Earnings

Against the earnings-versus-everything-else market backdrop, stellar earnings are easily outweighing elevated oil prices, rising yields and the increased probability that the Fed may hike rates before the year is out. US allocators should remain invested in equities.

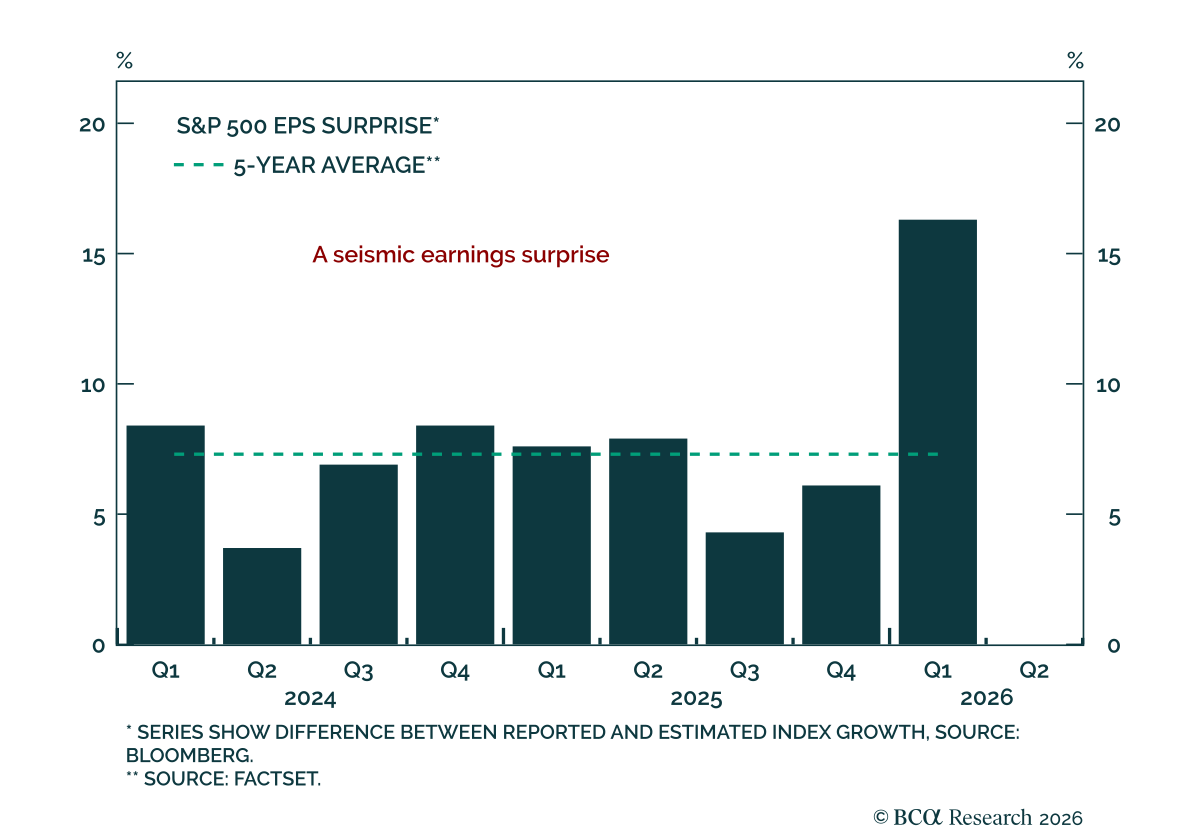

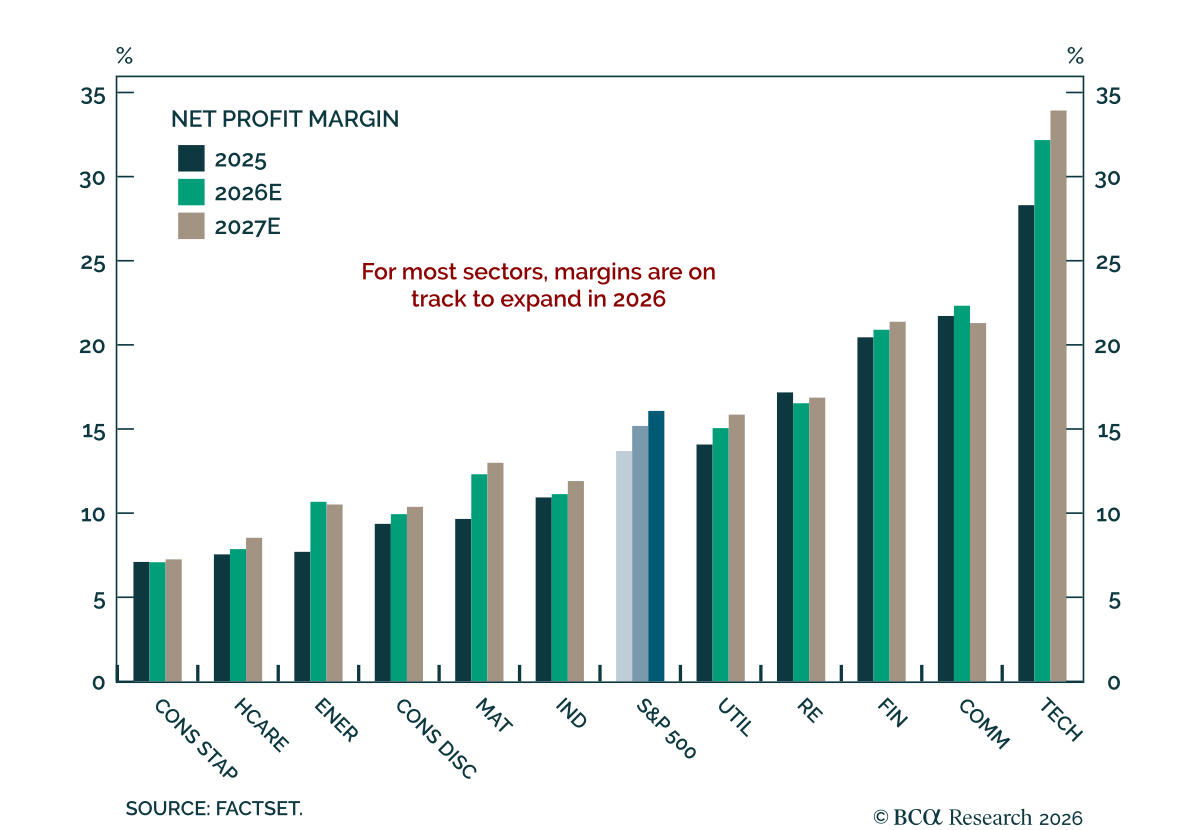

The investment cycle remains firmly intact, driving equity prices and fundamentals, as confirmed by both Q1 data and corporate commentary. Upside surprises, expanding margins, and rising capex expectations point to resilient demand. Companies confirm that AI-related demand is broad and visible, while geopolitical and credit risks remain contained and not yet systemic.

The S&P 500 finished last week at an all-time high as optimism over earnings has pushed the Iran conflict out of the spotlight. Despite uncertainty in the Strait of Hormuz, we do not think investors have enough evidence to justify underweighting equities and other risk assets.

