Economic Growth

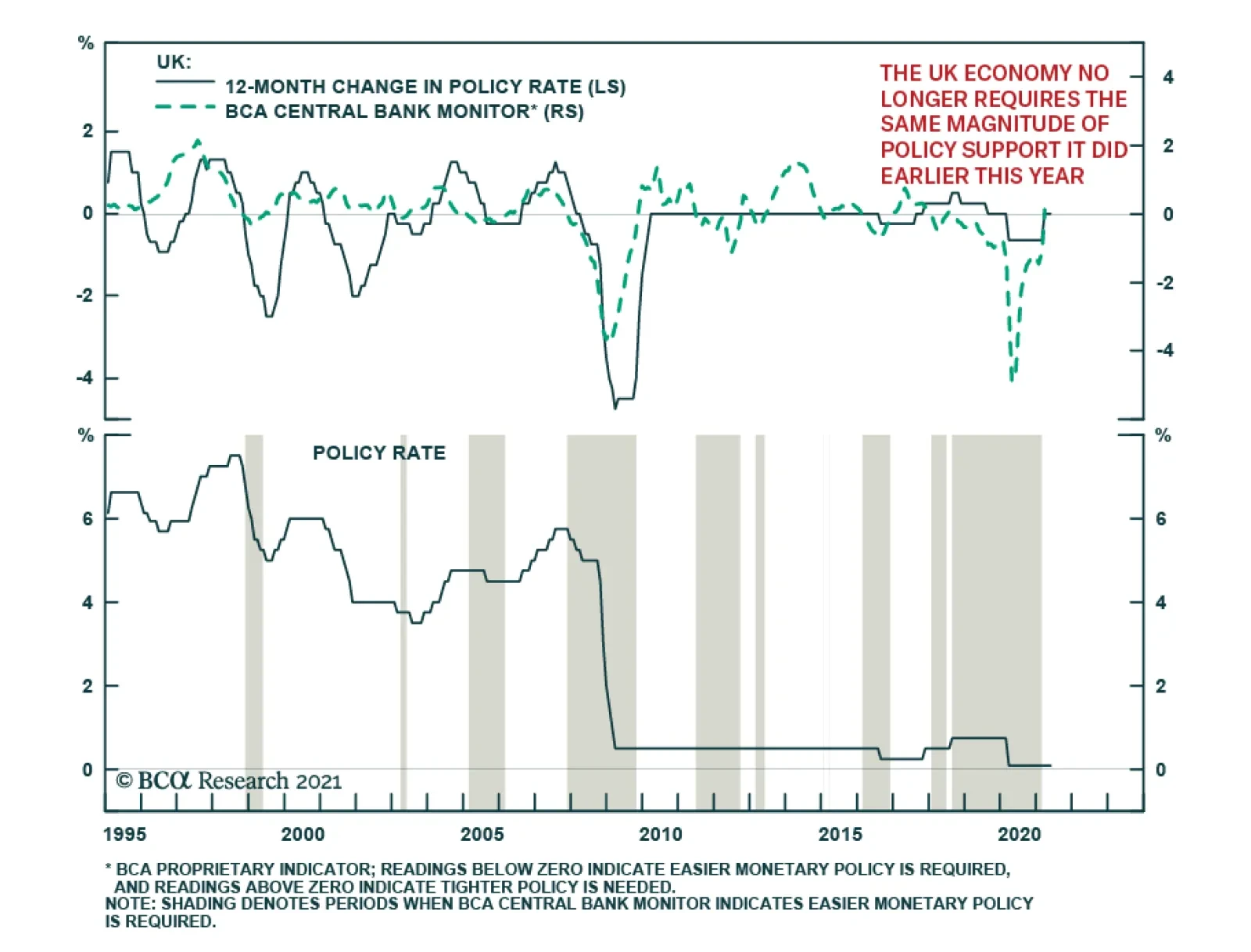

As expected, the Bank of England maintained the bank rate at 0.1% and kept the total target stock of asset purchases unchanged at its Thursday meeting. However, the central bank upgraded its growth outlook and now forecasts GDP to rise 7.25% in 2021 – up from…

Highlights US natural gas prices will remain well supported over the April-October injection season, as the global economic expansion gains traction, particularly in Europe, which also is refilling depleted storage levels. China's natgas demand is expected to rise more than 8% yoy, and EM Asia consumption also will be robust, which will revive US liquified natural gas (LNG) exports. Exports of US light-sweet crude into the North Sea Brent pricing pool – currently accounting for close to half the physical supply underpinning the global oil-price benchmark – also will increase over the course of the year, particularly in the summer, when maintenance will markedly reduce the physical supply of crudes making up the Brent index. At the margin, coal demand will increase in the US, as industrial natgas demand and LNG exports incentivize electric generators to favor coal. Higher-than-expected summer temperatures in the US also would boost coal demand. This will be tempered somewhat in Europe, where carbon-emissions rights traded through €50/MT for the first time this week on the EU's Emission Trading System (ETA). We expect US LNG and oil exports to revive this year (Chart of the Week) and remain long natgas in 1Q22. Feature The importance of US LNG and crude oil exports out of the US Gulf to the global economy is only now becoming apparent. As demand for these fossil fuels grows and the supply side continues to confront a highly uncertain risk-reward tradeoff, their importance will only grow. In natgas markets, US LNG cargoes out of the US Gulf balanced demand coming from Asia and Europe this past winter, which was sharply colder than expected and stretched supply chains globally. As a widening economic recovery from the COVID-19 pandemic spurs industrial, residential and commercial demand, and inventories in Europe and Asia are re-built in preparation for next winter, US LNG exports will be called upon to meet increasing demand, particularly since they are priced attractively vs regional importing benchmarks, with differentials vs the US presently $4+/MMBtu vs Europe and $5+/MMBtu vs Asia (Chart 2).1 Chart of the WeekUS LNG, Oil Export Growth Will Rebound

US LNG, Oil Export Growth Will Rebound

US LNG, Oil Export Growth Will Rebound

Chart 2Lower US Natgas Prices Encourage LNG Exports

Importance Of US Gas, Oil Exports Increases Daily

Importance Of US Gas, Oil Exports Increases Daily

In oil markets, an ongoing kerfuffle in the pricing of Brent Blend brought about by falling North Sea crude oil production makes American light-sweet crude oil exports from the Gulf (i.e., WTI produced mostly in the Permian Basin) account for almost half of the physical supplies in this critical benchmark-pricing market.2 US LNG Exports Will Increase US natural gas prices will remain well supported as the global economic expansion gains traction, and the US and Europe open the April-October injection season well bid (Chart 3). US inventories are expected to end the Apr-Oct injection season at just over 3.7 TCF according to the EIA, very close to where they ended the 2020 injection season. Chart 3US, Europe Rebuild Storage

Importance Of US Gas, Oil Exports Increases Daily

Importance Of US Gas, Oil Exports Increases Daily

Higher US LNG exports, industrial, commercial and residential demand will be offset by lower consumption from electric generators this year, netting to a slight decline in overall demand. The EIA expects generators to take advantage of lower generating costs to be had burning coal to produce electricity, a view we share given the current differentials in the forward curves for each fuel (Chart 4).3 On the supply side, the EIA's expecting output to remain unchanged from last year at just under 91.5 BCF/d in 2021. Higher LNG exports, even as generator demand is falling, pushes prices higher this year – averaging $3.04/MMBtu this year – which leads to a slight increase in output in 2022. For our part, we continue to expect higher prices during the November-March heating season than currently are clearing the market and remain long 1Q22 $3.50/MMBtu calls vs. short $3.75/MMbtu calls. As of Tuesday night, when we mark to market, this position was up 20.8% since inception on 8 April 2021. Chart 4Lower Prices Will Favour Increased Coal Demand

Lower Prices Will Favour Increased Coal Demand

Lower Prices Will Favour Increased Coal Demand

Natgas demand could surprise on the upside during the injection season if air-conditioning demand comes in stronger than expected and production remains essentially unchanged this year. This could reduce LNG exports and slow the rate of inventory refill in the US, which could further advantage coal as a burner fuel for generators in the US. The US National Weather Service's Climate Prediction Center expects above-average temperatures for most of the US population centers this summer (Chart 5). This could become a semi-permanent feature of the market if current temperature trends persist (Chart 6). Based on analyses’ run by the NOAA's National Centers for Environmental Information, 2021 "is very likely to rank among the ten warmest years on record," with lower (6%) odds of ranking in the top five hottest years on record.4 Chart 5Odds Of Hotter Summer Rising

