Disasters/Disease

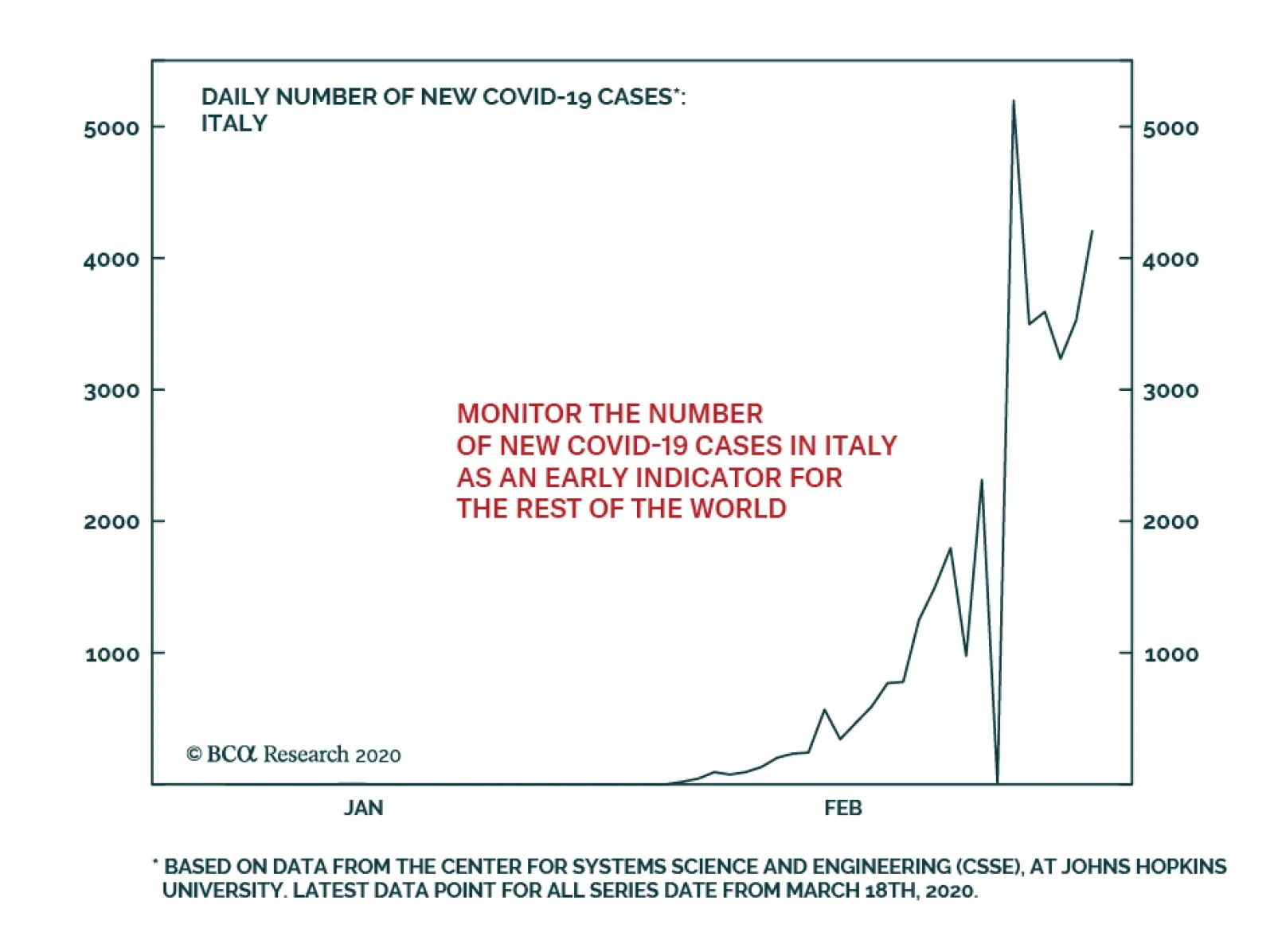

We recommend investors closely follow the number of new COVID-19 cases in Italy. At 4,207, as of March 18th, this number remains lower than it was on March 13th. However, new cases have nonetheless trended up over that past three days. Italy is…

Highlights Policy Responses: The COVID-19 pandemic has become a full-blown global crisis and recession. Governments and central bankers worldwide are now responding with aggressive monetary easing and fiscal stimulus. Markets will not respond positively to such stimulus, however, until there is some visibility on the true depth, and duration, of the economic downturn. Fixed Income Strategy: With a global recession now a certainty, bond yields will remain under downward pressure and credit spreads should widen further. Given how far yields have already fallen, we recommend emphasizing country and credit allocation in global bond portfolios, while keeping overall duration exposure around benchmark levels. Model Portfolio Changes: Following up on our tactical changes last week, we continue to recommend overweighting government debt versus spread product. Specifically, overweighting US & Canadian government bonds versus Japan and core Europe, and underweighting US high-yield and all euro area and EM credit. Feature In stunning fashion, the sudden stop in the global economy due to the COVID-19 pandemic has triggered a rapid return to crisis-era monetary and fiscal policies. The battle has now shifted to trying to fill the massive hole in global private sector demand left by efforts to contain the spread of the virus. It is unlikely that lower interest rates and more quantitative easing can mitigate the negative growth effects from travel bans, closing of bars and restaurants, and full scale lockdowns of cities. Fiscal policy, combined with efforts to boost market liquidity and ease the coming collapse of cash flows for the majority of global businesses, are the only plausible options remaining. It is unlikely that lower interest rates and more quantitative easing can mitigate the negative growth effects from travel bans, closing of bars and restaurants, and full scale lockdowns of cities. While the speed of these dramatic policy moves is unprecedented, the reason for them is obvious. Plunging equities and surging corporate bond credit spreads are signaling a global recession, but one of uncertain depth and duration given the uncertainties surrounding the spread of COVID-19 (Chart of the Week). Chart of the WeekCan Crisis-Era Monetary Policies Be Effective During A Pandemic?

Can Crisis-Era Monetary Policies Be Effective During A Pandemic?

Can Crisis-Era Monetary Policies Be Effective During A Pandemic?

Chart 2Risk Assets Will Not Bottom Until New COVID-19 Cases Ex-China Peak

Risk Assets Will Not Bottom Until New COVID-19 Cases Ex-China Peak

Risk Assets Will Not Bottom Until New COVID-19 Cases Ex-China Peak

The ability for policymakers to calibrate stimulus measures is pure guesswork at this point. The same thing goes for investors who see zero visibility on global growth, with the full extent of the virus yet to be felt in large economies like the United States and Germany – even as new cases in China, where the epidemic began, approach zero. The response from central bankers has been swift and bold – rapid rate cuts, increased liquidity programs for bank funding and increased asset purchases. The fact that global financial markets have remained volatile, even after what is a clear coordinated effort from policymakers, highlights how the unique threats to growth from the COVID-19 pandemic may be beyond fighting with traditional demand-side stimulus measures. We continue to recommend a cautious near-term investment stance, particular with regards to corporate bond exposure, until there is clear evidence that the growth rate of new COVID-19 cases outside China has peaked (Chart 2). Policymakers Throw The Kitchen Sink At The Problem The market moves and policy announcements have come fast and furious this past week, from virtually all major economies. We summarize some of the moves below: United States The Fed cut rates by -100bps in a Sunday night emergency move, taking the funds rate back to the effective lower bound of 0% - 0.25%. Importantly, Fed Chair Powell made it clear at his press conference that negative rates are not on the table, suggesting that we may have seen the last of the rate cuts for this cycle. A new round of quantitative easing (QE) was also announced, with purchases of $500 billion of Treasury securities and $200 billion of agency MBS that will occur in the “coming months”; Powell hinted that those amounts could be increased, if necessary (Chart 3). The MBS purchases are a clear effort to help bring down mortgage rates, which have not declined anywhere near as rapidly as US Treasury yields during the market rout (bottom panel). The Fed also cut the discount window rate – the rate at which banks can borrow from the Fed for periods of up to 90 days – by -150bps, bringing it down to 0.25%. The Fed said it is “encouraging banks to use their capital and liquidity buffers” – essentially telling banks to hold less cash for regulatory purposes. The Fed also reduced the rate on its US dollar swap lines with other central banks. The new rate is OIS +25bps. Coming on top of the massive increase in existing repo lines last week, the Fed is attempting to ensure that banks, both in the US and globally, that need USD funding have more liquidity available to support lending. Already, there are signs of worsening liquidity in the bank funding markets, like widening FRA-OIS spreads, but also evidence of illiquidity in financial markets like wide bid-ask spreads on longer-maturity US Treasuries and the growing basis between high-yield bonds and equivalent credit default swaps (Chart 4). Chart 3A Return To Fed QE

