Domestic Politics

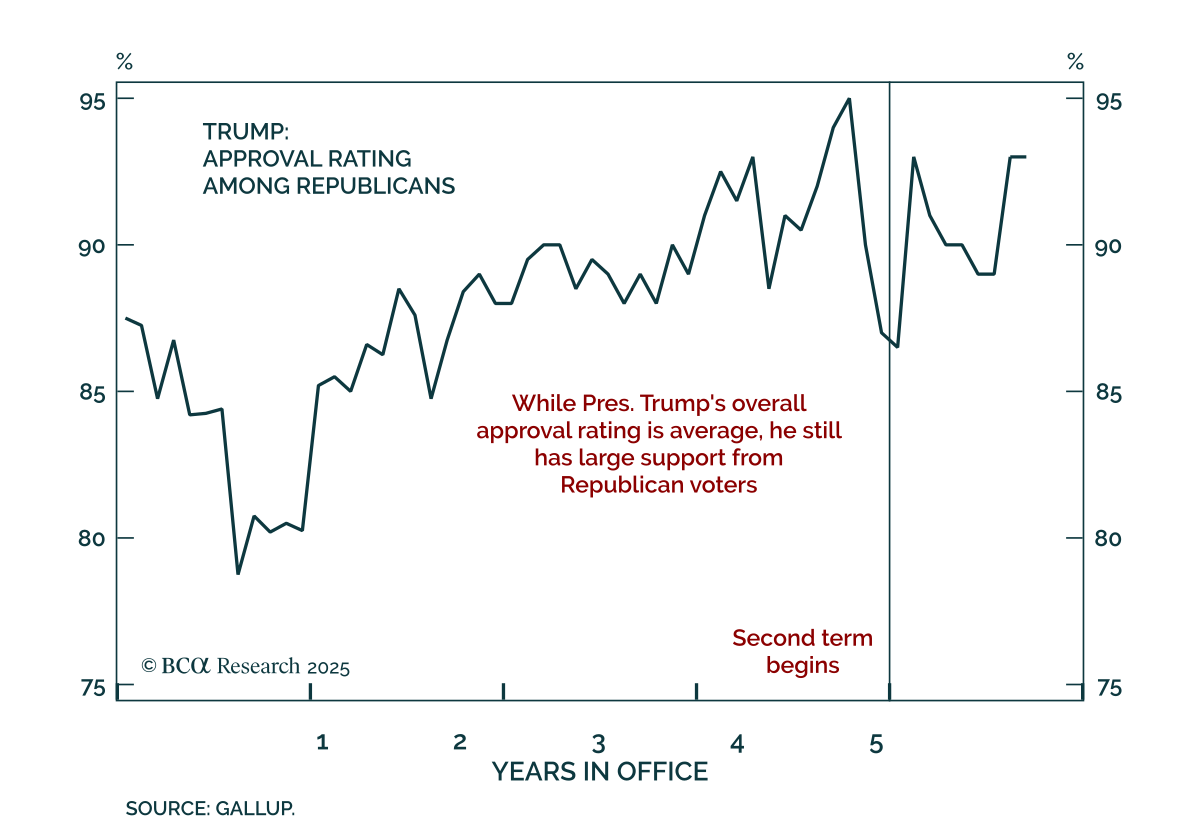

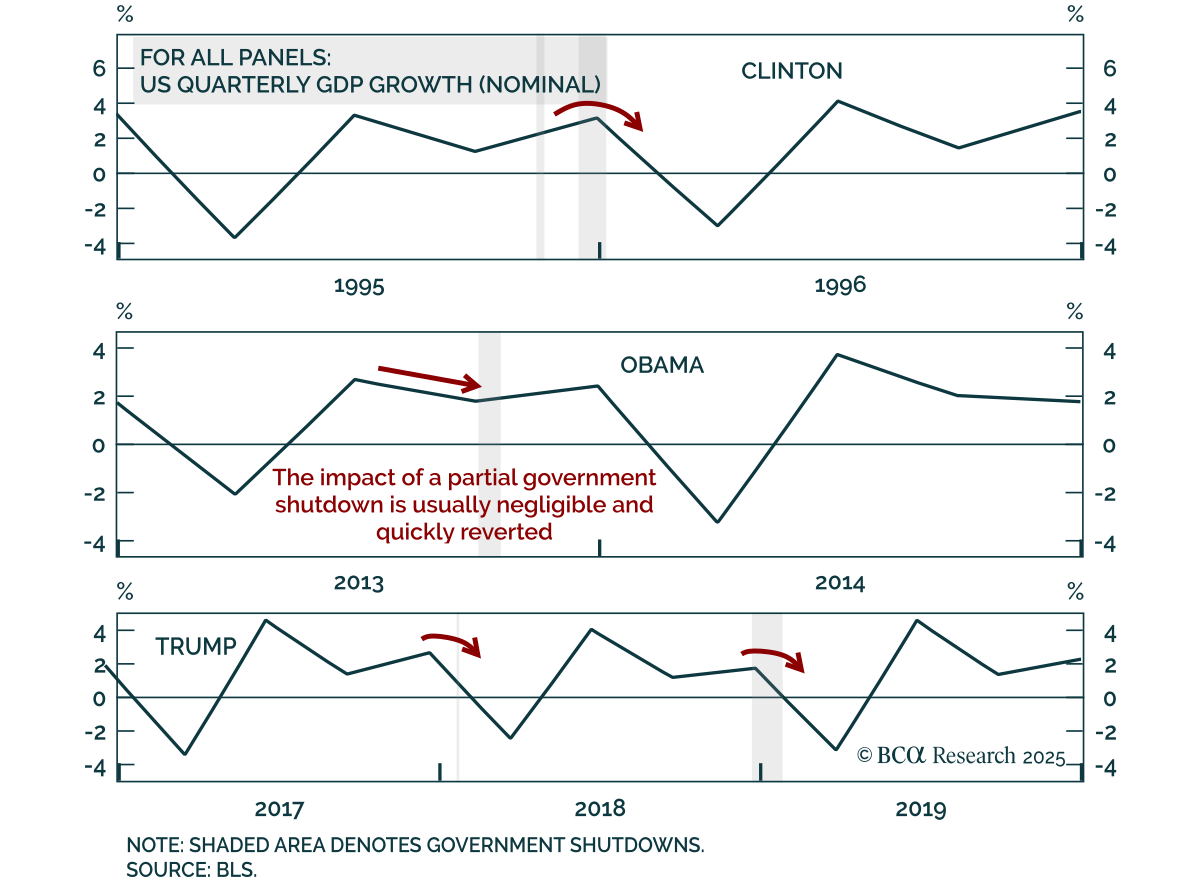

