Domestic Politics

The new national unity government in South Africa creates a geopolitical opportunity that investors should not bet against in the short term. A broad-based rally is likely to unfold relative to other emerging markets. However, structural problems and distrust within the new coalition hold out significant risks over the long run.

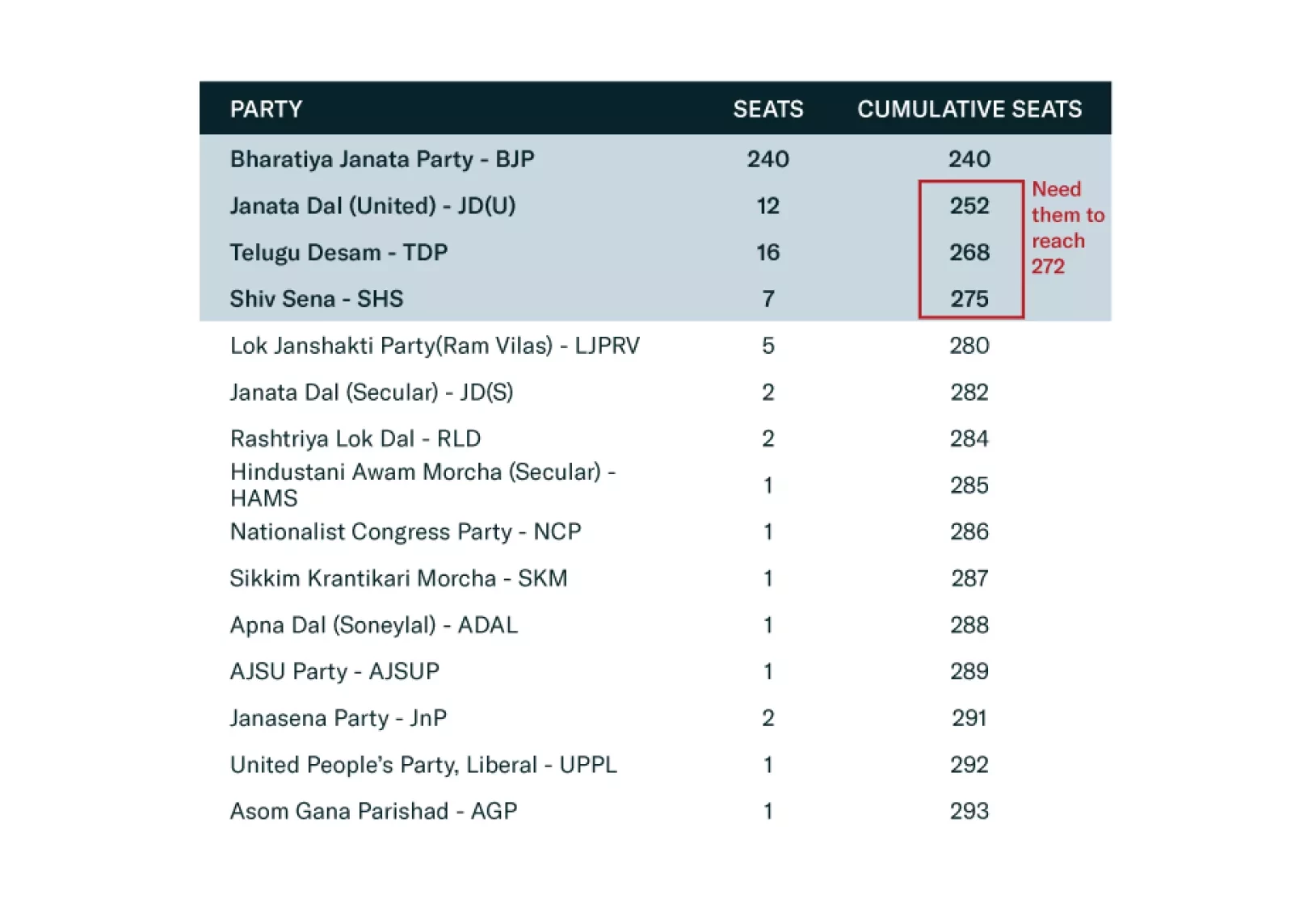

Prime Minister Narendra Modi won a third term and will become the third longest-serving prime minister of India. While investors responded negatively to the BJP’s loss of an outright majority, Modi and the NDA will continue to perpetuate the reforms they have already put into motion. The result also affirms that Indian democracy continues to thrive, contrary to the narrative that Modi had formed an authoritarian grip on the country, a view we always rejected.

