Economic Growth

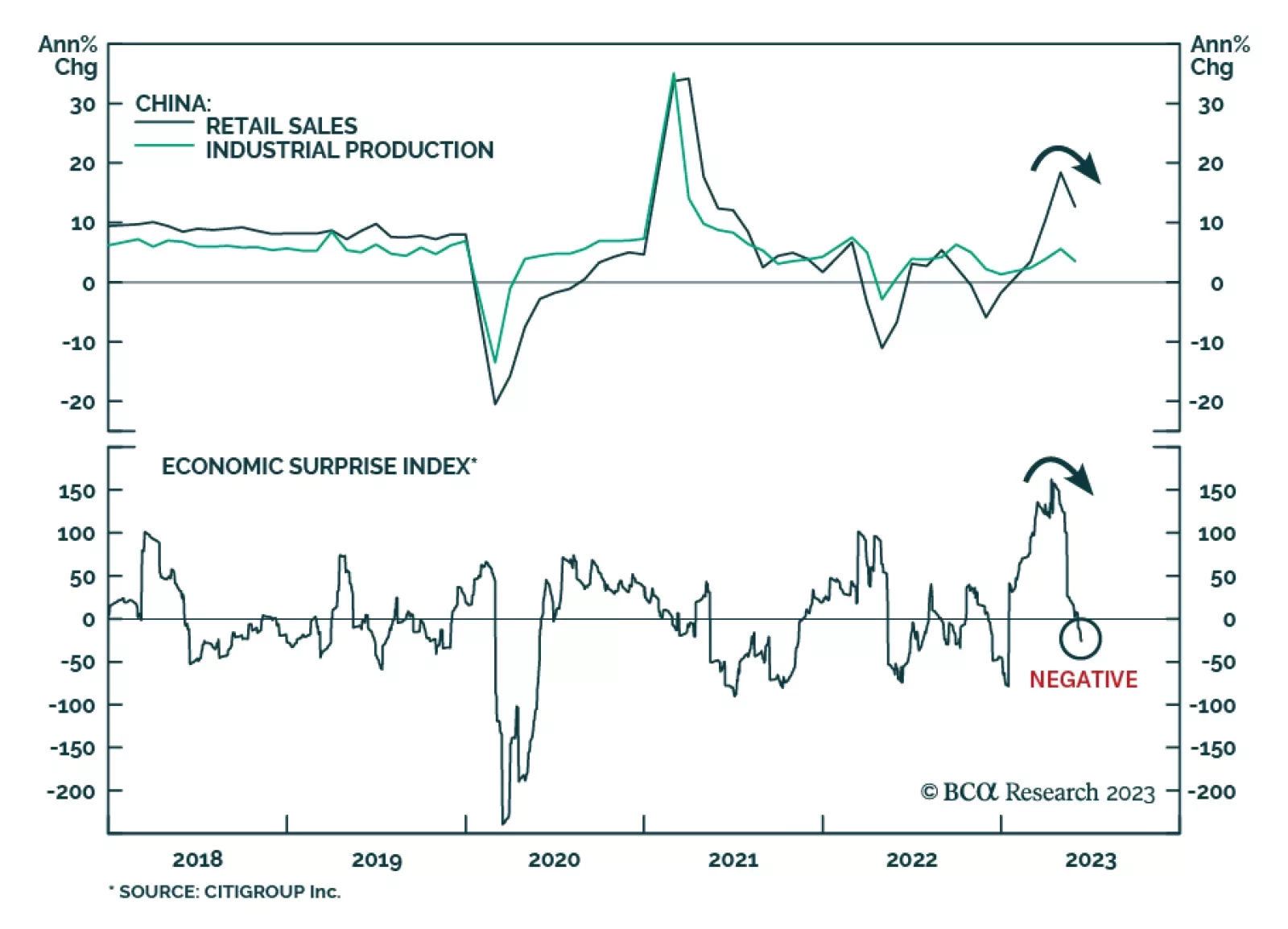

China is facing a risk of deflation. Marginal interest rate cuts and targeted stimulus will be insufficient to boost China’s growth given the current deflationary mindset and the danger is that the economy may be entering a liquidity trap. Deflation is bullish for government bonds, but negative for equity prices. Chinese share prices will continue to decline.