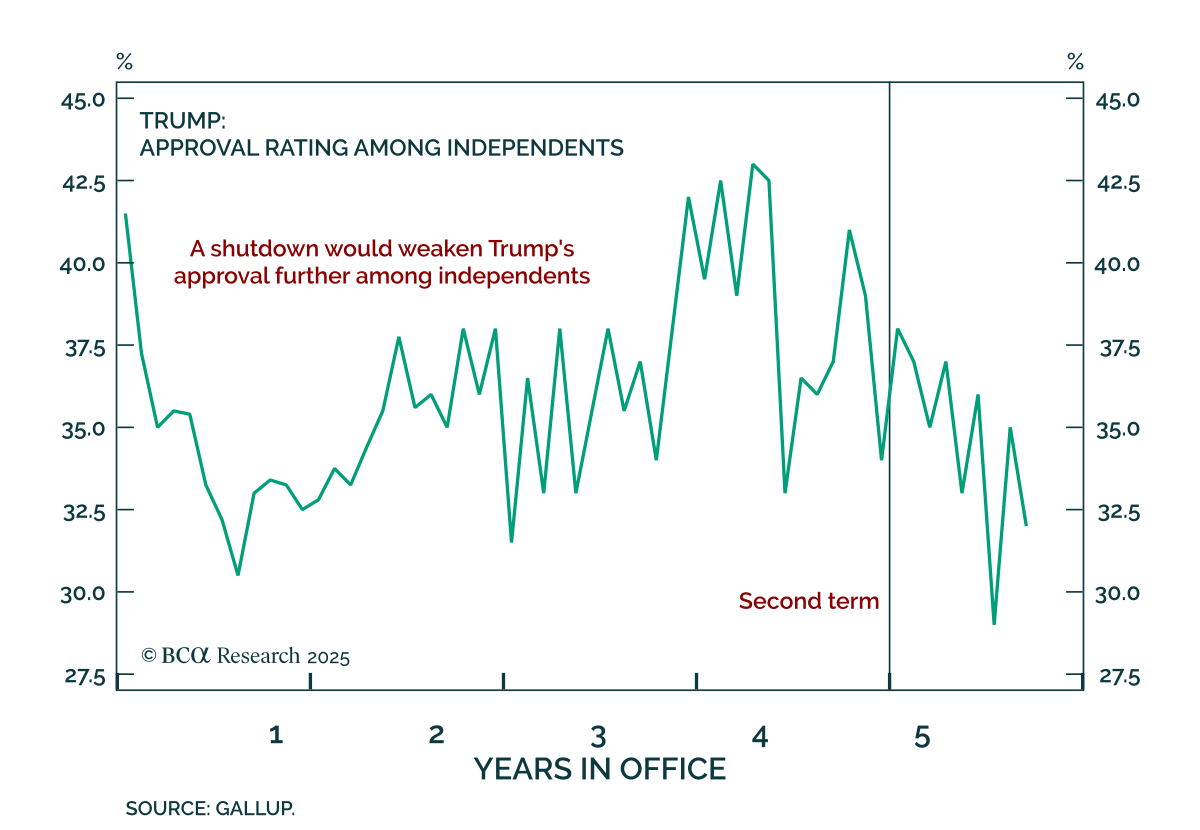

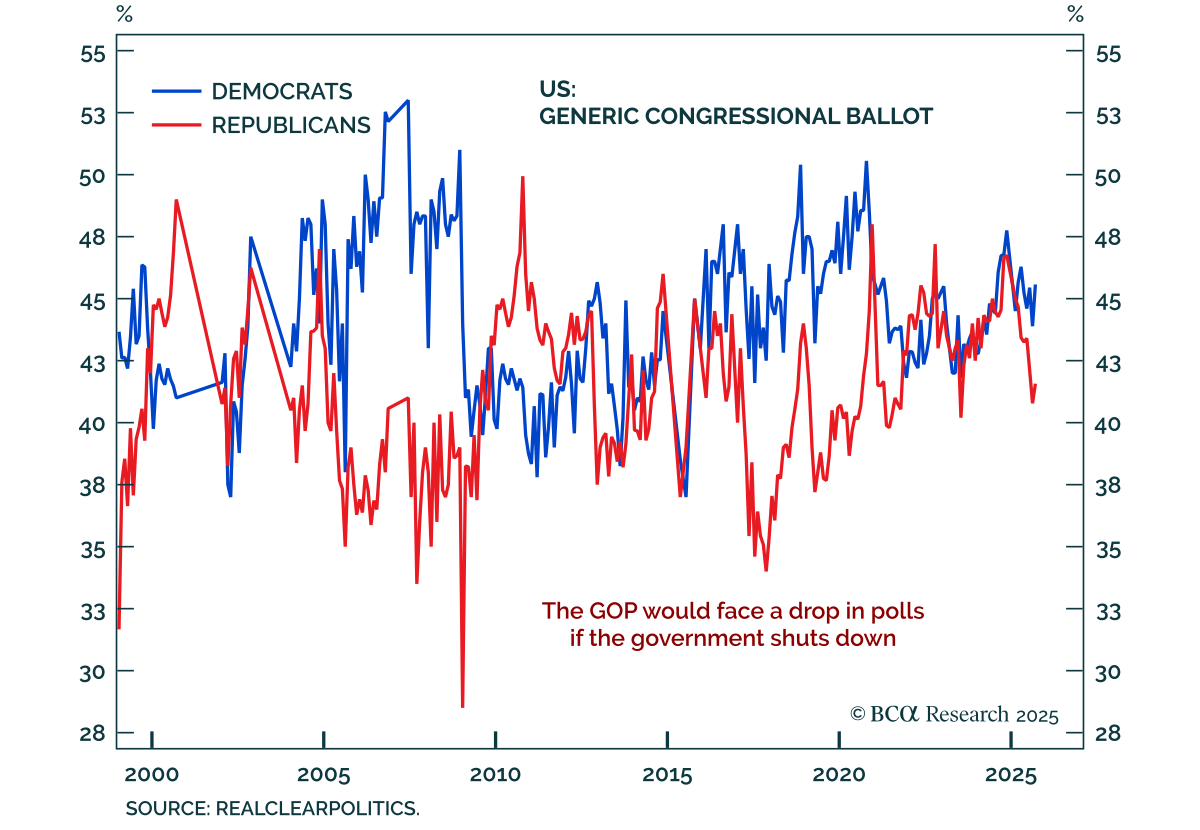

