Economic Growth

Much like how core measures of inflation strip out volatile food and energy prices to give a better sense of the underlying trend, we can also look at Real Final Sales To Domestic Purchasers (FSDP) to get a better sense of the underlying trend in economic…

Feature What Could Sour The Sweet Spot? This continues to look like a very benevolent environment for risk assets. Growth in the U.S. remains decent, with Q1 GDP growth beating expectations at 3.2% QoQ annualized (albeit somewhat distorted by rising inventories). Leading indicators point to U.S. GDP growth of around 2.5% for 2019. The rest of the world is showing the first “green shoots” of economic recovery. China continues to expand credit, and the effects of this are starting to stabilize growth in Europe, Japan, and the Emerging Markets (Chart 1). Recommended Allocation

Monthly Portfolio Update

Monthly Portfolio Update

Chart 1China Reflation Helping Growth To Bottom

China Reflation Helping Growth To Bottom

China Reflation Helping Growth To Bottom

At the same time, central banks everywhere have turned accommodative. Following the Fed’s dovish shift late last year, the market has priced in rate cuts by end-2019. The ECB is about to relaunch its TLTRO funding program, and is expected to keep rates in negative territory for at least another year (Chart 2) – though there are worries whether Mario Draghi’s successor as ECB president might be more hawkish. The Bank of Canada and Bank of Japan, among others, have recently reemphasized monetary caution. Chart 2No Rate Hikes Anywhere

No Rate Hikes Anywhere

No Rate Hikes Anywhere

Chart 3Term Premium Keeping Down Yields

Term Premium Keeping Down Yields

Term Premium Keeping Down Yields

This goes some way to explain the biggest puzzle in markets currently: why, despite global equities being less than 1% below a record high, long-term interest rates remain so low, with the 10-year U.S. Treasury yield at 2.5%, and yields in Germany and Japan hovering around zero. There are other explanations too. A decomposition of the U.S. 10-year yield shows that most of the downward pressure has come from a sharp drop in the term premium (Chart 3). This is partly because lousy growth in other developed economies, such as Germany and Japan, has pushed down yields in these countries and, given that spreads to the U.S. were at record highs, depressed U.S. rates too. It also reflects a lingering pessimism among investors who bought Treasuries at the end of last year to hedge against recession and who remain concerned about the economy. This is evidenced by continuing strong flows into bond funds in 2019 (Chart 4). A decomposition of the U.S. 10-year yield shows that most of the downward pressure has come from a sharp drop in the term premium. Chart 4Investors Buying Bonds, Not Equities

Investors Buying Bonds, Not Equities

Investors Buying Bonds, Not Equities

Chart 5Why Has Inflation Fallen?

Why Has Inflation Fallen?

Why Has Inflation Fallen?

A further explanation is the recent softness in inflation, with the Fed’s focus measure, core PCE inflation, slowing to an annual rate of only 0.7% over the past three months (Chart 5). This is probably mostly due to the economic slowdown late last year. But it may also have structural causes: the recent improvement in labor productivity can perhaps allow wages to rise without feeding through into consumer price inflation (Chart 6). Chart 6Maybe Because Of Better Productivity

Maybe Because Of Better Productivity

Maybe Because Of Better Productivity

Chart 7Indicators Suggest Inflation Will Still Trend Up

Indicators Suggest Inflation Will Still Trend Up

Indicators Suggest Inflation Will Still Trend Up

How is this all likely to pan out? We think it improbable that inflation will stay low for long if growth is as robust as we expect. Leading indicators of inflation continue to suggest prices will trend higher (Chart 7). The Fed may not rush to raise rates (not least since, with the lower inflation recently, the Fed Funds Rate in real terms is now at neutral according to the Laubach-Williams model, Chart 8). But we also find it inconceivable that the Fed will cut rates, if growth remains strong, stocks continue to rise, and global risks recede. By the end of this year, it should be able to make a renewed case for a further hike. But even if it doesn’t do that – and permits either inflation to overheat for a while, or asset bubbles to form – these scenarios should be more conducive to equity outperformance, than bond outperformance. Global equities have already risen by 22% since last December’s low and may struggle to make rapid progress over the next few months. The key to further upside for stocks will be earnings: since analysts have cut EPS forecasts for S&P 500 companies for this year to only 4%, those expectations should not be hard to beat. In the Q1 earnings season, for instance, 79% of companies have so far come in ahead of the consensus EPS forecast. For global asset allocators, the key decision is always at the asset-class level. Will equities outperform bonds over the coming 12 months? Equities should have further upside if our macro scenario proves correct. On the other hand, we find it hard to imagine that global bond yields will not rise moderately if global growth recovers, the Fed refrains from cutting rates, inflation rises somewhat, and investors turn less wary of equities. We continue, therefore, to expect the stock-to-bond ratio (Chart 9) to rise further over the next 12 months. We think it improbable that inflation will stay low for long if growth is as robust as we expect. Chart 8Is Fed Now At Neutral?

Is Fed Now At Neutral?

Is Fed Now At Neutral?

Chart 9Stock-To-Bond Ratio Can Rise Further

Stock-To-Bond Ratio Can Rise Further

Stock-To-Bond Ratio Can Rise Further

Chart 10Europe And EM Outperform Only Briefly

Europe And EM Outperform Only Briefly

Europe And EM Outperform Only Briefly

Equities: We remain overweight global equities, but are reluctant to take higher beta country exposure until there is greater clarity on the bottoming out of ex-U.S. growth. Moreover, the structural headwinds that have prevented anything more than short-term outperformance for eurozone stocks (banking sector weakness) and Emerging Markets (excess debt and poor productivity) since 2010 remain powerful negative factors (Chart 10). Our moderately pro-cyclical sector recommendations (overweight energy and industrials) should hedge us against upside risk emanating from a strong rebound in Chinese imports. Fixed Income: Over the past few years, periods where equities have decoupled from bond yields have been resolved with bond yields playing catch-up (Chart 11). We expect the same to happen over the next few months, with global government bond yields rising moderately. The risk-on environment continues to be positive for credit. We prefer credit to government bonds within fixed income, but are only neutral within our overall recommended portfolio. U.S. high-yield bonds in particular look attractively valued, as long as growth continues and default rates don’t start to rise too much (Chart 12). Chart 11When Bonds And Equities Diverge…

When Bonds And Equities Diverge...

When Bonds And Equities Diverge...