Importance Of US Gas, Oil Exports Increases Daily

Importance Of US Gas, Oil Exports Increases Daily

Chart 6Higher Global Temperatures Could Become A Recurring Phenomenon

Importance Of US Gas, Oil Exports Increases Daily

Importance Of US Gas, Oil Exports Increases Daily

The Crude Kerfuffle As the Chart of the Week shows, US exports of light-sweet crude oil peaked at ~ 3.7mm b/d in February 2020, just before the COVID-19 pandemic hit the world full force. Exports out of the US Gulf – i.e., WTI priced against the Midland, TX, gathering hub – accounted for ~ 95% of these volumes. With exports currently running ~ 2.5mm b/d, more than 1mm b/d of readily available export capacity remains in place. Additional volumes will be developed as dredging of the Corpus Christi, TX, progresses. While the surge in US crude oil production has subsided in the wake of the pandemic, it most likely will revive as the markets return to normal operating procedure, additional dredging operations are completed, and storage facilities are built out.5 Existing and additional export capacity of the US's light-sweet crude could not arrive at a more opportune time for the Brent market, which remains in a state of uncertainty as to whether markets will have to adjust to CIF contracts or a work-around to the existing FOB pricing regime, which can be augmented to accommodate increasing WTI volumes.6 This will have to be sorted, as this is the future of the market's most important pricing index (Chart 7). The buildout in crude-oil exporting capacity – and natgas LNG exporting capacity, for that matter – ideally accommodates shale-oil- and -gas assets, which can be ramped up quickly to meet demand, and ramped down quickly as demand falters. The quick payback – 2 to 3 years – on these investments allow the producers to expand and contract output without the massive risks longer-lived conventional assets impose. As OPEC 2.0's spare capacity is returned to the market, this will be a welcome feature of a market that most likely will require oil and gas supplies for decades, despite the uncertainty attending oil-and-gas capex during the transition to a low-carbon energy future. Chart 7Permian Replaces North Sea Losses

Permian Replaces North Sea Losses

Permian Replaces North Sea Losses

Bottom Line: As the future of hydrocarbons evolves, the LNG and crude oil exported from the US Gulf will occupy an increasingly important role in these markets. Oil and gas producers are making capex decisions under increasingly uncertain conditions, which favor exactly the type of resources that have propelled the US to the position of the world's largest producer of these fuels – i.e., shale-oil and -gas. Production from these resources can be ramped up and down quickly as prices dictate, and have quick paybacks (2-3 years), which means capital is not tied up for decades as a return is earned.7 Robert P. Ryan Chief Commodity & Energy Strategist rryan@bcaresearch.com Ashwin Shyam Research Associate Commodity & Energy Strategy ashwin.shyam@bcaresearch.com Commodities Round-Up Energy: Bullish OPEC 2.0 begins returning 2mm b/d to the market this month, expecting to be done by July. Half of these volumes are accounted for by Saudi Arabia, which voluntarily cut output by 1mm b/d earlier in the year to help balance the market. In line with our maintained hypothesis that OPEC 2.0 prefers prices inside the $60-$70/bbl price band, we expect the return of curtailed production to be front-loaded so as to bring prices down from current levels approaching $70/bbl for Brent (Chart 8). If, as we expect, demand recovers sooner than expected as Europe leans into its vaccination program, additional barrels will be returned to the market to get prices closer to a $60-$65/bbl range. Base Metals: Bullish The International Copper Study Group (ICSG) forecast copper mine production will increase by ~ 3.5% in 2021 and 3.7% in 2022, after adjusting for historical disruption factors. This forecasted increase – after three years of flat mined production growth – is due to a ramp-up of recently commissioned and new copper mines becoming operational in 2021. An improvement in the pandemic situation by 2022 will also boost mined copper production, according to the ICSG. 2020 production remained flat as recoveries in production in some countries due to constrained output in 2019 balanced the negative impacts of the pandemic in others. In Chile, the largest copper producer, state-owned Codelco and Collahuasi reported strong results in March. However, this was countered by a continued downturn at BHP’s Escondida. The world’s largest copper mine saw a drop in production for the eighth consecutive month. This mixed output resulted in a decline in total production of 1.2% year-on-year in March. Precious Metals: Bullish COMEX palladium touched a record high during intraday trading on Tuesday, reaching $3,019/oz due to continued tight market conditions (Chart 9). On the supply side, Nornickel is recovering from flooded mines, which occurred in February. By mid-April, one of the two affected mines was operating at 60% capacity; however, the company's other mine is only expected to come back online by early June. On the demand side, strength in US vehicle sales and a global economic recovery from the pandemic buoyed the metal used in catalytic converters. Palladium prices closed at $2,981.60/oz on Tuesday. Ags/Softs: Neutral Corn again traded above $7/bu earlier in the week on the back of drought-like dry weather conditions in Brazil's principal growing regions and surging US exports, according to Farm Futures. Chart 8

Brent Prices Going Up

Brent Prices Going Up

Chart 9

Palladium Prices Going Up

Palladium Prices Going Up

Footnotes 1 Stronger demand from China – where consumption is expected to rise more than 8% yoy – and EM Asia will continue to support LNG demand through the year. S&P Global Platts Analytics expects Chinese natural gas demand to reach 12,713 Bcf in 2021, up 8.4% from the previous year. Chinese national oil company Sinopec is slightly more conservative in its outlook, expecting gas demand of ~ 12,006-12,184 Bcf in 2021, up 6-8% from 2020. China’s average annual increase in natural gas demand is expected to exceed 716 Bcf in the 14th FYP and reach 15,185 Bcf in 2025. 2 Please see CIF Brent Benchmark? published 3 March 2021 by the Oxford Institute for Energy Studies for a discussion. 3 In Chart 3, we plot a rough measure of coal- vs natgas-fired generation economics for these fuels based on their average operating heat rates published by the EIA. We would note that a carbon tax would erase much of the benefit accruing to coal at this point in time. 4 Please see NOAA's Global Climate Report - March 2021. 5 Please see Low Rider - Corpus Christi's Ship Channel Dredging Will Streamline Crude Oil Exports published by RBN Energy 3 May 2021. 6 The OIES analysis cited above concludes, "… the volumes of the FOB deliverable crudes are diminishing and some change, bolstering the contract is certainly needed. The most likely compromise is to retain the existing FOB Brent with an inclusion of CIF WTI Midland assessment, netted back to an FOB equivalent North Sea value." We agree with this assessment. Please see CIF Brent Benchmark? published 3 March 2021 by the Oxford Institute for Energy Studies, p. 8. 7 Please see Is shale activity actually profitable? Size matters, says Rystad published 7 February 2019. Investment Views and Themes Strategic Recommendations Tactical Trades Commodity Prices and Plays Reference Table Trades Closed in 2021 Summary of Closed Trades

Higher Inflation On The Way

Higher Inflation On The Way

Highlights Sweden’s economic recovery is robust and will deepen. Policy is accommodative. Very few advanced economies will benefit as much from the global economic rebound. The labor market will tighten, capacity utilization will increase, and inflation will rise faster than the Riksbank forecasts. On a one- to two-year investment horizon, the SEK is a buy against both the USD and the EUR. Despite their pronounced outperformance, Swedish stocks possess significantly more upside against both Eurozone and US equities over the remainder of the cycle. Swedish industrials will beat their competitors in both these markets. Nonetheless, China’s policy tightening creates a meaningful tactical risk, which selling Norwegian stocks can hedge. Italy’s fiscal plan constitutes a new salvo in Europe’s efforts to avoid last decade’s mistakes. Feature Last week, the Swedish Riksbank did not follow in the footsteps of the Norges Bank. The Swedish central bank acknowledged that the economy is performing better than anticipated and that the housing market is gaining in strength; yet, it refrained from hinting at any forthcoming adjustment to its policy rate or the pace of its asset purchase program. The positive outlook for the Swedish economy will force the Riksbank to tighten policy significantly before the ECB. As a result, we expect the Swedish Krona to outperform the euro and the US dollar. Moreover, investors should continue to overweight Swedish equities due to their large exposure to industrials and financials, even if they have already significantly outperformed the Euro Area. Sweden’s Economic Outlook The Swedish economy will accelerate, which will put pressure on resource utilization and fan inflationary risk in the years ahead. The degree of stimulus supporting Sweden is consequential. Chart 1A Dual Labor Market

