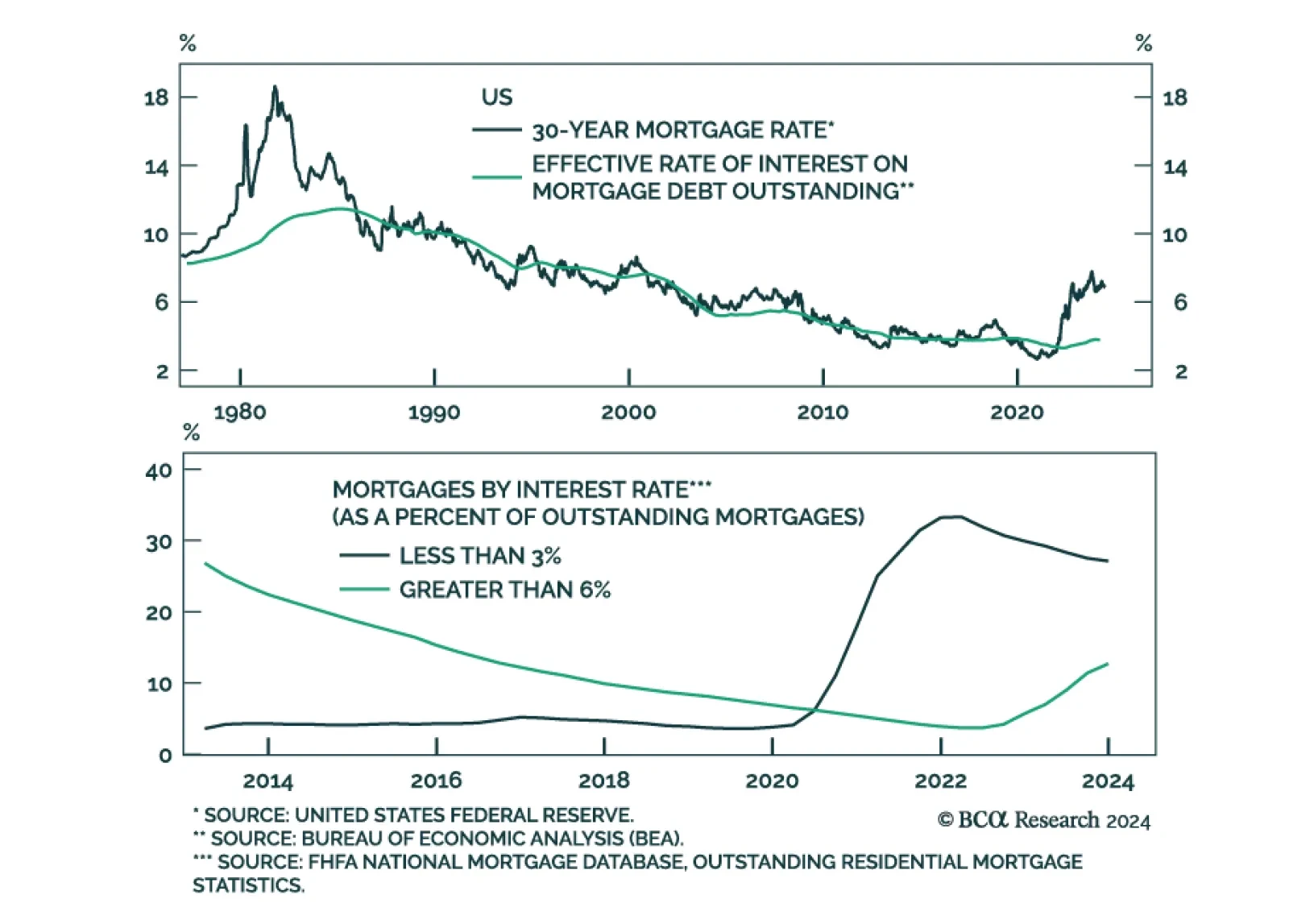

The US conventional 30-year mortgage rate climbed back above 7% in late June and drove a 2.6% weekly contraction in mortgage applications. The fixed-rate home affordability index sank to a nearly four-decade low. Housing is one of the most interest-rate…