Chart 12Junk Bonds Attractively Valued

Junk Bonds Attractively Valued

Junk Bonds Attractively Valued

Currencies: A pick-up in global growth would be negative for the U.S. dollar, typically a counter-cyclical currency (Chart 13). BCA’s currency strategists have slowly been moving towards a more positive stance on some currencies versus the dollar, particularly the euro and Australian dollar. We would expect to see the trade-weighted dollar start to depreciate in H2 once global growth accelerates, fueled by the very skewed long-dollar positioning currently. However, this may be only a six- to 12-month move, since growth and interest-rate differentials suggest that the structural dollar bull market that began in 2012 has not yet fully run its course. Commodities: Oil remains dominated by supply-side dynamics. How much the ending of waivers on Iranian oil sanctions, plus troubles in Venezuela and Libya, push up oil prices will depend on whether President Trump can persuade Saudi Arabia and UAE to increase production. BCA’s energy team expects he will be only partially successful in doing so, and see Brent reaching $80 a barrel and WTI $77 (from $72 and $64 currently) during 2019. Industrial commodities prices will depend on the strength and nature of China’s reflation: our commodities strategists see copper, the most sensitive metal to Chinese demand, as the best way to play this.1 Garry Evans Chief Global Asset Allocation Strategist garry@bcaresearch.com Chart 13Stronger Growth Would Be Dollar Negative

Stronger Growth Would Be Dollar Negative

Stronger Growth Would Be Dollar Negative

Footnotes 1 Please see Commodity & Energy Strategy Weekly Report, “Copper Will Benefit Most From Chinese Stimulus,” dated April 25, 2019, available at ces.bcaresearch.com GAA Asset Allocation

Highlights Fed: Fed policymakers are sending a unified message that they want to keep rates on hold until they see a significant increase in inflation. However, our reading of their recent remarks suggests that they will be reluctant to actually cut rates unless GDP growth falls to below its estimated potential. Economy: If we strip out the volatile net exports, government and inventory components of growth, we see that economic activity slowed to below potential in the first quarter. However, the timeliest data on consumer spending, nonresidential investment and residential investment all suggest that Q1 will be the trough for the year. All in all, economic growth should be comfortably above potential in 2019, keeping rate cuts at bay. Investment Strategy: Investors should keep portfolio duration low, avoiding the 5-year/7-year part of the Treasury curve. Investors should also overweight spread product versus Treasuries, with a focus on Baa and junk rated corporate bonds. Feature Since January, Federal Reserve policymakers have sent a strikingly unified message: Policy should remain “patient” in an effort to re-anchor inflation expectations and demonstrate the symmetry of the Fed’s 2 percent inflation target. Take for example, two excerpts from recent speeches by Boston Fed President Eric Rosengren and Chicago Fed President Charles Evans. Rosengren:1 My own preference is for the Federal Reserve to adopt an inflation range that explicitly recognizes the challenge of the effective lower bound. We might be forced to accept below-2-percent inflation during recessions, but we would commit to achieving above-2-percent inflation in good times, so as to provide more policy space to counteract the next recession. Evans:2 I think the Fed must be willing to embrace inflation modestly above 2 percent 50 percent of the time. Indeed, I would communicate comfort with core inflation rates of 2-1/2 percent, as long as there is no obvious upward momentum and the path back toward 2 percent can be well managed. The consensus appears to be not only that higher inflation is necessary before the Fed lifts rates again, but also that the Fed should explicitly target an overshoot of its 2 percent target. With trailing 12-month core PCE inflation running at only 1.55% as of March, it will undoubtedly take some time before these inflation goals are met. We think the Fed’s commitment to keeping rates steady could waver if financial conditions ease sufficiently.3 But for now, with the market priced for 36 basis points of rate cuts over the next 12 months, the more pertinent question is: What will it take for the Fed to lower rates from current levels? Expecting A Rate Cut? Don’t Hold Your Breath Our Fed Monitor has an excellent track record calling turning points in monetary policy, and at present it is very close to zero, consistent with the Fed’s “on hold” stance (Chart 1). The Monitor is comprised of 44 indicators of economic growth, inflation and financial conditions. In other words, for the Monitor to recommend rate cuts going forward we will need to see some further deterioration in either economic growth, inflation or financial markets (Chart 2). This is roughly consistent with how Chicago Fed President Evans described his reaction function in his speech from two weeks ago: Chart 1"On Hold" Stance Justified

