Domestic Politics

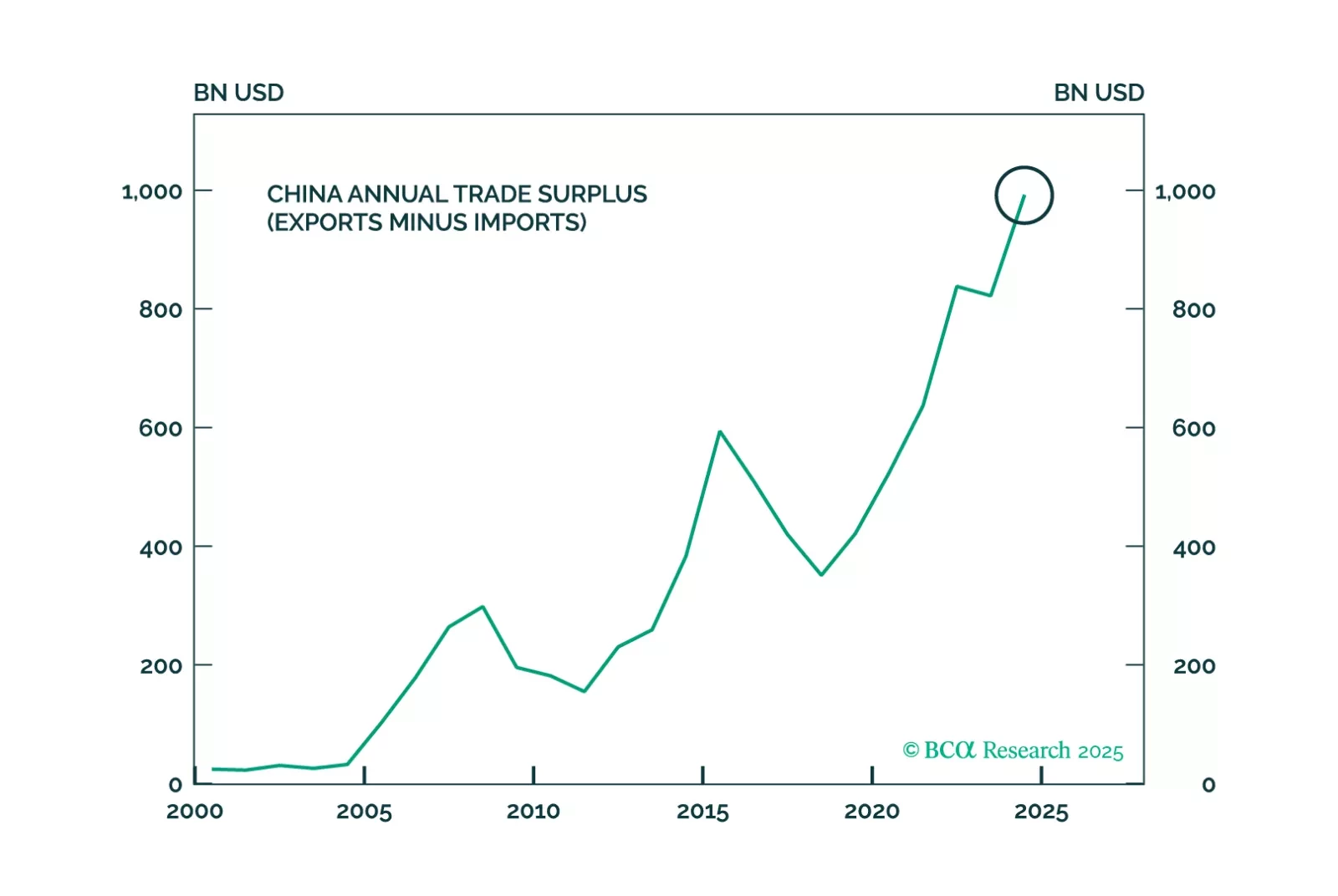

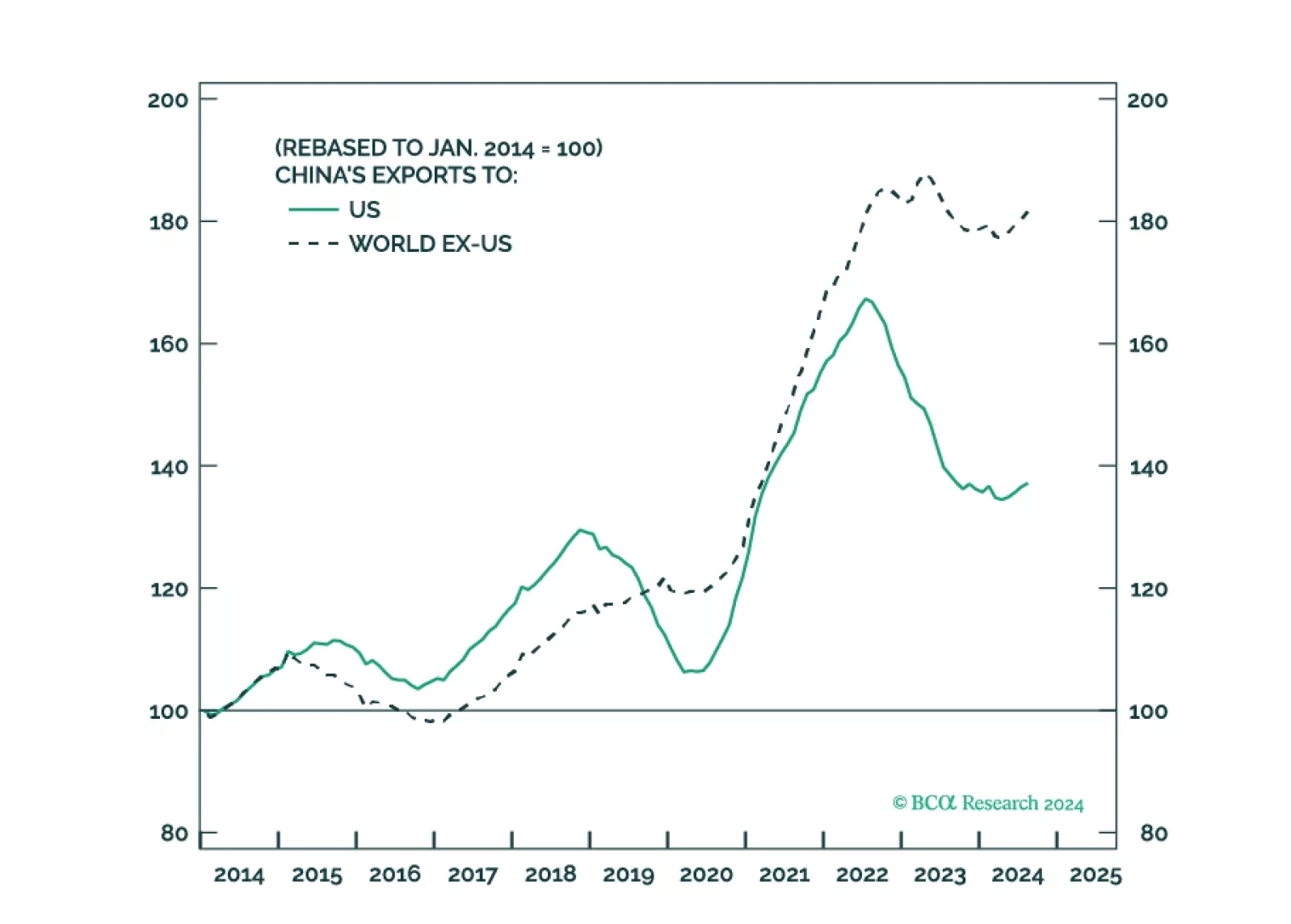

China barely hit its growth target in 2024 by shifting back to its old model of exports, racking up a record trade surplus with the world – right as Donald Trump walks back into the White House. Tariffs will elicit larger fiscal stimulus even as China rolls out innovations such as DeepSeek to meet its 2025 industrial goals, creating a volatile mix this year.