A Return To Fed QE

A Return To Fed QE

Chart 4Market Liquidity Issues Forced The Fed's Hand

Market Liquidity Issues Forced The Fed's Hand

Market Liquidity Issues Forced The Fed's Hand

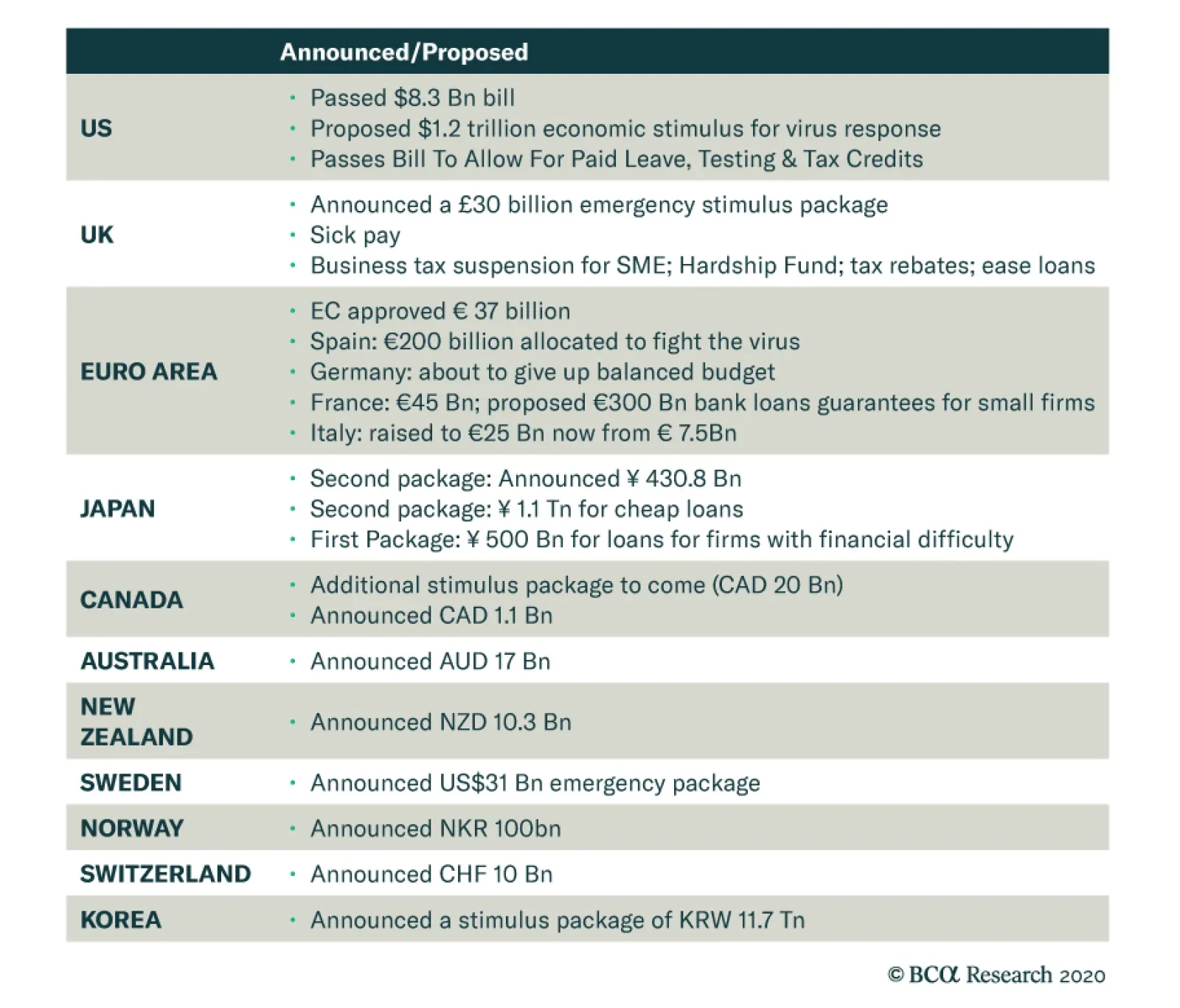

Turning to fiscal policy, the full response of the Trump administration is still being formed, but a major $850bn spending package has been proposed that would provide tax relief for American households and businesses while also including a $50bn bailout of the US airline industry. This comes on top of previously announced plans to offer free testing for the virus, paid sick leave, business tax credits and a temporary suspension of student loan interest payments. Chart 5The ECB Has Limited Policy Options

The ECB Has Limited Policy Options

The ECB Has Limited Policy Options

Euro Area The European Central Bank (ECB) unexpectedly made no changes to policy interest rates last week. It opted instead to increase asset purchases by €120bn until the end of 2020 (both for government bonds and investment grade corporates), while introducing more long-term refinancing operations (LTROs) to “provide a bridge” to the targeted LTRO (TLTRO-3) that is set to begin in June. The terms of TLTRO-3 were improved, as well; banks that accessed the liquidity to maintain existing lending could do so at a rate up to -25bps below the current ECB deposit rate of -0.5%, for up to 50% of the existing stock of bank loans. The ECB obviously had to do something, given the coordinated nature of the global monetary policy response to COVID-19. Yet the decisions taken show that the ECB is much more limited in its ability to ease policy further, with interest rates already negative, asset purchases approaching self-imposed country limits and, most worryingly, inflation expectations falling to fresh lows (Chart 5). The bigger responses to date have come on the fiscal front, with stimulus packages proposed by France (€45bn), Italy (€25bn), Spain (€3bn) and the European Commission (€37bn). The biggest news, however, came from Germany which has offered affected businesses tax breaks and cheap loans through the state development bank, KfW – the latter with an planned upper limit of €550bn (and with the German government assuming a greater share of risk on those new KfW loans). The German government has also vaguely promised to temporarily suspend its so-called “debt brake” to allow deficit financing of virus-related stimulus programs, if necessary. Other Countries The Bank of England cut interest rates by -50bps last week, while also lowering capital requirements for UK banks by allowing use of counter-cyclical buffers for lending. On the fiscal side, a £30bn package was introduced last week that included a tax cut for retailers, cash grants to small business, sick pay for those with COVID-19 and extended unemployment benefits. The Bank of Japan held an emergency meeting this past Sunday night, announcing no changes in policy rates but doubling the size of its ETF purchase program to $56 billion a year to $112 billion, while also increasing purchases of corporate bonds and commercial paper. The central bank also announced a new program of 0% interest loans to increase lending to businesses hurt by the virus. The Bank of Canada delivered an emergency -50bps cut in its policy rate last Friday, coming soon after the -50bp reduction from the previous week. The central bank also introduced operations to boost the liquidity of Canadian financial markets. The Canadian government also announced a fiscal package of up to C$20bn, including increased money for the state business funding agencies. The Reserve Bank of Australia did not cut its Cash Rate last week, which was already at a record-low 0.5%. It did, however, signal that it would begin a quantitative easing program for the first time, and introduce Fed-like repo operations, to provide more liquidity to the economy and local financial markets. The Australian government has also announced A$17bn of fiscal stimulus. Fiscal packages have also been introduced in New Zealand (where the Reserve Bank of New Zealand just cut its policy rate by -75bps), Sweden, Switzerland, Norway, and South Korea. To date, China has leaned more on monetary and liquidity measures – lowering interest rates and cutting reserve requirements – rather than a big fiscal stimulus package. Will all these policy measures be enough to offset the hit to global growth from COVID-19 and help stabilize financial markets? It is certainly a good start, particularly in countries with low government and deficit levels that have the fiscal space for even more stimulus, like Germany, Australia and Canada (Chart 6). Given these competing forces of global recession and monetary policy exhaustion on one side, but with increasingly more expansive fiscal policy on the other, we recommend a neutral (at benchmark) stance on overall global duration exposure on both a tactical and strategic basis. The ability to calibrate the necessary policy response is impossible to assess without knowing the full impact of COVID-19 pandemic on the global economy – including the size of related job losses and corporate defaults/bankruptcies. Policymakers are likely to listen to the combined message of financial markets – equity prices, credit spreads and government bond yields. The low level of yields and flat yield curves, despite near-0% policy rates across the developed world (Chart 7), suggests that investors see monetary policy as “tapped out”, leaving fiscal stimulus as the only way to fight the economic war against COVID-19. Chart 6At Global ZIRP, The Policy Focus Shifts To Fiscal

At Global ZIRP, The Policy Focus Shifts To Fiscal

At Global ZIRP, The Policy Focus Shifts To Fiscal

Chart 7Are Bond Yields Discounting A Global Liquidity Trap?

Are Bond Yields Discounting A Global Liquidity Trap?

Are Bond Yields Discounting A Global Liquidity Trap?

