Disasters/Disease

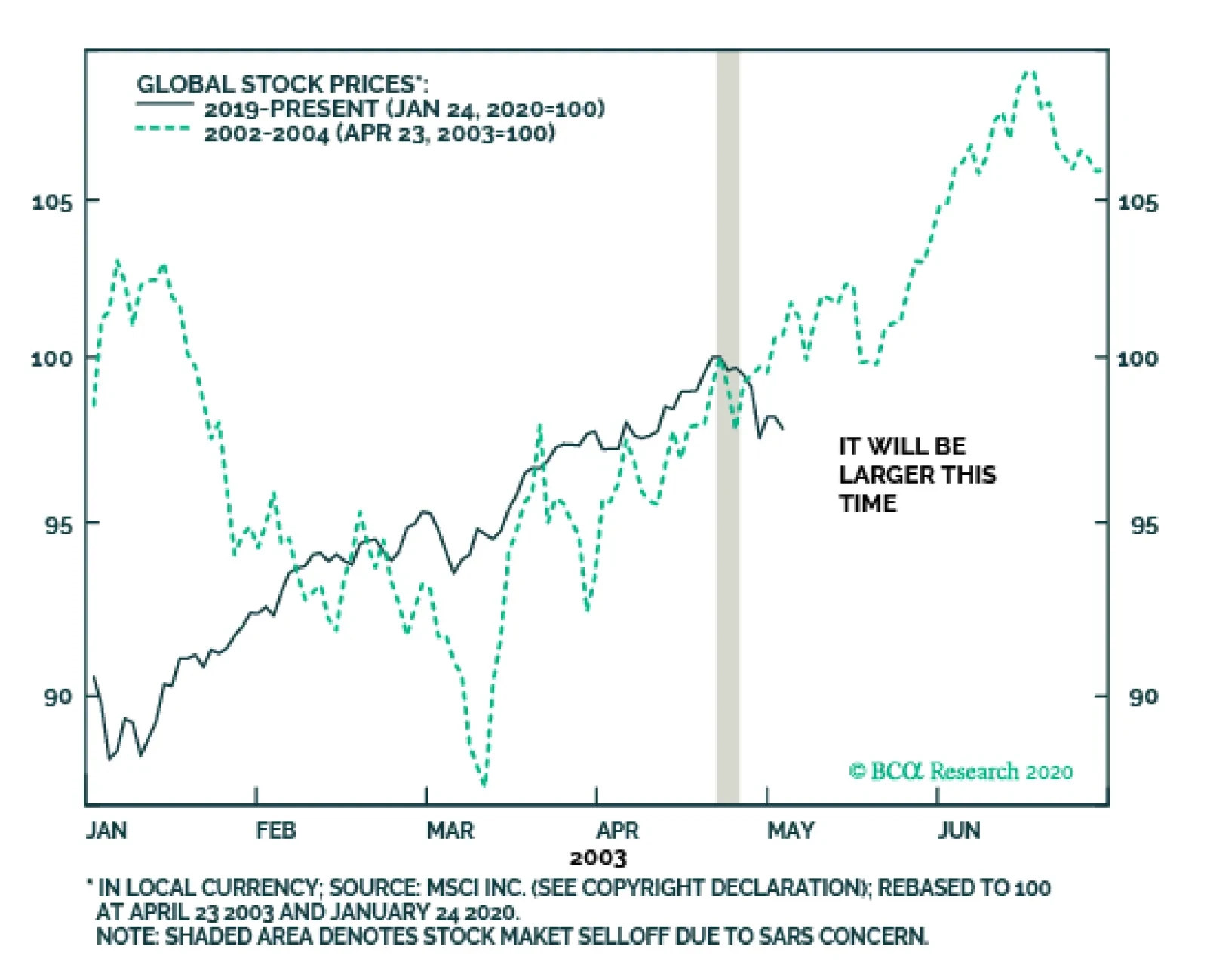

Highlights The SARS episode of 2003 suggests that the panic over the coronavirus will only subside when the number of new cases peaks. Although the latest data is somewhat encouraging, it is far from clear that we have reached that point. Provided the outbreak is contained, global equities should move higher over the course of the year. US companies remain net buyers of shares, implying that households and other holders have been net sellers. But against a backdrop of rising incomes, high savings, and improving confidence, households have also wanted to own more equities. How can households be net sellers of stocks while simultaneously increasing their equity exposure? There is only one answer: Share prices need to rise. The process will only stop once households decide they own enough stocks. In the US, while household equity holdings are on the high side as a share of household wealth, this is counterbalanced by the fact that the earnings yield on stocks is well above the yields on competing assets. Outside the US, household ownership of equities is quite low while the equity risk premium is still high. Going Viral We upgraded global equities after markets plunged in late 2018 and have remained overweight stocks on a 12-month horizon to this day. However, we indicated three weeks ago that equities had become technically overbought and would likely need to consolidate their gains. Thus, while we kept our 12-month views unchanged, we downgraded our tactical 3-month view on global stocks from overweight to neutral, while also advising clients with short horizons to boost exposure to cash and government bonds at the expense of riskier credit (our entire set of views can be found in the Global Investment Strategy View Matrix at the back of this report). Since then, the outbreak of the coronavirus has added another headwind to the near-term outlook for stocks. Many commentators have drawn comparisons between today’s outbreak and the SARS epidemic in 2003. The SARS episode imposed a significant but short-lived economic toll on the affected countries. While Chinese GDP growth fell to 3.4% in Q2 of 2003, it surged back to 15.7% in Q3, leaving the overall level of GDP down about 1% for the year as a whole relative to what would have transpired if the virus had never emerged.1 The broader Asia-Pacific region experienced a hit to growth of around 0.5%. In contrast, growth in developed economies was barely affected. Even in Canada, where 44 people died from SARS, the outbreak shaved only around 0.1% from the level of GDP in 2003, according to the Bank of Canada.2 The outbreak of the coronavirus has added another headwind to the near-term outlook for stocks. The obvious problem with the SARS analogy is that it is based on a sample of one. We do not know how this new strain of the virus compares to SARS or, for that matter, the Spanish flu, which killed 50-to-100 million people (3%-to-5% of the world’s population at the time). We do not even know if the full scope of the SARS outbreak was as fleeting as what we remember, since in a cosmic multiverse there will be a tendency to recall life-or-death outcomes more favorably than they actually were (I will have more to say about the financial implications of this in a future special report). Chart 1The Coronavirus Is Spreading Faster Than SARS Did

Buy The Dip, But Not Yet

Buy The Dip, But Not Yet

What we do know is that, to date, the coronavirus has spread more quickly than SARS (Chart 1). It is not clear if that is because of faster, more accurate reporting methods or because the virus is more communicable. The Chinese Minister of Health has said that this new virus, unlike SARS, can be transmitted while people are still asymptomatic. While others have cast doubt on this claim, if it turns out to be correct, the coronavirus may be much more difficult to control. Viruses often become less lethal as they mutate because a virus that kills its host is also a virus that kills itself. Unfortunately, in a world of mass travel, a virus can spread across the globe before it has time to lose potency. The typical seasonal flu kills less than 0.1% of those who contract it. Most estimates suggest that SARS killed 10%-15% of infected patients. The Spanish flu killed a similar percentage. The death rate from the coronavirus is currently tracking at 2%-to-3%. However, it is possible that this estimate will rise. The vast majority of the people who have contracted the coronavirus are still sick. In fact, more people have died from it than have fully recovered (Chart 2). Thus, an honest assessment would simply admit that we do not know how bad this potential pandemic will get. Chart 2How Will This End: Outbreak, Epidemic, Or Pandemic?