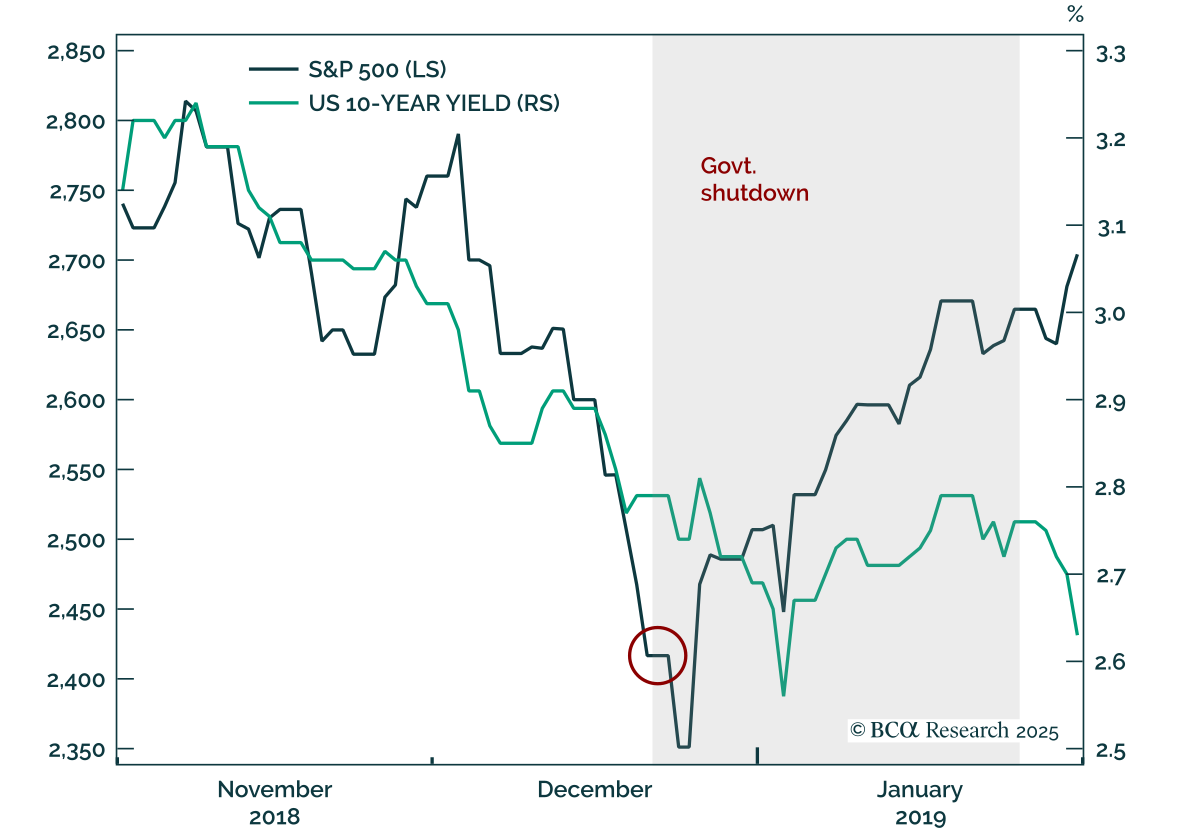

We give a one-third probability of a federal government shutdown. It probably will not happen before November. At worst, government shutdowns only cause temporary market volatility.