Given these competing forces of global recession and monetary policy exhaustion on one side, but with increasingly more expansive fiscal policy on the other, we recommend a neutral (at benchmark) stance on overall global duration exposure on both a tactical and strategic basis. Bottom Line: The COVID-19 pandemic has become a full-blown global crisis and recession. Governments and central bankers worldwide are now responding with aggressive monetary easing and fiscal stimulus. Markets will not respond positively to such stimulus, however, until there is some visibility on the true depth, and duration, of the economic downturn. Corporate Bonds In The US & Europe – Stay Tactically Defensive Chart 8This Crisis Is Different Than 2008

This Crisis Is Different Than 2008

This Crisis Is Different Than 2008

The COVID-19 global market rout has generated levels of market volatility not seen since the 2008 Global Financial Crisis. The US VIX index of option-implied equity volatility spiked to a high of 84, while the equivalent German VDAX measure reached a shocking high of 93. Equity valuations in both the US and Europe remain much higher on a forward price/earnings ratio basis compared to the troughs seen in 2008, even after the COVID-19 bear market. Yet even though volatility has returned to crisis-era extremes, and corporate credit has sold off hard in both the US and Europe, credit spreads remain well below the 2008 highs (Chart 8). Nonetheless, the credit selloff seen over the past few weeks has still been intense. Both investment grade and high-yield spreads have blown out, and across all credit tiers in both the US (Chart 9) and euro area (Chart 10). Even the highest-rated segments of the corporate bond universe have seen spreads explode, with AAA-rated investment grade spreads having doubled in both the US and Europe. Chart 9Broad-Based Spread Widening For Both Investment Grade...

Broad-Based Spread Widening For Both Investment Grade...

Broad-Based Spread Widening For Both Investment Grade...

Chart 10...And High-Yield

...And High-Yield

...And High-Yield

With the COVID-19 pandemic tipping the global economy into recession, it is not clear that the spread widening seen to date has been enough to compensate for the typical surge in downgrades and defaults seen during recessions – even though spreads do look wide on a duration-adjusted basis. With the COVID-19 pandemic tipping the global economy into recession, it is not clear that the spread widening seen to date has been enough to compensate for the typical surge in downgrades and defaults seen during recessions – even though spreads do look wide on a duration-adjusted basis. One of our favorite metrics to value corporate bonds is to look at option-adjusted spreads, adjusted for interest rate duration risk. We call this the 12-month breakeven spread, as it measures the amount of spread widening over one year that would leave corporate bond returns equal to those of duration-matched US Treasuries. We then look at the percentile rankings of those breakeven spreads versus their history as one indicator of corporate bond value. Chart 11US Corporates Look Cheaper On A Duration-Adjusted Basis

US Corporates Look Cheaper On A Duration-Adjusted Basis

US Corporates Look Cheaper On A Duration-Adjusted Basis

For the US, the 12-month breakeven spreads for the overall Bloomberg Barclays investment grade and high-yield indices are in the 82nd and 97th percentiles, respectively (Chart 11). This suggests that the latest credit selloff has made corporate debt quite cheap, although only looking through the prism of spread risk rather than potential default losses. Another of our preferred valuation metrics for high-yield debt is the duration-adjusted spread, or the high-yield index option-adjusted spread minus default losses. We then look at that default-adjusted spread versus its long-run average (+250bps) as a measure of high-yield value. To assess the current level of spreads, we use a one-year ahead forecast of the expected default rate using our own macro model. Over the past 12 months, the high-yield default rate was 4.5% and our macro model is currently calling for a rise to 6.2%. That estimate, however, does not yet include the certain hit to corporate profits from the COVID-19 recession. By way of comparison, the default rate peaked at 11.2% during the 2001/02 default cycle and at 14.6% during the 2008 financial crisis. In Chart 12, we show the historical default rate, our macro model for the default rate, and the history of the default-adjusted spread. We also show what the default-adjusted spread would look like in four different scenarios for the default rate over the next 12 months: 6%, 9%, 11% and 15%. The placement of these numbers in the bottom panel of Chart 12 indicates where the Default-Adjusted Spread will be if each scenario is realized. Chart 12US High-Yield Is Not Cheap On A Default-Adjusted Basis

US High-Yield Is Not Cheap On A Default-Adjusted Basis

US High-Yield Is Not Cheap On A Default-Adjusted Basis

Right now, our expectation is that there will be a virus driven US recession, but it will be shorter in magnitude than past recessions; this suggests a peak default rate closer to 9%. Such a scenario would still be consistent with a positive default-adjusted spread and likely positive excess returns for US high-yield relative to US Treasuries on a 12-month horizon. However, if a default rate similar to that seen during past recessions (11% or 15%) is realized, that would lead to a negative default-adjusted spread. Adding up both pieces of our valuation framework suggests that, while US high-yield spreads offer value on a duration-adjusted basis, spreads do not compensate enough for potential default losses if the US recession lasts longer than we expect. Thus, we recommend a tactical underweight position in US high-yield until we see better visibility on the severity, and duration, of the US recession. Adding up both pieces of our valuation framework suggests that, while US high-yield spreads offer value on a duration-adjusted basis, spreads do not compensate enough for potential default losses if the US recession lasts longer than we expect. As for euro area corporates, spreads for both investment grade and high-yield do look relatively wide on a breakeven spread basis, although less so than US credit (Chart 13). However, with the World Health Organization declaring Europe as the new epicenter of the COVID-19 pandemic, the harsh containment measures seen in Italy, Germany, France and elsewhere – coming from a starting point of weak overall economic growth – suggest that euro area spreads need to be wider to fully reflect downgrade and default risks. Chart 13Euro Area Corporates Look A Bit Cheaper On A Duration-Adjusted Basis

Euro Area Corporates Look A Bit Cheaper On A Duration-Adjusted Basis

Euro Area Corporates Look A Bit Cheaper On A Duration-Adjusted Basis

We recommend a tactical underweight allocation to both euro area corporate debt and Italian sovereign debt, as spreads have room to reprice wider to reflect a deeper recession (Chart 14). Chart 14Stay Underweight Euro Area Spread Product

Stay Underweight Euro Area Spread Product

Stay Underweight Euro Area Spread Product

Bottom Line: Corporate bond spreads on both sides of the Atlantic discount a sharp economic slowdown, but the odds of a deeper recession – and more spread widening - are greater in Europe relative to the US. A Quick Note On Recent Changes To Our Model Bond Portfolio In last week’s report, we made several adjustments to our model bond portfolio recommended allocations on a tactical (0-6 months) basis.1 Specifically, we downgraded our overall recommended exposure to global spread product to underweight, while increasing the overall allocation to government debt to overweight. The specific changes made to the model bond portfolio are presented in tables on pages 14 & 15. Within the country allocation of the government bond side of the portfolio, we upgraded US and Canada (markets more sensitive to changes in global bond yields, and with central banks that still had room to ease policy) to overweight, while downgrading core Europe to underweight and Japan to maximum underweight (both markets less sensitive to global yields and with no room to cut rates). On the credit side of the portfolio, we downgraded US high-yield to underweight (with a 0% allocation to Caa-rated debt), while also downgrading euro area investment grade and high-yield debt to underweight. We also lowered allocations to emerging market USD denominated debt, both sovereign and corporate, to underweight. We left the allocation to US investment grade debt at neutral, as the other reductions left our overall spread product allocation at the desired level (35% versus the 43% spread product weighting in our custom benchmark portfolio index). In terms of the specific weightings, the portfolio is now +11% overweight US fixed income versus the benchmark, coming most through US Treasury exposure. The portfolio is now -7% underweight euro area versus the benchmark, equally thorough government bond and corporate debt exposure. The portfolio is now also has a -7% weight in Japan versus the benchmark, entirely from government bonds. Note that these weightings represent a tactical allocation only, as we are recommending a defensive stance on spread product exposure given the near-term uncertainties over COVID-19 and global growth. On a strategic (6-12 months) horizon, however, we are neutral overall spread product exposure versus government bonds. Corporate bond spreads already discount a sharp economic slowdown and some increase in defaults. However, the rapid shift to aggressive monetary and fiscal easing by global policymakers to combat the virus will likely limit the duration and, potentially, the severity of the global slowdown currently discounted in wide credit spreads. Robert Robis, CFA Chief Fixed Income Strategist rrobis@bcaresearch.com Footnotes 1 Please see BCA Global Fixed Income Strategy Weekly Report, "The Train Is Empty", dated March 10, 2020, available at gfis.bcarsearch.com. Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Panicked Policymakers Move To A Wartime Footing

Panicked Policymakers Move To A Wartime Footing

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Corona Virus Proof Portfolio

Corona Virus Proof Portfolio

The coronavirus has served as a catalyst for a bear market in the SPX, the first since the GFC. We have been bearish up until this past Monday but given that we do not expect a GFC repeat we recommended investors with higher risk tolerance to dip their toes into the recent equity market weakness and deploy long-term capital. Today we introduce US Equity Strategy’s Corona Virus Proof Equity Basket, a portfolio of 15 stocks that we think can rise in absolute terms and continue to defy gravity compared with the broad market as it is rather insulated from the COVID-19 pandemic. This basket includes a bankruptcy consultant, an e-learning company on the cloud, a software company that enables remote access, three grocers, a tele-medicine company, two biotech giants, a Big Pharma company, the biggest online store in the US, an online streaming service company, a teleconferencing company, and finally two household/cleaning products leaders. Moreover, this basket can also serve as a signpost that the worse is behind us, and that the fear from the pandemic is dissipating. We will be closely monitoring this relative share price ratio for any weakness in order to gauge if such a turnaround is evident. Bottom Line: We would buy this US Equity Strategy Corona Virus Proof portfolio in order to ride out extreme volatility in the coming months. Stay tuned. The ticker symbols for the stocks in the US Equity Strategy Corona Virus Proof Equity Basket are: TDOC, INST, FCN, ZM, CTXS, JNJ, AMGN, REGN, CLX, RBGLY, WMT, COST, KR, NFLX, AMZN.