Buy The Dip, But Not Yet

Buy The Dip, But Not Yet

Chart 3Markets Bottomed As The SARS Infection Rate Was Peaking

Markets Bottomed As The SARS Infection Rate Was Peaking

Markets Bottomed As The SARS Infection Rate Was Peaking

What should investors do? The SARS experience suggests that risk assets will only bottom when the number of new cases peaks (Chart 3). It is not clear that we have reached this point yet. While the number of new cases reported by China’s National Health Commission has stabilized over the past two days, this could just be a temporary respite (Chart 4). Until the rate at which new cases are diagnosed begins a clear downward trend, a somewhat cautious stance towards risk assets is warranted. Global Growth Should Recover Provided the outbreak is contained during the coming weeks, global equities should move higher over the course of the year. This is partly because global growth should pick up thanks to the lagged effects of last year’s decline in bond yields, an improvement in the global manufacturing inventory cycle, and diminished Brexit and trade war risks. Continued fiscal/credit stimulus out of China should also help. China spends less on health care than almost all other countries (Chart 5). It is likely that the past few weeks will prompt the government to increase social spending. Chart 4The Number Of New Cases Has Stagnated Over The Past Two Days

Buy The Dip, But Not Yet

Buy The Dip, But Not Yet

Chart 5China: Public Spending On Health Care Has Room To Catch Up

Buy The Dip, But Not Yet

Buy The Dip, But Not Yet

Higher Equity Prices: Just A Matter Of Arithmetic? Chart 6There Is A Structural Decline In Listed Companies In The US

There Is A Structural Decline In Listed Companies In The US

There Is A Structural Decline In Listed Companies In The US

Chart 7The Supply Of US Stocks Has Been Drying Up

The Supply Of US Stocks Has Been Drying Up

The Supply Of US Stocks Has Been Drying Up

In addition to stronger global growth, there is another factor supporting stocks which receives insufficient attention and is worth highlighting in this week’s report: corporate buybacks. US companies have repurchased about 3% of their shares every year for the past decade. On the flipside, only 110 companies went public last year, less than a third of the number of new listings in 1996-99. In fact, the number of publicly traded domestic companies has fallen by over 40% since 1996 (Chart 6). The combination of copious buybacks and dearth of IPOs has caused the S&P divisor – a broad measure of the total number of split-adjusted shares outstanding – to decline by a cumulative 9% since 2011. Between 1990 and 2004, the divisor increased by 40% (Chart 7). If companies are net buyers of stocks, then households and other holders must be net sellers of stock. But this raises an obvious question: What if households also want to be net buyers of stocks? Chart 8Households Are Bullish

Households Are Bullish

Households Are Bullish

Chart 9High Equity Ownership By Households Translates Into Poor Long-Term Returns

High Equity Ownership By Households Translates Into Poor Long-Term Returns

High Equity Ownership By Households Translates Into Poor Long-Term Returns

This question is highly relevant in today’s environment, where unemployment is low, wage growth is accelerating, the household savings rate is high, consumer confidence is strong, and a higher-than-average percentage of people expect stocks to increase in the coming months (Chart 8). Arithmetically, there is only one way that households can be net sellers of stocks while simultaneously increasing their equity exposure: Share prices need to rise. At what point will share prices stop rising? That depends on two things: 1) How much stock market wealth households hold relative to other assets; and 2) The risk-adjusted rate of return that households expect from stocks compared to other assets. Stock returns are highest when equity holdings are low, but sentiment towards stocks is improving. Conversely, returns are lowest when equity holdings are high, but stock market sentiment is deteriorating (Chart 9 and Table 1). Table 1Equity Returns Tend To Suffer When Bulls Are Losing Conviction

Buy The Dip, But Not Yet

Buy The Dip, But Not Yet

The latter typically occurs during economic downturns when earnings are falling and risk aversion is rising. Thus, it is no surprise that recessions and equity bear markets tend to overlap (Chart 10). Chart 10Recessions And Bear Markets Tend To Overlap

Recessions And Bear Markets Tend To Overlap

Recessions And Bear Markets Tend To Overlap

Where Things Stand Today In the US, household equity holdings are on the high side. According to Fed data and our own estimates, households currently hold 33% of their financial assets in stocks (Chart 11). This is higher than in 2007, but still below the dotcom peak of 39%. Similarly, the monthly asset allocation survey conducted by the American Association of Individual Investors shows a somewhat elevated allocation to equities, although one that is still broadly on par with the 2003-2007 and post-2014 averages (Chart 12). Chart 11US Household Equity Holdings Are On The High Side (I)

US Household Equity Holdings Are On The High Side (I)

US Household Equity Holdings Are On The High Side (I)

Chart 12US Household Equity Holdings Are On The High Side (II)

US Household Equity Holdings Are On The High Side (II)

US Household Equity Holdings Are On The High Side (II)

Chart 13Relative Valuations Favor Stocks

Relative Valuations Favor Stocks

Relative Valuations Favor Stocks

One major difference with prior occasions when US equity allocations were elevated is that the earnings yield on stocks at present is still quite a bit higher than the yield on competing assets such as cash and bonds (Chart 13). While this is mainly because interest rates are so low, it does suggest that households may seek to further increase their equity allocations provided that the economy continues to perform well. Foreign companies have been less aggressive re-purchasers of their own shares than their US peers. That said, household equity ownership is significantly lower outside the US (Chart 14). The spread between equity earnings yields and bond yields is also higher abroad, reflecting the fact that both PE multiples and interest rates are generally lower outside the US. Given that investors tend to favor companies listed in their home country, efforts by non-US investors to increase their equity allocations will primarily benefit stock markets outside the US. In addition, stronger global growth tends to favor EM and European equities, largely because stock markets in those regions have more of a cyclical bent (Chart 15). Thus, on balance, we recommend that investors overweight non-US stocks this year. Chart 14Equity Ownership By Households Is Lower Outside The US

Buy The Dip, But Not Yet

Buy The Dip, But Not Yet

Chart 15Stronger Global Growth Tends To Favor A Cyclical Bias In Equity Allocation

Stronger Global Growth Tends To Favor A Cyclical Bias In Equity Allocation

Stronger Global Growth Tends To Favor A Cyclical Bias In Equity Allocation

Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 Jong-Wha Lee and Warwick J. McKibbin, “Globalization and Disease: The Case of SARS,” Brookings Institution, dated February 2004. 2 Please see Monetary Policy Report, Bank of Canada, October 2003. Global Investment Strategy View Matrix

Buy The Dip, But Not Yet

Buy The Dip, But Not Yet

MacroQuant Model And Current Subjective Scores

Buy The Dip, But Not Yet

Buy The Dip, But Not Yet

Strategic Recommendations Closed Trades

It is tempting to compare the potential impact of the current coronavirus outbreak on the global economy and financial markets with that of SARS in the spring of 2003. The correction in global equities due to the SARS outbreak lasted only a couple of days…

The coronavirus scare is the catalyst for the recent correction. The true cause is that the stock market had reached a point of groupthink-triggered instability and therefore needed the slightest catalyst to correct. The bond yield 6-month impulse had…

Highlights Collective market signals suggest a low but non-negligible probability of a dollar spike due to the coronavirus. Stay long the yen as a portfolio hedge. Short CHF/JPY bets also make sense. Our limit sell on the gold/silver ratio was triggered at 90. Place a stop at 95, with an initial target of 80. Feature Chart I-1Watching Market Signals

Watching Market Signals

Watching Market Signals

Investors can generally be classified in two camps. There are those who are predisposed to being risk averse. As such, capital preservation trumps the desire for outsized returns. For such investors, defensive equities such as staples and utility stocks, fixed-income assets, or even gold tend to be the favored vehicles over time. At the opposite end of the spectrum are the investors who desire hopping on and riding the next growth unicorn. Their favored investment universe can include technology and biotech concerns, but can also span industries such as automotive and food. The key, however, is that their inherent disposition is to multiply returns rather than preserve capital. There is a crucial difference between this bias and a risk-on/risk-off environment. For example, in a risk-on environment, the more prudent investor might choose high-yielding government bonds, while the high flyer will be in the S&P 500 or private equity. In the currency world, the “preservationist” might choose the euro as an anti-dollar play despite negative yields, while the “high flyer” would rather be in the New Zealand dollar or the Norwegian krone. The oscillation between these two bipolar universes can be measured in various ways, but one that has been prescient in gauging the direction for currency markets is the ratio between the S&P 500 index and gold prices. In general, whenever the S&P 500 has been outperforming gold, the dollar has tended to soar, and vice versa (Chart I-1). As a closed economy, US markets are generally more defensive. So even in a risk-off environment, this ratio can capture the preference for capital preservation versus growth. The collective signals from financial markets suggest there is a low probability of a dollar spike. The SPX/Gold ratio hit a peak of 2.5 in the last quarter of 2018 and has since been exhibiting a bearish pattern of lower highs, with the latest rise peaking a nudge below 2.2. Our belief is that it is less a story of greed versus fear, and more an indication of a powerful underlying preference for investors being revealed in asset prices. Gauging FX Market Signals The coronavirus outbreak has been dominating market headlines in recent weeks. We are not infectious disease specialists, so cannot provide any insight on the potential impact on growth and/or the probability for the virus to become much more widespread. However, the collective signals from financial markets suggest there is a low probability of a dollar spike. The rise in the dollar has been relatively on par with the SARS experience of 2002 (Chart I-2A and Chart I-2B). Back then, the Chinese economy had a much smaller effect on global growth, and so far, the number of reported cases is outpacing the SARS experience. So, it is possible that given the dollar bull market of the last decade or so, there is a dearth of new buyers in the greenback. Chart I-2ARun Of The Mill Virus ? (1)