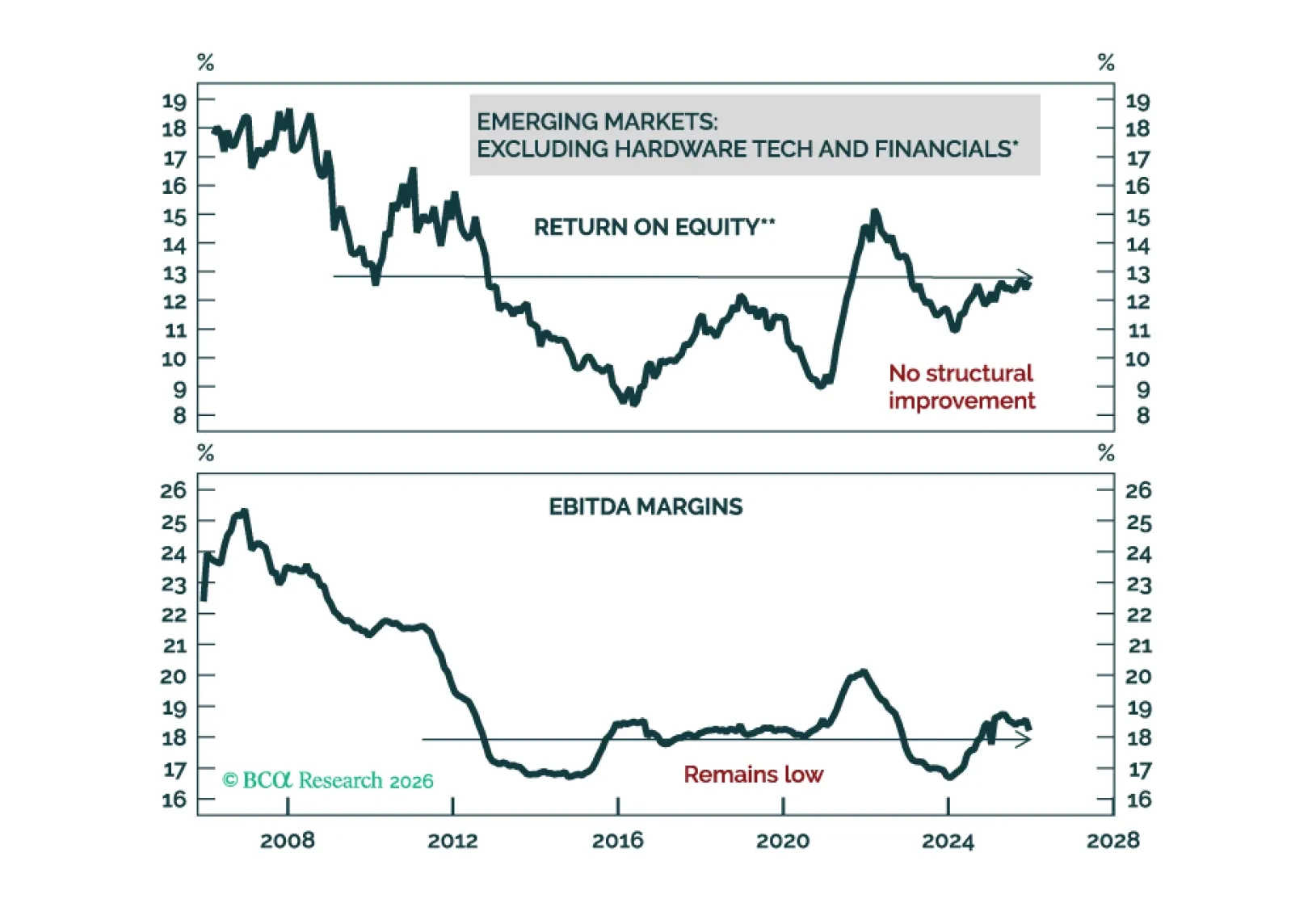

Outside Asian semiconductor producers, EM corporate earnings and profitability have seen little improvement. Despite the ceasefire in the Middle East, the medium-term outlook for EM stocks is still unattractive.