Dear Client, Next week we will be publishing a joint Special Report on the Chinese infrastructure investment outlook with our Emerging Markets Strategy service, authored by my colleague Ellen JingYuan He. Best regards, Jing Sima, China Strategist Feature Chart I-1Chinese Non-Financial Corporations Are Heavily Indebted

Chinese Non-Financial Corporations Are Heavily Indebted

Chinese Non-Financial Corporations Are Heavily Indebted

There are fears that the two-month hiatus in China’s business activities due to the COVID-19 epidemic has sparked acute cash shortages among Chinese companies. In turn, this has increased the danger that the highly leveraged Chinese corporate sector may be pushed into widespread insolvency (Chart I-1). The number of bankruptcies will undoubtedly climb, but small and micro firms are most at risk versus larger companies that have deeper cash reserves and easier access to financing. Our analysis shows that, before the outbreak hit China in January, companies listed in China’s onshore and offshore equity markets exhibited relatively healthy financial statements with adequate operating cash flows to cover debt obligations. This increases the probability that Chinese listed companies will survive the economic and financial shocks from the epidemic, and that their stock prices will rebound along with the expectations of a recovery in the Chinese economy. Chart I-2Both Chinese Economy And Corporate Profits Are Largely Driven By Domestic Demand

Both Chinese Economy And Corporate Profits Are Largely Driven By Domestic Demand

Both Chinese Economy And Corporate Profits Are Largely Driven By Domestic Demand

It also appears that China’s domestic economy is relatively insulated from the global financial market turmoil and impending global recession. China’s corporate profit outlook is dominated by domestic economic conditions rather than external demands. This view is also reflected in the relative performance of Chinese onshore and offshore stocks (Chart I-2). Moreover, the charts in the Appendix illustrate that corporate financial ratios in almost all sectors of China’s onshore and offshore equity markets have somewhat improved from the previous economic down cycle that began in 2014. This underscores our view that if reflationary measures overcompensate for the economic slowdown, as in the 2015/2016 easing cycle, then Chinese stocks will likely rally in absolute terms, as well as outperform global benchmarks. We selected three categories of financial ratios to monitor profitability, leverage and operating cash flow conditions of Chinese domestic and investable listed non-financial companies (Table I-1).1 The financial data in our exercise are from Refinitiv Datastream Worldscope. Its corresponding stock price indexes for China’s overall market and sectors most closely resemble the MSCI China Index and the MSCI China Onshore index. Table I-1

Monitoring Cash Flow Conditions In Chinese Listed Companies

Monitoring Cash Flow Conditions In Chinese Listed Companies

It is also noted that the Chinese investable index, excluding financial companies, is dominated by large technology companies such as Alibaba, Tencent, and Baidu.2 These tech companies generally have more adequate cash flows and lower debt ratios than the more capital intensive sectors such as industrial and energy. The analysis we present in this report on non-financial companies in the offshore market, therefore, is not indicative of China’s overall corporate financial health. Rather, our findings are indicative of how investors should view the listed companies and their sector performance within China’s investable market. Several observations from our analysis of the listed companies’ financial ratios are noteworthy: Chinese non-financial corporations are highly leveraged, and have not de-levered much despite the financial deleverage campaign that began in late 2017. Contrary to the belief that Chinese corporates’ financial health is significantly weaker than that in developed economies, the leverage ratio, profit margins, and debt-servicing ability among Chinese domestic and investable non-financial companies are actually in the range of their global peers (Chart I-3). Yet, Chinese companies trade at substantial discounts to global benchmarks. This is particularly evident in the offshore market, whereas domestic Chinese stocks were priced at a discount until the recent global market selloffs (Chart I-4). This underpins our view that, when China’s economy and corporate profits recover, Chinese stocks should outperform their global benchmarks on a cyclical time horizon. Importantly, with a stronger aggregate corporate financial health and a large price discount. Chinese investable non-financial stocks have more upside potential than their domestic counterparts. Chart I-3Financial Health Among Listed Chinese Companies Comparable With DMs

Financial Health Among Listed Chinese Companies Comparable With DMs

Financial Health Among Listed Chinese Companies Comparable With DMs

Chart I-4Chinese Investable Stock Prices Remain Deeply Discounted Relative To Global Benchmarks

Chinese Investable Stock Prices Remain Deeply Discounted Relative To Global Benchmarks

Chinese Investable Stock Prices Remain Deeply Discounted Relative To Global Benchmarks

Utilities, machinery, industrials and construction materials are among the sectors with the lowest cash flow-to-interest expense ratios, in both China’s domestic and investable markets. In particular, machinery, industrials and construction materials are pro-cyclical sectors and their profit growth is positively correlated with economic growth. Their low profitability and high leverage contribute to their poor cash flows. Those sectors have been severely impacted by the stoppages in manufacturing and construction activities due to the COVID-19 epidemic in China, making them vulnerable to cash shortages. However, there is a low risk of a broad-based default among these firms, because state-owned enterprises (SOEs) dominate these sectors in the Chinese equity market. The stock performance in these sectors is also extremely sensitive to shifts in China’s monetary and policy stance, and thus should benefit from the recent loosening in monetary conditions and the push for a substantial increase in infrastructure investment this year. Chart I-5Small Property Developers In China Are Much More Vulnerable To Cash Shortages Than Large Ones

Small Property Developers In China Are Much More Vulnerable To Cash Shortages Than Large Ones

Small Property Developers In China Are Much More Vulnerable To Cash Shortages Than Large Ones

The leverage ratio in the real estate sector has doubled in the past 10 years. The sector’s cash flow-to-total liabilities ratio has also declined sharply since 2017, when the authorities tightened lending standards to property developers. However, the sector’s aggregate cash flow situation is still an improvement from its lowest point in 2014, in both China’s domestic and investable markets. The countrywide lockdowns in January and February will undoubtedly have severe impacts on Chinese property developers’ cash flows. But the real estate sector is perhaps the best example in exhibiting a pronounced divergence in cash flow conditions between larger and smaller firms. Chart I-5 shows that, while the median ratio of cash-to-total liabilities tuned negative among 76 domestic listed real estate developers, the average ratio from total companies in the same sector suggests that the cash situation has actually improved since mid-2018. This divergence indicates that larger developers have more solid financial fundamentals and easier access to liquidity compared with their smaller counterparts, even before the lockdowns. We expect the divergence in cash flow conditions to widen in the coming months, and smaller property developers will face intensifying pressure to consolidate. China’s domestic healthcare companies have a much better cash balance than the investable healthcare sector, which has the lowest ratio of cash-to-interest expenses among all sectors. The poor cash flow conditions in investable healthcare companies are due to high leverage and low profitability, as well as high operating costs and R&D expenses. Chinese domestic healthcare sector has outperformed the broad market since the epidemic broke out in January. While we think the overall Chinese investable stocks have more upside than their domestic peers, domestic healthcare companies’ lower leverage ratio, stronger cash flows, and much higher profit margin make the sector a better bet than investable healthcare stocks on a cyclical time horizon (Chart I-6). Chart I-6Domestic Healthcare Sector Likely To Continue Outperforming The Broad Market

Domestic Healthcare Sector Likely To Continue Outperforming The Broad Market

Domestic Healthcare Sector Likely To Continue Outperforming The Broad Market

Chart I-7Energy Stocks Will Remain Depressed Until Oil Prices Rebound

Energy Stocks Will Remain Depressed Until Oil Prices Rebound

Energy Stocks Will Remain Depressed Until Oil Prices Rebound

Historically, there has been a strong positive correlation between the energy sector’s profitability, cash flow conditions, stock performance and crude oil prices (Chart I-7). In the past two years, the sector’s leverage ratio has risen, profit margins have thinned and the cash flow situation has sharply deteriorated to the same level as in 2014 when oil prices collapsed. The ongoing oil price rout will generate powerful deflationary forces in the energy sector and will likely further deteriorate energy firms’ profitability and cash flow. While we stay long cyclical stocks versus defensives on both a 0-3 month and a 6-12 month view, we recommend a cautious stance towards energy stocks until the evolving oil price war situation is clarified. Qingyun Xu, CFA Senior Analyst qingyunx@bcaresearch.com Jing Sima China Strategist jings@bcaresearch.com Appendix Overall Markets Excluding Financials

Overall Markets Excluding Financials Sector

Overall Markets Excluding Financials Sector

Consumer Discretionary Sector

Consumer Discretionary Sector

Consumer Discretionary Sector

Consumer Staples Sector

Consumer Staples Sector

Consumer Staples Sector

Real Estate Sector

Real Estate Sector

Real Estate Sector

Automobile Sector

Small Property Developers In China Are Much More Vulnerable To Cash Shortages Than Large Ones