"On Hold" Stance Justified

"On Hold" Stance Justified

Chart 2Fed Monitor Components

Fed Monitor Components

Fed Monitor Components

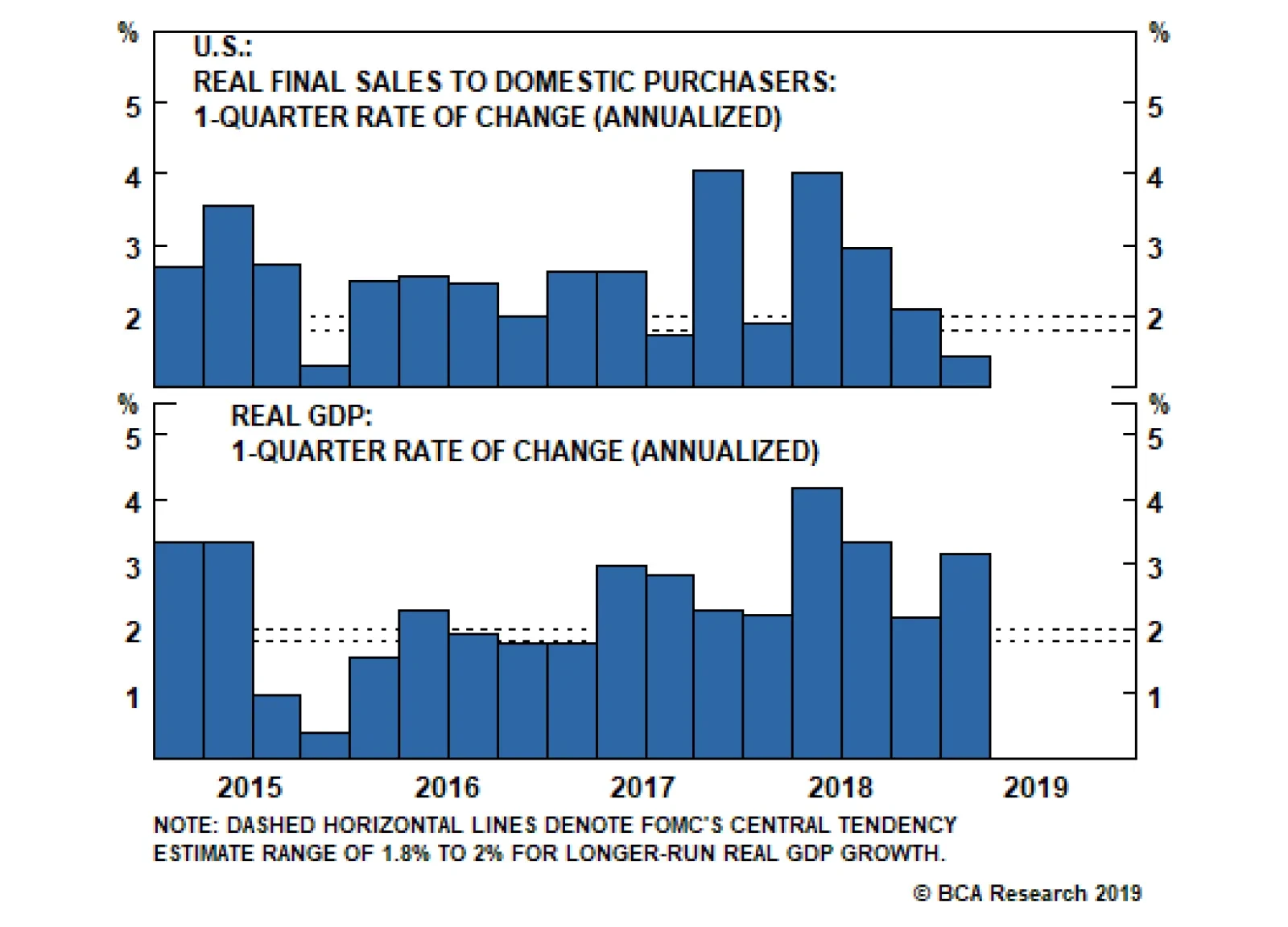

If growth runs close to or somewhat above its potential and inflation builds momentum, then some further rate increases may be appropriate over time… In contrast, if activity softens more than expected or if inflation and inflation expectations run too low, then policy may have to be left on hold – or perhaps even loosened – to provide the appropriate accommodation to obtain our objectives. Our interpretation of the Fed’s reaction function is that it wants to maintain an accommodative monetary policy to ensure that inflation and inflation expectations move higher over time. However, it will consider monetary policy to be accommodative as long as GDP growth stays close to, or above, estimates of its potential rate. In other words, while the Fed is in no rush to tighten, we probably need to see a significant period of below-potential GDP growth before rate cuts are on the table. In his speech, Evans indicates that his personal estimate of potential GDP growth is 1.75%. The March Summary of Economic Projections shows that the central tendency of FOMC participant estimates is 1.8% - 2%. Our view is that U.S. growth will easily surpass this threshold in 2019, keeping rate cuts at bay. Tracking U.S. Growth Markets were caught off guard last week when we learned that real GDP grew 3.17% in the first quarter, above consensus estimates and well above the 1.8% - 2% potential growth threshold. However, the headline Q1 figure was flattered by significant gains in a few volatile GDP components. Chart 3Underlying Growth Slowdown

Underlying Growth Slowdown

Underlying Growth Slowdown

Much like how core measures of inflation strip out volatile food and energy prices to give us a better sense of the underlying trend, we can also look at Real Final Sales To Domestic Purchasers (FSDP) to get a better sense of the underlying trend in economic growth. FSDP includes only consumer spending, nonresidential investment and residential investment. That is, it removes government spending, net exports and inventory investment from the overall number. Viewed this way, we see that the U.S. economy did experience a significant growth slowdown in the first quarter. Real FSDP grew only 1.45% in Q1, below the 1.8% - 2% potential growth threshold (Chart 3). Net Exports & Inventories Chart 4Net Exports & Inventories

Net Exports & Inventories

Net Exports & Inventories

First quarter GDP was boosted by a +1.03% contribution from net exports and a +0.65% contribution from inventory investment, neither of which is likely to be repeated in Q2 (Chart 4). The top panel of Chart 4 shows just how unusual it is to see such a large contribution from net exports, an event that becomes even less likely when you factor in the dollar’s recent appreciation (Chart 4, panel 2). Turning to inventories, a significant build was long overdue given the backlog of orders seen during the past two years. But the ISM Manufacturing Index’s backlog of orders component has now fallen back to a neutral level (Chart 4, bottom panel). This suggests that firms are comfortable with their current inventory stockpiles, and that no aggressive inventory increases are likely during the next few quarters. Interestingly, while net exports and inventories will almost certainly pressure GDP growth lower in Q2, back toward the growth rate in FSDP, the latter has probably already troughed for the year. Recent data on consumer spending, nonresidential investment and residential investment all appear to have turned a corner. Consumer Spending Consumer spending added a meager +0.8% to GDP in Q1, but core retail sales growth has recovered sharply after having plunged near the end of last year (Chart 5). What’s more, with consumer sentiment close to one standard deviation above its historical mean – whether we look at expectations or current conditions surveys – consumers don’t seem inclined to retrench in the months ahead (Chart 6). Chart 5Consumer Spending

Consumer Spending

Consumer Spending

Chart 6Buoyant Consumer Sentiment

Buoyant Consumer Sentiment

Buoyant Consumer Sentiment

Nonresidential Investment Chart 7Nonresidential Investment

Nonresidential Investment

Nonresidential Investment

We expected business investment to weaken in Q1, and its +0.4% growth contribution is low compared to recent readings. The decline was anticipated due to last year’s significant deterioration in global growth. Slower global growth necessarily causes firms to downgrade their profit expectations. Faced with lower expected profits, companies are much more inclined to curtail investment. However, considering the outlook heading into mid-year, we have already noticed signs of improvement in leading global growth indicators.4 More recently, we have even seen that improvement translate into stronger U.S. investment data. Core durable goods new orders grew +17% (annualized) in March, dragging the year-over-year rate up to +5.3% (Chart 7). Further, our BCA Composite New Orders Indicator – a weighted combination of ISM New Orders and NFIB Capital Spending Plans – has bounced during the past few months, returning close to its historical mean (Chart 7, panel 3). An average of Capital Spending Intentions from regional Fed surveys also remains close to one standard deviation above its historical average (Chart 7, bottom panel). Residential Investment Residential investment (aka Housing) has exerted a meaningful drag on GDP growth in each of the past five quarters, and it lowered GDP by -0.1% in Q1 (Chart 8). However, much like with consumer spending and nonresidential investment, the timely economic data suggest a turnaround is in the offing. Much like with consumer spending and nonresidential investment, the timely economic data suggest a turnaround is in the offing. Optimism has returned to housing since mortgage rates fell earlier this year. New home sales and mortgage purchase applications have jumped, and single-family housing starts are the only important housing-related data that haven’t yet rebounded. We expect that rebound to occur soon, as do homebuilders whose confidence has risen during the past few months. Homebuilder optimism surveys remain close to one standard deviation above their historical averages (Chart 9). Chart 8Residential Investment