Run Of The Mill Virus ? (1)

Run Of The Mill Virus ? (1)

Chart I-2BRun Of The Mill Virus ? (2)

Run Of The Mill Virus ? (2)

Run Of The Mill Virus ? (2)

The most recent fall in the S&P 500 index versus gold is definitely a sign of risk aversion, but the much broader peak almost two years ago might be signaling an outright shift in the investment universe. In other words, capital preservation might now be best sought outside US bourses. If this is the case, cheap and unloved value stocks will provide better shelter compared to the growth champions of the last decade. It is interesting that emerging market cyclical stocks (where the epicenter of the crisis is) have not underperformed defensives in a meaningful way during the latest riot (Chart I-3). The typical narrative is that the dollar is now a high-yielding currency within the G10. That means it has now become the object of carry trades. Should the investment universe be shifting to one of prudence, it is plausible though not probable that the greenback will provide both functions. Chart I-3Mixed Message From Cyclicals Versus Defensives

Mixed Message From Cyclicals Versus Defensives

Mixed Message From Cyclicals Versus Defensives

Chart I-4Correlation Break Down Or Unsustainable Gap?

Correlation Break Down Or Unsustainable Gap?

Correlation Break Down Or Unsustainable Gap?

The absolute collapse in the gold-to-bond ratio further confirms that after almost a decade of underperformance, hard money might be coming back into favor versus yield plays (Chart I-4). Gold was a monetary aggregate for centuries, and continues to stand as a viable threat to dollar liabilities. This is not only visible in the rampant accumulation of gold by foreign central banks, notably Russia and China, but also by the breakout in gold in almost every currency, including safe-havens like the Swiss franc and the Japanese yen (Chart I-5). The absolute collapse in the gold-to-bond ratio further confirms that after almost a decade of underperformance, hard money might be coming back into favor. Data from the US Treasury confirms that foreign entities have been fleeing US bond markets at among the fastest pace in recent years. On a rolling 12-month total basis, the US saw an exodus of about US$250 billion in Treasurys from foreigners, one of the largest on record (Chart I-6). Foreign private investors are still net buyers of US Treasurys, but the downtrend in purchases in recent years is evident. In addition, this helps explain why gold has also outperformed Treasurys over this period. Chart I-5Soft Versus Hard ##br##Money

Soft Versus Hard Money

Soft Versus Hard Money

Chart I-6Official Data Shows Less Preference For Treasurys

Official Data Shows Less Preference For Treasurys

Official Data Shows Less Preference For Treasurys

The US dollar’s reserve status remains intact for now. But subtle shifts in this exorbitant privilege are worth monitoring. If balance-of-payment dynamics continue to head in the wrong direction, as they are now, this will favor hard money and non-US assets, while accelerating divestment out of US Treasurys. This is irrespective of whether we enter a risk-on versus risk-off environment. A good proxy for whether the US government was prudent or profligate over the past four decades can be measured by the gap between unemployment relative to NAIRU (the so-called unemployment gap) and the corresponding budget deficit. In simple terms, full employment should be accompanied by balanced budgets, while governments can step in during recessions to put a floor under aggregate demand. Not surprisingly, using this simple rule, sound fiscal policies in the US were usually accompanied by a strong dollar, and vice versa. Chart I-7The Risk To Long Dollar Positions

The Risk To Long Dollar Positions

The Risk To Long Dollar Positions

Over the next five years, the US Congressional Budget Office (CBO) estimates that the US budget deficit will swell to 4.6% of GDP. Assuming the current account deficit remains stable, this will pin the twin deficits at 7.2% of GDP. This assumes no recession, which would have the potential to boost the deficit even further. In the last forty years, there has not been any prolonged period where twin deficits in the US have been expanding while the dollar has been in a bull market (Chart I-7). In a nutshell, even though the coronavirus is dominating headlines, the lack of a more pronounced greenback strength can be pinpointed to a rising number of negative market signals. Our bias is that when this eventually rolls over and global growth picks up in earnest, dollar bulls may be forced to capitulate. Bottom Line: We are not downplaying the potential impact of the coronavirus, but are skeptical of its ability to catapult the dollar higher. We are short the DXY index, with a target of 90 and a stop at 100. Stick with it. Bullish Both Gold And Silver, But Go Short The GSR If we are right, then both gold and silver will tend to rise in an environment where the dollar is falling. That said, the gold/silver ratio (GSR) hit a three-decade high of 93.3 last summer, opening up an arbitrage opportunity. The history of these reversals is that they tend to be powerful, quick, and extremely volatile (Chart I-8). This not only paves the way for an excellent entry point to short gold versus silver, but provides important information on the battleground between easing financial conditions and a pick-up in economic (or manufacturing) activity. The ratio of the velocity of money between the US and China has tended to track both the gold/silver ratio and the dollar closely. Just like gold, silver benefits from low interest rates, plentiful liquidity, and the incentive for fiat money debasement. However, the gold/silver ratio is sitting near two standard deviations above its mean. Meanwhile, over the past century, the peak in GSR has been around 100. The gold/silver ratio tends to rally ahead of an economic slowdown, but then peaks when growth is still weak but liquidity conditions are plentiful enough to affect the outlook for future growth. This appears to be the case today. The simple reason is that silver has more industrial uses than gold (Chart I-9). Chart I-8GSR At A Speculative Extreme

GSR At A Speculative Extreme

GSR At A Speculative Extreme

Chart I-9No Recession = Buy Silver

No Recession = Buy Silver

No Recession = Buy Silver

The ratio of the velocity of money between the US and China has tended to track both the gold/silver ratio and the dollar closely (Chart I-10). A falling ratio signifies that the number of times money is changing hands in China is outpacing that number in the US. This also tends to coincide with a preference for US versus non-US assets, since animal spirits (as measured by money velocity) tend to be pronounced in places where returns on capital are higher. Silver is a more volatile metal than gold. Part of the reason is that the silver market is thinner, with future open interest that is about one-third that of gold. As such, silver tends to rise faster than gold during precious metal bull markets (Chart I-11). Chart I-10Falling GSR = Rising Manufacturing Activity

Falling GSR = Rising Manufacturing Activity

Falling GSR = Rising Manufacturing Activity

Chart I-11Silver Is More Volatile Than Gold

Silver Is More Volatile Than Gold

Silver Is More Volatile Than Gold

This brings us to the sweet spot for silver. Even if global growth remains tepid over the next few months, due to a rise in infections from the coronavirus, a lot of the bad news is already reflected in a high GSR. This means the potential for upside will have to be nothing short of a deep recession. Relative speculative positioning favors gold, which is positive from a contrarian standpoint. Ditto for relative sentiment. More often than not, a positive signal from both these indicators has been a good timing tool for a selloff in the GSR. If global growth bottoms, then the rise in silver prices could be explosive. Silver fabrication demand benefits from new industries such as solar and a flourishing “cloud” industry that are capturing the new manufacturing landscape. Meanwhile, we are also entering a window where any pickup in demand could lead to a sizeable increase in the physical silver deficit. Bottom Line: A falling GSR provides important information about the battleground between easing financial conditions and a pickup in economic activity. We remain bullish on both gold and silver, but a trading opportunity has opened up for a short GSR position. Housekeeping Chart I-12AUD Will Follow Asian Currencies