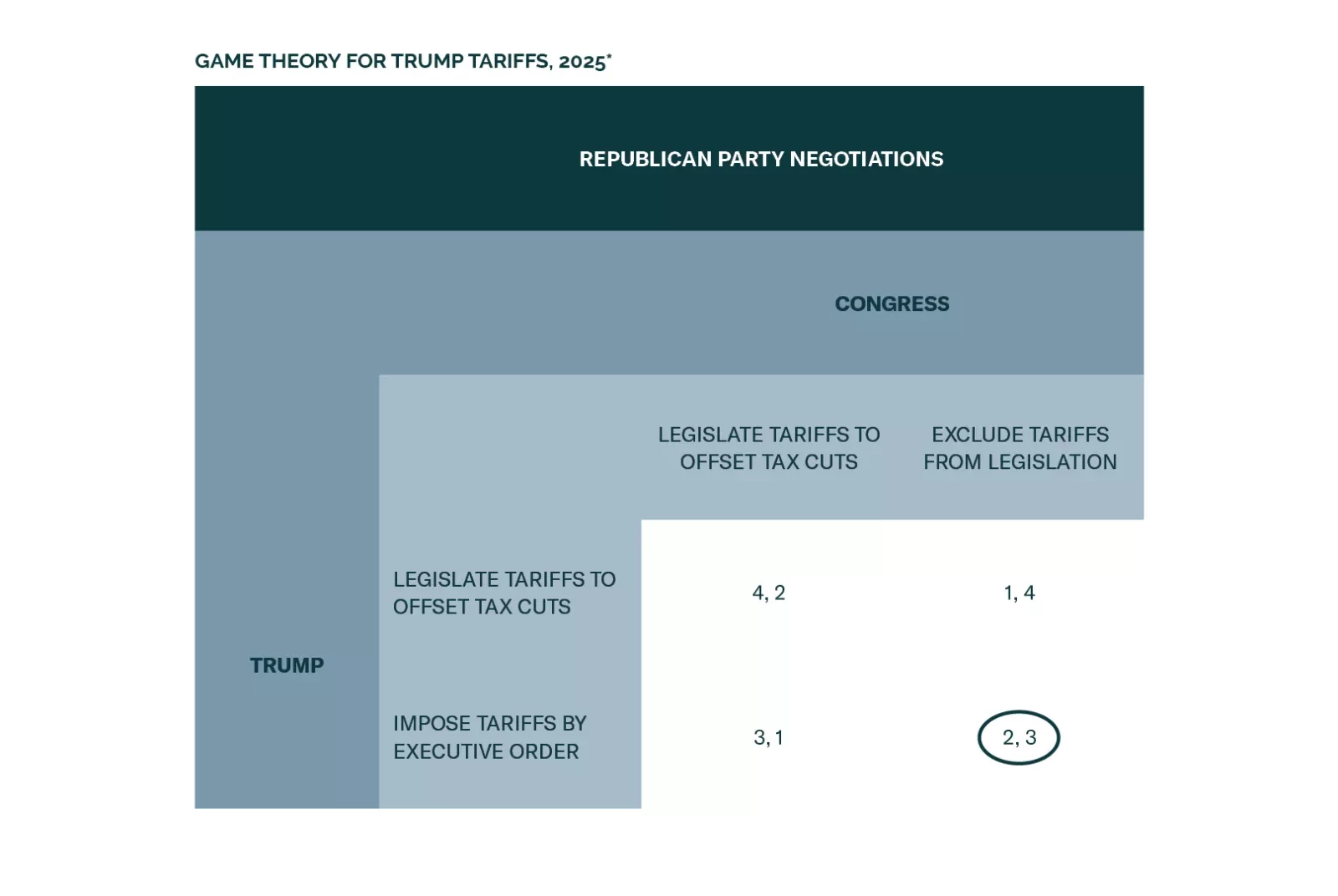

Simple games allow us to model several of the Trump administration’s most disruptive policies in 2025. We find that markets face an increase in volatility as Congress expands the budget, Trump implements tariffs on the world, China retaliates, and Taiwan tensions persist. A ceasefire in Ukraine is a marginally positive outcome for Europe, although it is not a long-term peace treaty.

- Congress will pass tax cuts by end of 2025 producing a fiscal thrust of about 0.9% of GDP in 2026.

- Trump will count on that stimulus as a basis for slapping tariffs on leading trade partners.

- China will retaliate against Trump and stimulate its domestic economy, while pursuing stronger trade ties with other countries. Europe will also retaliate.