Residential Investment

Residential Investment

Chart 9Buoyant Homebuilder Confidence

Buoyant Homebuilder Confidence

Buoyant Homebuilder Confidence

Bottom Line: Fed policymakers are sending a unified message that they want to keep rates on hold until they see a significant increase in inflation. However, our reading of their recent remarks suggests that they will be reluctant to actually cut rates unless GDP growth falls to below its estimated potential. Potential GDP growth is estimated to be in the 1.8% to 2% range. If we strip out the volatile net exports, government and inventory components of growth, we see that economic activity slowed to below potential in the first quarter. However, the timeliest data on consumer spending, nonresidential investment and residential investment all suggest that Q1 will be the trough for the year. All in all, economic growth should be comfortably above potential in 2019, keeping rate cuts at bay. Investment Implications To translate the above views on the economy and the Fed’s reaction function into a portfolio strategy, we first return to our Golden Rule of Bond Investing.5The Golden Rule states that if the Fed delivers more (fewer) rate hikes than are currently discounted in the market over the next 12 months, then the Treasury index will earn negative (positive) excess returns versus cash during that investment horizon (Chart 10). At present, this means that investors should only expect positive excess returns from taking duration risk in the event that the Fed cuts rates by more than 36 basis points during the next 12 months. Given our view that rate cuts are unlikely, investors should maintain below-benchmark portfolio duration. Chart 10The Golden Rule's Track Record

The Golden Rule's Track Record

The Golden Rule's Track Record

If we further assume that market expectations will shift to price-in fewer rate cuts, or even possibly some rate hikes, then we would expect 5-year and 7-year yields to rise the most (Chart 11). Investors should avoid those maturities and focus their Treasury exposure on the short and long ends of the curve. These barbell over bullet trades have the advantage of being positive carry, so they will earn money even if rate hike expectations are unchanged.6 Chart 11Avoid The 5- And 7-Year Maturities

Avoid The 5- And 7-Year Maturities

Avoid The 5- And 7-Year Maturities

Chart 12Investment Grade Spread Targets

Investment Grade Spread Targets

Investment Grade Spread Targets

Finally, the combination of above-potential GDP growth and a patient Fed is positive for spread product. Investors should remain overweight spread product versus Treasuries in bond portfolios, focusing on Baa and junk rated corporate bonds. Spreads for those credit tiers remain wide compared to historical median levels for this phase of the cycle (Charts 12 &13).7 Chart 13High-Yield Spread Targets

High-Yield Spread Targets

High-Yield Spread Targets

Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Footnotes 1 https://www.bostonfed.org/news-and-events/speeches/2019/monetary-policymaking-in-todays-environment.aspx 2 https://www.chicagofed.org/publications/speeches/2019/risk-management-and-the-credibility-of-monetary-policy 3 Please see U.S. Bond Strategy Weekly Report, “The New Battleground For Monetary Policy”, dated March 26, 2019, available at usbs.bcaresearch.com 4 Please see U.S. Bond Strategy Weekly Report, “Bond Kitchen”, dated April 9, 2019, available at usbs.bcaresearch.com 5 Please see U.S. Bond Strategy Special Report, “The Golden Rule Of Bond Investing”, dated July 24, 2018, available at usbs.bcaresearch.com 6 Please see U.S. Bond Strategy Weekly Report, “Paid To Wait”, dated February 26, 2019, available at usbs.bcaresearch.com 7 For further details on how we calculate these spread targets please see U.S. Bond Strategy Weekly Report, “The Value In Corporate Bonds”, dated February 19, 2019, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Highlights Central bankers appear to be in a rush to boost inflation expectations before the next economic downturn. This in practice should be stimulative for the global economy. Historically, currencies of small, open economies are typically the first to benefit from rebounding global growth. Ditto for those whose output gaps have fully closed. However, there appears to be a shift in the behavior of certain currency pairs in the current cycle. For example, the U.S. dollar has tended to perform better in a low-volatility environment in recent years, a shift from the past. Correspondingly, its safe-haven status may have been marginally eroded. The U.S. decision not to extend waivers on Iranian oil exports beyond the May 2 deadline is bullish for petrocurrencies such as the RUB and NOK. The Bank of Canada kept rates on hold but will be hard pressed to meet its inflation mandate before the next downturn. This suggests standing aside on USD/CAD. Rising net short positioning on the yen and Swiss franc is making them attractive from a contrarian standpoint. Place a limit-buy on CHF/NZD at 1.45. Feature Chart I-1Volatility Is Due For A Bounce

Volatility Is Due For A Bounce

Volatility Is Due For A Bounce

The four most important financial variables that could give a near-complete snapshot of the world economy at any point in time are probably the level of the S&P 500, the U.S. 10-year Treasury yield, the trade-weighted dollar and a commodity bellwether, say, crude oil prices. Any permutation of these variables can identify what quadrant the world economy is operating in, with the two most important states being either boom or bust. Taking three of those variables today – the S&P 500 breaking to all-time highs, crude oil prices up 40% from their lows and U.S. 10-year Treasury yields off by almost 100 basis points from their October highs – it is hard to justify why the dollar has hardly budged, this week’s rally aside. Obviously, this is a very simplified view of an intricately complex world economy. But it highlights a point we have been making in recent bulletins: that extended periods of low currency volatility have been very unusual in the post-Bretton Woods world (Chart I-1). The typical narrative has been that as we enter a reflationary window, pro-cyclical currencies should outperform. The reason is simple enough: These economies are export-oriented and tied to the global cycle. So, a rising current account surplus as demand for their goods and services picks up provides underlying support for the currency. Should there be little slack in their domestic economies, this also raises the probability that the central bank tightens monetary policy to fend off future inflationary pressures. It does not hurt if these countries are also commodity producers, since rising terms of trade also provides an additional exchange-rate boost. The reality is that the world is not static, and some of these dynamics have been shifting. The evidence is in the counterfactual: At current levels, China’s credit injection should have lit a fire under pro-cyclical trades because they tend to work in real-time rather than with a lag. The foreign exchange market is one of the deepest and most liquid where new information tends to get digested and discounted instantaneously. As such, the lack of more pronounced strength in pro-cyclical currencies like the Australian, New Zealand and Canadian dollar exchange rates is genuine reason for concern and worth investigation. Why Is The Dollar Breaking Higher? Our Special Report1 on March 29th highlighted the fact that the dollar should be 5-10% higher simply based on measures of relative trends, and recent data corroborate this view. The growth differential between the U.S. and the rest of the world remains wide. Meanwhile, exports and industrial production from Southeast Asia continue to decelerate. Interbank rates in China are spiking higher, suggesting most of the monetary stimulus may have already been frontloaded. And on the earnings front, U.S. profit leadership also continues. It is unclear which of these catalysts was the actual trigger for dollar strength, since these have been in place for a while now, but confirmation from any and all of them was sufficient to reinvigorate the dollar bulls. That said, it is important to pay heed to shifting market forces, but it will be imprudent to change investment strategy on this week’s moves alone. Given these moves, a few observations are in order: Almost all currencies are already falling versus the U.S. dollar – a trend that has been in place for several months now (Chart I-2). This means most of the factors putting upward pressure on the dollar are well understood by the market. For example, global growth has been slowing for well over a year, based on the global PMI. Putting on fresh U.S. long positions is at risk of a washout from stale investors, just as it was back in 2015, a year after growth had peaked. Dollar technicals are also very unfavorable (Chart I-3). Speculators are holding near-record long positions, sentiment is stretched and our intermediate-term indicator is also flagging yellow. Over the past five years, confirmation from all three indicators has been followed by some period of U.S. dollar indigestion. This time should be no different. Chart I-2Is It Time To Initiate Fresh Dollar Longs?