AUD Will Follow Asian Currencies

AUD Will Follow Asian Currencies

Our limit buy on the Australian dollar was triggered at 68 cents. We discussed the Aussie at length in our report dated January 17.1 Place an initial target at 0.75 cents and a tight stop at 0.66. The near-term risk to this trade is any escalation in virus infections that will collectively send Asian currencies into a tailspin (Chart I-12). Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy Weekly Report, titled "On AUD And CNY," dated January 17, 2020, available at fes.bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the US have been positive: The Markit manufacturing PMI fell to 51.7 while the services component increased to 53.2 in January. The Dallas Fed manufacturing index improved from -3.2 to -0.2 in January. Moreover, the Richmond Fed manufacturing index soared to 20 in January. Durable goods orders increased by 2.4% month-on-month in December. The trade deficit widened further to $68.3 billion from $63 billion in December. Annualized GDP growth was unchanged at 2.1% year-on-year in Q4. Initial jobless claims fell to 216K from 223K for the week ended January 24th. The DXY index appreciated by 0.1% this week. While the coronavirus spurred worries about a further slowdown in the global economy, the impact on the US remains to be seen. On Wednesday, the Fed committee voted unanimously to keep interest rates on hold at 1.75% and concluded that the current rate is appropriate to support sustained expansion of the US economy. Report Links: Portfolio Tweaks Before The Chinese New Year - January 24, 2020 On Oil, Growth And The Dollar - January 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area have been mostly positive: The Markit manufacturing PMI jumped to 47.8 in January while the services PMI fell slightly to 52.2. The German IFO current assessment index increased to 99.1 from 98.8 in January, while expectations component fell to 92.9. The economic sentiment indicator increased to 102.8 from 101.3 in January. The unemployment rate fell further to 7.4% in December from 7.5% the prior month. The euro has been flat against the US dollar this week. Though the German IFO expectations component disappointed, the overall assessment has shown tentative signs of recovery. More importantly, changes in the manufacturing PMI indices, especially in Germany, are staging the V-shaped recovery we have been expecting. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 On Money Velocity, EUR/USD And Silver - October 11, 2019 A Few Trade Ideas - Sept. 27, 2019 Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been positive: Consumer confidence was unchanged at 39.1 in January. Services PPI increased by 2.1% year-on-year in December. Headline inflation increased to 0.8% year-on-year from 0.5% in December. Both manufacturing and services PMIs increased to 49.3 and 52.1, respectively in January. The Japanese yen appreciated by 0.6% against the US dollar this week. The flare up in risk aversion was a very potent catalyst, given the yen had become unloved and under owned. Persistent global risks, including Mid East tensions, and more recently, the spread of coronavirus, all warrant holding the Japanese yen as a portfolio hedge. Our last weekly report discussed why we prefer the Japanese yen to the Swiss franc as portfolio insurance. Report Links: Portfolio Tweaks Before The Chinese New Year - January 24, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Signposts For A Reversal In The Dollar Bull Market - November 1, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the UK have been solid: Both Markit manufacturing and services PMIs soared to 49.8 and 52.9 respectively in January. Nationwide housing prices increased by 1.9% year-on-year in January, compared with 1.4% the previous month. The saucer-shaped bottom in home prices is becoming more and more evident. The British pound has been flat against the US dollar this week. On Thursday, the BoE decided to leave interest rates unchanged at 0.75%. The fact that there were only two dissenters, in line with the previous month, suggests that rising bets for a rate cut were misplaced. The UK is due to leave the EU as of January 31st and enter a transition period that is supposed to last until December 31st 2020. The immediate aftermath of the exit will be business as usual. Trading strategy on the pound should be a buy on dips. We will continue to explore opportunities in GBP in upcoming reports. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 A Few Trade Ideas - Sept. 27, 2019 United Kingdom: Cyclical Slowdown Or Structural Malaise? - Sept. 20, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been mixed: The NAB business conditions index fell to 3 from 4 in December. Moreover, the business confidence index decreased to -2 from 0. Headline inflation increased to 1.8% year-on-year from 1.7% in the fourth quarter. Import prices increased by 0.7% quarter-on-quarter, while export prices plunged by 5.2% quarter-on-quarter in Q4. The Australian dollar fell by 2.1% against the US dollar this week, triggering our limit buy position at AUD/USD 0.68. Despite temporary challenges from the bushfires and the coronavirus, we continue to hold our base case view that global growth is likely to rebound in the next 12-to-18 months, which is bullish for the Aussie dollar. Report Links: On AUD And CNY - January 17, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 A Contrarian View On The Australian Dollar - May 24, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been positive: Headline inflation increased to 1.9% year-on-year in Q4, compared with 1.5% the previous quarter. It also beat expectations of 1.8%. The trade balance shifted to a surplus of NZ$547 million in December. Goods exports rose by 4.8% year-on-year to NZ$5.5 billion, while imports fell by 5.4% year-on-year to NZ$5 billion. Shortly after the rise along with inflation data, the New Zealand dollar fell by more than 2% this week, amid growing risk aversion. New Zealand, as a chief exporter of agricultural products, bore a good brunt of speculative selling. Assuming infections peak in the coming weeks, we remain positive on the kiwi as the Chinese government is likely to inject more stimulus into the economy. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Place A Limit Sell On DXY At 100 - November 15, 2019 USD/CNY And Market Turbulence - August 9, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been mostly positive: Retail sales increased by 0.9% month-on-month in November. The Bloomberg Nanos confidence index rose to 56.5 from 56.1 for the week ended January 24th. The Canadian dollar fell by 0.6% against the US dollar this week. As a petrocurrency, the risk of much reduced travel hit the loonie. We have written at length in various reports about the loonie, but the bottom line is that Canada benefits less than other petrocurrencies in oil bull markets. Ergo, the underperformance of short CAD/NOK and long AUD/CAD positions this week is expected. In other news, Trump has signed the new USMCA bill into law this week, leaving Canada the only member of the trilateral deal that has yet to ratify the agreement. Report Links: The Loonie: Upside Versus The Dollar, But Downside At The Crosses Updating Our Balance Of Payments Monitor - November 29, 2019 Making Money With Petrocurrencies - November 8, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been mixed: The trade surplus narrowed for a fourth consecutive month in December, falling to CHF 2 billion. Real exports decreased by 3.4% month-on-month while real imports grew by 0.2% month-on-month. The ZEW expectations index fell to 8.3 from 12.5 in January. The KOF leading indicator jumped to 100.1 from 96.2 in January. The Swiss franc has been more or less flat against the US dollar this week. The fall in exports of chemical and pharmaceutical production was the main driver behind the decrease in the Swiss trade balance in December. The SNB is walking a fine line. The improvement in the KOF leading indicator, along with rising inflation and PMI data is definitely a source of comfort, but the surge in EUR/CHF will hurt competitiveness and warrant stealth intervention. Buy EUR/CHF at 1.06. Report Links: Portfolio Tweaks Before The Chinese New Year - January 24, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Notes On The SNB - October 4, 2019 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Recent data in Norway have been negative: Retail sales fell by 2% month-on-month in December. The Norwegian krone fell by 1.9% against the US dollar this week. The WTI crude oil price plunged by 20% since the peak earlier this month, due to a combination of falling global travel demand, eased Iran tensions and a bearish EIA inventory report. That being said, our Commodity & Energy strategists continue to be bullish energy prices and expect the WTI crude oil price to reach $63/bbl in 2020, based on recovering global demand and supply constraints. This should eventually lift the Norwegian krone. OPEC is scheduled to meet early March, and plunging prices could be a catalyst for the cartel to cut production. Report Links: On Oil, Growth And The Dollar - January 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Making Money With Petrocurrencies - November 8, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been mixed: Producer prices increased by 1.3% year-on-year in December. The trade surplus shrank to SEK 0.3 billion from SEK 2.7 billion in December. Retail sales grew by 3.4% year-on-year in December. Consumer confidence marginally fell to 92.6 from 94.7 in January, while business confidence jumped to 97.4 in January, the highest in seven months. The Swedish krona fell by 1.3% against the US dollar this week. Recent Swedish data has been disappointing given the steep decline during the trade war, but we are beginning to see second-derivative improvements. The trade surplus is rising on a year-on-year basis. Particularly noteworthy was the improvement in business confidence, which has historically led the Swedbank PMI index tick for tick. Report Links: Updating Our Balance Of Payments Monitor - November 29, 2019 Where To Next For The US Dollar? - June 7, 2019 Balance Of Payments Across The G10 - February 15, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights China’s economic rebound in Q1 will be delayed due to the coronavirus, which will have a larger negative hit than SARS. New stimulus measures will assist a rebound in demand later this year. Europe remains a geopolitical opportunity rather than a risk. As long as global growth rebounds this year, European equities can outperform their richly valued American counterparts. Emerging markets face a new headwind from the coronavirus. Emerging market performance relative to developed markets will be a key test of whether endogenous growth trends are taking shape. Tactically – over a 12-month horizon – we remain long industrial commodities; long Korean equities versus Taiwanese; and long Malaysian equities relative to emerging markets. Feature Global equities will ultimately push through the coronavirus and the Democratic Party primary election, but risks are elevated and Q1 looks to bring significant volatility. Last week we shifted to a tactically neutral stance on risk assets but we remain cyclically bullish. In this report we update our market-based GeoRisk indicators, which are almost all set to rise from low levels in the coming months as developed market equities and emerging market currencies face higher risk premiums. China: The Year Of The Rat Chart 1Markets Will Rebound Once Toll Of Virus Peaks