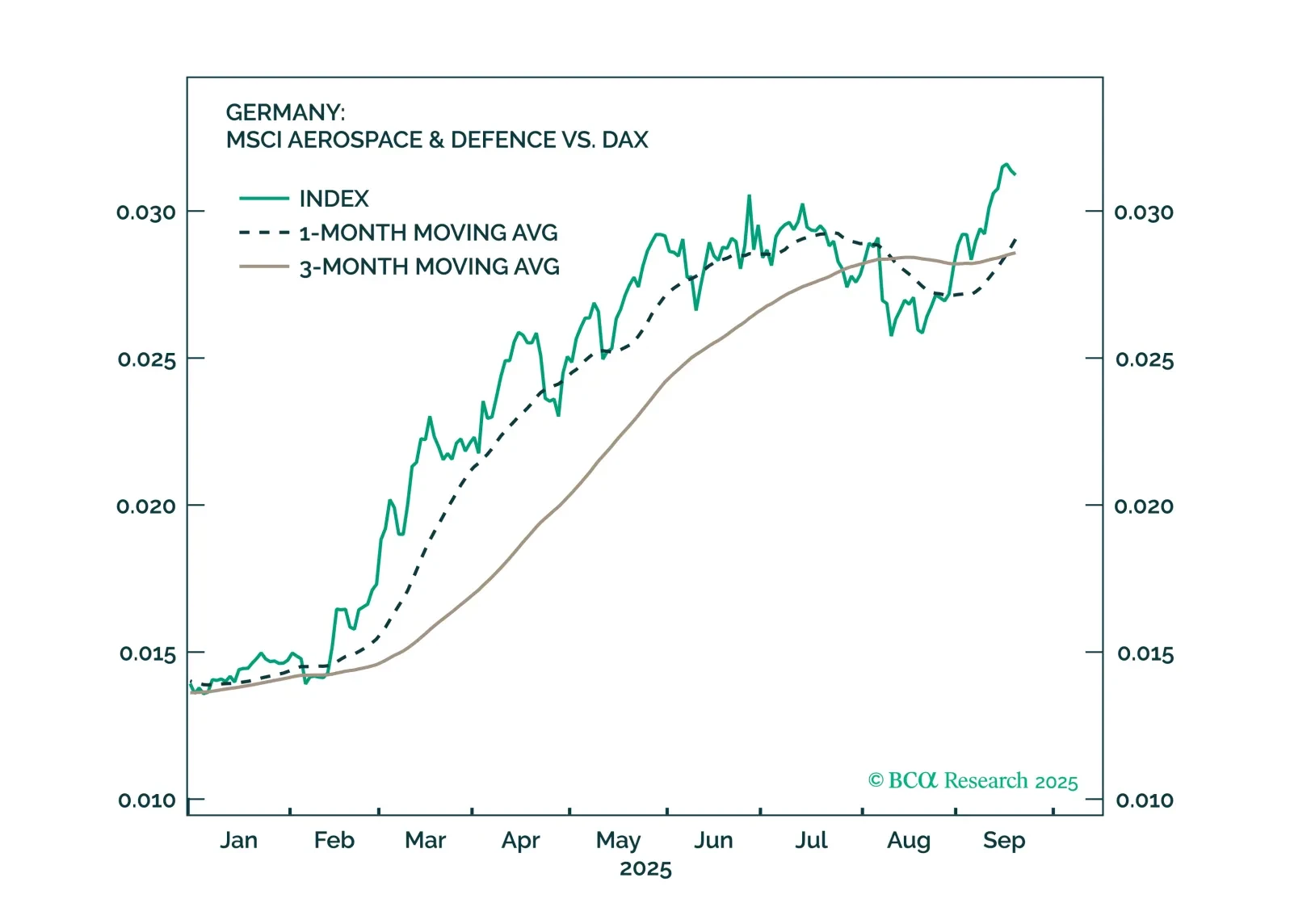

Germany is moving forward with implementing the large fiscal and defence spending announced earlier this year. Fiscal reforms are also positive, though they will fall short of expectations.

Political instability will persist in France as PM François Bayrou loses the confidence vote. The nomination of a new PM will not end the country’s political paralysis and will further fuel fiscal fears. Investors should remain underweight French OAT. French equities, especially French banks, should be bought on dips.