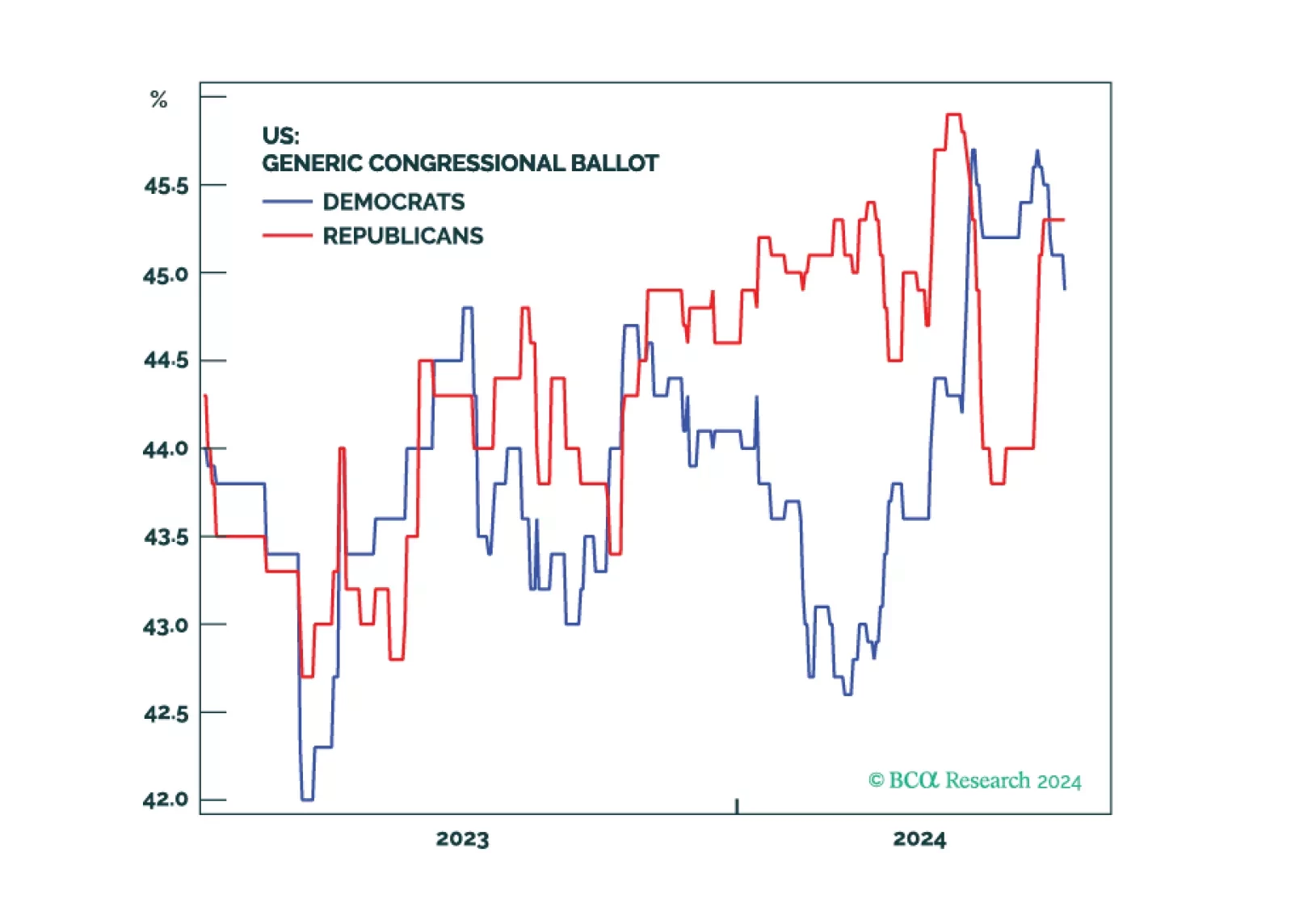

Republicans are favored in the House and Senate even if they do not win the White House. A Democratic sweep is a 20% risk. The policy implication would be inflationary, but not so much as under a Republican sweep. Election uncertainty should increasingly weigh on cyclical and high-beta assets in the second half of 2024.