A Dual Labor Market

A Dual Labor Market

On the fiscal front, the government support measures that have been announced since the beginning of the COVID-19 crisis currently amount to SEK420bn, or SEK197bn for 2020 (4% of GDP), and SEK223bn for 2021 (4.5% of GDP). Moreover, generous labor market protection and part-time employment schemes meant that the number of employees in permanent employment contracts remained stable during the pandemic (Chart 1). Thus, the bulk of the rise in Swedish unemployment came from workers on fixed-term contracts. Monetary policy remains very accommodative as well. The Riksbank left its repo rate unchanged at 0% through the crisis, but cut its lending rate from 0.75% to 0.1%. More importantly, the Swedish central bank is aggressively injecting liquidity into the economy. It set up a SEK500bn funding-for-lending facility in order to incentivize bank lending to the nonfinancial private sector, and started a SEK700bn QE program, which as of Q1 2021 had purchased SEK380bn securities and which will purchase another SEK120bn in Q2, with covered bonds issued by banks accounting for 70% of it. As a result, the amount of securities held on the Riksbank balance sheet will nearly triple by year end (Chart 2). Chart 2The Riksbank Is Open For Business

Take A Chance On Sweden

Take A Chance On Sweden

Beyond the monetary and fiscal stimulus, many factors point to greater economic strength for Sweden. Despite a slow start to the process, as of last week, nearly 30% of the Swedish population had received at least one vaccine dose, which is broadly in line with vaccination rates prevalent in France or Germany. Crucially, the pace of vaccination is accelerating at a rate of 13% per week. Even if this second derivative slows, more than 70% of the population will have received at least one dose by this summer. Thus, greater mobility is in the cards during the second quarter, which will boost household spending. Chart 3The Wealth Effect

The Wealth Effect

The Wealth Effect

The housing market also favors a pick-up in consumption. The HOX housing price index is growing at a 15% annual rate, its fastest expansion in over 5 years. As a result of the wealth effect, this rapid appreciation is consistent with a swift improvement in the growth rate of household expenditures (Chart 3). Moreover, spending on durable goods now stands 1.3% above its pre-pandemic levels, while spending on non-durables is back to pre-pandemic levels. This context suggests that increased mobility translates into greater spending. The industrial sector remains a particularly bright spot in the Swedish economy. Sweden is extremely sensitive to the global industrial and trade cycle, because exports represent 45% of GDP. Moreover, the highly cyclical intermediate and capital goods comprise 56% of the country’s foreign shipments, which accentuates the beta of the Swedish economy. BCA Research remains optimistic about the global industrial cycle. Sweden will reap a significant dividend. Already the Swedish PMI points to stronger industrial production, and the index’s exports component is roaring ahead (Chart 4). The potential for a greater uptake in consumption, capex, and durable goods spending in the rest of the EU (Sweden’s largest trading partner) bodes well for the Swedish manufacturing sector. Additionally, if the collapse in the US inventory-to-sales ratio is any indication for the rest of the world, a global restocking cycle is forthcoming, which will further boost Swedish industrial activity (Chart 4, bottom panels). Finally, global public infrastructure plans are on the rise, which will also help Sweden. Chart 4Sweden Is well Placed

Sweden Is well Placed

Sweden Is well Placed

Chart 5Brightening Labor Market Prospects

Brightening Labor Market Prospects

Brightening Labor Market Prospects

In this context, the Swedish labor market should tighten significantly in the approaching quarters. Already, job vacancies are rebounding, and redundancy notices have normalized, which matches both the GDP growth surprise in Q1 and the continued rise in the NIER Sweden Economic Tendency Indicator. Furthermore, the employment component of the PMIs stands at 58.9 and is consistent with a sharp improvement in job growth over the coming year (Chart 5). The expected labor market growth will contribute to an increase in capacity utilization, which will place upward pressure on wages and inflation. When the 12-month moving average of US and Eurozone imports rises, so does the Riksbank Resource Utilization Indicator, because global trade has such a pronounced effect on the Swedish economy (Chart 6). Meanwhile, greater resource utilization leads to accelerated inflation, greater labor shortages, and rising unit labor costs (Chart 7). Chart 6CAPU Will Rise

CAPU Will Rise

CAPU Will Rise

Chart 7The Coming Pressure Buildup

The Coming Pressure Buildup

The Coming Pressure Buildup

Bottom Line: As a result of generous stimulus and the global economic recovery, the Swedish economy is set to continue its rebound. Consequently, employment and capacity utilization will improve meaningfully, which will lead to a resurgence of inflation and wages in the coming 24 months. Investment Implications On a 12 to 24 months horizon, we remain positive on the Swedish krona and Swedish equities. Fixed Income And FX Chart 8Three Hikes By 2025

Three Hikes By 2025

Three Hikes By 2025

The backend of the Swedish OIS curve only discounts 75bps of hikes by 2025. This pricing is too modest (Chart 8). The Swedish economy will rebound further as the vaccination campaign advances, and rising house prices and household indebtedness will fan growing long-term risk to financial stability, both of which suggest that the Riksbank will have to change its tack in 2022. The great likelihood that the Fed will start tapering off its asset purchase toward the end this year, that the ECB will follow sometime in 2022, and that the Norges Bank will be increasing interest rates next year will give more leeway to the Swedish central bank. A wider Sweden/Germany 10-year government bond spread is not an appealing vehicle to play a more hawkish Riksbank down the road. This spread hit a 23-year high in March and now rests at 62bps or its 98th percentile since 2000. Moreover, the terminal rate proxy embedded in the German money market curve is currently so low that the spread between Sweden’s and the Eurozone’s terminal rate proxy stands near a record high. Hence, German yields already embed much more pessimism than Swedish ones. Nonetheless, BCA recommends a below benchmark duration exposure within the Swedish fixed-income space, as we do for other government bond markets around the world.1 A bullish bias toward the SEK is a bet on the Riksbank that offers a very appealing risk/reward ratio, according to BCA Research’s Foreign Exchange Strategy strategists.2 The krona is very cheap against both the euro and the US dollar, trading at 9% and 29% discounts to purchasing power parity, respectively. Moreover, the Swedish current account stands at 5.2% of GDP, compared to 2.3% and -3.1% for the Euro Area and the US, creating a natural underpinning under the SEK. Chart 9The SEK Loves Growth

The SEK Loves Growth

The SEK Loves Growth

Over the coming 12 to 24 months, cyclical forces favor selling EUR/SEK and USD/SEK on any strength. The SEK is one of the most cyclical G-10 currencies and has one of the strongest sensitivities to the US dollar. Hence, our positive global economic outlook and our FX strategists negative view on the greenback are synonymous with a weak USD/SEK. These same factors also mean that the krona will appreciate more than the euro, as the negative correlation between EUR/SEK and our Boom/Bust Indicator and global earnings growth illustrate (Chart 9). Equities We also like Swedish equities, but the state of the Swedish economy and the evolution of the Riksbank policy surprise have a limited impact on Swedish equities. The Swedish bourse is mostly about the evolution of the global business cycle. The Swedish benchmark heightened sensitivity to the global business cycle reflects its massive overweight in deep cyclicals, with industrials, financials, consumer discretionary, and materials accounting for 38.4%, 26.1%, 9.7% and 3.7% of the MSCI index respectively, or 78% altogether (Table 1). As a result, BCA’s preference for global cyclicals at the expense of defensives and this publication’s fondness for the recovery laggards like the industrial and financial sectors automatically translate into a favorable bias toward Sweden’s stocks.3 Table 1Mamma Mia! That’s A Lot Of Cyclicals

Take A Chance On Sweden

Take A Chance On Sweden

Valuations offer a more complex picture, but they do not diminish our predilection for Sweden. Swedish equities trade at a discount to US stocks but at a premium to Euro Area ones (Chart 10). However, Swedish stocks offer higher RoEs and profit margins than both the US and the Euro Area, while also sporting lower leverage (Chart 11). Thus, their valuation premium to Euro Area stocks is warranted and their discount to US ones is excessive, especially when rising yields hurt the relative performance of the growth stocks that dominate US indexes. Chart 10Swedish Discounts And Premia

Swedish Discounts And Premia

Swedish Discounts And Premia

Chart 11Profitable Sweden

Profitable Sweden

Profitable Sweden

The outlook for Swedish earnings is appealing, both in absolute and relative terms. The Swedish market’s extreme sensitivity to global economic activity means that Sweden’s EPS increase and beat US profits when the Riksbank Resource Utilization Indicator expands (Chart 12). These relationships are artefacts of the Swedish economy’s pro-cyclicality, which causes capacity utilization to interweave tightly with the global business cycle (Chart 6). Chart 12The Winner Takes It All