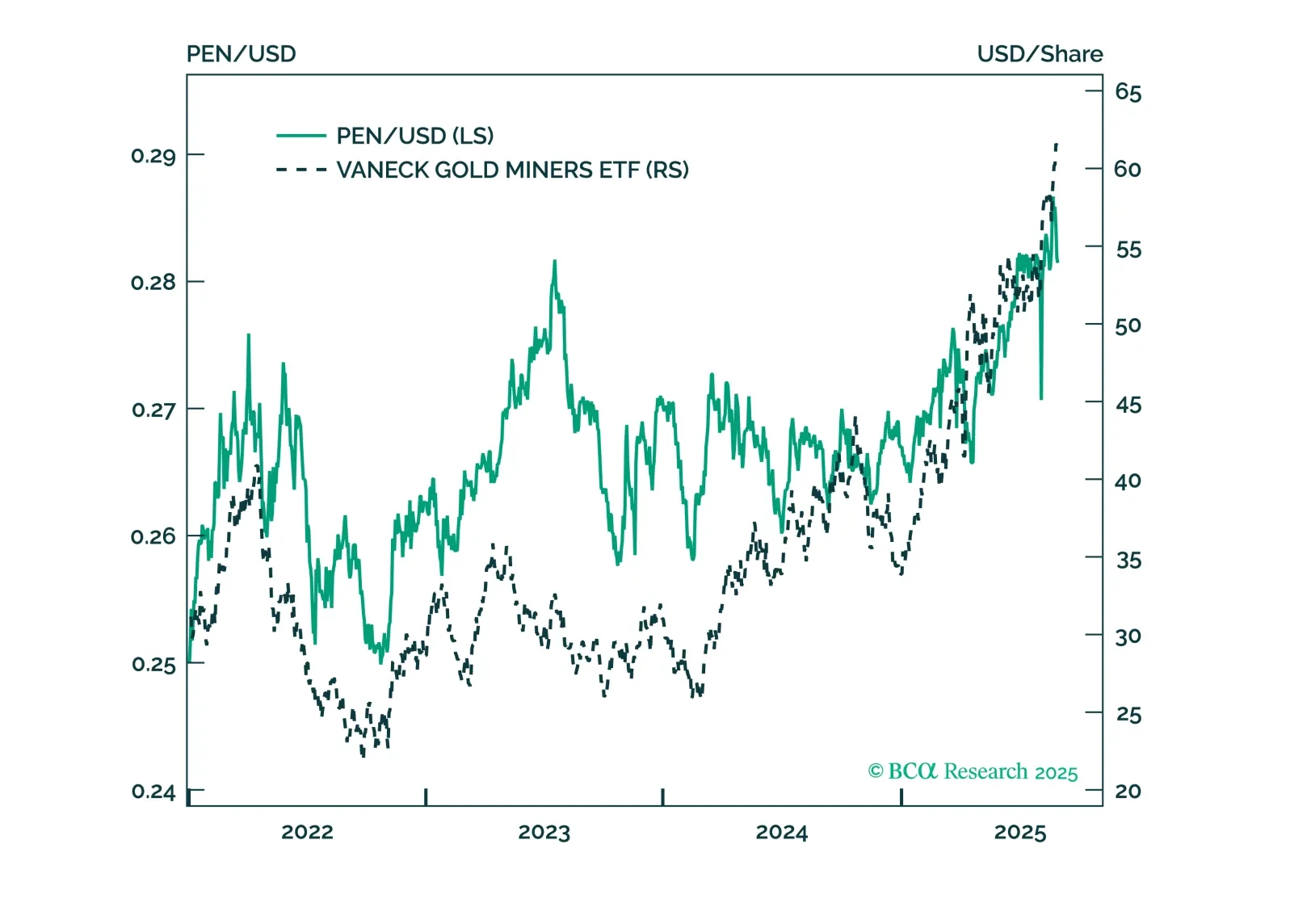

Peru’s April 2026 election will inject political volatility, but fundamentals are strong and we are constructive. Buy gold mining equities and gold on dips to capture the supportive global cycle and wait for a more attractive entry point for Peruvian assets.