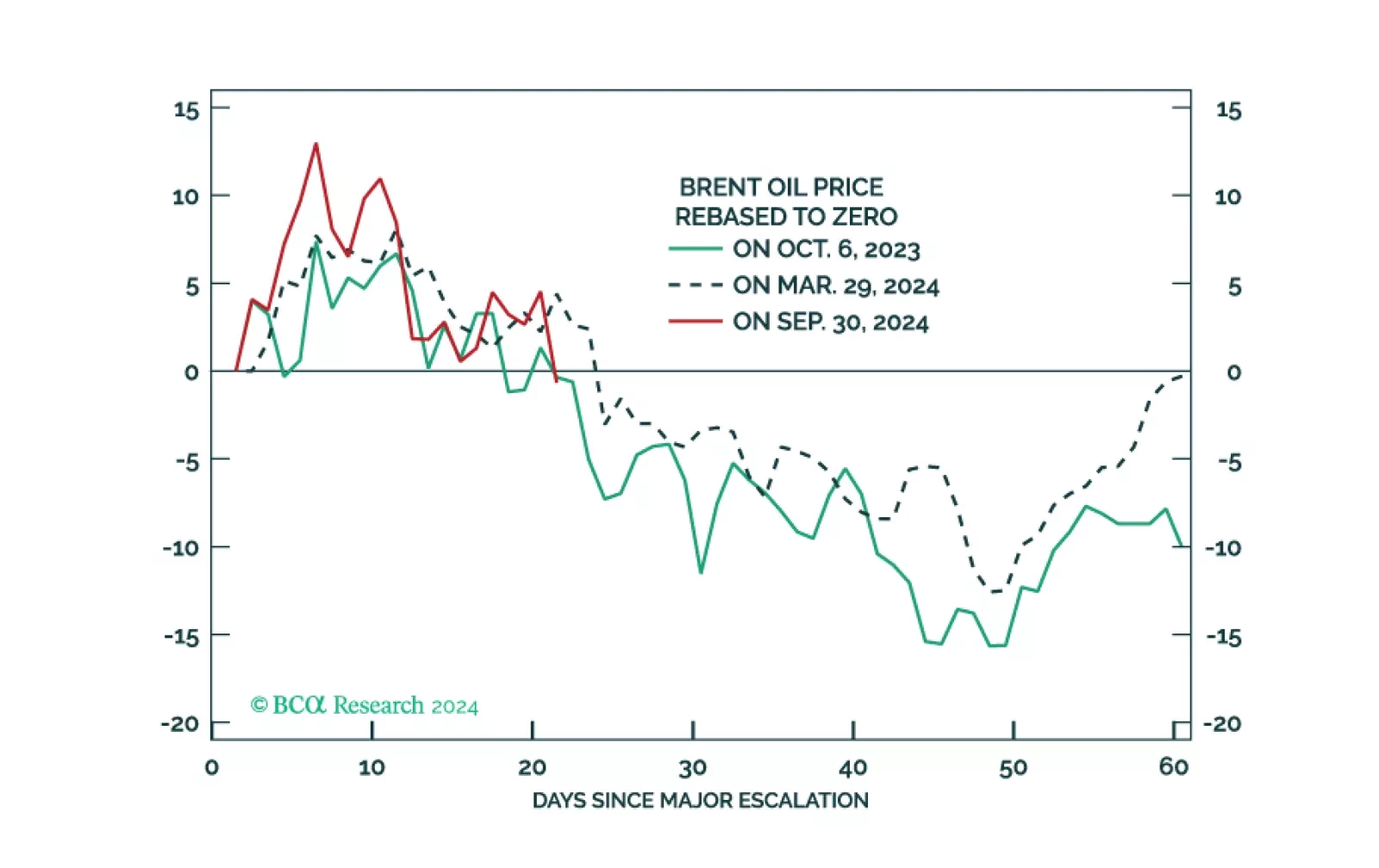

- Geopolitical risk will shift from Ukraine-Russia to Israel-Iran, where the conflict will continue to escalate until a crisis point is reached within 2025.

Investors are overstating the positive fiscal impact of the Trump presidency. The bond market will have something to say about the scope for further deficit expansion via tax cuts. As such, the trade after the trade of the Trump 2.0 administration may involve less growth out of the US, not more. In the interim, however, investors should continue to expect higher yields and increased equity volatility. There are plenty of risks ahead, including geopolitics, trade, and uncertainty surrounding fiscal policy.