The Winner Takes It All

The Winner Takes It All

Chart 13Better Capex Play Than You

Better Capex Play Than You

Better Capex Play Than You

Global capex and infrastructure spending favor Swedish equities compared to Euro Area ones. Over the past thirty years, Sweden’s stocks have outperformed those of the Eurozone when capital goods orders in the advanced economies have expanded (Chart 13). This reflects the Swedish benchmark’s large overweight in industrials, a sector that is the prime beneficiary of global capex. Capital goods orders are recovering well, and their growth rate can climb higher, especially as western multinationals announce capex plans and as governments from the US to Italy intend to ramp up infrastructure spending. Moreover, the large pent-up demand for durable goods in the Eurozone further enhances the potential of industrial firms, and thus, of Swedish equities.4 Chart 14Another Sign Of Pro-Cyclicality

Another Sign Of Pro-Cyclicality

Another Sign Of Pro-Cyclicality

BCA Research’s positive cyclical stance on commodities offers another reason to overweight Sweden’s market relative to that of the US and the Euro Area. Our Commodity and Energy Strategy sister service anticipates significant further upside for natural resources, especially base metals, over the remainder of the business cycle.5 Commodity prices still have room to rally, because demand will grow as the global economy continues to recover and because the supply of natural resources has been constrained by a decade of low investment. As a result, rising metal prices will symptomatize strong economic activity around the world and will incentivize capex in commodity extraction, both of which will boost the revenue of industrial firms. Furthermore, commodity price inflation often corresponds with rising yields, which boosts financials as well. These relationships explain the Swedish stocks’ outperformance of US and Eurozone stocks, when natural resource prices rally, despite the former’s low exposure to materials (Chart 14). At the sector level, the appeal of Swedish industrials relative to those of the Eurozone and the US completes the rationale to favor Swedish equities in a global portfolio. Swedish industrials are just as profitable as US ones and are more so than Euro Area ones, while having significantly lower leverage than either of them (Chart 15). Additionally, for the past two years, the EPS growth of Swedish industrials has bested that of US and Eurozone ones. Yet, their forward P/E ratio trades in line with the US and the Euro Area, while the sell-side’s long-term relative earnings growth estimate is too depressed (Chart 16). The same observations are valid when comparing Swedish industrials to French or German ones. Hence, in the context of a global business cycle upswing, buying Swedish industrials while selling their US and Euro Area competitors is an appealing pair trade, especially since it also involves short USD/SEK and short EUR/SEK bets. Chart 15Attractive Swedish Industrials...

Attractive Swedish Industrials...

Attractive Swedish Industrials...

Chart 16...And Not Expensive

...And Not Expensive

...And Not Expensive

Despite our optimism toward Swedish stocks on a 12 to 24 months basis, investors must hedge a near-term risk. Chinese authorities are aiming to contain financial excesses and trying to restrain credit growth. As we showed four weeks ago, China’s excess reserve ratio is contracting, which points toward a slowdown in the Chinese credit impulse.6 Historically, such a development can hurt global cyclicals, and thus, also Swedish equities. However, BCA Research’s China strategists believe that Beijing will not kill off the Chinese business cycle; thus, the recent disappointment in the Chinese PMI is transitory.7 Chart 17Industrials vs Materials: Europe vs China

Industrials vs Materials: Europe vs China

Industrials vs Materials: Europe vs China

Materials more than industrials will suffer the brunt of a China slowdown, as the re-opening trade and capex cycle among advanced economies will create a buffer for the latter. Indeed, the performance of global industrials relative to materials stocks correlates with the evolution of the spread between the Euro Area and Chinese PMI (Chart 17). Thus, we recommend selling Norwegian equities to hedge the tactical risk inherent in an overweight on Sweden. As Table 1 above shows, Norway overweighs materials and energy (two sectors greatly exposed to China), hence, a temporary pullback in commodity prices should hurt Norwegian stocks more than Swedish ones. Bottom Line: The SEK is an inexpensive and attractive vehicle to bet on both the global business cycle strength and the Swedish economic recovery. Thus, investors should use any rebound in EUR/SEK and USD/SEK to sell these pairs. Moreover, Swedish stocks greatly overweight cyclical sectors, particularly industrials and materials. This sectoral profile renders Swedish equities as attractive bets on the global economy. Additionally, Swedish shares display alluring operating metrics. As a result, we recommend investors go long Swedish industrials relative to those of the US and Euro Area. They should also overweight Swedish equities against the US and the Eurozone. Consequent to some China-related tactical risks, an underweight stance on Norwegian stocks constitutes an attractive hedge to this Swedish exposure. A Few Words On Italy’s National Recovery And Resilience Plan Mario Draghi’s plan to revive the Italian economy, announced last week, is an important marker of Europe’s changing relationship with fiscal policy. Last decade, excessive austerity contributed to subpar growth, ultimately firing up concerns about debt sustainability in many peripheral economies, and fueled risk premia in Italy and Spain. Under the cover of the current crisis, and in the face of the changing political winds in Brussel and Berlin where fiscal rectitude is not the mantra it once was, national European governments are beginning to propose ambitious fiscal stimulus plans. The National Recovery and Resilience program illustrates these dynamics. The EUR248bn plan is a testament to the importance of the NGEU recovery program as well as the REACT EU recovery fund. Through these facilities, the EU will contribute EUR191.5bn to the fiscal plan via grants and loans. Italy will contribute the remainder of the funds. While the total amount disbursed over the next six years corresponds to 14% of Italy’s 2019 GDP, the Draghi government estimates that the program will add 3.2 percentage points to GDP between 2024 and 2026. Importantly, markets are not rebelling. Despite expectations that Italy would continue to run an accommodative fiscal policy, the BTP/Bund spreads remain stable. We can expect this trend of greater stimulus to be mimicked around the EU. Spain is another large recipient of the NGEU program, and it too is likely to increase stimulus beyond what the EU will fund. France will hold an election in May 2022, and President Macron has all the incentives to stimulate the economy between now and then. If, as we wrote last week, Germany shifts to the left in September, then this outcome will be guaranteed. Bottom Line: The Draghi plan is the first salvo of greater fiscal stimulus in the EU. This trend will help Eurozone growth improve relative to the US over the coming few years. Despite a loose fiscal policy, BTPs and other peripheral bonds will continue to outperform on the back of declining risk premia. Mathieu Savary, Chief European Investment Strategist Mathieu@bcaresearch.com Footnotes 1Please see Global Fixed Income Strategy “GFIS Model Bond Portfolio Q1/2021 Performance Review & Current Allocations: Grand Reopening,” dated April 6, 2021, available at gfis.bcaresearch.com 2Please see Foreign Exchange Strategy “2021 Key Views: Tradeable Themes,” dated December 4, 2020, available at fes.bcaresearch.com 3Please see European Investment Strategy “Summer Of ‘21,” dated March 22, 2021, available at eis.bcaresearch.com 4Please see European Investment Strategy “Winds Of Change: Germany Goes Green,” dated April 23, 2021, available at eis.bcaresearch.com 5Please see Commodity & Energy Strategy “Industrial Commodities Super-Cycle Or Bull Market?” dated March 4, 2021, available at ces.bcaresearch.com 6Please see European Investment Strategy “The Euro Dance: One Step Back, Two Steps Forward,” dated March 29, 2021, available at eis.bcaresearch.com 7Please see China Investment Strategy “National People’s Congress Sets Tone For 2021 Growth,” dated March 17, 2021, available at cis.bcaresearch.com Cyclical Recommendations Structural Recommendations Currency Performance

Take A Chance On Sweden

Take A Chance On Sweden

Fixed Income Performance Government Bonds

Take A Chance On Sweden

Take A Chance On Sweden

Corporate Bonds

Take A Chance On Sweden

Take A Chance On Sweden

Equity Performance Major Stock Indices

Take A Chance On Sweden

Take A Chance On Sweden

Geographic Performance

Take A Chance On Sweden

Take A Chance On Sweden

Sector Performance

Take A Chance On Sweden

Take A Chance On Sweden

Closed Trades

Highlights The kiwi will continue to benefit from a pandemic-free recovery and normalization in monetary policy from the RBNZ. However, the kiwi is becoming expensive according to most of our models. This will begin to impact growth via the trade channel. For the rest of the year, the NZD/USD could hit 75 cents, but will likely underperform other developed market currencies. Feature Chart I-1NZD And Relative Economic Growth