Small Property Developers In China Are Much More Vulnerable To Cash Shortages Than Large Ones

Machinery Sector

Machinery Sector

Machinery Sector

Industrials Sector

Industrials Sector

Industrials Sector

Construction Materials Sector

Construction Materials Sector

Construction Materials Sector

Telecommunications Sector

Telecommunications Sector

Telecommunications Sector

Technology Sector

Technology Sector

Technology Sector

Healthcare Sector

Healthcare Sector

Healthcare Sector

Energy Sector

Energy Sector

Energy Sector

Utilities Sector

Utilities Sector

Utilities Sector

Footnotes 1 We exclude banks and financial institutions from this analysis, due to discrepancy in Chinese banks’ accounting measures from those of non-financial corporations’. 2 Alibaba, Tencent, Baidu, and JD together account for nearly 40% of the non-financial market cap in Chinese investable index. Cyclical Investment Stance Equity Sector Recommendations

In his recent television address, French President Emmanuel Macron referred to the current situation as a war. History is clear; nothing busts government budgets like wars. In fact, for most of the modern era, inflation was mainly a consequence of wartime…

Highlights Duration: We are not prepared to say that bond yields have troughed, even with the fed funds rate now back to the zero bound. Investors should keep portfolio duration close to benchmark. We do not rule out longer-maturity Treasury yields falling to 0% during the next couple of months, but negative bond yields in the US are not possible. TIPS: Current low TIPS breakeven inflation rates signal a rare buying opportunity. Though price swings will be volatile for the next few months, investors with horizons of 1-year or longer would be well advised to go long TIPS versus equivalent-maturity nominal Treasuries. Corporate Bonds: Corporate spreads are widening rapidly but still don’t offer above-average compensation if we adjust for likely future default scenarios. We will wait for a better entry point before recommending a shift back to overweight. Feature Does The Fed’s Bazooka Signal The Bottom In Yields? Chart 1Back To The Zero-Lower-Bound

Back To The Zero-Lower-Bound

Back To The Zero-Lower-Bound

In response to liquidity stresses witnessed in Treasury and MBS markets last week, the Fed decided to move this month’s FOMC meeting up to Sunday afternoon. It then took the opportunity to roll out a massive amount of easing. First the facts: The Fed cut the policy rate by 100 bps, back to the effective lower bound of 0% - 0.25%. Chair Powell also made it clear at his press conference that negative rates are not on the table. The Fed announced purchases of at least $500 billion of Treasury securities and $200 billion of agency MBS that will occur in the “coming months.” The Fed cut the discount window rate – the rate at which banks can borrow from the Fed for periods of up to 90 days – by 150 bps, bringing it down to 0.25%. The Fed said it is “encouraging banks to use their capital and liquidity buffers” (more on this below). The Fed also reduced the rate on its US dollar swap lines with other central banks. The new rate is OIS + 25 bps. The first major question for bond investors is whether this move will mark the bottom in yields (Chart 1). We aren’t so sure. As we write this on Monday morning the 2-year yield is 0.35%, down 14 bps from Friday’s close and the 10-year yield is 0.79%, down 15 bps from Friday. Obviously, further rate cuts won’t be the catalyst for lower bond yields, but investors can still push long-dated yields down if they start to price-in a longer period of time at the zero bound. In contrast, long-dated bond yields will only move up if we start to price-in an eventual economic recovery and exit from zero-bound rate policy. The fact that S&P futures went limit down immediately after the Fed’s big announcement suggests we aren’t at that point yet. Further rate cuts won’t be the catalyst for lower bond yields, but investors can still push long-dated yields down if they start to price-in a longer period of time at the zero bound. In last week’s report we introduced four criteria to monitor to decide when to call the trough in bond yields.1 Even with the Fed’s move back to zero, these four factors remain the most important things to watch. First, we want to see signs that the COVID-19 pandemic is becoming contained. That is, we want to see the daily number of new cases fall close to zero. We are still far away from that point (Chart 2), but evidence from China shows that containment is possible if the rest of the world follows a similar roadmap. Second, we want to see evidence of improving global growth, particularly in China. We showed last week how the Global and Chinese Manufacturing PMIs plunged in February. Since then, higher frequency global growth indicators – such as the performance of cyclical equities over defensives and the CRB Raw Industrials index – have not recovered at all (Chart 3). With very few new COVID cases in China and a large amount of stimulus on the way, we expect Chinese growth indicators to rebound in the coming months. Chart 2Tracking ##br##COVID-19

Tracking COVID-19

Tracking COVID-19

Chart 3Waiting For A Stronger Global Growth & Weaker US Growth

Waiting For A Stronger Global Growth & Weaker US Growth

Waiting For A Stronger Global Growth & Weaker US Growth

Third, we want to see some bad economic data coming out of the US. As of today, the US Economic Surprise Index is a robust +74 and last week’s initial jobless claims and Consumer Sentiment releases were healthy (Chart 3, bottom 2 panels). We know the weak economic data are coming, but they haven’t arrived yet. Until they do, there is an elevated risk of another downleg in bond yields. We expect the time to call the bottom in bond yields will be when the US data are very weak and the Global and Chinese data are improving. Investors will use the global rebound as a roadmap for the US and start to push yields higher. Finally, we would like to see signals from some technical trading rules that have good track records of calling bottoms in bond yields. The technical rules we examined last week are all based on identifying periods when bond market sentiment is extremely bullish and when bond yield momentum hooks up. Chart 4Technical Trading Rules

Technical Trading Rules

Technical Trading Rules

So far, none of the technical rules we identified have been triggered. Our Composite Technical Indicator remains in deeply “overbought” territory (Chart 4), but to generate a sell signal we also need one of our momentum measures to turn positive (Chart 4, bottom 3 panels). This hasn’t happened yet. All in all, none of our four criteria have been met. We are therefore inclined to think that it is too soon to call the bottom in bond yields. Investors should keep portfolio duration close to benchmark. Negative Yields In The US? We think it’s entirely possible that the 10-year Treasury yield could fall as low as 0% during the next couple of months. With the front-end of the curve already pinned at zero, any further market panic will be disproportionately felt at the long-end, and another spate of bad news could easily push the 10-year yield down to 0%. However, if the 10-year yield were to fall to 0%, we would declare that the trough in yields. In other words, negative bond yields will not occur in the US. Why is this the case? We can think of the 10-year Treasury yield as the market’s expected average fed funds rate for the next decade.2 That being the case, the 10-year yield would only turn negative if the market believed that the Federal Reserve was willing to take the policy rate below zero. On Sunday, Chair Powell was adamant that negative interest rates won’t be considered. He said that any further easing would take the form of forward guidance and asset purchases. The strongest form of that would involve caps on intermediate- and/or long-maturity bond yields. Please note that Powell didn’t mention yield caps specifically on Sunday, this is our inference based on past Fed communications. But the main point is that negative bond yields are a policy choice, one that the Federal Reserve is not inclined to make any time soon. It’s highly notable that no country without a negative policy rate has seen negative bond yields further out the curve. One result of the Fed’s “lower for longer” bias is that, coming out of the current crisis, we would expect the equity market to bottom and corporate bond spreads to peak before Treasury yields move higher. Another factor that will weigh on how low long-end Treasury yields fall is whether the market thinks that the Fed views its recent rate cut as an “emergency measure” that will be quickly reversed when the COVID crisis passes, or as a more long-lasting policy change. The Fed was deliberately vague on this question in its statement, saying that it will maintain the current fed funds rate “until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” The Fed was deliberately vague precisely because it doesn’t know how quickly it will tighten policy. But given that the result of this year’s Strategic Review will likely be an explicit targeting of above-2% inflation, we can be fairly certain that the Fed will be slow to remove accommodation. We continue to view inflation expectations and financial conditions as the two most important indicators to track to determine the pace of eventual tightening.3 One result of the Fed’s “lower for longer” bias is that, coming out of the current crisis, we would expect the equity market to bottom and corporate bond spreads to peak before Treasury yields move higher. Bottom Line: We are not prepared to say that bond yields have troughed, even with the fed funds rate now back to the zero bound. So far, none of the four triggers we will use to call the bottom in yields have sent a signal. In fact, we do not rule out longer-maturity Treasury yields falling to 0% during the next couple of months, but negative bond yields in the US are not possible. The Fed’s Emergency Liquidity Measures Chart 5A Lack Of Liquidity