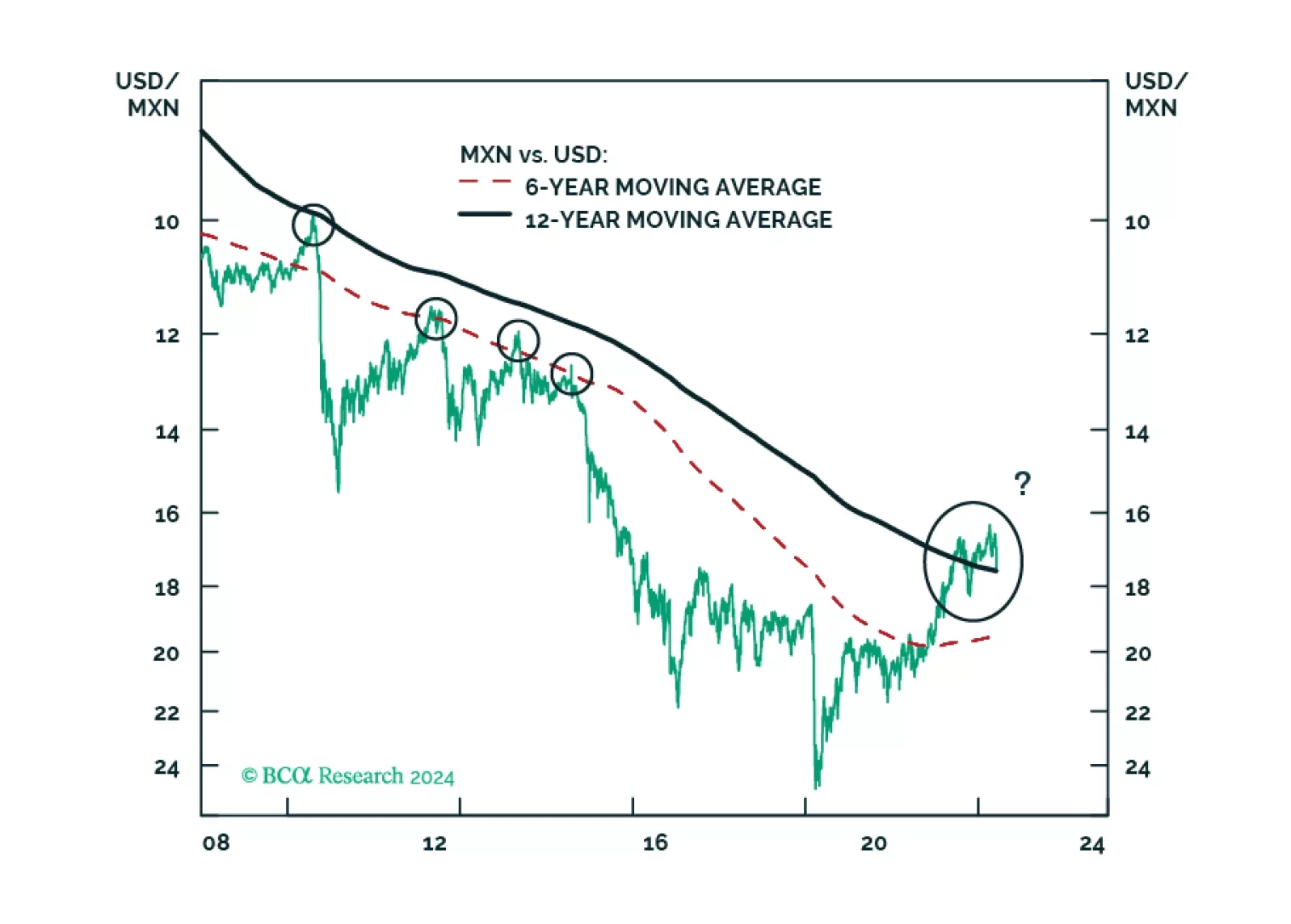

MORENA has once again swept the Mexican election: Claudia Sheinbaum will be president, with little to no constraint in Congress. All in all, Mexican politics will remain stable and overall supportive of markets. In the medium term, fiscal spending will return to conservatism and the constitutional reforms will lead to mixed fiscal and economic repercussions. In the long term, however, fiscal and institutional risks will rise. We advise investors to remain overweight Mexican risk assets relative to EM in cyclical and structural time horizons, but prepare for Mexican markets to sell off in absolute and relative terms in the next couple of months.