Markets Will Rebound Once Toll Of Virus Peaks

Markets Will Rebound Once Toll Of Virus Peaks

The ink had hardly dried on our “Black Swan” report for 2020 when Chinese scientists confirmed human-to-human transmission of the Wuhan coronavirus (2019-nCoV), sending a wave of fear over China and the world. The number of new cases and new deaths is rising and economic activity will suffer as the Chinese New Year is extended, shoppers stay home, and international travel is canceled. The virus is likely to prove more troublesome than stock investors want to admit, at least in the short term. Too little is known to make confident assertions about promptly containing the virus or its impact on global economy and markets. The analogy with the SARS outbreak of 2003 is limited: it is not certain that this virus has a lower death rate, but it is certain that the Chinese economy is more vulnerable to disruption today than at that time – and much more influential on the global economy. The SARS episode is useful, however, in suggesting that the market will not rebound until the number of new cases and deaths turn down (Chart 1). Assuming the virus is ultimately contained – both in China and in neighboring Asian countries whose governments may not be as effective at quarantining the problem – regional consumption and production will bounce back. New stimulus measures will also take effect with a lag. Domestic political risk is structurally understated in China. Stimulus will indeed be the answer. First, the negative shock to consumer demand comes at a time when global trade is still relatively weak, thus presenting a two-pronged threat to China’s economy, which was only just stabilizing after the truce in the trade war. Second, China’s hundredth anniversary of the Communist Party, in 2021, will require the government to stabilize the economy now. The important political leadership reshuffle at the twentieth National Party Congress in 2022 is another imperative to avoid a deepening slump today (Chart 2). Chart 2China Will Stimulate To Avoid A Deepening Slump

China Will Stimulate To Avoid A Deepening Slump

China Will Stimulate To Avoid A Deepening Slump

Beyond 2020, the Wuhan virus highlights our theme that domestic political risk is structurally understated in China. At the centennial celebration, China’s leaders aim to show that the country is a “moderately prosperous society in all respects,” emphasis added. For decades China’s leaders have emphasized industrial production to the detriment of other social and economic goals, such as food safety and a clean and safe environment for households to live in. The emergence of the middle class, writ broadly, as a majority of the population is a persistent source of pressure on leaders, as the limited opinion polling available from China demonstrates (Chart 3). In other emerging markets, a large middle class has led to social and political change when the government failed to meet growing middle class demands (Chart 4). Chart 3Chinese Social And Economic Conditions Are Source Of Pressure

GeoRisk Update: The Year Of The Rat

GeoRisk Update: The Year Of The Rat

Chart 4Consumerism Encourages Democracy

Consumerism Encourages Democracy

Consumerism Encourages Democracy

Chart 5China’s Government Is Behind The Curve

GeoRisk Update: The Year Of The Rat

GeoRisk Update: The Year Of The Rat

Under General Secretary Xi Jinping, the government has cracked down on corruption and pollution as well as poverty, and has attempted to improve consumer safety and the health care system. The party officially aims to shift its policy focus from meeting the basic material needs of the population to improving quality of life. The problem is that China’s government is behind the curve (Chart 5). While it is making rapid progress – for instance, the communicable disease burden has dropped dramatically – and has unique authoritarian tools, acute problems of health, food safety, pollution, and public services will nevertheless persist. The government’s responses will inevitably fall short from time to time and heads will roll. Crisis events create the potential for the market to be surprised by the level of domestic political change or pushback, which will prove disruptive at times. Bottom Line: China’s economic rebound in Q1 will be delayed due to the coronavirus, which will have a larger negative hit than SARS. The SARS episode suggests that Chinese equities will be a tactical buy when the number of new cases and deaths begin falling. New stimulus measures will assist a rebound in demand later this year – underscoring our constructive cyclical view on Chinese and global growth. The episode highlights the challenges China faces in modernizing and improving regulations, health, and safety for the emerging middle class. Domestic political risk is understated. Europe: Political Risks Still Contained China’s near-term hit, and rebound later this year, will echo in Europe, where the economy and equity market are highly reliant on China’s credit cycle and import demand. Politically, however, Europe remains a geopolitical opportunity rather than a risk (Chart 6). Chart 6China's Hit Will Echo In Europe, But Political Risks Are Contained There

GeoRisk Update: The Year Of The Rat

GeoRisk Update: The Year Of The Rat

The final months of last year saw the biggest and most immediate political risk – a disorderly UK exit from the EU – removed. The Trump administration is not likely to slap large-scale tariffs – such as auto tariffs on a national security pretext – because Trump is constrained by the weak manufacturing sector in advance of his election. Meanwhile immigration and terrorism have declined since 2016, draining the fuel of Europe’s anti-establishment parties. Pound weakness during the Brexit transition period is an opportunity for investors to buy. Chart 7Immigration Is Ticking Up, But From Low Levels

Immigration Is Ticking Up, But From Low Levels

Immigration Is Ticking Up, But From Low Levels

Chart 8Refugees Will Favor Western Route Across The Mediterranean

Refugees Will Favor Western Route Across The Mediterranean

Refugees Will Favor Western Route Across The Mediterranean

Chart 9Government Gridlock, Catalonia, And Poor Reform Momentum Will Pull Up Spanish Risk

Government Gridlock, Catalonia, And Poor Reform Momentum Will Pull Up Spanish Risk

Government Gridlock, Catalonia, And Poor Reform Momentum Will Pull Up Spanish Risk

There are some signs of immigration numbers ticking up, but from very low levels (Chart 7). This uptick must be monitored for Spain (and France), as the renewed civil war in Libya is forcing refugees to shift to the western route across the Mediterranean (Chart 8). (Note that even peace in Libya opens the possibility of greater migrant flows as the country then becomes a viable transit route again). Our Spanish risk indicator is already ticking up due to government gridlock, the Catalonian conflict, and a declining commitment to structural economic reform (Chart 9). But this is not a major concern for global investors. The United Kingdom The UK will formally exit the European Union on January 31. The transition period – in which the UK remains fully integrated into the EU single market – expires on December 31, 2020. This is the official deadline for the two sides to negotiate a trade agreement – though it can, and likely will, be delayed. Chart 10British Political Risk Will Revive, But Not Dramatically

British Political Risk Will Revive, But Not Dramatically

British Political Risk Will Revive, But Not Dramatically

The trade agreement is intended to minimize the negative economic impact of Brexit while ensuring that the UK reclaims its sovereignty and the EU retains the integrity of the single market. As negotiations get under way, the pound will face a new round of volatility and British political risk will revive somewhat, but we do not expect a dramatic increase (Chart 10). Ultimately we see pound weakness as an opportunity for investors to buy. The twin risks of no-deal Brexit or a socialist Jeremy Corbyn government have been decisively cast off. The end-of-year deadline can be extended and the two sides can find technical ways to compromise over regulations, tariffs, and border checks. Challenges to global growth only make an amicable solution more obtainable. Italy Our Italian GeoRisk indicator is collapsing as political risks proved yet again to be overstated (Chart 11). Chart 11Italian GeoRisk Indicator Is Collapsing

Italian GeoRisk Indicator Is Collapsing

Italian GeoRisk Indicator Is Collapsing

The local election in Emilia-Romagna was hyped as a major populist risk, in which the chief anti-establishment players, Matteo Salvini and the League, would take power in a region viewed as the symbolic home of the Italian left wing. Instead, the League lost, the ruling Democratic Party won, and the current government coalition will survive. While the populists prevailed at another election in Calabria, this outcome was fully expected. The trend of recent provincial elections does not suggest a swell of Italian populism (Chart 12). Chart 12Recent Local Elections Do Not Suggest A Swell Of Italian Populism

GeoRisk Update: The Year Of The Rat

GeoRisk Update: The Year Of The Rat

Chart 13The Italian Coalition Will Not Rush To Elections

The Italian Coalition Will Not Rush To Elections

The Italian Coalition Will Not Rush To Elections

This local election is not the end of the coalition’s troubles. The left-wing, anti-establishment Five Star Movement is suffering in the polls as a result of its uninspiring, politically expedient pairing with the establishment Democrats. The Democrats may receive a boost from Emilia-Romagna but the Five Star’s leadership change – the resignation of party leader Luigi di Maio – will not be enough to revive its fortunes alone. A new Five Star leader will have to decide whether to collaborate more deeply with the Democrats or try to reclaim the party’s anti-establishment credentials. The latter would push the coalition toward an election before too long. But the Five Star’s weak polling – and the League’s persistent 10 percentage point lead over the Democratic Party in nationwide polling – suggests that the coalition will not rush to elections but will try to prepare by passing a new electoral law (Chart 13). What is clear is that the Five Star Movement will not court elections until they improve their polling. France In France, Emmanuel Macron and his ruling En Marche party have seen their popularity drop to new lows amid the historic labor strikes in opposition to Macron’s pension reforms (Chart 14). Macron’s current trajectory is dangerously close to that of his predecessor, Francois Hollande, and threatens to turn him into a lame duck. We doubt this is the case. Chart 14Macron’s Popularity Is On A Dangerous Trajectory