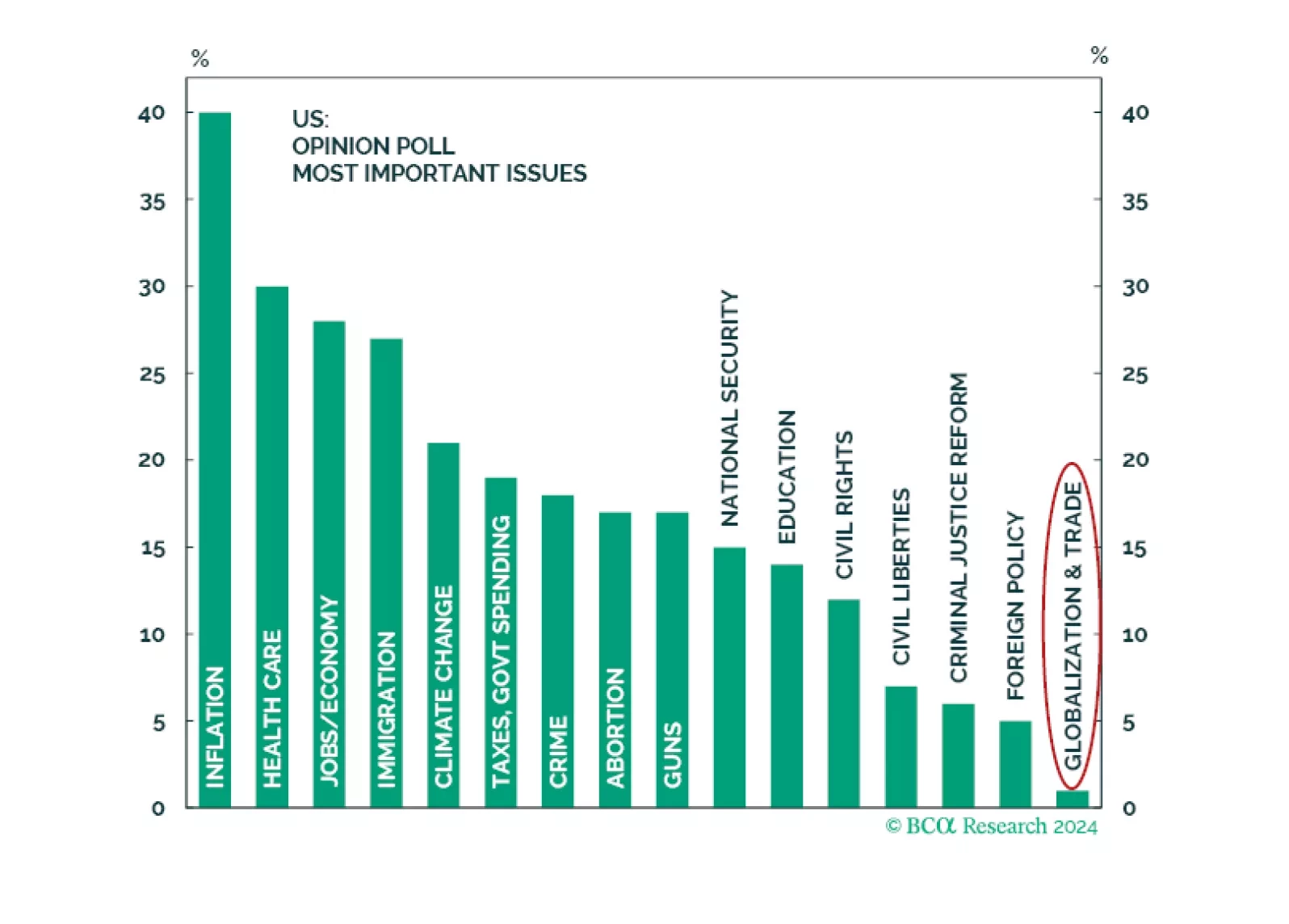

Ultimately, 2024 is not 2016 — a seemingly obvious point, but one with market relevance. In 2016, voters gave Trump a strong mandate for nominal GDP growth. It is not clear if this is the case today. Inflation is the most important issue, least relevant is trade and globalization. As such, Trump’s renewed mandate is for supply side reforms, not more populism and protectionism.