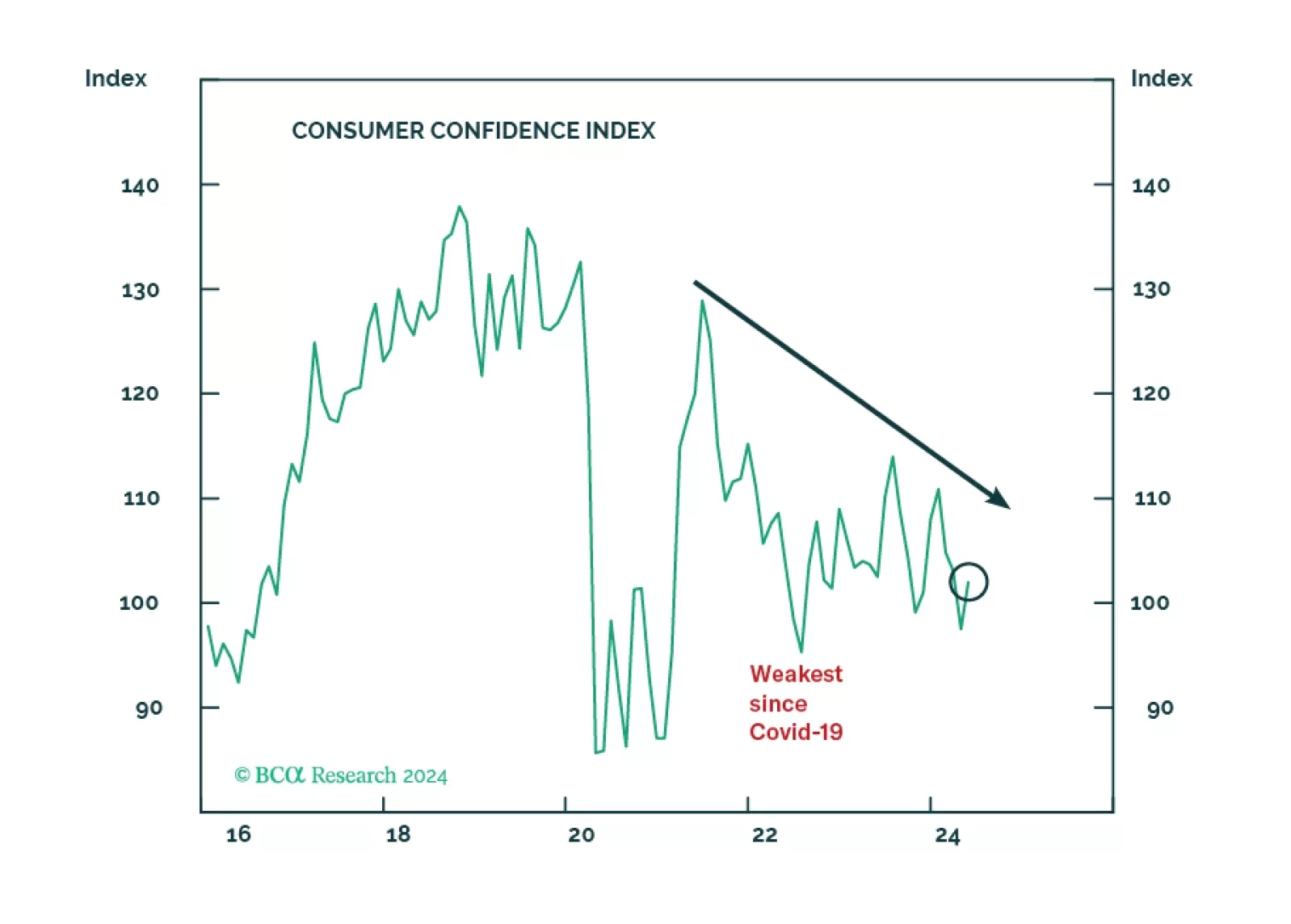

Democrats remain slightly favored for the White House because they are the four-year incumbent presidential party and the economy is not in recession. But if the unemployment rate rises in the lead up to November, then Biden and Democrats will become disfavored regardless of Trump’s convictions.