GeoRisk Update: The Year Of The Rat

GeoRisk Update: The Year Of The Rat

Diagram 1The ‘J-Curve’ Of Structural Reform

GeoRisk Update: The Year Of The Rat

GeoRisk Update: The Year Of The Rat

We view Macron’s decline as another example of the “J-Curve of Structural Reform,” in which a leader’s political capital drops amid controversial reforms (Diagram 1). If the leader avoids an election during the trough of the curve, the danger zone, then his or her political capital may well revive after the benefits of the structural reform are recognized. In this case, the reform is neutral for France’s budget deficit – a cyclical positive – but it encourages an improvement in pension sustainability by incentivizing workers to work longer and postpone retirement – a structural positive. Chart 15France's Economy Is Holding Up

France's Economy Is Holding Up

France's Economy Is Holding Up

Chart 16A Relatively Strong Economy Will Buffer Against Political Risk In France

A Relatively Strong Economy Will Buffer Against Political Risk In France

A Relatively Strong Economy Will Buffer Against Political Risk In France

Municipal elections in March will not go Macron’s way, but the presidential and legislative elections are not until 2022. France’s GDP growth is holding up better than that of its neighbors, wages are rising, and confidence did not collapse amid the Christmas labor strike (Chart 15). Hence we expect the increase in political risk to be manageable (Chart 16), a boon for French equities. Germany German political risk is set to rise from today’s depths (Chart 17). The country faces a major shift: globalization is structurally declining and Chancellor Angela Merkel is stepping down. Merkel’s heir-apparent, Annegret Kramp-Karrenbauer (AKK), is floundering in the opinion polls (Chart 18). Chart 17German Political Risk Will Rise

German Political Risk Will Rise

German Political Risk Will Rise

Chart 18Merkel's Heir-Apparent Is Floundering In The Opinion Polls

Merkel's Heir-Apparent Is Floundering In The Opinion Polls

Merkel's Heir-Apparent Is Floundering In The Opinion Polls

Thus intra-party struggle, and conceivably even a rare early election, could emerge. But the US-China trade ceasefire offers a temporary reprieve. Next year will be different, with elections looming in the fall and the potential for a Trump reelection to trigger a second round of the US-China trade war or to shift to trade war with the EU and tariffs on German cars. The overall political trend in Germany is centrist and pro-Europe, and most of the parties are becoming more willing to upgrade fiscal policy over time. South Korea’s economic problems are priced in, while the market is dismissing Taiwan’s immense political risk. Bottom Line: The US election cycle is the chief source of policy risk and geopolitical risk in 2020, a stark contrast with the EU. European political risk will spike with a full-fledged recession, but for now it is contained. In fact the risks are largely to the upside in the short term as the countries turn slightly more fiscally accommodative. As long as global growth rebounds this year, European equities can outperform their richly valued American counterparts. Emerging Markets: Can They Outperform? With volatility likely in the near-term, Arthur Budaghyan of BCA Research’s Emerging Markets Strategy argues that the key test for emerging markets equities is whether they outperform their developed market counterparts. If they do not, then it suggests that investors still do not see endogenous growth, capital spending and profitability in emerging markets and therefore that they will lag their DM counterparts in the eventual equity upswing. Our long Korea / short Taiwan trade exploded out of the gate but has since fallen back in the face of the new headwind from the coronavirus. We have a high conviction in this trade because the difference in equity valuations faces a looming catalyst in the market’s mispricing of relative geopolitical risk: South Korea’s risk indicator is in a broad upswing while Taiwan’s has collapsed, despite the persistence of the diplomatic track with North Korea and Taiwan’s resounding reelection of both a pro-independence president and legislature (Chart 19). Mainland China will send both risk indicators upward in the near term, but South Korea’s economic problems are priced in and Trump’s diplomacy with North Korea is grounded in well-established constraints on Washington, Beijing, Pyongyang, and Seoul. By contrast the market is entirely dismissing Taiwan’s immense political risk, which does not depend on the outcome of the US election. In the coming 1-3 years, Beijing, Taipei, and Washington are all more likely to take self-interested actions that test the constraints in the Taiwan Strait, upsetting the market, before those constraints are reconfirmed (assuming they are). Beijing is likely to impose economic sanctions as Taipei’s demand for greater freedom and alliance with the US will agitate Chinese leaders who will seek to get the Kuomintang back into power. Brazilian political risk has failed to reach new highs, as anticipated, suggesting that President Jair Bolsonaro’s many problems are not driving investors to sell the real amid underlying indications of rebounding global growth and at least attempts at pro-market reform (Chart 20). Chart 19Markets Are Mispricing Geopolitical Risks In South Korea And Taiwan

Markets Are Mispricing Geopolitical Risks In South Korea And Taiwan

Markets Are Mispricing Geopolitical Risks In South Korea And Taiwan

Chart 20Political Risks Remain Contained In Brazil

Political Risks Remain Contained In Brazil

Political Risks Remain Contained In Brazil

Turkey’s military intervention into Libya’s civil war is another example of the foreign adventurism that we see as an outgrowth of populism and the need to distract the public’s attention from domestic mismanagement. We expect the risk indicator to rise or be flat and would remain short Turkish currency and risk assets. Bottom Line: Emerging markets face a new headwind from the coronavirus. Not only will China’s growth rebound sputter but Asian EMs will be exposed to the virus and may be less capable than China of dealing with it rapidly and effectively. With volatility looming, emerging market performance relative to developed markets will be a key test of whether endogenous growth trends are taking shape. Investment Conclusions Tactically we are closing our long GBP/JPY trade and UK curve steepener for negligible gains. We are also closing our long Egyptian sovereign bond trade for a gain of 5.59%. We remain long industrial commodities; long Korean equities versus Taiwanese; and long Malaysian equities relative to emerging markets. We expect these trades to perform well over a 12-month horizon. Strategically several of our recommendations will benefit from heightened volatility in the near term but face challenges later in the year as growth rebounds and risk sentiment revives. Nevertheless our time horizon is three-to-five years. In that span we remain long gold, long euro, long defense, short US tech, and short CNY-USD. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Appendix Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

Germany: GeoRisk Indicator

France: GeoRisk Indicator

France: GeoRisk Indicator

France: GeoRisk Indicator

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Italy: GeoRisk Indicator

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

Spain: GeoRisk Indicator

UK: GeoRisk Indicator

UK: GeoRisk Indicator

UK: GeoRisk Indicator

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

Canada: GeoRisk Indicator

China: GeoRisk Indicator

China: GeoRisk Indicator

China: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Taiwan: GeoRisk Indicator

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Korea: GeoRisk Indicator

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Russia: GeoRisk Indicator

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Brazil: GeoRisk Indicator

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Turkey: GeoRisk Indicator

Section III: Geopolitical Calendar

Highlights The intense focus on the weakening of global oil demand expected in the wake of another coronavirus outbreak in China – dubbed 2019-nCoV – obscures likely supply-side responses by OPEC 2.0. The producer coalition likely will rebalance markets by extending production cuts from end-March to at least the end of June when it meets in Vienna March 5-6. OPEC 2.0 producers will be exquisitely sensitive to Asian refiner demand. They will use it as a gauge for how severe 2019-nCoV’s impact will be on EM demand, and adjust production and exports accordingly. On the demand side, it is difficult to analogue the 2019-nCoV outbreak to the 2003 SARS outbreak, given all the conflicting fundamentals at play at that time. Forward curves for the principal benchmark crude oils – Brent and WTI – remain backwardated, in spite of the 2019-nCoV-related sell-off. Longer-dated WTI (out to December 2023) traded below $50/bbl earlier in the week, roughly in line with shale-breakeven costs reported by the Dallas Fed earlier this month. This likely will continue to pressure capex in the US shales, keeping future supply growth constrained. Feature Forward curves for the principal benchmark crude oils – Brent and WTI – remain backwardated, in spite of the 2019-nCoV-related sell-off. Chart of the WeekChina's Oil Demand Drives Global Growth