As the S&P 500 nears our 4,500 target, we review the rationale behind the call to assess its merit.

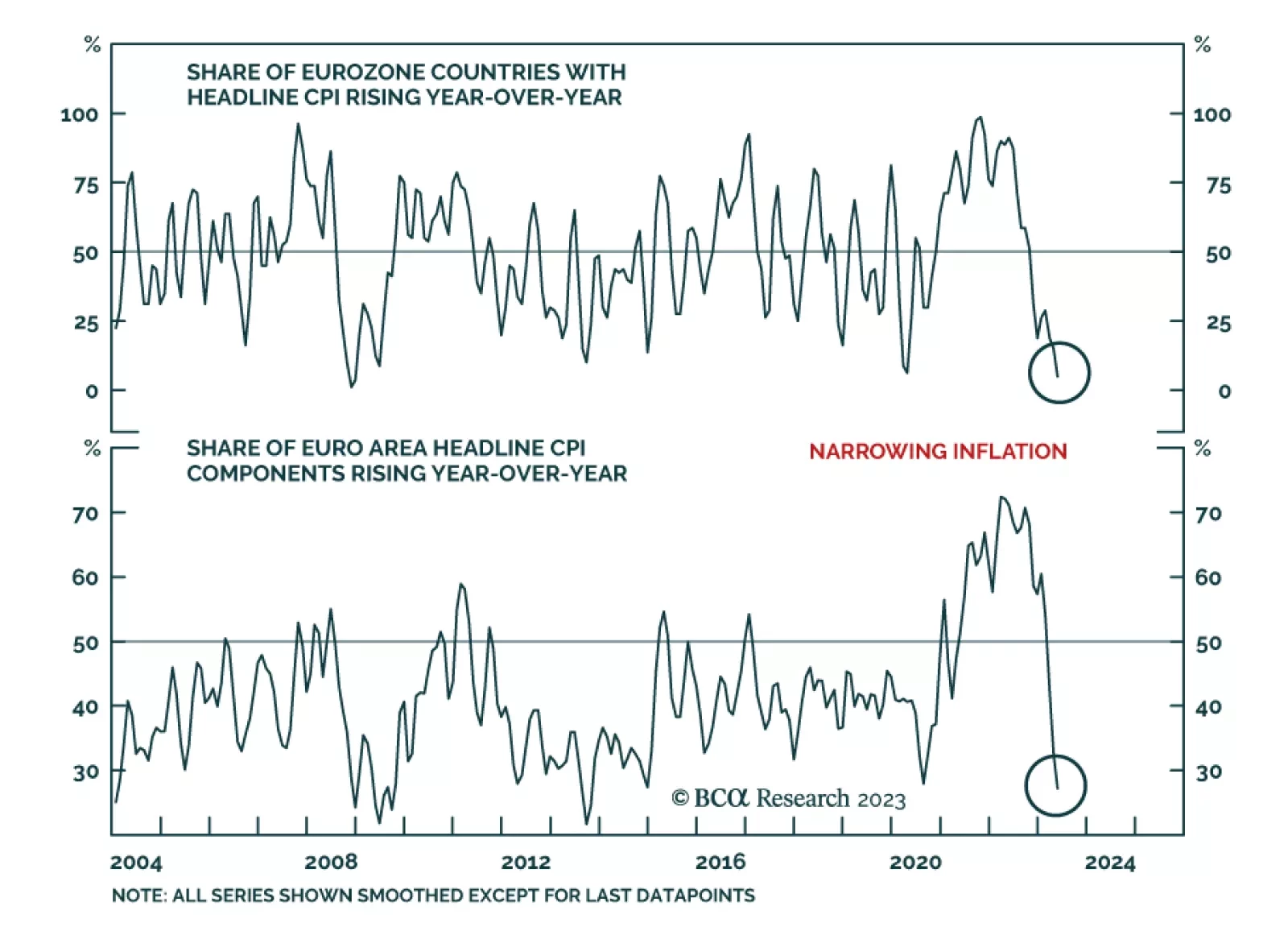

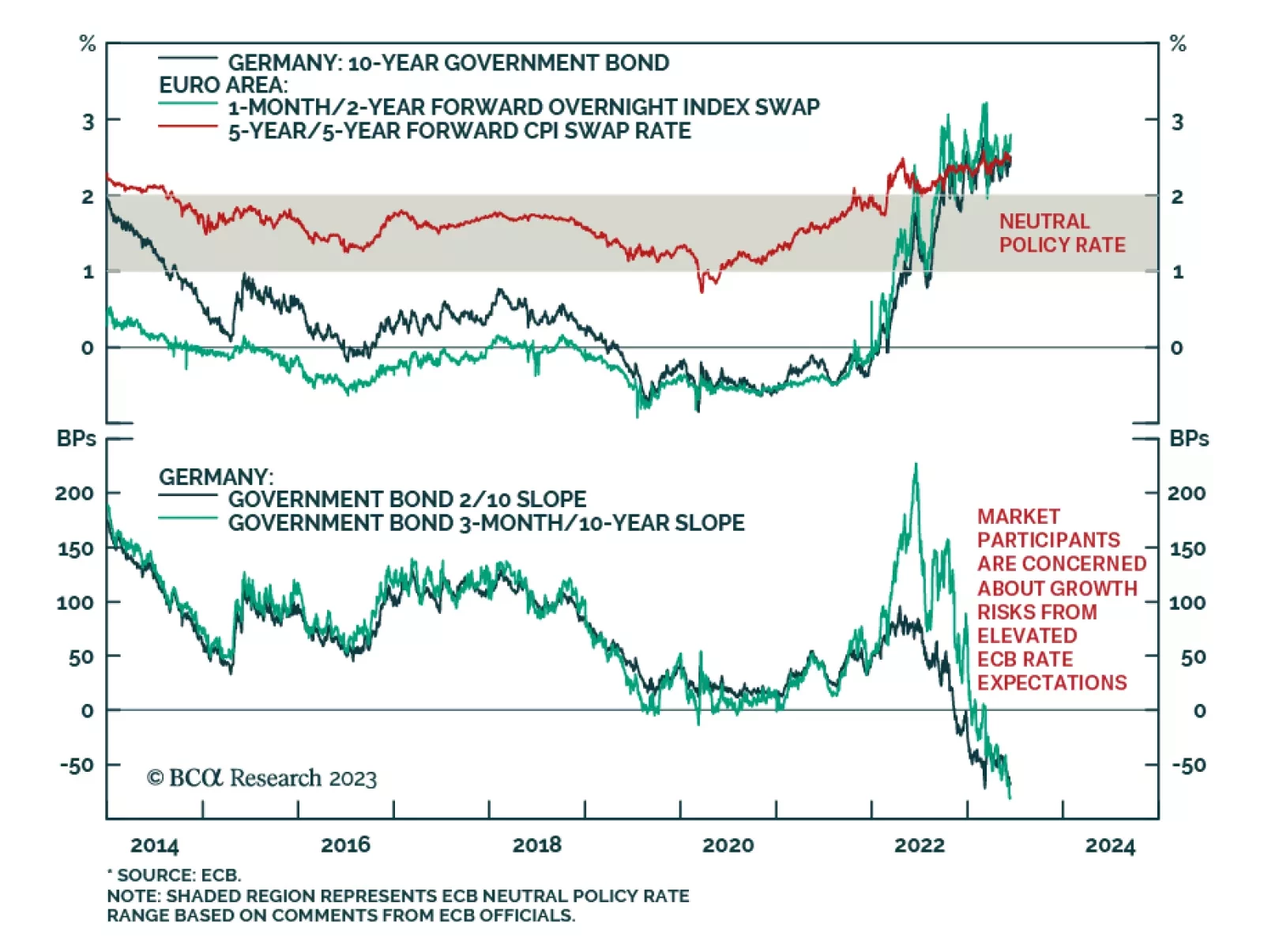

The Eurozone just experienced two consecutive quarters of GDP contraction. For the remainder of the year, can growth pick up or will the ECB decimate activity?

Global semiconductor demand will continue contracting, even though the pace of decline will moderate in 2023H2. While demand has increased briskly for Artificial Intelligence-type semiconductors, this will not be enough to lift aggregate global chip sales out of contraction. While momentum could push Emerging Asian semiconductor stocks higher in the short term, their share prices are vulnerable to the downside due to shrinking demand.