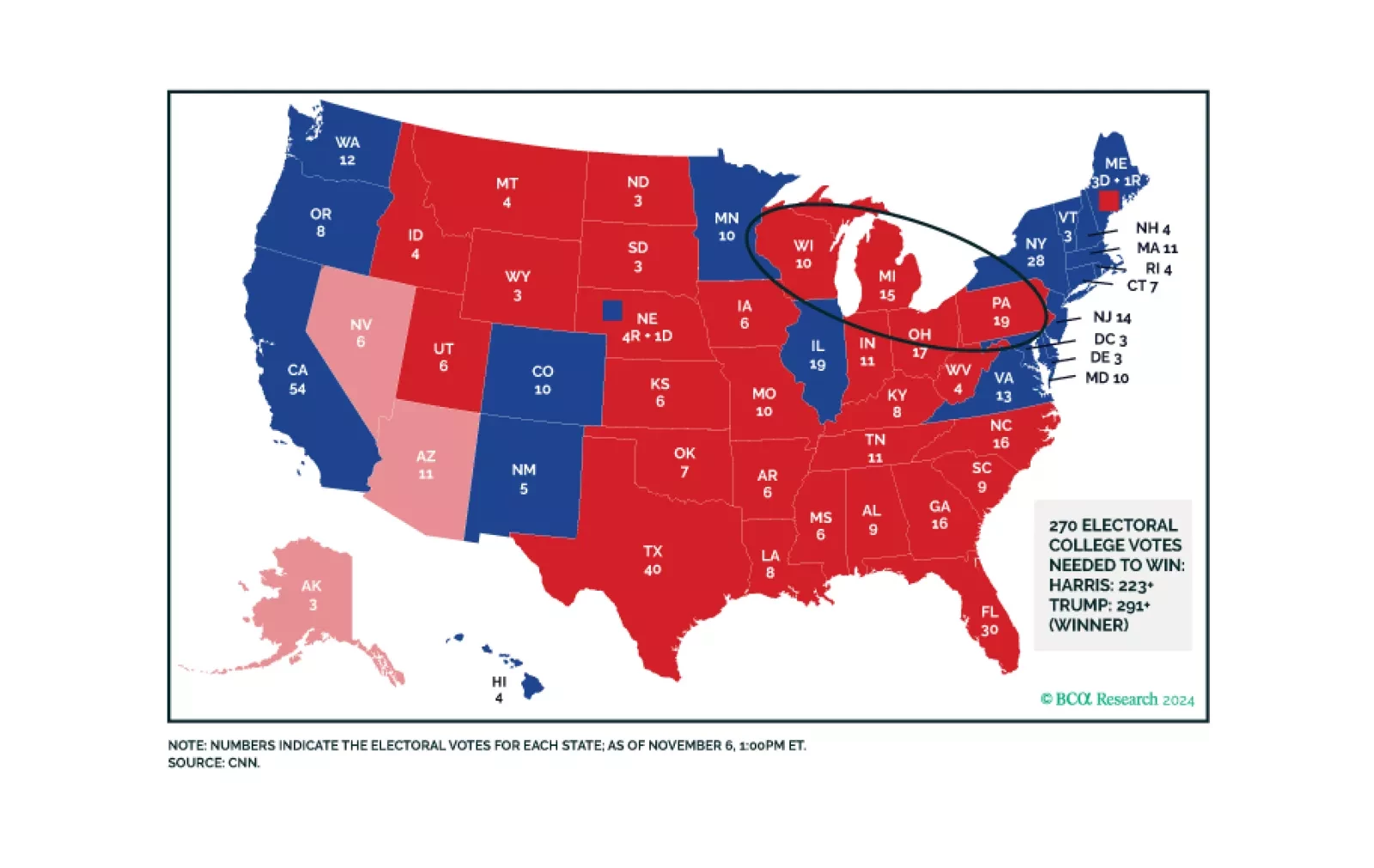

Trump’s resounding victory brings a popular mandate that ensures deregulation and higher trade tariffs. Higher budget deficit and immigration reform are also in the cards as the Republicans look like they may squeak a thin margin in the House of Representatives. Foreign policy will become more unilateral, with US assets outperforming initially.

Over the next few months, Japan’s new government will ease fiscal policy, which will improve domestic demand on the margin. Monetary policy may tighten further in the short run but not too much over the long run. The geopolitical setting drives Japan into accommodative economic policy.