Favor defensive sectors, low-beta assets, and long-duration bonds until the election uncertainty is lifted one way or another over the next five months.

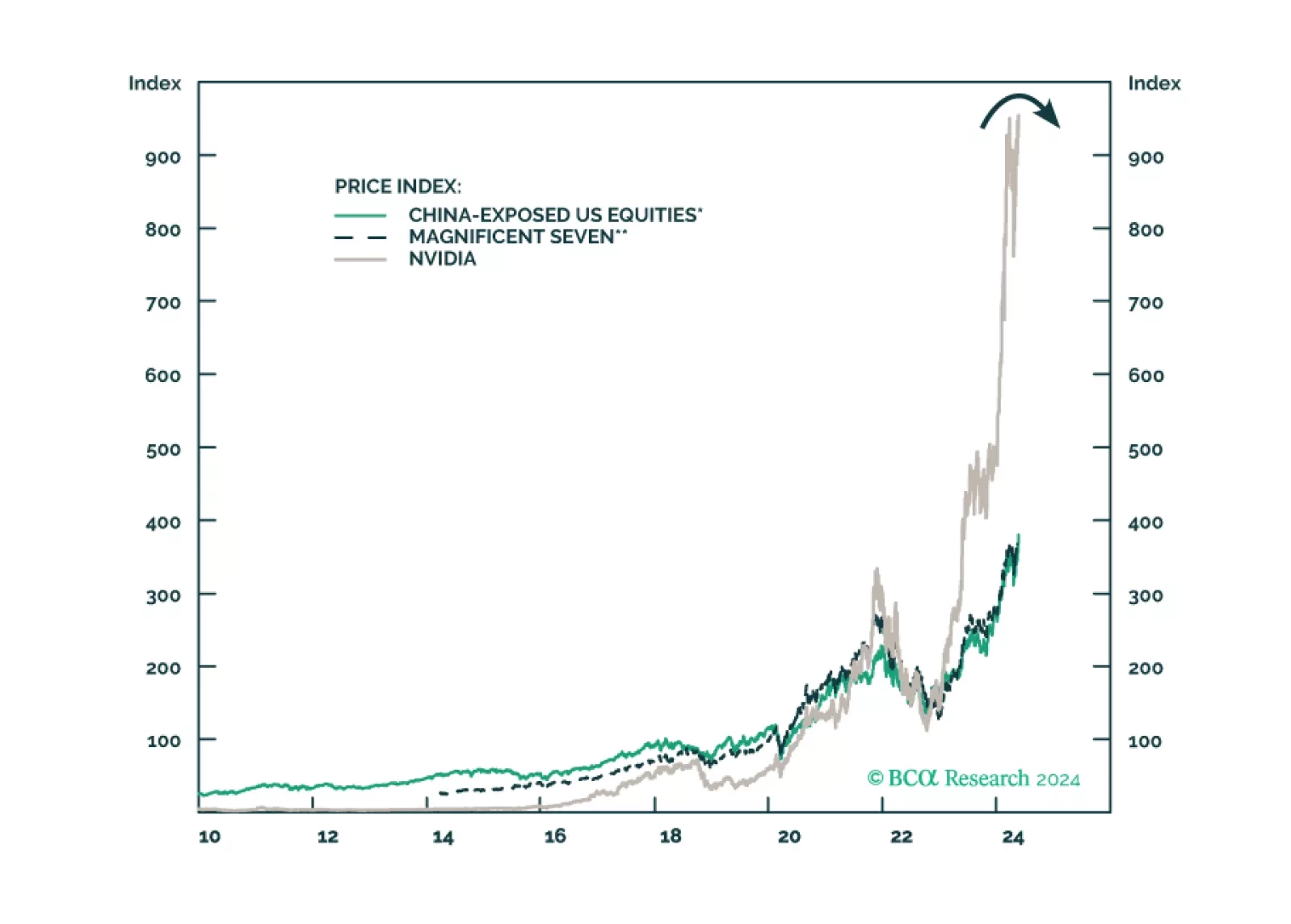

China is trying to export its way out of its economic slowdown while the US has already formed a hawkish consensus on foreign policy and trade. Investors should take cover as global financial markets are underrating the new phase of the trade war, which will escalate from here.