Diplomacy/Foreign Relations

The green energy transition will drive a surge in copper demand over a long-term horizon. However, a better entry point to get long will emerge after the next economic downturn begins.

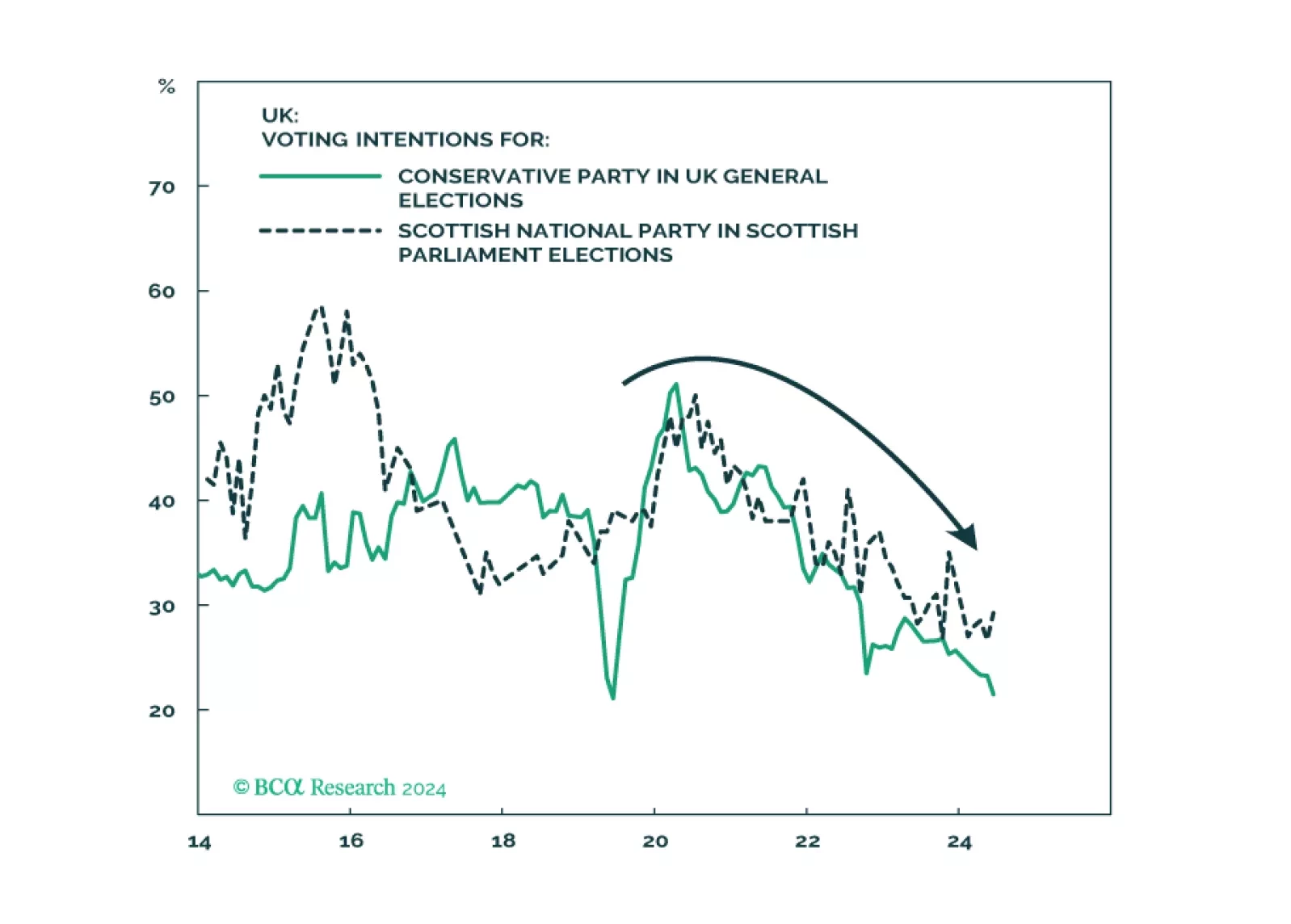

The Labour Party’s comeback in the UK is widely expected and will lead to fiscal stimulus consisting of increased public spending with minimal tax hikes. But a sweeping single-party majority will reduce social unrest only at the cost of higher taxes over the medium term. The paradigm has shifted away from the Thatcherite low-tax regime of the now-discredited Tories. v