A Lack Of Liquidity

A Lack Of Liquidity

On Sunday, Fed Chair Powell said that the reason for moving the FOMC meeting forward was because of worrying signs of deteriorating liquidity in Treasury and Agency MBS markets. Specifically, many observed that the spreads between short-term financing rates (both secured and unsecured) and the risk-free OIS curve jumped last week (Chart 5). Also, mortgage rates didn’t follow Treasury yields lower (Chart 5, bottom panel) and bid/ask spreads widened in the Treasury market. Diagnosing The Problem Our assessment of last week’s liquidity problems is that they arose because, in this post Dodd-Frank/Basel III world, dealer banks are still not sure how to respond during periods of stress. Last week, a lot of nonfinancial firms tapped their revolving credit lines in an attempt to weather the upcoming downturn. This caused an outflow of cash from the banking system. With banks now holding less cash than they were comfortable with, the price of cash in money markets (repo, LIBOR, etc…) started to spike. Because repo is a commonly used tool for financing Treasury trades, the knock-on effect of a spike in the repo rate is a loss of liquidity in the Treasury market. But are banks really short of cash? We got a small taste of the confusion around this issue when repo rates spiked last September. The Fed assumed that it had plenty of room to shrink its balance sheet and drain cash from the banking system because the banks were operating with large liquidity buffers, in excess of what was mandated by regulations like the Liquidity Coverage Ratio (LCR). However, it turned out that banks wanted to hold much more cash than was required by the LCR, in large part because they worried about the Fed’s periodic stress tests, the criteria of which can change over time. The Fed’s Solutions Fortunately, the Fed has taken a lot of aggressive action to help mitigate these problems. First, it announced a large quantity of repo operations last week, then followed that up by announcing direct Treasury and MBS purchases on Sunday. The Fed also lowered the discount window rate to a mere 0.25%, and is encouraging banks to tap that facility if necessary. But, in our view, perhaps the most important measure the Fed announced is simply that policymakers will encourage banks to “use their capital and liquidity buffers”. The fact of the matter is that banks are carrying large amounts of cash but have been hesitant to deploy it because they are worried about regulatory backlash from the Fed. If the Fed can effectively assure banks that it won’t be aggressively enforcing any regulatory action against them for the foreseeable future, then there is already a lot of liquidity in the system waiting to be deployed. Though we expect the Fed’s measures will have a significant positive impact on market liquidity, it will be important to monitor money market spreads going forward. The Fed has still not taken the extreme step of re-launching its crisis-era commercial paper facility and lending directly to nonfinancial corporates. This would be a likely next step if liquidity conditions continue to deteriorate. A Rare Opportunity In TIPS Together, the COVID-induced global demand shock and the OPEC-induced oil supply shock have taken TIPS breakeven inflation rates down to extraordinarily low levels. As of Friday’s close, the 10-year TIPS breakeven inflation rate was a mere 0.92%, the 5-year rate was 0.56% and the 1-year rate was an absurd -0.49%. In fact, both the 1-year and 2-year breakeven rates were negative! For buy and hold investors, this presents an outstanding opportunity to buy TIPS and short the equivalent-maturity nominal bond. For example, a buy and hold investor will make money by going long TIPS and short nominals as long as headline CPI inflation averages above 0.56% per year for the next five years or above 0.92% per year for the next decade (Chart 6). The fact that the 1-year and 2-year breakeven rates are negative is an even greater mispricing because TIPS come with embedded deflation floors. That is, TIPS principal is adjusted higher by the rate of headline CPI inflation but it is never adjusted lower if headline CPI inflation turns negative. The deflation floor means that a negative 1-year or 2-year TIPS breakeven inflation rate represents risk-free profit for anyone who can commit capital for the entire 1-year or 2-year investment horizon. A buy and hold investor will make money by going long TIPS and short nominals as long as headline CPI inflation averages above 0.56% per year for the next five years or above 0.92% per year for the next decade. But abstracting from deflation floors, is it even realistic to expect negative headline CPI during the next 12 months? Even in a worst-case scenario, it is difficult to imagine. First, let’s assume that the Brent crude oil price falls to $20 during the next month and then stays there. The second panel of Chart 7 shows that this would cause year-over-year Energy CPI to hit -20% before recovering. Second, let’s assume that core CPI follows the path implied by our Pipeline Inflation Pressure Gauge, falling from its current 2.4% to 1.8% for the next 12 months (Chart 7, panel 4). Third, let’s assume that year-over-year food inflation collapses all the way to 0% (Chart 7, panel 3). Chart 6TIPS Breakeven Inflation Rates Are Too Low

TIPS Breakeven Inflation Rates Are Too Low

TIPS Breakeven Inflation Rates Are Too Low

Chart 7Worst-Case Scenario For CPI

Worst-Case Scenario For CPI

Worst-Case Scenario For CPI

This worst-case scenario would result in 12-month headline CPI of +0.09% for the next 12 months (Chart 7, bottom panel). Now, core CPI inflation did fall below 1% during the last recession, an occurrence that would certainly lead to headline CPI deflation if it happened again. However, shelter makes up 42% of core CPI. Without a significant slowdown in the housing market, such a large decline in core inflation is unlikely. Bottom Line: Current low TIPS breakeven inflation rates signal a rare buying opportunity. Though price swings will be volatile for the next few months, investors with horizons of 1-year or longer would be well advised to go long TIPS versus equivalent-maturity nominal Treasuries. Corporate Bond Spreads:Too Soon To Buy Corporate bond spreads have widened dramatically during the past few weeks. Within the investment grade space, the overall index spread and the average spread excluding the energy sector have both broken above their 2016 peaks. The investment grade energy spread is still 56 bps below its 2016 peak (Chart 8A). In high-yield, the overall index spread is still 112 bps below its 2016 peak. The energy spread is 23 bps below its 2016 peak and the ex-energy spread is 112 bps below its 2016 peak (Chart 8B). Chart 8AInvestment Grade Corporate Bond Spreads

Investment Grade Corporate Bond Spreads

Investment Grade Corporate Bond Spreads

Chart 8BHigh-Yield Corporate Bond Spreads

High-Yield Corporate Bond Spreads

High-Yield Corporate Bond Spreads

Obviously, spreads are widening quickly and value is returning to the sector. This raises the important question of: When will it be a good idea to step in and buy? To answer this question we need to view current spread levels relative to the magnitude of the upcoming economic shock. During the past 12 months, the speculative-grade corporate default rate was 4.5% and our macro model already anticipates a rise to 6.2%. This would bring the default rate above the 5.8% peak seen in 2017, but is probably still too low of an estimate given that the upcoming corporate profit hit is not yet reflected in our model (Chart 9). Gross leverage – the ratio of total debt to pre-tax profits – enters our default rate model with a roughly six month lag, meaning that we wouldn’t expect any current hit to profits to impact the default rate for another six months. For further context, we note that the default rate peaked at 11.2% during the 2001/02 default cycle and at 14.6% during the 2008 financial crisis. Chart 9An Above-Average Default-Adjusted Spread Signals A Buying Opportunity

An Above-Average Default-Adjusted Spread Signals A Buying Opportunity

An Above-Average Default-Adjusted Spread Signals A Buying Opportunity

The bottom panel of Chart 9 shows our High-Yield Default-Adjusted Spread. This is a measure of the excess spread in the high-yield index after subtracting ex-post default losses. Its historical average is around 250 bps. We shocked our Default-Adjusted Spread to see what it would be in four different scenarios for the default rate: 6%, 9%, 11% and 15%. The placement of these numbers in the bottom panel of Chart 9 indicates where the Default-Adjusted Spread will be if each scenario is realized. For example, if the default rate comes in at 6% for the next 12 months then the Default-Adjusted Spread will be +347 bps, above its historical average. If the default rate is 9% during the next 12 months the Default-Adjusted Spread will still be positive, at +108 bps, but will be below historical average. A default rate similar to what was seen during past recessions (11% or 15%) would lead to a negative Default-Adjusted Spread. Right now, our best estimate of a short-lived recession would suggest a peak default rate of somewhere between 6% and 9%, probably closer to 9%. Such a scenario would be consistent with a positive Default-Adjusted Spread and likely positive excess returns for corporate bonds (both investment grade and high-yield) relative to Treasuries on a 12-month horizon. However, we also note that periods of spread widening usually culminate with our Default-Adjusted Spread measure well above its historical average. This was the case in 2016, 2009 and 2002. As of now, this sort of attractive valuation will only be achieved if the default rate is 6% or lower during the next 12 months, a forecast that seems overly optimistic. The bottom line is that we are inclined to wait for a more attractive entry point before recommending a shift back to an overweight allocation to corporate bonds versus Treasuries. Though it is probably too late for investors with long time horizons (12 months or more) to sell. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see US Bond Strategy Weekly Report, “When And Where Will Bond Yields Trough?”, dated March 10, 2020, available at usbs.bcaresearch.com 2 Technically, the 10-year yield is equal to 10-year rate expectations plus a term premium to compensate investors for locking up funds for 10 years instead of rolling over a series of overnight investments. The term premium is difficult to estimate in practice, but it is likely to be quite close to zero at present. 3 For further details on why investors should focus on these two measures to assess the pace of eventual policy tightening please see US Bond Strategy / Global Fixed Income Strategy Special Report, “The Fed In 2020”, dated December 17, 2019, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