Is It Time To Initiate Fresh Dollar Longs?

Is It Time To Initiate Fresh Dollar Longs?

Chart I-3Dollar Technicals Are Unfavourable

Dollar Technicals Are Unfavourable

Dollar Technicals Are Unfavourable

A breakout in the dollar along with rising equity markets suggests that the correlation is once again shifting. The dollar has tended to trade as a counter-cyclical currency for most of the time, with a negative correlation even to global equities (Chart I-4). Importantly, given current low levels of volatility and elevated equity market valuations, the dollar would have been a great insurance policy for any stock market correction. But with U.S. interest rates having risen significantly versus almost all G10 countries in recent years, the dollar has itself become the object of carry trades. This has also come with a good number of unhedged trades, as the rising exchange rate has lifted hedging costs (Table I-1). Chart I-4The Dollar Remains A 'Risk-Off' Currency

The Dollar Remains A 'Risk-Off' Currency

The Dollar Remains A 'Risk-Off' Currency

Chart I-

It will be difficult for the dollar to act as both a safe-haven and carry currency, because the forces that drive both move in opposite directions. For one, safe-haven assets tend to be lower-yielding but also during episodes of capital flight, investors choose to repatriate capital to pay down debt, with creditor nations having the upper hand. And given U.S. investors have already been repatriating close to $400 billion in assets over the past 12 months, it is unlikely this pace persists (Chart I-5). The bottom line is that investors who believe that the U.S. dollar has become a high-beta currency should be prepared to stampede out the door on any rise in volatility. Our bias remains that the U.S. dollar will ultimately weaken, given that the forces driving it higher are mostly behind us. Meanwhile, currencies such as the Japanese yen or even Swiss franc that have been used to fund carry trades are very ripe for short-covering flows. Putting everything together suggests at minimum building portfolio hedges. It will be difficult for the dollar to act as both a safe-haven and carry currency. One such hedge is going long CHF/NZD. This trade has a high negative carry, so we do not intend to hold it for longer than three months. But speculative positioning and relative economic trends also support this cross for the time being (Chart I-6). We are placing a limit-buy at 1.45. Chart I-5How Much More Will Repatriation Flows Help?

How Much More Will Repatriation Flows Help?

How Much More Will Repatriation Flows Help?

Chart I-6CHF/NZD Is An Attractive ##br##Hedge

CHF/NZD Is An Attractive Hedge

CHF/NZD Is An Attractive Hedge

A Shifting Landscape If the dollar eventually weakens, let’s consider the premise that the most export-dependent economies should benefit more from a rebound in global growth, and by extension, their currencies should appreciate the most. Within the G10 universe, this will be notably the European currencies led by the Swiss franc, the Swedish Krona, the euro and the pound (Chart I-7). However, from the trough in the global Purchasing Managers’ Index (PMI) in December 2008 until the peak in April 2010, it was the commodity currencies that outperformed. During that time frame, the Swiss franc actually fell. It is well known that Switzerland’s persistent trade surplus over the decades has been a key factor behind structural appreciation in the currency. However, at any point in time, other nuances such as whether the rebound is China or commodities driven, the starting point for valuations or even interest rate differentials take center stage in explaining currency moves. The lesson is that investors have to become nimble with currency investment strategy. The lesson is that investors have to become nimble with currency investment strategy. For pro-cyclical currencies, there have been dramatic shifts in the export share of GDP for various countries, according to World Bank data. Most euro area countries have massively expanded their export share of GDP as they have gained ground in value-added products and services. Meanwhile, the export share in Australian GDP has been stuck at 20% for many years, while that in Norway, New Zealand and Canada has seen a huge drop, even since 2009 (Chart I-8). At first blush, this suggests diminishing marginal returns to their currencies from global growth.

Chart I-7

Chart I-8A Shifting Export ##br##Landscape

A Shifting Export Landscape

A Shifting Export Landscape

Take the example of New Zealand, where commodities are over 75% of exports. Since the 2000s, the government has been actively trying to redistribute growth from net exports to domestic demand. This has been mainly via the skilled workers program. The result has been a collapse in the export share of GDP from 36% to about 26%. This means that the New Zealand dollar, which has typically been a higher-beta play on global growth, is giving way to other currencies such as the euro and the Swedish krone (Chart I-4). In addition to this, while global growth might eventually recover, part of the widespread deterioration since the global financial crisis may be structural. If the overarching theme over slowing global trade is a global economy that is trying to lift its precautionary savings and spend less, then the world may not see the high rates of trade growth registered in the 1990s anytime soon. This is because at a lower rate of potential GDP growth, trade elasticities also tend to fall.2 There are many reasons for this, including less willingness among creditor nations to finance current account deficits, the paradox of thrift or just outright saturation in the turnover of trade. All of this dampens marginal returns toward all pro-cyclical currency trades. Chart I-9Trade Volatility Has Fallen

Trade Volatility Has Fallen

Trade Volatility Has Fallen

The bottom line is that the overall magnitude and volatility of trade relative to GDP has fallen, at least until the recent China – U.S. trade spat (Chart I-9). This has had the effect of dampening the volatility of the corresponding mediums of trade exchanges. Part of this is clearly cyclical, but a part may be structural as well. If we embrace confirmation that the Chinese economy has bottomed, it will be important to monitor if this cycle plays out like those in the past. Notes On Petrocurrencies, And The BoC The U.S. has decided not to extend waivers on Iranian oil exports beyond the May 2 deadline. Supposedly, a coalition with both Saudi Arabia and the United Arab Emirates would ensure that oil markets remain adequately supplied, though Saudi Arabia has since signaled they are in no rush to raise production. Overall, this increases the bullish narrative for oil. First, the Iranian response to a shutoff in their exports could be unpredictable. The U.S. threat of driving Iranian oil exports to zero increases the geopolitical risk premium in prices, as full implementation pushes Iran to a wall, raising the odds of retaliation. Chart I-10Iran Is A Meaningful Oil Supplier