NZD AND RELATIVE ECONOMIC GROWTH

NZD AND RELATIVE ECONOMIC GROWTH

New Zealand has been one of the few countries to get the COVID-19 pandemic under control in short order. Since June of last year, the number of new infections has been practically zero. The vaccination program is lagging most other developed countries, but the authorities expect most citizens will be inoculated by the end of this year. The travel bubble with Australia has opened up the service sector to a recovery that remains the envy of most other developed economies. The New Zealand dollar has responded in tandem with the improvement in domestic conditions (Chart I-1). While the USD is up this year, NZD has still appreciated by about 1% against the dollar. From the March lows last year, the kiwi is up 22%, only trailing the Australian dollar and Norwegian krone within the G10. In this report, we explore the outlook for the kiwi, looking at key drivers such as the pandemic, the commodities boom, and the prospect for monetary policy amidst a hot housing market. In our view, the NZD still faces upside, but less so than other developed market currencies. A Robust Recovery Together with Singapore and Australia, Bloomberg ranks New Zealand as one of the safest places to be during the pandemic. This has allowed the manufacturing PMI in New Zealand to hit fresh highs, easily surpassing very robust activity in the US. Relative economic performance between New Zealand and its trading partners has tended to define the trend in the currency. The services sector is still trailing behind, as most of the world remains under lockdown (Chart I-2). However, a travel bubble has opened up with Australia, and it is fair to assume that service-sector activity is a coiled spring ready to rebound, especially as tourism constitutes a non-negligible share of New Zealand GDP (Chart I-3). Chart I-2A Recovery In Services Underway

A RECOVERY IN SERVICES UNDERWAY

A RECOVERY IN SERVICES UNDERWAY

Chart I-3Tourism Will Boost NZ GDP

TOURISM WILL BOOST NZ GDP

TOURISM WILL BOOST NZ GDP

Employment in New Zealand has already seen a sizeable recovery. The unemployment rate hit 4.9% in December, very close to the Reserve Bank of New Zealand’s (RBNZ) own estimate of NAIRU. Next week’s release should show an even more robust rebound. Inflation remains well contained at 1.5%, but as the economy begins to bump against supply-side constraints, this should change. The quarterly employment survey showed that wages are rising at a 4% clip. Eventually, a labour market that has fully recovered, burgeoning inflationary pressures and an economy open for business will mean the need for the RBNZ to maintain emergency monetary policy settings will be eliminated. A Terms-Of-Trade Boom While the domestic economy has benefited from strong government support, and very accommodative monetary policy settings, the external environment has also provided a gentle tailwind for the New Zealand economy. Over the last few decades, one of the key primary drivers of the NZD exchange rate has been terms of trade. New Zealand’s top exports are predominantly in agricultural commodities. Strong export growth has boosted the trade balance, both in volume and price terms (Chart I-4). An increasing trade balance naturally means that NZDs are being buffeted with demand. China has led the pack in imports from New Zealand vis-à-vis other countries by simple virtue of the fact that the authorities started injecting stimulus much earlier on, which helped ease domestic financing conditions. China is also New Zealand’s biggest export market. While the credit impulse in China is set to slow this year, demand for foodstuffs is less sensitive compared to demand for other higher-beta commodities. This will support New Zealand exports. At the same time, there has been a supply component to the boom in agricultural commodity prices. Adverse weather has impacted the planting season for many agricultural goods. As a result, stock-to-use ratios have begun to roll over, particularly in some of the goods that New Zealand exports (Chart I-5). This is likely to reverse, as farmers take advantage of higher prices and increase productivity. Chart I-4A Terms Of Trade ##br##Boom

A TERMS OF TRADE BOOM

A TERMS OF TRADE BOOM

Chart I-5Falling Stocks Have Boosted Agricultural Prices

FALLING STOCKS HAVE BOOSTED AGRICULTURAL PRICES

FALLING STOCKS HAVE BOOSTED AGRICULTURAL PRICES

In a nutshell, the outperformance of the kiwi has been a combination of supply shocks in the agricultural market, and an economy that has had an impressive rebound. Going forward, the kiwi should continue to do well versus the dollar as economic momentum picks up. The Housing Mandate Housing prices in New Zealand have been on a tear (Chart I-6). As a result, the government has mandated that house price considerations be tied into monetary policy decisions. The direct implication of this is that interest rates in New Zealand are set to increase. In the coming months, the labor market mandate for the RBNZ is about to become a lot tougher, because of the opposing forces between financial and economic stability. Tightening monetary policy too fast and too soon will expose the economy to a potential relapse in growth. But allowing housing prices to continue to become unaffordable for most residents is both politically untenable and economically unsustainable. The end game is likely to be as follows: The RBNZ will be quick to tighten monetary policy on domestic grounds and housing market concerns. This will provide a further boost to the kiwi. Yields in New Zealand are already among the highest in the G10, which will only accelerate with tighter monetary conditions. By the same token, the Chinese economy will likely slow as the credit impulse is peaking. This means New Zealand domestic growth will become more important for the NZD than external conditions. Countries with relatively easier monetary policy will see some benefit. Particularly, the Reserve Bank of Australia might lag the RBNZ. If this eventually benefits the Aussie economy, it might hurt the AUD/NZD cross now, but might make way for fresh long positions later (Chart I-7). Chart I-6A Housing Market Boom

A HOUSING MARKET BOOM

A HOUSING MARKET BOOM

Chart I-7Where Next For AUD/NZD?

WHERE NEXT FOR AUD/NZD

WHERE NEXT FOR AUD/NZD

Historically, housing prices in New Zealand have correlated quite strongly with the exchange rate. If the RBNZ is successful in engineering lower housing prices, it will also succeed in weakening the NZD (Chart I-8). Chart I-8House Prices And The Kiwi

HOUSE PRICES AND THE KIWI

HOUSE PRICES AND THE KIWI

We were stopped out of our long AUD/NZD trade last week for a modest profit of 2.3%. We are standing aside for the time being, but will be buyers of the cross at 1.05. This will likely be realized towards the end of this year when optimism on the kiwi is likely to peak. How High Can The NZD Bounce? Another reason why the rise in the NZD might soon face strong upside resistance is valuation. Usually, a rise in the NZD over a cycle goes uninterrupted until the cross becomes expensive. On this basis, the kiwi might soon peak. Our purchasing power parity (PPP) models point to a 10% overvaluation in the New Zealand dollar (Chart I-9) versus the USD. Chart I-9The NZD Is Expensive

THE NZD IS EXPENSIVE

THE NZD IS EXPENSIVE

One of our favorite metrics for the kiwi’s fair value is its real effective exchange rate relative to its terms of trade. On this basis, the New Zealand dollar is around fair value. On a longer-term real effective exchange rate basis (REER), the kiwi is 7.4% expensive, or 0.7 standard deviation above the mean (Chart I-10). Chart I-10The NZD Is Expensive

THE NZD IS EXPENSIVE

THE NZD IS EXPENSIVE

The equity market in New Zealand looks particularly vulnerable. Heavily weighted in defensive sectors, this bourse will be particularly vulnerable to a rise in yields that will derail potential equity inflows (Chart I-11). Chart I-11Kiwi Stocks Are Expensive

KIWI STOCKS ARE EXPENSIVE

KIWI STOCKS ARE EXPENSIVE

Chart I-12CHF/NZD Could Rise With Volatility

CHF/NZD COULD RISE WITH VOLATILITY

CHF/NZD COULD RISE WITH VOLATILITY

Another opportunity is to buy the CHF/NZD cross, which looks attractive at current levels (Chart I-12). Should markets experience some form of turbulence, the cross will benefit. Meanwhile, CHF/NZD just dipped to the upward sloping trend line that has dictated support levels for this cross since 2007. Thus, we recommend investors initiate a long position in CHF/NZD. Chester Ntonifor Foreign Exchange Strategist chestern@bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