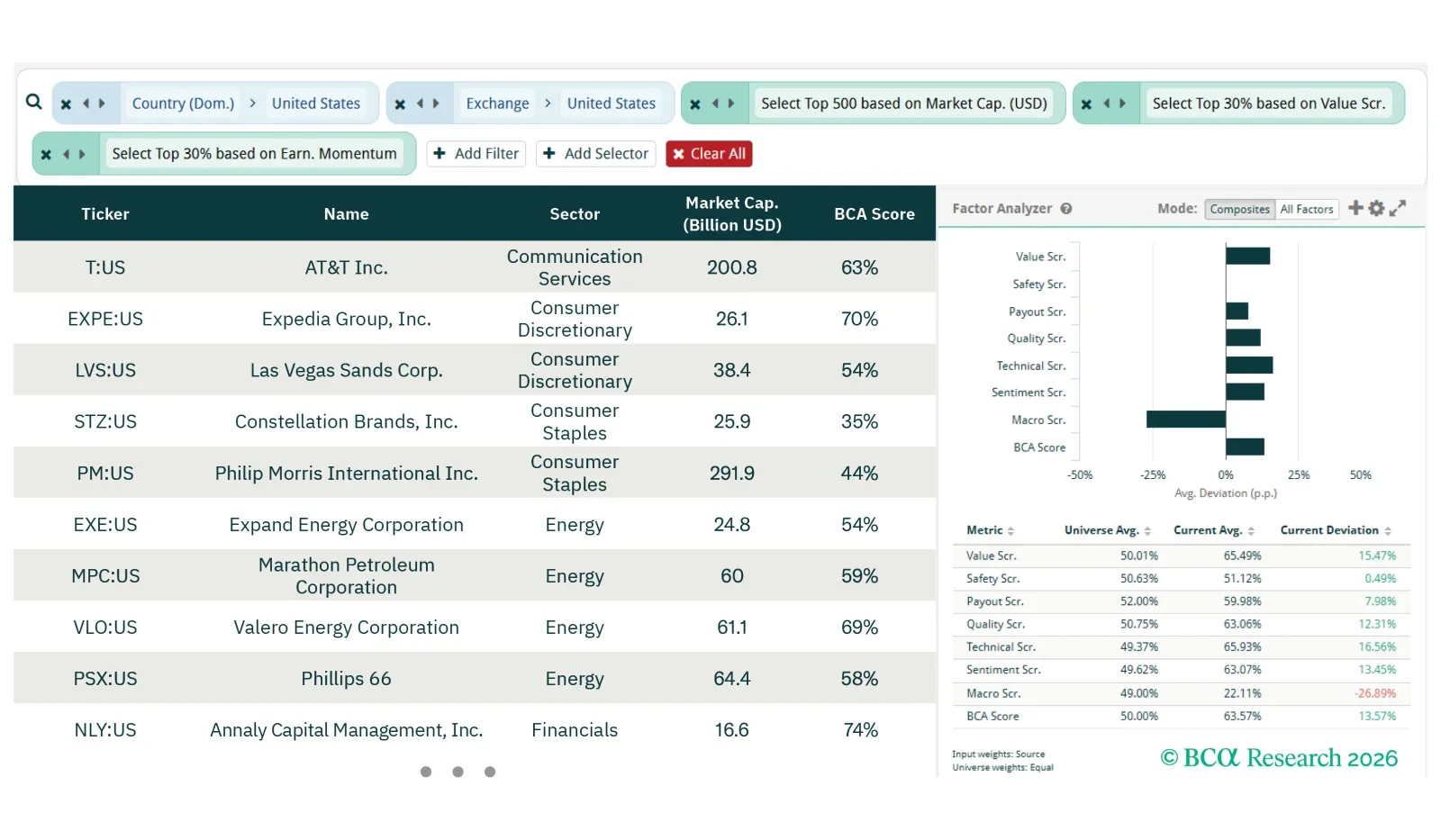

For this screener report, we explore opportunities in laggards with earnings momentum, Japanese semiconductors and US rate-sensitive stocks.

Earnings strength, durability, and breadth are all improving. As the market transitions from multiple-driven to earnings-driven returns, this backdrop supports continued gains in 2026—but with less concentration and greater scope for laggards to catch up rather than leaders to roll over.

Q3 results were strong but failed to impress investors, and Q4 will likely prove more challenging. Beneath the surface, earnings diverged sharply: Firms catering to affluent consumers maintained solid momentum, while those reliant on the mass market lagged. We remain equal weight Consumer Services and underweight Consumer Staples.