China's Oil Demand Drives Global Growth

China's Oil Demand Drives Global Growth

Oil markets are rightly focused on the demand implications of the 2019-nCoV outbreak in China.1 Since 2000, China has accounted for 42% of annual oil-demand growth worldwide (Chart of the Week). China is second only to the US in oil demand, accounting for 14% of total global demand of 100.7mm b/d at the end of 2019; its oil imports averaged more than 10mm b/d last year, and are expected to remain strong as it continues to build out its refining sector. Chart 2Asian Air Travel Hit Hard By SARS

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Historical analogues for 2019-nCoV are difficult. The immediate analogue is the SARS coronavirus outbreak identified in China in February 2003, which lasted six months and hit Asian air travel especially hard (Chart 2). During the height of the SARS outbreak in April 2003, air-travel passenger demand in Asia plunged 45%, according to the International Air Transport Association (IATA). This pushed jet fuel prices lower in Asia and in other key markets, along with distillate prices generally (Chart 3).2 Chart 3Fundamental Supply-Demand Balances Support Higher Crude Oil Prices

Fundamental Supply-Demand Balances Support Higher Crude Oil Prices

Fundamental Supply-Demand Balances Support Higher Crude Oil Prices

China now is an extremely large share of global jet fuel consumption. Chart 4BCA Models, Base Metals Prices Suggest SARS Effect Was Short-Lived

BCA Models, Base Metals Prices Suggest SARS Effect Was Short-Lived

BCA Models, Base Metals Prices Suggest SARS Effect Was Short-Lived

The industry now is more reliant on Chinese travelers. Since 2003, the number of annual air passengers has more than doubled, with China growing to become the world’s largest outbound travel market. In 2003, close to 7mm passengers from China traveled on international flights. By 2018, that number had grown close to 64mm people, according to China’s aviation authority. As Chart 2 demonstrates, China now is an extremely large share of global jet fuel consumption. Still, oil is a global market – the avoidance of China during the SARS outbreak in 2003 would have impacted global air travel, and, as a result, global jet-fuel prices. Our proprietary EM commodity-demand models and the behavior of base metals prices, which were and remain heavily influenced by China’s economy, suggest China’s GDP growth slowed in 2003 (mainly 1H03) because of the SARS outbreak (Chart 4). The LME’s base metals index fell 9% between February and July 2003, while copper prices fell 11%. By year-end, these markets had fully recovered. Oil-Supply Management Drives Price Evolution In the modern era of the oil market beginning roughly around 2000, there have been numerous demand shocks requiring a supply response from OPEC. During the SARS outbreak in 2003, oil-market fundamentals at the time were complicated by the sudden loss of Venezuelan output in December 2002 to a general strike, which lasted three months and removed more than 2mm b/d from the market, and the US invasion of Iraq on March 2003. Both of these supply-side shocks hit markets just as demand was being hit by SARS. This makes it difficult to extract a pure price response on the demand side to the SARS episode. In the modern era of the oil market beginning roughly around 2000, there have been numerous demand shocks requiring a supply response from OPEC. These including the 9/11 terror attacks in the US in 2001; the SARS outbreak in late 2002-03; the Global Financial Crisis in 2007-08; and the euro debt crisis in 2011-12 (Chart 5).3 Chart 5Demand Shocks Abound In 21st Century

Demand Shocks Abound In 21st Century

Demand Shocks Abound In 21st Century

Chart 6OPEC Lost Key Members' Output During SARS Outbreak

OPEC Lost Key Members' Output During SARS Outbreak

OPEC Lost Key Members' Output During SARS Outbreak

OPEC 2.0’s goal – similar to OPEC’s goal before it – is to avoid an unintended inventory accumulation. Importantly, these demand shocks were accompanied by supply shocks – Venezuela's general strike; the US invasion of Iraq continues to play havoc with global supply; the BP Macondo blowout in the Gulf of Mexico in 2010; the Arab Spring and the loss of Libyan output in 2011 – all of which complicated OPEC’s decision making (Chart 6). Much of OPEC’s adjustment then and now is made by the Kingdom of Saudi Arabia (KSA), which functions as the central bank of the global oil market increasing and decreasing production to balance markets (Chart 7). Chart 7KSA Primarily Balances Markets During Supply, Demand Shocks

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

OPEC 2.0’s goal – similar to OPEC’s goal before it – is to avoid an unintended inventory accumulation, which would push prices lower and severely alter the forward curves for the principal crude oil pricing benchmarks, WTI and Brent (Chart 8). Chart 8OPEC 2.0’s Goal: Avoid Unintended Inventory Accumulation

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Navigating The 2019-nCoV Outbreak Oil prices – like all commodity prices – are a function of supply and demand, which clear the market instantaneously (here and now), and across time as buyers and sellers contract for forward delivery. The relentless focus on the demand-side consequences of the 2019-nCoV outbreak is not helpful in determining how oil prices will trade going forward. Oil prices – like all commodity prices – are a function of supply and demand, which clear the market instantaneously (here and now), and across time as buyers and sellers contract for forward delivery. The discussion above is meant to highlight this, by recalling OPEC’s production management during various demand shocks, not just the SARS outbreak in 2003. OPEC then, and OPEC 2.0 now, is not forced to produce oil and export regardless of the physical realities it confronts. It can adjust production and exports in response to direct demand indications from its refinery buyers and traders lifting its crude oil. Demand slowdowns, all else equal, typically will show up in falling crack-spread differentials between refined products and crude oil prices (Chart 9).4 Chart 9Crack Spreads Inform Crude Oil Production Decisions

Crack Spreads Inform Crude Oil Production Decisions

Crack Spreads Inform Crude Oil Production Decisions

It still is too early to gauge the extent of the fall-off in demand arising from 2019-nCoV, but it will become apparent in cracks and in OPEC 2.0 producers’ responses to lower refiner demand. Falling crack spreads inform crude oil producers they need to throttle back on production – refiners are not able to profitably run all the crude being made available to them and crude and product are backing up in inventory. It still is too early to gauge the extent of the fall-off in demand arising from 2019-nCoV, but it will become apparent in cracks and in OPEC 2.0 producers’ responses to lower refiner demand, which will determine how much production they need to cut in order to balance the market. This will be done against a backdrop of supply concerns that are not too dissimilar to those prevailing during the 2003 SARS crisis – e.g., instability in Iraq and Iran that could threaten production, and the loss of Venezuelan exports. Bottom Line: Markets still are in the process of assessing how damaging 2019-nCoV will be for industrial commodity demand – oil, bulks and base metals, in particular. As has been the case in all such demand shocks, OPEC’s supply response (and now OPEC 2.0’s) will determine how deeply and for how long prices are impacted. Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Hugo Bélanger Senior Analyst Commodity & Energy Strategy HugoB@bcaresearch.com Commodities Round-Up Energy: Overweight Brent prices fell 8% since last Monday amid the coronavirus outbreak in China. The number of confirmed cases is rapidly expanding, reaching more than 6,000 as of Wednesday which surpasses the trajectory of SARS in the first month of the outbreak in 2003. Nonetheless, the fatality rate remains below that of SARS, estimated at less than 3% vs. ~ 10% for SARS. Separately, the WCS discount to WTI averaged -$23/bbl this month. This is in line with our view that the discount would drop below -$20/bbl in 1Q20. This level is appropriate to incentivize additional rail transportation to the US. We expect the discount will remain close to current levels and for crude-by-rail volumes to pick up this year (Chart 10). Base Metals: Neutral Base metals have been severely impacted this week by the coronavirus outbreak – copper, aluminum, zinc, and lead are down 9%, 4%, 9%, and 5%. A prolonged slowdown in China’s economic activity – the driver of the global industrial activity recovery we expect – would plunge metals’ prices. China’s base metal consumption more than doubled since 2003. Thus, the potential impact of 2019-nCoV is much larger compared to SARS and market participants are pricing in the probability of damaging scenarios to global growth. This explains the pronounced decline in metals’ prices this year vs. 2003. Precious Metals: Neutral Gold was one of the few commodities in the green since last week. The yellow metal rose 1% since last Monday, supported by renewed safe-haven demand flows. Gold and the USD have been rising simultaneously amid the virus outbreak, which is typical of uncertain periods. The spectrum of possible outcomes is wide and negatively skewed. This warrants protection through safe-haven assets. We remain strategically long gold as a portfolio hedge. Our recommendation is up 28% since inception. Ags/Softs: Underweight Corn markets focused on USDA reports of rising exports, highlighted by the sale of 124,355 MT to Mexico. CBOT March corn futures were up 6% Tuesday, reversing earlier losses Monday. Beans remain under pressure, as traders await tangible evidence that China will go ahead with purchases announced in the so-called phase-one deal negotiated between the US and China (Chart 11). Chart 10WCS Discount Under Pressure