The data out of the US were mildly positive this week. Quarter-on-quarter annualized GDP growth came in at 6.4% in Q1, rising from 4.3% in the previous quarter. Initial jobless claims fell to 553K in the week ended April 23, from 566K the previous week. Consumer Confidence for April came in at 121.7 beating the expected 113. The S&P/Case-Shiller House Price Index rose 11.9% year-on-year in February. Fed maintained the target range for the Fed Funds rate at 0 to 0.25%. The US dollar DXY index was flat this week. Although the dollar advanced earlier in the week with treasury yields posting small gains, it weakened on Wednesday ahead of the Fed meeting. Compared to the record-breaking preliminary PMIs of last Friday, milder data this week and the dovish tone of the Fed aren’t helping the downward trend of the dollar. Report Links: Arbitrating Between Dollar Bulls And Bears - March 19, 2021 The Dollar Bull Case Will Soon Fade - March 5, 2021 Are Rising Bond Yields Bullish For The Dollar? - February 19, 2021 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent euro area data have been soft. The IFO Business Climate Index inched up only 0.2 points to 96.8 and disappointed expectations of a much more significant increase to 97.8. The BNB Business Barometer of Belgium surprised to the upside and jumped to a decade high of 4.4 from a revised 1.04. The German GfK Consumer Confidence contracted to -8.8 for May and the French Consumer Confidence stayed the same in April. The euro strengthened by 0.5% against the US dollar this week. The uneven data out of Europe reflects differences in COVID restrictions throughout the region. Tighter measures were announced in some German regions and Belgium is easing restrictions. However, overall, we remain optimistic on the outlook for the entire region as the accelerating vaccination effort should support the economy reopening this summer. We are long EUR/CHF. Report Links: Relative Growth, The Euro, And The Loonie - April 16, 2021 Portfolio And Model Review - February 5, 2021 On Japanese Inflation And The Yen - January 29, 2021 The Japanese Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

The data out of Japan was scant this week. Bank of Japan maintained interest rates at -0.1%. Retail Sales in March grew 5.2% year-on-year, beating forecasts of 4.7%. The Japanese yen weakened by 0.5% this week. Due to the current state of emergency throughout the country, the Bank of Japan is ready to further ease monetary policy as needed and warned of the likelihood for consumption to stay depressed. That said, our intermediate term indicator is hinting at a rebound in the currency. Report Links: The Dollar Bull Case Will Soon Fade - March 5, 2021 On Japanese Inflation And The Yen - January 29, 2021 The Dollar Conundrum And Protection - November 6, 2020 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

The data out of the UK this week was positive. The Confederation of British Industry (CBI) retail sales volume balance rose to 20 in April from -45 in March, recording the sharpest growth since 2018. The British pound rose by 0.7% against the US dollar this week. The strong retail sales numbers came amidst lockdowns being lifted. While May will continue to see further restrictions eased, cable faces threats from its own success so far this year as well as UK’s recent political turmoil. Also, both the speculative positioning and our intermediate-term indicator are at elevated levels. Report Links: Portfolio And Model Review - February 5, 2021 The Dollar Conundrum And Protection - November 6, 2020 Revisiting Our High-Conviction Trades - September 11, 2020 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

The data out of Australia have been soft lately. CPI in Q1 rose 0.6% versus Q4 last year, below the expected 0.9%. The year-on-year growth of 1.1% also undershot the 1.4% forecast. Trimmed mean CPI grew 0.3% on the prior quarter and 1.1% versus a year ago, both failing to beat expectations. The Q1 export price index rose 11.2% over the prior quarter, compared to the 5.5% rise in Q4. The Australian dollar rose by 1% against the US dollar this week. In addition to both CPI measures disappointing to the downside, a foreseeable peak in the commodity market driven by the slowdown in China can also be a downward drag on the currency especially when the sentiment on the Aussie is elevated. We are short AUD/MXN and were stopped out of our long AUD/NZD trade. Report Links: The Dollar Bull Case Will Soon Fade - March 5, 2021 Portfolio And Model Review - February 5, 2021 Australia: Regime Change For Bond Yields & The Currency? - January 20, 2021 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

The data out of New Zealand have been neutral. Trade Balance in March improved by NZD 33M over a month ago and NZD 1690M a year ago. ANZ business confidence came in at -2 in April, higher than the -4.1 the prior month. The New Zealand dollar strengthened by 1% against the US dollar this week. We discuss the kiwi at length in the front section of this week’s report. The conclusion is that NZD faces near-term upside, but will lag other procyclical currencies over the longer term. Report Links: Portfolio And Model Review - February 5, 2021 Currencies And The Value-Versus-Growth Debate - July 10, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

The data out of Canada this week continue to be positive. Both Retail Sales and Core Retail Sales in February grew 4.8% over the prior month, comfortably exceeding the expectations of 3.7% and 4% growth, respectively. The Canadian dollar rose 0.8% against the US dollar this week. The loonie reacted positively to the strong retail numbers as it continues its path upward on strong inflation data of recent months and a hawkish Bank of Canada. However, even as the COVID case count appears to have peaked, there remains downside risks of very elevated commodity prices and our intermediate-term indicator still just off a recent peak. Report Links: Relative Growth, The Euro, And The Loonie - April 16, 2021 Will The Canadian Recovery Lead Or Lag The Global Cycle? - February 12, 2021 Currencies And The Value-Versus-Growth Debate - July 10, 2020 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

There was scant data out of Switzerland this week. ZEW expectations for April came in at 68.3, slightly higher than the 66.7 from the prior month. The Swiss franc rose 0.4% against the US dollar this week. While the waning of investors’ sentiment and net speculative positioning may point to some softening in the near term, the recent COVID crisis in India can provide support to this risk-off currency. We are long EUR/CHF. Report Links: Portfolio And Model Review - February 5, 2021 The Dollar Conundrum And Protection - November 6, 2020 On The DXY Breakout, Euro, And Swiss Franc - February 21, 2020 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

The data out of Norway this week was positive. Core Retail Sales came in unchanged in March versus the prior month, but beat expectations of a 0.9% decline. The Norwegian krone was 0.8% higher against the USD this week. Norway fits the bill in terms of a post-pandemic boom. New COVID-19 cases are under control, the economy is rebounding, oil prices are strong and the central bank is on a path the raise interest rates this year. Being long the NOK is one of our strongest convictions calls in FX. We are long NOK/USD and NOK/EUR. Report Links: Portfolio And Model Review - February 5, 2021 Revisiting Our High-Conviction Trades - September 11, 2020 A New Paradigm For Petrocurrencies - April 10, 2020 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Data out of Sweden this week have been mixed. The Riksbank maintained the policy rate at 0%. Trade Balance in March came in at SEK4.1B versus SEK6B in the prior month. Retail sales in March grew by 2.6% month-on-month and 9.1% year-on-year, both an improvement versus the prior period. The unemployment rate in March rose to 10% versus 9.7% the prior month. The Swedish Krona strengthened 0.5% against the US dollar this week, continuing its upward momentum throughout April. The recent accommodative signals from the Riksbank meeting were within expectations amidst elevated COVID case counts and restrictions. Despite its commendable gains so far this month, we remain optimistic on this high beta currency as the eurozone recovery and global reflation are in sight. Report Links: Revisiting Our High-Conviction Trades - September 11, 2020 Updating Our Balance Of Payments Monitor - November 29, 2019 Where To Next For The US Dollar? - June 7, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Limit Orders Closed Trades

Highlights Biden’s first 100 days are characterized by a liberal spend-and-tax agenda unseen since the 1960s. It is not a “bait and switch,” however. Voters do not care about deficits and debt. At least not for now. The apparent outcome of the populist surge in the US and UK in 2016 is blowout fiscal spending. Yet the US and UK also invented and distributed vaccines faster than others. US growth and equities have outperformed while the US dollar experienced a countertrend bounce. While growth will rotate to other regions, China’s stimulus is on the wane. Of Biden’s three initial geopolitical risks, two are showing signs of subsiding: Russia and Iran. US-China tensions persist, however, and Biden has been hawkish so far. Our new Australia Geopolitical Risk Indicator confirms our other indicators in signaling that China risk, writ large, remains elevated. Cyclically we are optimistic about the Aussie and Australian stocks. Mexico’s midterm elections are likely to curb the ruling party’s majority but only marginally. The macro and geopolitical backdrop is favorable for Mexico. Feature US President Joe Biden gave his first address to the US Congress on April 28. Biden’s first hundred days are significant for his extravagant spending proposals, which will rank alongside those of Lyndon B. Johnson’s Great Society, if not Franklin Delano Roosevelt’s New Deal, in their impact on US history, for better and worse. Chart 1Biden's First 100 Days - The Market's Appraisal