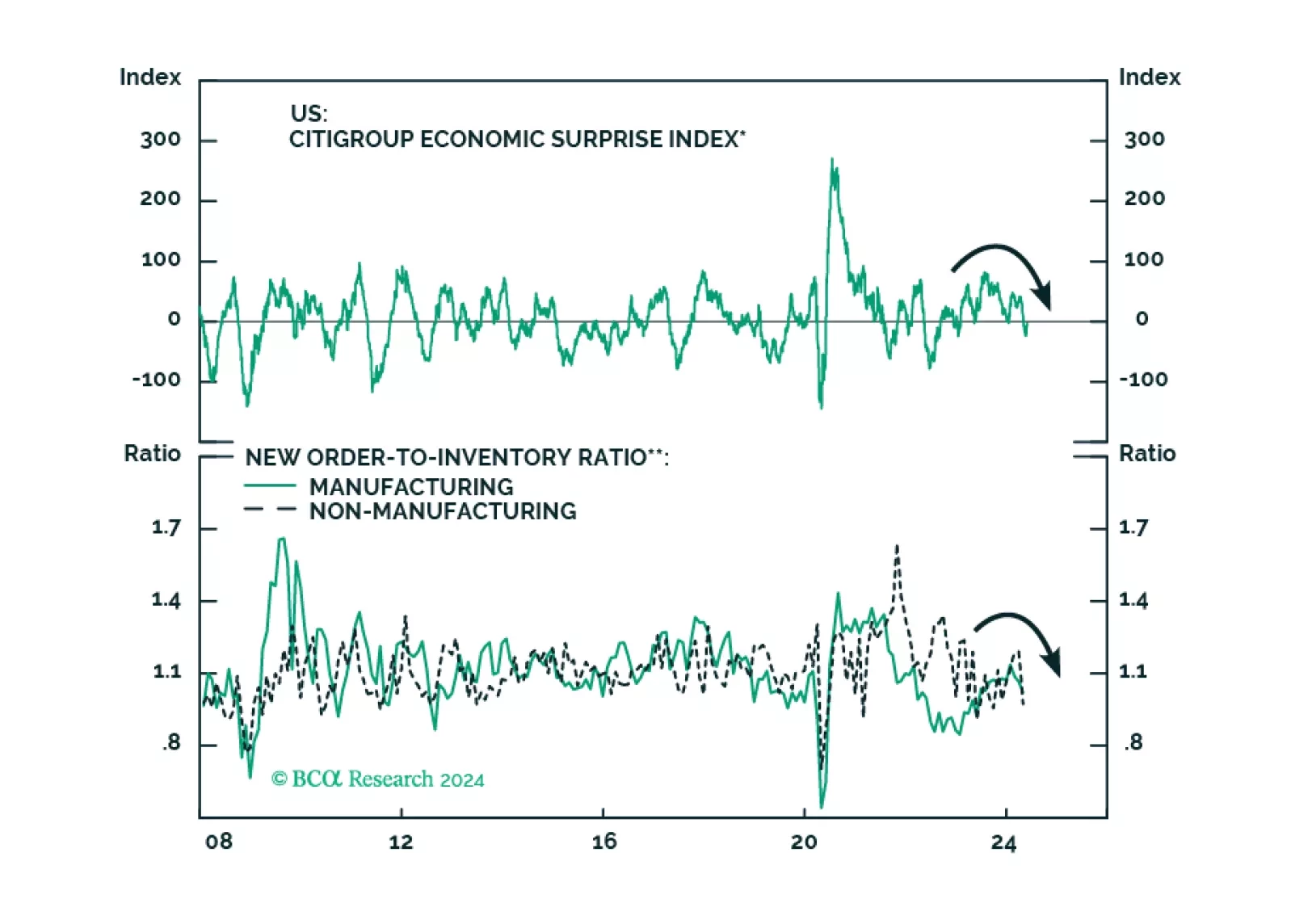

US assets and the US dollar should remain resilient relative to global peers over the next 12 months as policy uncertainty, election risk, and geopolitical risk reach a climax. After that, investors should reassess their regional allocation.