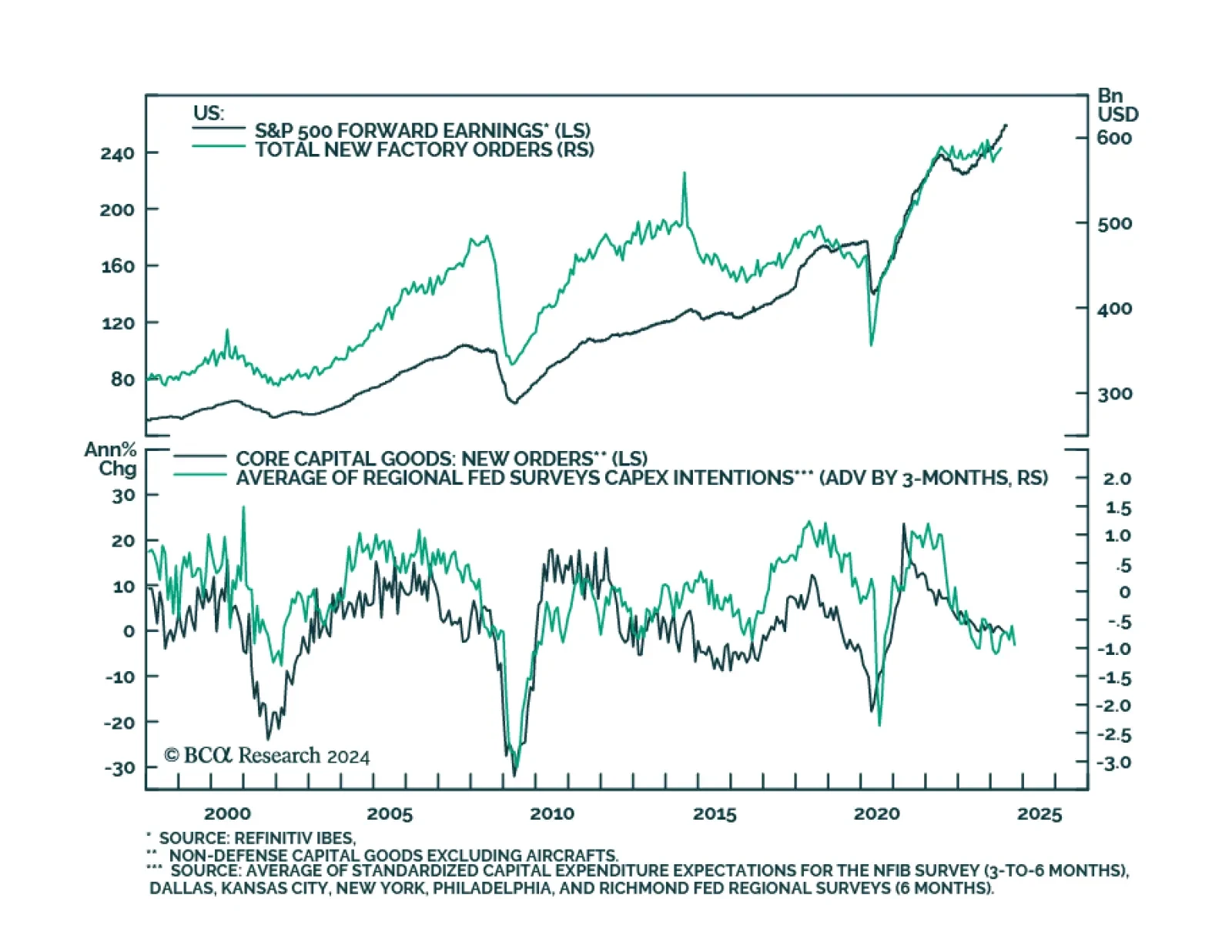

US durable goods orders grew by 0.1% m/m in May, a tick below April’s pace, and upending preliminary expectations they would decline by 0.5%. Moreover, the contraction in core capital goods shipments (an input into the calculation of GDP) was revised lower…