HighlightsPortfolio Strategy“There is blood in the streets”. Investors with higher risk tolerance should be buying into this weakness and start to deploy long-term oriented capital. S&P 500 futures fell to 2394 which is a whopping 1000 points below the February 19, 2020 high of 3393. We cannot time the bottom, but future returns will be handsome from current SPX levels.Stick with health care stocks as the coronavirus pandemic will boost demand for health care goods and services, at a time when investors will also seek the refuge of defensive equities as the economy is in recession.Surging demand for pharmaceuticals, firming operating metrics, cheap relative valuations, an appreciating greenback along with the drubbing in the global manufacturing PMI, all signal that an underweight stance is no longer warranted in pharma equities. Recent ChangesLift the S&P pharmaceuticals index to neutral today. Table 1

Inflection Point

Inflection Point

Feature"Be fearful when others are greedy, and greedy when others are fearful"- Warren Buffett"The time to buy is when there's blood in the streets"- Baron RothschildEquities were unhinged last week, as the trifecta of the corona virus becoming a pandemic, Saudi ripping the cord out of crude oil and the convulsing bond markets made for an explosive equity market cocktail. The result was two circuit breaker triggers at the -7% mark that (thankfully) worked as planned and brought some liquidity back into the markets.Our Complacency-Anxiety index plunged to a panic level that has marked previous equity market troughs (Chart 1A). CNN’s Fear & Greed Index fell from near 100 to 1. While it could fall further at least a reflex rebound is in order. The Monday and Thursday mini-crashes felt like a capitulation (Chart 1B). Whoever wanted to get out likely got out. Chart 1ATime To Buy

Time To Buy

Time To Buy

Chart 1BThere’s Is Blood In the Streets

There’s Is Blood In the Streets

There’s Is Blood In the Streets

Volumes in the SPX soared to the highest level since 2011 and the bullish percentage index1 fell to 1.4%2 below the low hit in 2008! Early last week six out of ten stocks in the broad-based Russell 3000 were down 30% or more from their 52-week highs. As a reminder, the SPX took the elevator down and erased 13 months of gains in a mere 13 trading days (Chart 2)! Chart 2Selling Is Overdone

Selling Is Overdone

Selling Is Overdone

Chart 3Our Roadmap

Our Roadmap

Our Roadmap

A big crack has now formed.Given the tremor we just experienced, we doubt a V-shaped recovery to fresh all-time highs is in store for stocks similar to the one following the 2018 Christmas Eve lows V-shaped advance. Instead, parallels with the early-2018, 2015/16, 2011 or 19873 market action are more apt (Chart 3).Historically, Table 2 shows that the median time it takes for the stock market to make fresh all-time highs following a minimum 20% bear market from the most recent highs is two years. Table 2Bear Markets Duration

Inflection Point

Inflection Point

In other words, this will likely be a prolonged troughing phase and a retest near last Thursday’s lows is a high probability event, at which point we think the market will hold those lows, and this will serve as a catalyst to definitively put cyclical-oriented capital to work.Our purpose here is not to scare investors when a number of markets are in duress and already in a bear market. We have been sending these warning shots4 since last summer5 all the way until the recent SPX February peak. Now that we have reached the proverbial “riot point” we would recommend taking a cold shower and keeping calm and collected in order to put things into perspective as one of our mentors would always do in tumultuous times.Importantly, investors with higher risk tolerance should be buying into this weakness and start to deploy long-term oriented capital. We cannot time the bottom, but future returns will be handsome from current SPX levels. As a reminder, S&P 500 futures fell to 2394 which is a whopping 1000 points below the February 19, 2020 high of 3393.This drubbing blew past our most bearish SPX estimate of 2544,6 pushing the SPX from overvalued to undervalued overnight. In fact, the forward P/E has fallen to one standard deviation below the historical time trend (Chart 4). Chart 4From Overvalued To Undervalued

From Overvalued To Undervalued

From Overvalued To Undervalued

Our sense is that we will avoid a GFC type collapse, and thus investors with higher risk tolerance should start putting long-term cash to work as “there is blood in the streets”.Recapping the sequence of recent events is instructive. Two Fed officials (Clarida and Evans) made a huge error in our view by relaying that the Fed should stand pat and refrain from cutting rates. This culminated in a Powell press release that the Fed is ready to act, basically canceling these misplaced statements from the two Fed officials.Following these communication whipsaws, G7 finance ministers and central bankers held a conference call and then, the Fed panicked and cut rates inter-meeting further fueling the blazing fire. Now the Fed is cornered and has to act anew and further cut the fed funds rate (FFR) on March 18 all the way down to the zero lower bound. As a reminder, the last time the markets fell roughly 20% in late-2018 it took the Fed seven months to cut rates, this time it happened a mere two trading days after the market had a near 16% decline from the February peak.All of this bred uncertainty and a bond market spasm. There is little doubt we are in recession. The 10-year US Treasury yield plunging below 0.4% has fully discounted a recession, 100bps of Fed cuts and QE5 in our view.Keep in mind that the bond market now knows the Fed will cut the FFR to zero and eventually resort to QE, so it really front runs the Fed. This is something the bond market never anticipated or discounted on the eve of the Great Financial Crisis.While it is definitely true that interest rate cuts and further QE will neither cure COVID-19 nor reverse work-related disruptions, the Fed has to act and cut interest rates and restart QE for three reasons:a) to instill confidence that it is doing something and it is not a bystander,b) to loosen financial conditions as the VIX at a recent high near 76 and a more than doubling in junk spreads are screaming “help” (Chart 5), andc) to jawbone the US dollar lower.Our sense is that the fixed income market hit an inflection point for stocks when the 10-year US Treasury yield breeched the 1.5% mark: the correlation between stocks and bond yields quickly snapped from negative to positive. Based on recent empirical evidence, stocks cannot stomach a 10-year US Treasury yield above 3%, and suffer indigestion below 1.5% (Chart 2). Crudely put, while lower yields act as a shock absorber for equities (via lifting the forward P/E multiple), below a breaking point they warn of a deflationary shock. Thus, we would view an eventual return of the 10-year US Treasury yield near the 1.5% as a positive sign for stocks. Chart 5Watching Spreads

Watching Spreads

Watching Spreads

The other shock two weekends ago was the deflationary oil market spiral out of the OPEC meeting in Vienna where a fight apparently erupted between the Saudis and the Russians with regard to rebalancing the oil markets and resulted in $30/bbl oil. The timing could not have been worse. Oil related capex will fall off a cliff given the looming bankruptcies in the US shale oil patch (bottom panel, Chart 5) and that makes a fiscal package from the US even more pressing.We deem that only a mega fiscal package comparable to the $750bn TARP will definitively stop the hemorrhaging. A comprehensive fiscal package close to $1tn in order to deal with the aftermath of the corona virus would mark a bottom in the equity market.Health care stocks will benefit both from a fiscal package and from the corona virus pandemic automatic rise in demand for health care services and goods. Thus, this week we reiterate our overweight stance in the health care sector and make a small shift to our sub-sector positioning.Continue To Hide In Health Care…We recommend investors continue to take refuge in health care stocks within the defensive universe as the coronavirus pandemic unfolds. The S&P health care sector relative share price ratio recently bounced off the one standard deviation below the historical time trend line and is primed to vault higher in coming quarter (Chart 6). Chart 6Health Care Shines In Recessions

Health Care Shines In Recessions

Health Care Shines In Recessions

If severe government measures are a prerequisite to stop the spread of the virus then growth will suffer a massive setback. Were President Trump to take draconian measures similar to what the Italian Prime Minister imposed recently and effectively shut down the country, then PCE will collapse.In fact, PCE excluding health care will take a beating. Health care outlays will rise both in absolute terms and relative to overall spending (Chart 7). Given the safe haven status of the S&P health care index and the stable cash flows these businesses command, when growth is scarce, investors flock to any source of growth they can come by and health care stocks definitely fit that bill.Not only is firming demand reawakening health care stocks that have been trading at a discount to the broad market owing to political uncertainty, but also their defensive stature is a heavily sought after attribute during recessions (Chart 6). Chart 7Upbeat Demand Profile…

Upbeat Demand Profile…

Upbeat Demand Profile…

Chart 8…Will Boost Selling Prices And Sales

…Will Boost Selling Prices And Sales

…Will Boost Selling Prices And Sales

Inevitably, demand for health care goods and services will rise in the coming weeks straining the US health care system, as the number of infections increases. This will sustain industry selling price inflation and underpin revenue growth at a time when the world will be deflating (Chart 8).The implication is an earnings-led durable health care sector outperformance phase, a message that our relative macro EPS growth model is forecasting for the rest of the year (Chart 9).Importantly, such a rosy outlook is neither discounted in relative forward sales nor profit growth expectations for the coming year and we would lean against such pessimism (third panel, Chart 10). Chart 9Macro Profit Growth Model Says Buy