Iran Is A Meaningful Oil Supplier

Iran Is A Meaningful Oil Supplier

Second, oil production is being curtailed at a time when Venezuelan output is rapidly falling, conflict in Libya is reviving and OPEC spare capacity remains tight. This could nudge the oil market dangerously close to a negative supply shock (Chart I-10). Meanwhile, there is the non-negligible risk of unplanned outages which have been rising in 2019, which is another source of risk for oil supply Oil futures have responded positively to the news, with both Brent and WTI making fresh 2019 highs. However, while initially reacting favorably, petrocurrencies such as the Canadian dollar, Russian ruble and Norwegian krone are selling off amid dollar strength. We think Brent will continue to trade at a premium to WCS crude. This bodes well for currencies tied to North Sea production. Hold short CAD/NOK and long NOK/SEK positions, despite the selloff this week. As for Canada, we are neutral on the loonie both short and medium term. The dovish shift by the BoC and looser fiscal policy are likely to be growth tailwinds. So is the rise in oil prices. However, there appears to be a genuine slowdown in the Canadian economy that is not yet fully reflected in economic forecasts. The key drivers for the CAD/USD exchange rate are interest rate differentials with the U.S. (which we think will compress further) and energy prices (which we think Canada benefits less from due to the discount Canadian oil sells for, and persistent infrastructure problems). As such, we think domestic conditions will continue to knock down whatever benefit comes from rising oil prices (Chart I-11). Chart I-11CAD/USD Will Benefit From##br## Rising Terms Of Trade

CAD/USD Will Benefit From Rising Terms Of Trade

CAD/USD Will Benefit From Rising Terms Of Trade

Chart I-12Can The BoC Hike Given ##br##This Backdrop? (1)

Can The BoC Hike Given This Backdrop? (1)

Can The BoC Hike Given This Backdrop? (1)

On the consumer side, real retail sales are deflating at the worst pace since the financial crisis, and demand for housing loans is falling off (Chart I-12). This is unlikely to improve if house prices continue to roll over (Chart I-13). A study by the Reserve Bank of New Zealand shows that on average, the elasticity of consumption growth to house price changes is asymmetric with negative housing shocks, hurting consumption by more than the boost received from positive shocks. This asymmetry may be due to the fact that at very elevated debt levels, leveraged gains are used to pay down debt aggressively, whereas leveraged losses hit bottom lines directly. There appears to be a genuine slowdown in the Canadian economy that is not yet fully reflected in economic forecasts. On the corporate side of the equation, the latest Canadian Business Outlook Survey is very telling. Firms’ expectations for sales have softened significantly, as businesses in several sectors are less optimistic about demand. This is driven by uncertainty in the oil patch, weak housing and weak external conditions. This in turn, has led to a steep drop in plans to increase capex (Chart I-14). For external investors, the large stock of debt in the Canadian private sector and overvaluation in the housing market are likely to continue leading to equity outflows on a rate-of-change basis. Chart I-13Can The BoC Hike Given This Backdrop? (2)

Can The BoC Hike Given This Backdrop? (2)

Can The BoC Hike Given This Backdrop? (2)

Chart I-14Can The BoC Hike Given This Backdrop? (3)

Can The BoC Hike Given This Backdrop? (3)

Can The BoC Hike Given This Backdrop? (3)

Technically, USD/CAD failed to break below the upward sloping trendline drawn from its 2017 lows. The next resistance zone is the 1.36-1.38 level. Our bias is that this zone will prove to be formidable resistance. We continue to recommend investors short the CAD, mainly via the euro. Housekeeping Our limit-buy on AUD/USD was triggered at 0.70. Place tight stops at 0.68 until further evidence that global growth has bottomed. Our short USD/SEK position garnered losses this week. The RiksBank’s dovish shift surprised the market, and triggered panic selling as important technical levels were broken. With a manufacturing PMI at 52.8, inflation at 1.8% and wages growing near 3%, this is not exactly the symptoms of an economy that needs more stimulus. We recommend holding onto positions, but will respect our stop loss a few hundred pips away. Finally, the dovish shift by the Bank of Japan does not change our thinking on the yen. The resilience in the currency might indicate the pool of yen bears has been exhausted. Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy Special Report, titled “Tug Of War With Gold As Umpire,” dated March 29, 2019, available at fes.bcaresearch.com. 2 Cristina Constantinescu, Aaditya Mattoo, and Michele Ruta, “The Global Trade Slowdown: Cyclical Or Structural?” IMF working paper (2015). Currencies U.S. Dollar Chart II-1

USD Technicals 1

USD Technicals 1

Chart II-2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. suggest a weaker housing market: In March, building permits contracted by 1.7% month-on-month, falling to 1.27 million; housing starts decreased by 0.3% month-on-month, coming in at 1.14 million. March new home sales grew by 4.5% month-on-month, coming in at 0.69 million. However, existing home sales contracted by 4.9% month-on-month, falling to 5.21 million. The house price index grew by 0.3% month-on-month in February, in line with expectations. MBA mortgage applications decreased by 7.3% in April. The Chicago Fed National Activity index fell to -0.15 in March, underperforming expectations. Durable goods orders increased by 2.7% in March, surprising to the upside. DXY index appreciated by 1% this week, hitting the highest level since June 2017. While a more accommodative monetary policy stance has been taken in China, global growth momentum remains weak, which is a cause for concern. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 Tug OF War, With Gold As Umpire - March 29, 2019 The Euro Chart II-3

EUR Technicals 1

EUR Technicals 1

Chart II-4

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area continue to soften: Italian business confidence and consumer confidence in March fell to 100.6 and 110.5, respectively. April preliminary consumer confidence in the euro area fell to -7.9, below expectations. German IFO business climate fell to 99.2 in April; expectations and current assessment fell to 95.2 and 103.3, respectively. French business confidence improved to 105, while business climate decreased to 101 in April. Italian trade balance came in at a larger surplus of 3.42 billion euro in April. EUR/USD depreciated by 1% this week. The incoming data from the euro area and globally have been weaker than expected. The recent ECB Economic Bulletin remains positive for the growth outlook going forward, stating that “the supportive financing conditions, favorable labor market dynamics and rising wage growth should continue to underpin the euro area expansion.” Report Links: Reading The Tea Leaves From China - April 12, 2019 Into A Transition Phase - March 8, 2019 A Contrarian Bet On The Euro - March 1, 2019 The Yen Chart II-5