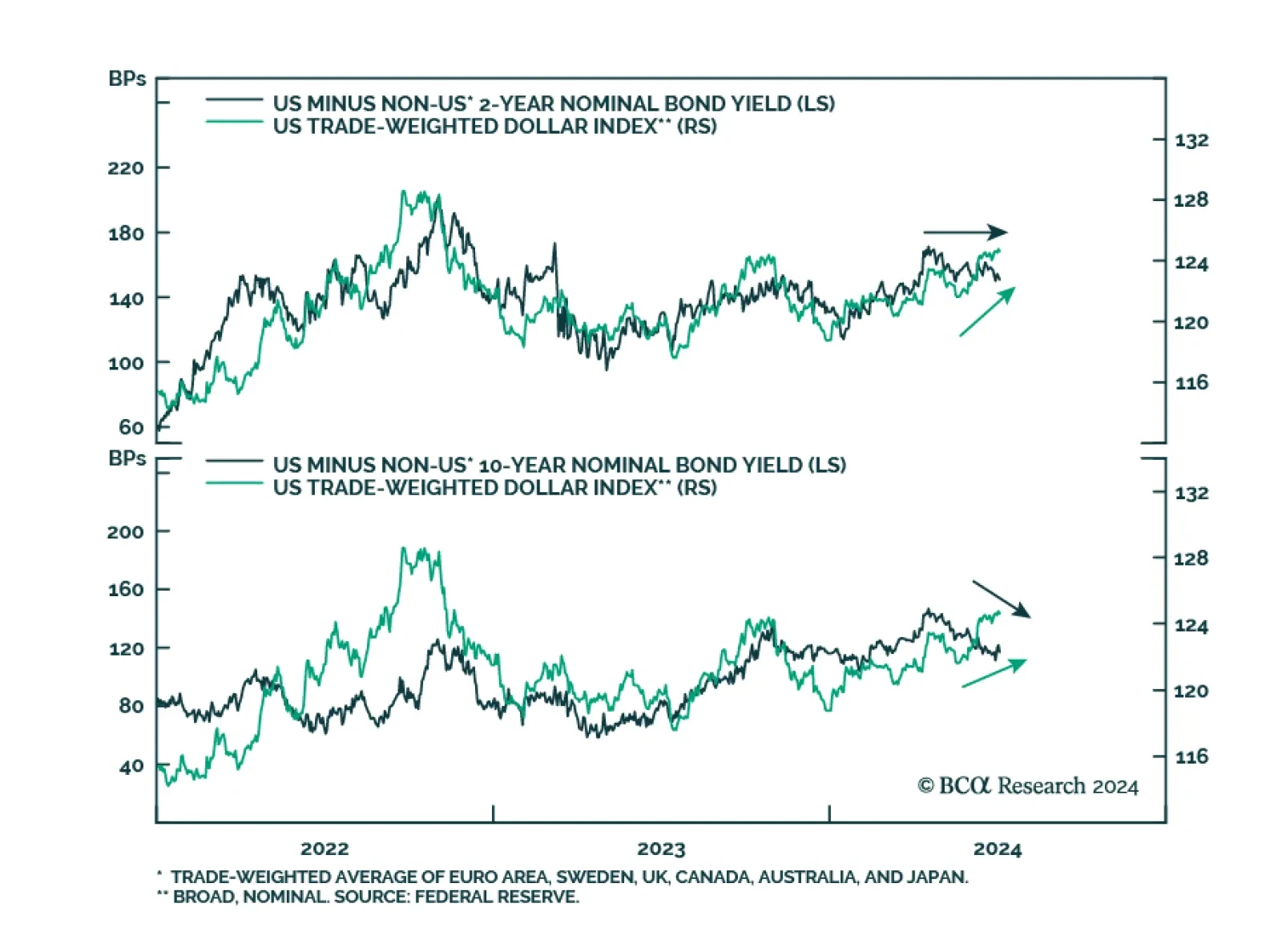

The trade-weighted US dollar ranked among the top performing major asset classes we track in June. It hit a low on June 3rd and has appreciated by 1.5% since then. This is despite no change in short-end rate differentials and an outright narrowing in long-end…

BCA Research’s newly launched GeoMacro Strategy service presents the User’s Manual in its inaugural report navigating the differences between Geopolitical alpha and beta. What is the difference between geopolitical alpha and beta?…

We explain how to distinguish between ‘good’, ‘bad’ and ‘ugly’ unemployment, why bad unemployment is a much better gauge of the jobs market than headline unemployment, and what this means for the tactical positioning in bonds and stocks. Plus: base metals (XBM) have already sold off sharply, so take profits in the short position and open a tactical overweight in global materials (MXI).

Our Portfolio Allocation Summary for July 2024.