Macro Profit Growth Model Says Buy

Macro Profit Growth Model Says Buy

Chart 10Unloved And Under-owned

Unloved And Under-owned

Unloved And Under-owned

Finally, valuations and technicals are both flashing green. On a forward P/E basis health care stocks still trade at a 15% discount to the broad market and momentum is washed out offering a compelling entry point for fresh capital.In sum, in times of malaise investors flock to defensive health care stocks, that are currently direct prime beneficiaries of the ongoing coronavirus pandemic.Bottom Line: We reiterate our overweight recommendation in the largest market capitalization weighted defensive sector in the SPX, the S&P health care sector.Upgrade Pharma To NeutralLift the S&P pharmaceuticals index to neutral from underweight for a modest loss of -1% since inception.A structurally downbeat pricing power backdrop was the primary driver of our bearish call on the S&P pharma index as both sides of the political aisle were out to get Big Pharma (bottom panel, Chart 11). This portfolio position was up double digits since inception, but it has given back almost all the gains recently since the coronavirus pandemic took stage a few weeks ago.While our thesis has not changed, we do not want to be bearish any health care related equities in times of a health epidemic. In addition, there is a chance that one of these behemoths discovers a compound to beat the virus and could serve as a catalyst for a sharp reversal of the downtrend.Importantly, from an operating perspective, margins appear to have troughed following 15 years of declines (middle panel,Chart 11). Now that inadvertently demand for medicines will surge, sales and profits will expand smartly (third & bottom panels, Chart 12). Chart 11It No Longer Pays To Be Bearish

It No Longer Pays To Be Bearish

It No Longer Pays To Be Bearish

Chart 12Firming Demand

Firming Demand

Firming Demand

As a result of the coronavirus pandemic, we deem pharma factories will start to hum reversing the recent contraction in pharmaceutical industrial production (second panel, Chart 12).From a macro perspective, layoffs are inevitable from the coronavirus catalyzed recession and a softening labor market bodes well for defensive pharma profits (bottom panel, Chart 12).The collapse in the February global manufacturing PMI, primarily driven by China, is a window into what the future holds for developed market (DM) PMIs. DMs will feel the coronavirus aftermath in the current month and likely sustain downward pressure on the global manufacturing PMI print. Historically, relative forward profits and the global manufacturing PMI have been inversely correlated and the current message is to expect catch up phase in the former (global PMI shown inverted, middle panel, Chart 13).Moreover, the same rings true for the ultimate macro indicator, the US dollar. A rising greenback reflects global growth ills and a safe haven bid in times of duress as investors park their money in the reserve currency of the world. Therefore, defensive pharma relative forward EPS enjoy a positive correlation with the US dollar, and the path of least resistance remains higher (bottom panel, Chart 13).Finally, relative valuations are hovering near one standard deviation below the historical mean and technicals have returned back to the neutral zone underscoring that it no longer pays to be bearish pharma stocks (Chart 14). Chart 13Macro Backdrop Is Favorable

Macro Backdrop Is Favorable

Macro Backdrop Is Favorable

Chart 14Value Has Been Restored

Value Has Been Restored

Value Has Been Restored

Adding it all up, surging demand for pharmaceuticals, firming operating metrics, cheap relative valuations, an appreciating greenback along with the drubbing in the global manufacturing PMI, all signal that an underweight stance is no longer warranted in pharma equities.Bottom Line: Lift the heavyweight S&P pharma index to neutral today, for a modest loss of -1% since inception. The ticker symbols for the stocks in this index are: BLBG: BLBG: S5PHAR – JNJ, MRK, PFE, BMY, LLY, ZTS, AGN, MYL, PRGO. Anastasios Avgeriou US Equity Strategistanastasios@bcaresearch.com Footnotes1 https://school.stockcharts.com/doku.php?id=index_symbols:bpi_symbols2 https://schrts.co/IfrNQmIu3 Please see BCA US Equity Strategy Daily Report, “Gravitational Pull” dated March 12, 2020, available at uses.bcaresearch.com.4 Please see BCA US Equity Strategy Weekly Report, “A Recession Thought Experiment” dated June 10, 2019, available at uses.bcaresearch.com.5 Please see BCA US Equity Strategy Special Report, “What Goes On Between Those Walls? BCA’s Diverging Views In The Open” dated July 19, 2019, available at uses.bcaresearch.com.6 Please see BCA US Equity Strategy Weekly Report, “From "Stairway To Heaven" To "Highway To Hell"?” dated May 2, 2020, available at uses.bcaresearch.com.Current RecommendationsCurrent TradesStrategic (10-Year) Trade Recommendations

Inflection Point

Inflection Point

Size And Style ViewsJune 3, 2019Stay neutral cyclicals over defensives (downgrade alert) January 22, 2018Favor value over growthMay 10, 2018Favor large over small caps (Stop 10%)June 11, 2018Long the BCA Millennial basket The ticker symbols are: (AAPL, AMZN, UBER, HD, LEN, MSFT, NFLX, SPOT, TSLA, V).

Highlights The S&P 500 is in a bear market, and a recession appears to be inevitable, … : The longest bull market in S&P 500 history succumbed last week to the Saudi-Russia oil war, the relentless drumbeat of spreading COVID-19 disruptions and the realization that it will take even worse market conditions to prompt a meaningful fiscal response. … but it is BCA’s view that the recession will be short, if sharp: Although our conviction level is low, and our view is subject to change as more information becomes available, we expect that the recession is much more likely to produce a V-bottom than a U-bottom. Pent-up demand will be unleashed once the coronavirus runs its course, stoked by monetary and fiscal stimulus initiatives around the world. Are central banks out of bullets?: We are not yet ready to embrace the most provocative idea that came up at our monthly View Meeting last week, but the question highlights the uncertainty that currently pervades markets. First, do no harm: What should an investor do now? Watch and wait. It is too early to re-risk a portfolio, but safe-haven assets are awfully overbought. Cash is worth its weight in gold right now, and those who have it should remember that they call the shots. Feature The S&P 500 entered a bear market last Thursday, bringing down the curtain on the longest US equity bull market in recorded history at just under 11 years.1 We are duly chastened by the misplaced bravado we expressed in last week’s report, which crumbled under the force of the ensuing weekend’s oil market hostilities between Saudi Arabia and Russia. We see the plunge in oil prices, and the looming spike in oil-patch defaults, bankruptcies and layoffs, as the straw that broke the camel’s back, ensuring a 2020 recession. Now that it has slid so far, we expect that the S&P 500 will generate double-digit returns over the next twelve months, but we do not believe that investors should be in any rush to buy. Wild oscillations are a sign of an unhealthy market, and stocks don’t establish a durable bottom while they are still experiencing daily spasms. The Fundamental Take (For What It’s Worth) We nonetheless believe that the recession will be fairly brief, even if it is sharp. The global economy was clearly turning around before the virus emerged, and the US economy was as fit as a fiddle. Data releases across February were decidedly positive, on balance, and the year-to-date data, as incorporated in the Atlanta Fed’s GDPNow model, pointed to robust first quarter growth in an economy that was firing on all cylinders (Chart 1). We continue to believe that most of the demand that goes missing across the first and the second quarters will not be lost for good, but will simply be deferred to the second half of this year and the beginning of next year. The coronavirus has brought an end to the expansion, but the US economy was in rude health before it was infected, and we expect it will make a full and swift recovery. Chart 1The First Quarter Had Been Shaping Up Really Well

March Sadness

March Sadness

Chart 2Old Faithful

Old Faithful

Old Faithful

That pent-up demand will be goosed by abundant monetary and fiscal stimulus. We expect that China and the US will take the lead, and will have the most impact on global aggregate demand, but that policymakers in other major economies will also lend a hand. Central banks in Australia, Canada and England have all cut rates in the last two weeks, and British policymakers took the boldest step, pairing last week’s rate cut with an immediate 30-billion-pound infusion of emergency spending, and a pledge to spend 600 billion pounds on infrastructure upgrades between now and 2025.2 Australia announced a plan to inject fiscal stimulus equivalent to about 1% of GDP Thursday morning, and Germany’s ruling party indicated a willingness to run a budget deficit to combat the virus.3 Our China Investment Strategy team notes that the Chinese authorities are already supporting domestic demand via aid to threatened businesses and out-of-work individuals, and are poised to open the infrastructure taps (Chart 2). Global aggregate demand is also set to receive a boost from the oil plunge, although it will arrive with a lag. Energy sector layoffs and the tightening in monetary conditions from wider bond spreads and marginally tighter bank lending standards will exert an immediate drag on activity. Once that drag fades, however, the positive supply-shock effects will take hold, helping households stretch their paychecks and non-energy businesses expand their profit margins. Although the effect of falling oil prices is mixed for the US now that fracking has made it a heavyweight oil producer, more economies are oil importers than exporters, and global growth is inversely related to oil price moves. We are keenly aware that markets are paying no attention whatsoever to economic data releases right now. They are backward-looking, after all, and fundamentals are not the driving force behind current market moves anyway. The data are useful, however, for evaluating the fundamental backdrop once the non-stop selling abates, as it eventually will. When it becomes important to take the measure of the economy and where it’s headed, investors will be able to make a more informed judgment if they have a good read on how the economy was doing before it was exposed to the virus (Chart 3). Chart 3Layoffs Are Coming, But They Hadn't Started By Early March

Layoffs Are Coming, But They Hadn't Started By Early March

Layoffs Are Coming, But They Hadn't Started By Early March