JPY Technicals 1

JPY Technicals 1

Chart II-6

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been negative: Headline inflation and core inflation were unchanged at 0.5% and 0.4% year-on-year in March, respectively. Machine tool orders in March contracted by -28.5% year-on-year. All industry activity index fell by 0.2% month-on-month in February, in line with expectations. USD/JPY surged initially by 0.4% ahead of BoJ’s rate decision, then fell sharply, returning flat this week. The BoJ has decided to keep the interest rate on hold at -0.1%. The shift to a calendar-based form of forward guidance is unlikely to be a game-changer on its own. Moreover, the BoJ expects the Japanese economy to pick up through 2021 supported by highly accommodative financial conditions and government spending, despite the weakness of global growth and scheduled consumption tax hike. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Tug OF War, With Gold As Umpire - March 29, 2019 A Trader’s Guide To The Yen - March 15, 2019 British Pound Chart II-7

GBP Technicals 1

GBP Technicals 1

Chart II-8

GBP Technicals 2

GBP Technicals 2

Recent data in the U.K. have been positive: Public sector net borrowing increased to 0.84 billion pounds in March. In April, the CBI retailing reported sales increased to 13. The CBI business optimism came in at -16 in April, an improvement compared to the last reading of -23. GBP/USD fell by 1% this week, mostly affected by the U.S. dollar’s broad strength. The pound is likely to rebound once we see more signs confirming the strength in global growth, given Brexit has been kicked down the road. Report Links: Not Out Of The Woods Yet - April 5, 2019 A Trader’s Guide To The Yen - March 15, 2019 Balance Of Payments Across The G10 - February 15, 2019 Australian Dollar Chart II-9

AUD Technicals 1

AUD Technicals 1

Chart II-10

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been negative: Headline inflation fell to 1.3% year-on-year in Q1, missing expectations. Trimmed mean inflation in Q1 fell to 1.6% year-on-year. AUD/USD fell by 2.3% this week, which triggered our limit buy order at 0.7 on Wednesday. Inflation is a lagging indicator. While the Q1 inflation number missed expectations, the Australian dollar is likely to bottom as Chinese stimulus plays out and global growth starts to pick up. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Not Out Of The Woods Yet - April 5, 2019 Into A Transition Phase - March 8, 2019 New Zealand Dollar Chart II-11

NZD Technicals 1

NZD Technicals 1

Chart II-12

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand has been negative: Credit card spending contracted by 5.1% year-on-year in March, underperforming expectations. NZD/USD fell by 1.36% this week. We remain bearish on the New Zealand dollar due to the Achilles’ heel of an overvalued housing market. Moreover, the Kiwi is still expensive compared to its fair value. Report Links: Not Out Of The Woods Yet - April 5, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Canadian Dollar Chart II-13

CAD Technicals 1

CAD Technicals 1

Chart II-14

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been positive: Wholesale sales grew by 0.3% month-in-month in February, surprising to the upside. CFIB business barometer increased to 56.7 in April. USD/CAD surged by 0.95% this week. The Canadian dollar seems to be less responsive to the energy prices this week due to lots of concerns regarding the pipeline issue in Alberta. The Bank of Canada maintained its overnight interest rate target at 1.75% on Wednesday. In the April Monetary Policy Report, the BoC projects real GDP growth of 1.2% in 2019, and around 2% in 2020 and 2021. Given the current developments in household spending, energy investment, and trade conditions, a dovish stance by BoC is warranted. Report Links: A Shifting Landscape For Petrocurrencies - March 22, 2019 Into A Transition Phase - March 8, 2019 Balance Of Payments Across The G10 - February 15, 2019 Swiss Franc Chart II-15

CHF Technicals 1

CHF Technicals 1

Chart II-16

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been mostly positive: Money supply M3 grew by 3.5% year-on-year in March, same as last month. ZEW survey expectations increased to -7.7 from the previous reading of -26.9. USD/CHF increased by 0.66% this week. While global growth is set to rebound, the uncertainties regarding geopolitical risks, trade conditions, and oil prices will weigh on the growth pace. We remain neutral on the Swiss franc against U.S. dollar, but acknowledge that the large short positioning is attractive from a contrarian standpoint. Report Links: Beware Of Diminishing Marginal Returns - April 19, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Norwegian Krone Chart II-17

NOK Technicals 1

NOK Technicals 1

Chart II-18

NOK Technicals 2

NOK Technicals 2

There is no significant data from Norway this week. USD/NOK appreciated by 2.2% this week. We remain overweight the NOK based on our bullish outlook for oil. The Trump administration said they would not renew the waivers for Iranian oil exports, a move that roiled the energy market. The spike in oil prices will eventually benefit the Norwegian krone once global growth stabilizes. Report Links: A Shifting Landscape For Petrocurrencies - March 22, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Swedish Krona Chart II-19

SEK Technicals 1

SEK Technicals 1

Chart II-20

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden suggest a more positive sentiment: Consumer confidence increased to 95.8 in April, surprising to the upside. Economic tendency survey increased to 102.7 in April. Moreover, the manufacturing confidence also improved to 108.4 in April. USD/SEK appreciated by 2.64% this week. The Riksbank has kept its interest rate unchanged at -0.25% this week, as widely expected. The dovish shift of central banks worldwide is likely to help the global economy, which will benefit the Swedish krona. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Global Liquidity Trends Support The Dollar, But... - January 25, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

Highlights An aging population, a banking sector in poor health, and a private sector focused on building up savings are the key factors undermining euro area growth on a structural basis. A large manufacturing sector makes the euro area vulnerable to EM competition. Unlike the U.S., the region’s tech sector is held back by regulatory burdens, taxes and heavy dependence on bank funding. The euro area growth faces decades of low growth and inflation. Euro area rates will stay depressed, but paradoxically, the euro can still experience structural appreciation. Euro area equities are cheap for a good reason, and banks will continue to weigh on performance. Feature Over the past 10 years, the euro area has gone through a sovereign debt crisis, a double-dip recession, persistent below-target inflation, and most recently, yet another major growth slowdown. Moreover, this economic malaise materialized despite highly stimulative monetary policy, including negative interest rates. The ongoing economic weakness has raised the specter that the euro area is the new Japan. Nearly three decades after the bursting of the Nikkei bubble, the Land of the Rising Sun remains mired in low growth and mild but persistent deflation. Consequently, charts showing that European policy rates or bond yields are tracking Japanese developments with a 17-year lag (Chart II-1) have not only become commonplace, they elicit fears that European growth, interest rates and asset valuations will lag the rest of the world for decades to come. Chart II-1Europe Is Following The Japanese Example