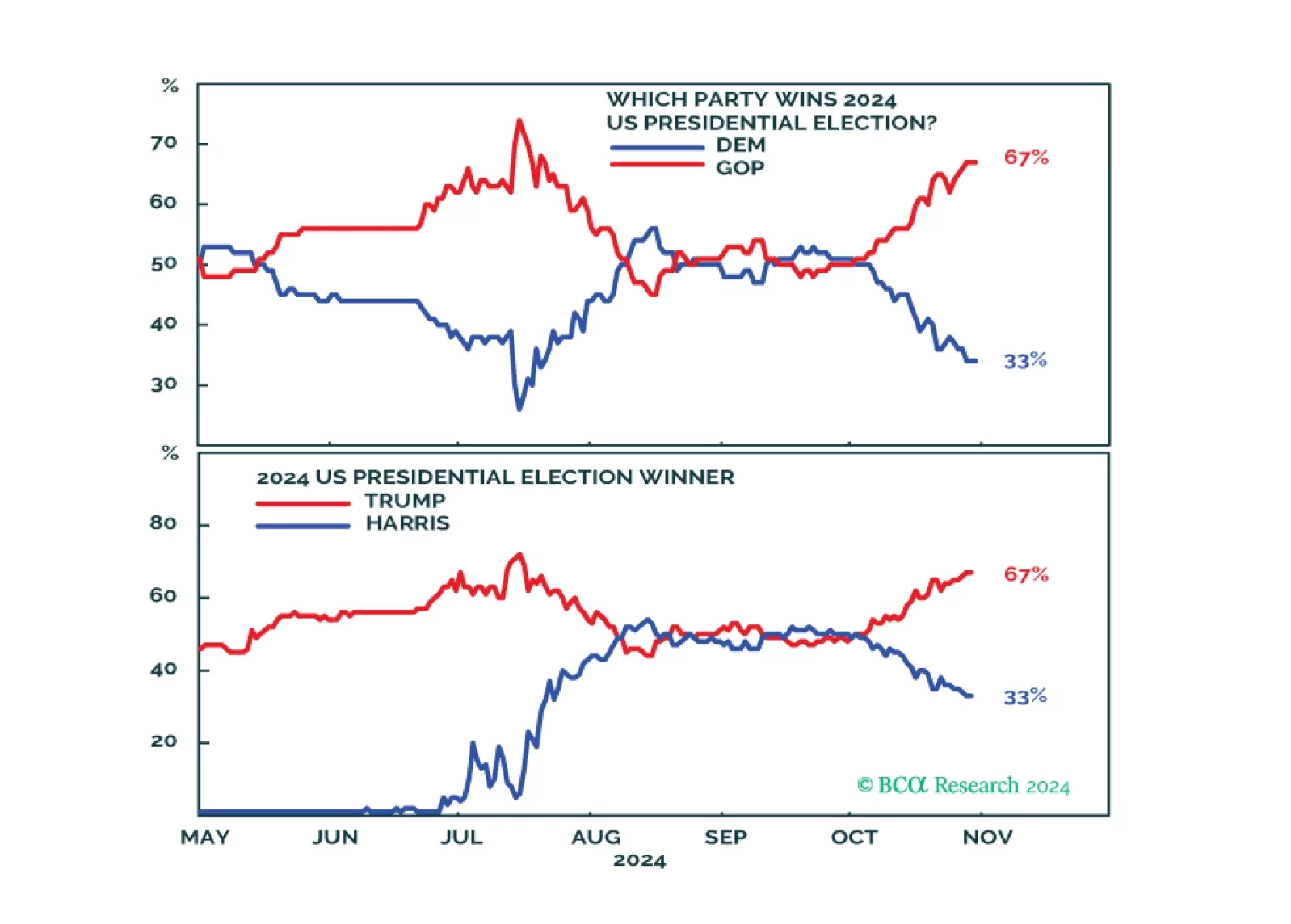

Trump may be favored, but Harris is now underrated. The Senate is highly likely to go Republican – Harris would be gridlocked if she pulled off a victory. If Trump wins it will be a full sweep. Expect volatility in the short term.

The global political system is destabilizing and the US will turn more hawkish in foreign policy, trade policy, or both, regardless of the election outcome. Tactically go long the dollar.