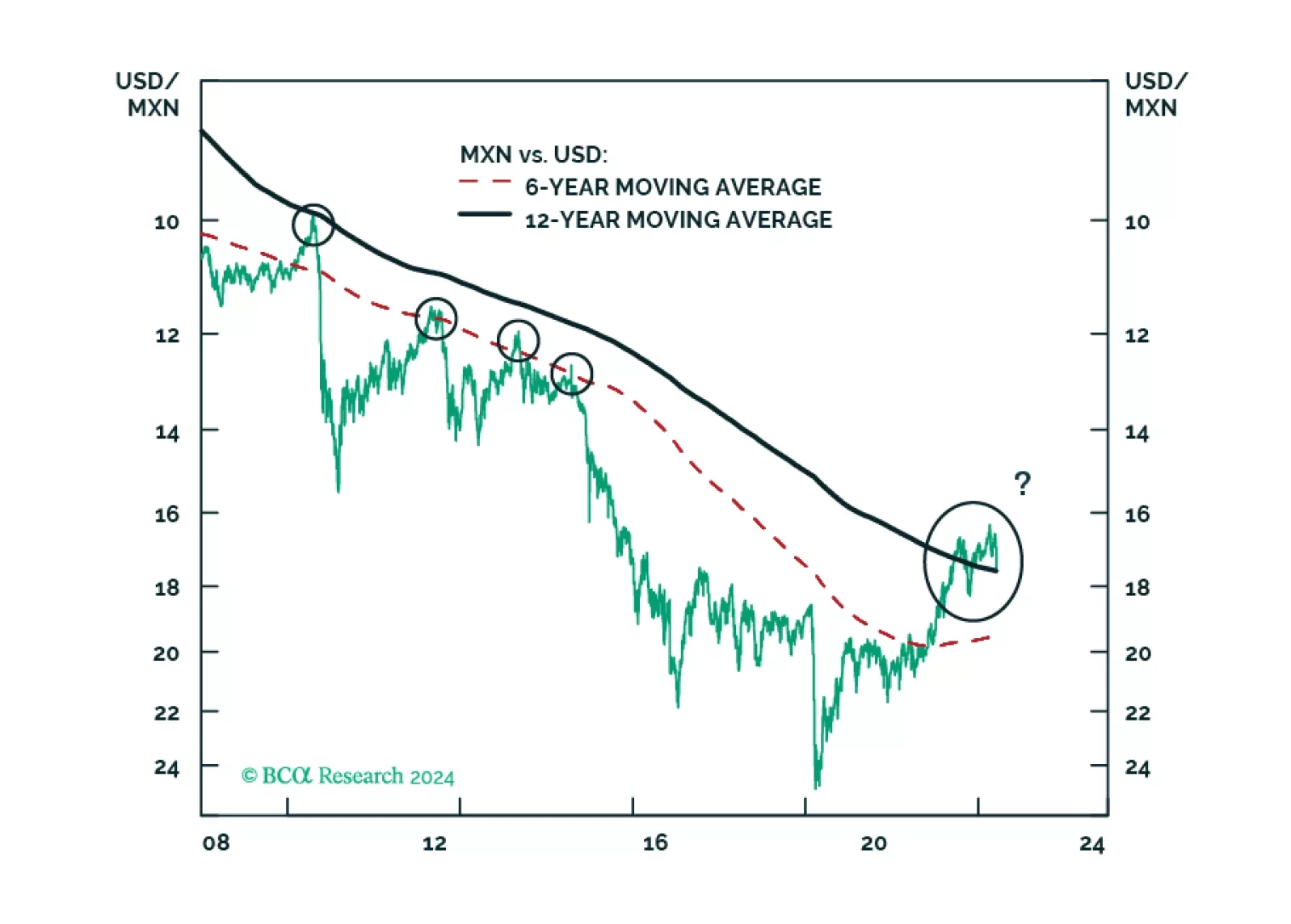

MORENA has once again swept the Mexican election: Claudia Sheinbaum will be president, with little to no constraint in Congress. All in all, Mexican politics will remain stable and overall supportive of markets. In the medium term, fiscal spending will return to conservatism and the constitutional reforms will lead to mixed fiscal and economic repercussions. In the long term, however, fiscal and institutional risks will rise. We advise investors to remain overweight Mexican risk assets relative to EM in cyclical and structural time horizons, but prepare for Mexican markets to sell off in absolute and relative terms in the next couple of months.