Biden's First 100 Days - The Market's Appraisal

Biden's First 100 Days - The Market's Appraisal

The global financial market appraisal is that Biden’s proposals will turn out for the better. The market has responded to the US’s stimulus overshoot, successful vaccine rollout, and growth outperformance – notably in the pandemic-struck service sector – by bidding up US equities and the dollar (Chart 1). From a macro perspective we share the BCA House View in leaning against both of these trends, preferring international equities and commodity currencies. However, our geopolitical method has made it difficult for us to bet directly against the dollar and US equities. Geopolitics is about not only wars and trade but also the interaction of different countries’ domestic politics. America’s populist spending blowout is occurring alongside a sharp drop in China’s combined credit-and-fiscal impulse, which will eventually weigh on the global economy. This is true even though the rest of the world is beginning to catch up in vaccinations and economic normalization. As for traditional geopolitical risk – wars and alliances – Biden has not yet leaped over the three initial foreign policy hurdles that we have highlighted: China, Russia, and Iran. In this report we will update the view on all three, as there is tentative improvement on the Russian and Iranian fronts. In addition, we will introduce our newest geopolitical risk indicator – for Australia – and update our view on Mexico ahead of its June 6 midterm elections. Biden’s Fiscal Blowout From a macro point of view, Biden’s $1.9 trillion American Rescue Plan Act (ARPA) was much larger than what Republicans would have passed if President Trump had won a second term. His proposed $2.3 trillion American Jobs Plan (AJP) is also larger, though both candidates were likely to pass an infrastructure package. The difference lies in the parts of these packages that relate to social spending and other programs, beyond COVID relief and roads and bridges. The Republican proposal for COVID relief was $618 billion while the Republicans’ current proposal on infrastructure is $568 billion – marking a $3 trillion difference from Biden. In reality Republicans would have proposed larger spending if Trump had remained president – but not enough to close this gap. And Biden is also proposing a $1.8 trillion American Families Plan (AFP). Biden’s praise for handling the vaccinations must be qualified by the Trump administration’s successful preparations, which have been unfairly denigrated. Similarly, Biden’s blame for the migrant surge at the southern border must be qualified by the fact that the surge began last year.1 A comparison with the UK will put Biden’s administration into perspective. The only country comparable to the US in terms of the size of fiscal stimulus over 2019-21 so far – excluding Biden’s AJP and AFP, which are not yet law – is the United Kingdom. Thus the consequence of the flare-up of populism in the Anglo-Saxon world since 2016 is a budget deficit blowout as these countries strive to suppress domestic socio-political conflict by means of government largesse, particularly in industrial and social programs. However, populist dysfunction was also overrated. Both the US and UK retain their advantages in terms of innovation and dynamism, as revealed by the vaccine and its rollout (Chart 2). Chart 2Dysfunctional Anglo-Saxon Populism?

Dysfunctional Anglo-Saxon Populism?

Dysfunctional Anglo-Saxon Populism?

No sharp leftward turn occurred in the UK, where Prime Minister Boris Johnson and his Conservatives had the benefit of a pre-COVID election in December 2019, which they won. By contrast, in the US, President Trump and the Republicans contended an election after the pandemic and recession had virtually doomed them to failure. There a sharp leftward turn is taking place. Going forward the US will reclaim the top rank in terms of fiscal stimulus, as Biden is likely to get his infrastructure plan (AJP) passed. Our updated US budget deficit projections appear in Chart 3. Our sister US Political Strategy gives the AJP an 80% chance of passing in some form and the AFP only a 50% chance of passing, depending on how quickly the AJP is passed. This means the blue dashed line is more likely to occur than the red dashed line. The difference is slight despite the mind-boggling headline numbers of the plans because the spending is spread out over eight-to-ten years and tax hikes over 15 years will partially offset the expenditures. Much will depend on whether Congress is willing to pay for the new spending. In Chart 3 we assume that Biden will get half of the proposed corporate tax hikes in the AJP scenario (and half of the individual tax hikes in the AFP scenario). If spending is watered down, and/or tax hikes surprise to the upside, both of which are possible, then the deficit scenarios will obviously tighten, assuming the economic recovery continues robustly as expected. But in the current political environment it is safest to plan for the most expansive budget deficit scenarios, as populism is the overriding force. Chart 3Biden’s Blowout Spending

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s campaign plan was even more visionary, so it is not true that Biden pulled a “bait and switch” on voters. Rather, the median voter is comfortable with greater deficits and a larger government role in American life. Bottom Line: The implication of Biden’s spending blowout is reflationary for the global economy, cyclically negative for the US dollar, and positive for global equities. But on a tactical time frame the rotation to other equities and currencies will also depend on China’s fiscal-and-credit deceleration and whether geopolitical risk continues to fall. Russia: Some Improvement But Coast Not Yet Clear US-Russia tensions appeared to fizzle over the past week but the coast is not yet clear. We remain short Russian currency and risk assets as well as European emerging market equities. Tensions fell after President Putin’s State of the Nation address on April 21 in which he warned the West against crossing Russia’s “red lines.” Biden’s sanctions on Russia were underwhelming – he did not insist on halting the final stages of the Nord Stream II pipeline to Germany. Russia declared it would withdraw its roughly 100,000 troops from the Ukrainian border by May 1. Russian dissident Alexei Navalny ended his hunger strike. Putin attended Biden’s Earth Day summit and the two are working on a bilateral summit in June. Chart 4Russia's Domestic Instability Will Continue

Russia's Domestic Instability Will Continue

Russia's Domestic Instability Will Continue

De-escalation is not certain, however. First, some US officials have cast doubt on Russia’s withdrawal of troops and it is known that arms and equipment were left in place for a rapid mobilization and re-escalation if necessary. Second, Russian-backed Ukrainian separatists will be emboldened, which could increase fighting in Ukraine that could eventually provoke Russian intervention. Third, the US has until August or September to prevent Nord Stream from completion. Diplomacy between Russia and the US (and Russia and several eastern European states) has hit a low point on the withdrawal of ambassadors. Fourth, Russian domestic politics was always the chief reason to prepare for a worse geopolitical confrontation and it remains unsettled. Putin’s approval rating still lingers in the relatively low range of 65% and government approval at 49%. The economic recovery is weak and facing an increasingly negative fiscal thrust, along with Europe and China, Russia’s single-largest export destination (Chart 4). Putin’s handouts to households, in anticipation of the September Duma election, only amount to 0.2% of GDP. More measures will probably be announced but the lead-up to the election could still see an international adventure designed to distract the public from its socioeconomic woes. Russia’s geopolitical risk indicators ticked up as anticipated (Chart 5). They may subside if the military drawdown is confirmed and Biden and Putin lower the temperature. But we would not bet on it. Chart 5Russian Geopolitical Risk: Wait For 'All Clear' Signal

Russian Geopolitical Risk: Wait For 'All Clear' Signal

Russian Geopolitical Risk: Wait For 'All Clear' Signal

Bottom Line: It is possible that Biden has passed his first foreign policy test with Russia but it is too soon to sound the “all clear.” We remain short Russian ruble and short EM Europe until de-escalation is confirmed. The Russian (and German) elections in September will mark a time for reassessing this view. Iran: Diplomacy On Track (Hence Jitters Will Rise) While Russia may or may not truly de-escalate tensions in Ukraine, the spring and summer are sure to see an increase in focus on US-Iran nuclear negotiations. Geopolitical risks will remain high prior to the conclusion of a deal and will materialize in kinetic attacks of various kinds. This thesis is confirmed by the alleged Israeli sabotage of Iran’s Natanz nuclear facility this month. The US Navy also fired warning shots at Iranian vessels staging provocations. Sporadic attacks in other parts of the region also continue to flare, most recently with an Iranian tanker getting hit by a drone at a Syrian oil terminal.2 The US and Iran are making progress in the Vienna talks toward rejoining the 2015 nuclear deal from which the US withdrew in 2018. Iran pledged to enrich uranium up to 60% but also said this move was reversible – like all its tentative violations of the Joint Comprehensive Plan of Action (JCPA) so far (Table 1). Iran also offered a prisoner swap with the US. Saudi Arabia appears resigned to a resumption of the JCPA that it cannot prevent, with crown prince Mohammed bin Salman offering diplomatic overtures to both the US and Iran. Table 1Iran’s Nuclear Program And Compliance With JCPA 2015

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Still, the closer the US and Iran get to a deal the more its opponents will need to either take action or make preparations for the aftermath. The allegation that former US Secretary of State John Kerry’s shared Israeli military plans with Iranian Foreign Minister Javad Zarif is an example of the kind of political brouhaha that will occur as different elements try to support and oppose the normalization of US-Iran ties. More importantly Israel will underscore its red line against nuclear weaponization. Previously Iran was set to reach “breakout” capability of uranium enrichment – a point at which it has enough fissile material to produce a nuclear device – as early as May. Due to sabotage at the Natanz facility the breakout period may have been pushed back to July.3 This compounds the significance of this summer as a deadline for negotiating a reduction in tensions. While the US may be prepared to fudge on Iran’s breakout capabilities, Israel will not, which means a market-relevant showdown should occur this summer before Israel backs down for fear of alienating the United States. Tit-for-tat attacks in May and June could cause negative surprises for oil supply. Then there will be a mad dash by the negotiators to agree to deal before the de facto August deadline, when Iran inaugurates a new president and it becomes much harder to resolve outstanding issues. Chart 6Iran Deal Priced Into Oil Markets?