WCS Discount Under Pressure

WCS Discount Under Pressure

Chart 11Markets Waiting For China Demand

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Footnotes 1 The US Centers for Disease Control and Prevention’s 2019-nCoV website highlights the marked differences between China’s response to the current coronavirus outbreak vs the 2003 SARS outbreak. One notable response by the Chinese government this time around – besides the rapid lockdown on travel – has been the alacrity with which officials posted the genome for the virus to a global research database, which allowed US researchers to quickly compare it to the strain they isolated. Separately, Reuters reported Australian researchers were able to grow the virus in a lab, which could accelerate development of a vaccine. 2 Distillates comprise the so-called middle of the refined barrel, and include jet fuel, diesel fuel and heating oil (also known as gasoil). These are primarily associated with industrial markets – mining and transportation, e.g. – and are key barometers of economic activity generally. 3 The "modern" era for oil began roughly in 2000, when oil prices became a random walk. WTI prices were mean-reverting from 1986 to roughly 2000, then became a random walk. Please see Helyette Geman, (2007), "Mean Reversion versus Random Walk in Oil and Natural Gas Prices," in Advances in Mathematical Finance, Birkhäuser, Boston; and Haidar, I. and C.R. Wolff, "Forecasting crude oil price (revisited)," The proceeding of the 30th USAEE Conference, Washington , D.C. USA. 9-12 October, 2011. 4 The “crack spread” is the USD/bbl difference between refined-product prices and crude-oil prices. It represents the gross margin of refiners. Investment Views and Themes Recommendations Strategic Recommendations Tactical Trades TRADE RECOMMENDATION PERFORMANCE IN 2019 Q4

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Commodity Prices and Plays Reference Table Trades Closed in 2019 Summary of Closed Trades

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

Expect OPEC 2.0 To Cut Supply In Response to Demand Shock

An analysis on Hong Kong is available below. Highlights The correction in EM risk assets and currencies will be larger than during the SARS outbreak. A number of market indicators that are pertinent for EM assets are sending a disconcerting message. The trouble is that they have relapsed from already low levels. We are closing our long position in EM stocks to manage risk and continue recommending underweighting EM equities and credit versus their DM counterparts. Stay short EM currencies versus the US dollar. A new trade: Go short Hong Kong banks / long Taiwanese banks. Feature Chart I-1Global Equity Correction: SARS- And Coronavirus-Episodes

Global Equity Correction: SARS- And Coronavirus-Episodes

Global Equity Correction: SARS- And Coronavirus-Episodes

It is tempting to compare the potential impact of the current coronavirus outbreak on the global economy and financial markets with that of SARS in the spring of 2003. The correction in global equities due to the SARS outbreak lasted only a couple of days during April 2003, and global share prices sold off by only 2.5% (Chart I-1). During that period, the EM equity index dropped by 4% and emerging Asian bourses by 8% in US dollar terms (Chart I-2). Presently, the drawdowns in global stocks and EM share prices have been 2.5% and 4%, respectively. Thus, the magnitude of the current correction is on a par with what occurred during the 2003 SARS outbreak (Charts I-1 and I-2). Further, in 2003, share prices bottomed when the number of registered new SARS infections – on a rolling fortnight basis – declined (Chart I-3). This was true both worldwide and in the case of Hong Kong. Chart I-2EM And Asian Stock Corrections: SARS- And Coronavirus-Episodes

EM And Asian Stock Corrections: SARS- And Coronavirus-Episodes

EM And Asian Stock Corrections: SARS- And Coronavirus-Episodes

Chart I-3Number Of New Cases And Share Prices: Global And Hong Kong

Number Of New Cases And Share Prices: Global And Hong Kong

Number Of New Cases And Share Prices: Global And Hong Kong

However, such simplistic comparisons between SARS in 2003 and the current coronavirus outbreak are uninformative. There are striking economic differences between these two episodes. The impact on both the Chinese and global economies will be larger today compared with the effects of SARS. This is true even if the spread of the coronavirus is contained soon and the number of infections and deaths peaks earlier and at much lower levels compared to the SARS outbreak. The rationale behind the meaningful impact on Chinese and global growth is two-fold: The safety measures undertaken by the Chinese authorities, including the extension of the Lunar New Year holiday period and imposition of limits on travel – are much greater than their response in 2003. These efforts might contain the spread of the virus and save human lives, but they will likely dampen economic activity in the near term. The importance of the Chinese economy in the world and hence its impact have grown immensely since early 2003. Overall, the current correction in EM risk assets and currencies will be larger than the one during the SARS outbreak. China’s Share Of The Global Economy: Today Versus 2003 Table I-1China’s Importance Now And In 2003

Coronavirus Versus SARS: Mind The Economic Differences

Coronavirus Versus SARS: Mind The Economic Differences

China’s economy is much more important to global aggregate demand and growth today than it was in 2003 (Table I-1). Specifically: China’s GDP at purchasing power parity accounts for 19.3% of world GDP compared to 8.3% in 2002 before the SARS outbreak occurred. In nominal US dollar terms, the mainland currently accounts for 17% of global GDP versus 4.3% in 2002. We use 2002 because the SARS outbreak occurred in early 2003, so China’s share of world GDP in 2002 is the more accurate measure of the country’s importance in early 2003. Chinese imports of goods and services make up 13.5% of global trade at present, significantly greater than their 4.5% share in 2002. The mainland’s share of consumption of various industrial metals has surged, from between 10-20% in 2002 to 50-60% presently (Table I-1). For copper, it has soared from 18% in 2002 to its current share of 53%. China’s iron ore imports have risen from 21% of the global total in 2002 to 64% presently. The nation’s oil consumption presently accounts for 13.5% compared with 6.6% in 2002. Total semiconductor sales in China currently constitute 34.6% of global semiconductor sales versus 5% in 2002. Personal computer sales in China make up 20% of worldwide sales compared with 2.4% in 2002. Mobile phones sales in China constituted 11% of worldwide sales in 2002. Today, smartphone sales account for 29% of global sales. Finally, in the past 12 months, passenger car sales in China were 21.5 million units, or 34.5% of the global total. In 2002, China’s share in global passenger auto demand was only 7.3%. Other relevant differences between China’s economy then and now include: Chart I-4China's Leverage In 2003 And Now

China's Leverage In 2003 And Now

China's Leverage In 2003 And Now

First, leverage among companies and households was low in 2002 compared with the current debt bubble. Aggregate local currency indebtedness of companies, households and the various levels of government stood at 120% of GDP in 2002, compared with 260% currently (Chart I-4). Even a temporary reduction in cash flows of enterprises due to shutdowns and a plunge in demand will weigh on their ability to service debt. This could in turn temporarily curtail their appetite for new investments and hiring. Second, by 2003 China had just completed a major overhaul of its state-owned enterprises (SOEs) and banks. As a result, the nation was in the early stages of a structural economic boom driven by higher productivity growth. Presently, neither SOE reforms nor deleveraging are meaningfully advanced (Chart I-4, bottom panel). Consequently, China is still in a structural decline in terms of productivity growth. Third, China entered the World Trade Organization in late 2001, and by early 2003 it was enjoying an FDI inflow boom and was on the verge of rapidly increasing its market share in global trade (Chart I-5). Presently, both multinational and Chinese producers are moving their production and supply chains out of China in response to US trade protectionism. Chart I-5China's Global Export Market Share In 2003 And Now

China's Global Export Market Share In 2003 And Now

China's Global Export Market Share In 2003 And Now

Finally, enterprises and organizations were not forced to shut down because of the SARS virus in the spring of 2003. Consequently, the hit to economic activity in the spring of 2003 was mild, as shown in Chart I-6A and I-6B. In contrast, the government today has extended the Chinese New Year holidays by a few days, and some companies will be operating on a part-time basis for a couple of weeks. It is impossible to forecast the evolution of the outbreak, but the odds are that a hit to economic activity in China due to the coronavirus outbreak is likely to be worse than during the SARS episode. Chart I-6AChina: Cyclical Variables During SARS Outbreak

China: Cyclical Variables During SARS Outbreak

China: Cyclical Variables During SARS Outbreak

Chart I-6BChina: Cyclical Variables During SARS Outbreak