Democrats remain slightly favored for the White House because they are the four-year incumbent presidential party and the economy is not in recession. But if the unemployment rate rises in the lead up to November, then Biden and Democrats will become disfavored regardless of Trump’s convictions.

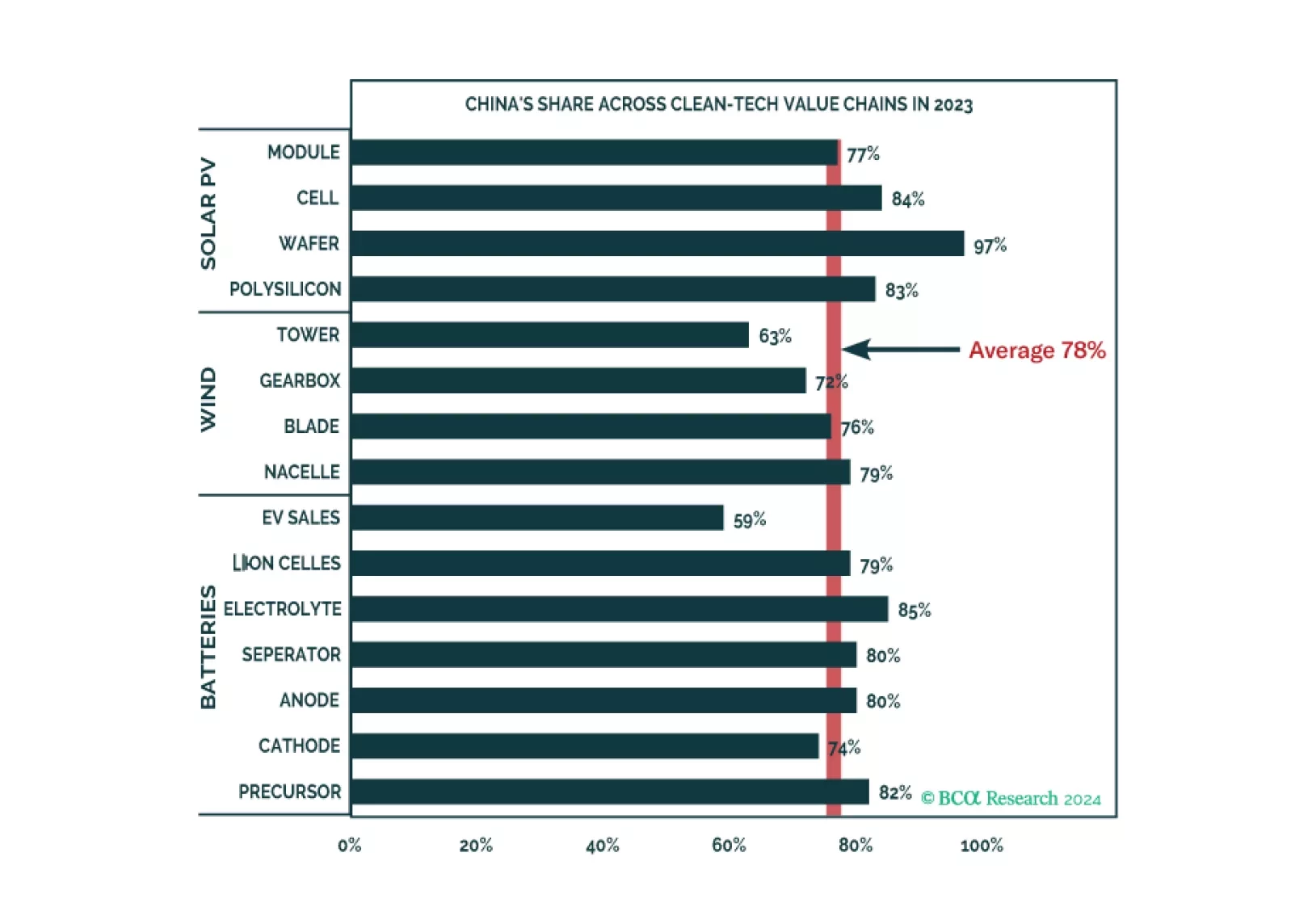

China is trying to export its way out of its economic slowdown while the US has already formed a hawkish consensus on foreign policy and trade. Investors should take cover as global financial markets are underrating the new phase of the trade war, which will escalate from here.