Iran Deal Priced Into Oil Markets?

Iran Deal Priced Into Oil Markets?

Hence our argument that geopolitics adds upside risk to oil prices in the first half of the year but downside risk in the second half. The market’s expectations seem already to account for this, based on the forward curve for Brent crude oil. The marginal impact of a reconstituted Iran nuclear deal on oil prices is slightly negative over the long run since a deal is more likely to be concluded than not and will open up Iran’s economy and oil exports to the world. However, our Commodity & Energy Strategy expects the Brent price to exceed expectations in the coming years, judging by supply and demand balances and global macro fundamentals (Chart 6). If an Iran deal becomes a fait accompli in July and August the Saudis could abandon their commitment to OPEC 2.0’s production discipline. The Russians and Saudis are not eager to return to a market share war after what happened in March 2020 but we cannot rule it out in the face of Iranian production. Thus we expect oil to be volatile. Oil producers also face the threat of green energy and US shale production which gives them more than one reason to keep up production and prevent prices from getting too lofty. Throughout the post-2015 geopolitical saga between the US and Iran, major incidents have caused an increase in the oil-to-gold ratio. The risk of oil supply disruption affected the price more than the flight to gold due to geopolitical or war risk. The trend generally corresponds with that of the copper-to-gold ratio, though copper-to-gold rose higher when growth boomed and oil outperformed when US-Iran tensions spiked in 2019. Today the copper-to-gold ratio is vastly outperforming the oil-to-gold on the back of the global recovery (Chart 7). This makes sense from the point of view of the likelihood of a US-Iran deal this year. But tensions prior to a deal will push up oil-to-gold in the near term. Chart 7Biden Passes Iran Test? Likely But Not A Done Deal

Biden Passes Iran Test? Likely But Not A Done Deal

Biden Passes Iran Test? Likely But Not A Done Deal

Bottom Line: The US-Iran diplomacy is on track. This means geopolitical risk will escalate in May and June before a short-term or interim deal is agreed in July or August. Geopolitical risk stemming from US-Iran relations will subside thereafter, unless the deadline is missed. The forward curve has largely priced in the oil price downside except for the risk that OPEC 2.0 becomes dysfunctional again. We expect upside price surprises in the near term. Biden, China, And Our Australia GeoRisk Indicator Ostensibly the US and Russia are avoiding a war over Ukraine and the US and Iran are negotiating a return to the 2015 nuclear deal. Only US-China relations utterly lack clarity, with military maneuvering in the Taiwan Strait and South China Sea and tensions simmering over the gamut of other disputes. Chart 8Biden Still Faces China Test

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

Biden’s First 100 Days In Foreign Policy (GeoRisk Update)

The latest data on global military spending show not only that the US and China continue to build up their militaries but also that all of the regional allies – including Japan! – are bulking up defense spending (Chart 8). This is a substantial confirmation of the secular growth of geopolitical risk, specifically in reaction to China’s rise and US-China competition. The first round of US-China talks under Biden went awry but since then a basis has been laid for cooperation on climate change, with President Xi Jinping attending Biden’s virtual climate change summit (albeit with no bilateral summit between the two). If John Kerry is removed as climate czar over his Iranian controversy it will not have an impact other than to undermine American negotiators’ reliability. The deeper point is that climate is a narrow basis for US-China cooperation and it cannot remotely salvage the relationship if a broader strategic de-escalation is not agreed. Carbon emissions are more likely to become a cudgel with which the US and West pressure China to reform its economy faster. The Department of Defense is not slated to finish its comprehensive review of China policy until June but most US government departments are undertaking their own reviews and some of the conclusions will trickle out in May, whether through Washington’s actions or leaks to the press. Beijing could also take actions that upend the Biden administration’s assessment, such as with the Microsoft hack exposed earlier this year. The Biden administration will soon reveal more about how it intends to handle export controls and sanctions on China. For example, by May 19 the administration is slated to release a licensing process for companies concerned about US export controls on tech trade with China due to the Commerce Department’s interim rule on info tech supply chains. The Biden administration looks to be generally hawkish on China, a view that is now consensus. Any loosening of punitive measures would be a positive surprise for Chinese stocks and financial markets in general. There are other indications that China’s relationship with the West is not about to improve substantially – namely Australia. Australia has become a bellwether of China’s relations with the world. While the US’s defense commitments might be questionable with regard to some of China’s neighbors – namely Taiwan (Province of China) but also possibly South Korea and the Philippines – there can be little doubt that Australia, like Japan, is the US’s red line in the Pacific. Australian politics have been roiled over the past several years by the revelation of Chinese influence operations, state- or military-linked investments in Australia, and propaganda campaigns. A trade war erupted last year when Australia called for an investigation into the origins of COVID-19 and China’s handling of it. Most recently, Victoria state severed ties with China’s Belt and Road Initiative. Despite the rise in Sino-Australian tensions, the economic relationship remains intact. China’s stimulus overweighed the impact of its punitive trade measures against Australia, both by bidding up commodity prices and keeping the bulk of Australia’s exports flowing (Chart 9). As much as China might wish to decouple from Australia, it cannot do so as long as it needs to maintain minimum growth rates for the sake of social stability and these growth rates require resources that Australia provides. For example, global iron ore production excluding Australia only makes up 80% of China’s total iron ore imports, which necessitates an ongoing dependency here (Chart 10). Brazil cannot make up the difference. Chart 9China-Australia Trade Amid Tensions

China-Australia Trade Amid Tensions

China-Australia Trade Amid Tensions

Chart 10China Cannot Replace Australia

China Cannot Replace Australia

China Cannot Replace Australia

This resource dependency does not necessarily reduce geopolitical tension, however, because it increases China’s supply insecurity and vulnerability to the US alliance. The US under Biden explicitly aims to restore its alliances and confront autocratic regimes. This puts Australia at the front lines of an open-ended global conflict. Chart 11Introducing: Australia GeoRisk Indicator (Smoothed)

Introducing: Australia GeoRisk Indicator (Smoothed)

Introducing: Australia GeoRisk Indicator (Smoothed)

Our newly devised Australia GeoRisk Indicator illustrates the point well, as it has continued surging since the trade war with China first broke out last year (Chart 11). This indicator is based on the Australian dollar and its deviation from underlying macro variables that should determine its course. These variables are described in Appendix 1. If the Aussie weakens relative to these variables, then an Australian-specific risk premium is apparent. We ascribe that premium to politics and geopolitics writ large. A close examination of the risk indicator’s performance shows that it tracks well with Australia’s recent political history (Chart 12). Previous peaks in risk occurred when President Trump rose to power and Australia, like Canada, found itself beset by negative pressures from both the US and China. In particular, Trump threatened tariffs and the Australian government banned China’s Huawei from its 5G network. Today the rise in geopolitical risk stems almost exclusively from China. There is potential for it to roll over if Biden negotiates a reduction in tensions but that is a risk to our view (an upside risk for Australian and global equities). Chart 12Australian GeoRisk Indicator (Unsmoothed)

Australian GeoRisk Indicator (Unsmoothed)

Australian GeoRisk Indicator (Unsmoothed)

What does this indicator portend for tradable Australian assets? As one would expect, Australian geopolitical risk moves inversely to the country’s equities, currency, and relative equity performance (Chart 13). Australian equities have risen on the back of global growth and the commodity boom despite the rise in geopolitical risk. But any further spike in risk could jeopardize this uptrend. Chart 13Australia Geopolitical Risk And Tradable Assets

Australia Geopolitical Risk And Tradable Assets

Australia Geopolitical Risk And Tradable Assets