Europe Is Following The Japanese Example

Europe Is Following The Japanese Example

In this piece, we discuss the various forces that explain why the euro area economy has been so weak this decade, and why such low interest rates have had so little impact on growth. We also study what sets the U.S. and euro area apart, and whether or not Europe will follow the trail blazed by Japan nearly 30 years ago. The Three Headwinds Three ills have kept European growth particularly depressed this cycle and are likely to remain significant headwinds into the foreseeable future: demographics, the banking sector’s poor health, and nonfinancial private sector balance sheet cleansing. 1) Demographics This is the most well understood and acknowledged problem impacting Europe today. Since 2008, the European population has grown by 2%, or only 0.2% a year, with the working age population having peaked around that year. Going forward, the picture will only deteriorate: The UN expects Europe’s population to contract by 12% over the next 27 years, and the working age population to fall by 15%. This also means that the dependency ratio – the number of individuals aged less than 15 and above 65 per 100 working-age people – will approximately double over the coming 40 years. This is a clear parallel with Japan. As Chart II-2 illustrates, Europe’s population, the number of working-age individuals and the dependency ratio are all tracking Japan with a 17-year lag. Like Japan, Europe’s trend growth will thus only deteriorate further. Not only will Europe not be able to add as many workers as the U.S. to its total, but it will need to build even fewer schools, malls, office buildings or units of housing. Consequently, both the supply and demand sides of the economy will lag due to this factor alone. 2) Banking Sector Health The poor health of the euro area banking sector is well known. BCA’s Global Asset Allocation service published an in-depth analysis of the European banking sector last December.4 The piece demonstrated that European banks have been much slower to recognize non-performing loans, curtail credit and rebuild capital than their U.S. counterparts. U.S. bank loans to the private sector fell by 13% in the two years during the crisis, while in Europe, these same loans have only fallen by 2% since 2008. Euro area banks generally remain burdened with significant non-performing loans as a percentage of regulatory capital. Moreover, net interest margins are also dismal, implying that the income cushion against bad loans is thin. Consequently, outside of France, Finland and Germany, European banks have either not grown their loan books to the private sector or, as is the case with Spain, Portugal, and Ireland, these books are continuously shrinking (Chart II-3). Chart II-2Same Demography In Europe Now Than In Japan Then

Same Demography In Europe Now Than In Japan Then

Same Demography In Europe Now Than In Japan Then

Chart II-3Peripheral Banks Continue To Curtail Credit

Peripheral Banks Continue To Curtail Credit

Peripheral Banks Continue To Curtail Credit

The poor health of the European banking system is now constraining the supply of new credit to the rest of the economy. This is a much bigger problem than is the case in the U.S. given that in Europe, 72% of corporate funding comes from the banking system while 88% of household liabilities are also funded this way. In the U.S., the share of bank funding for these sectors is 32% and 29%, respectively (Chart II-4). A weak euro area banking system prevents the nonfinancial private sector from growing as robustly as it could.

Chart II-4

3) Nonfinancial Private Sector Balance Sheet Cleanse Another major drag on European growth has been the continued efforts of the European private sector to rebuild its balance sheet. To use the terminology developed by our upcoming conference speaker Richard Koo, the euro area has been in the thralls of a powerful balance sheet recession. Households in the euro area, Japan and the U.S. are all accumulating more financial assets than liabilities. However, only in the U.S. is the nonfinancial corporate sector building more liabilities than it is accumulating assets (Chart II-5). In Japan and Europe, the nonfinancial corporate sector is also a source of savings for the economy. Moreover, in Europe, the government runs a much smaller financial deficit. The current account balance tells this story vividly. A country’s current account is equal to the private sector’s savings minus investment and minus government deficits. As Italy, Spain, and other peripheral economies increased their aggregate savings after 2008, their large current account deficits vanished. Meanwhile, the governments of countries like Germany or the Netherlands, which sported healthy public finances, did not increase their spending in a commensurate way. This adjustment transformed an overall euro area current account deficit of 1.5% in 2008 into a surplus of 3.0% of GDP today, sending some of Europe’s excess savings abroad. This mimics the post-1990 Japanese experience. In the U.S., where the private sector savings did not rise as durably as in Europe, the current account stopped improving meaningfully in 2010 (Chart II-6). Chart II-5European Businesses Are Savers, Like In Japan

European Businesses Are Savers, Like In Japan

European Businesses Are Savers, Like In Japan

Chart II-6The Current Account Dynamics Epitomise The Savings Dynamics

The Current Account Dynamics Epitomise The Savings Dynamics

The Current Account Dynamics Epitomise The Savings Dynamics

A private sector squarely focused on rebuilding its balance sheet liquidity can lead to a liquidity trap. In this state, monetary policy can become ineffective as spending does not respond to lower interest rates. This is where Europe is currently stuck, explaining why the European Central Bank is finding that inflation and growth are not experiencing much lift, despite seemingly incredibly accommodative monetary conditions. Why Such An Urge To Save? The fact that the household sector is a net saver is not surprising, as this is a normal state of affairs across most economies. But why is the European nonfinancial corporate sector still trying to improve its balance sheet liquidity by accumulating more assets than liabilities? Like Japanese businesses 30 years ago, European firms have large debt loads. Another problem is the lack of capex opportunities in Europe. Why do we make this assertion? The return on assets in Europe has been at rock-bottom levels ever since the introduction of the euro (Chart II-7). In the decade from 1998 to 2008, this was a non-issue. Strong global growth flattered European sales, and easy access to credit meant that via rising leverage euro area-listed nonfinancial corporations were able to generate returns on equity comparable to U.S. firms (Chart II-8, top panel). Once European banks got cold feet and European nonfinancial businesses began focusing on deleveraging, the low level of return on assets became more apparent. Part of the problem is that European profit margins are much closer to Japanese than U.S. levels (Chart II-8, middle panel). Even more damning, asset turnover – how much sales are generated by a unit of assets – has been structurally lower in Europe than in both Japan and the U.S. for multiple decades (Chart II-8, bottom panel). Chart II-7Europe Suffers From A Lower RoA

Europe Suffers From A Lower RoA

Europe Suffers From A Lower RoA

Chart II-8DuPont's Decomposition Shows Why The Euro Area RoA Is Poor

DuPont's Decomposition Shows Why The Euro Area RoA Is Poor

DuPont's Decomposition Shows Why The Euro Area RoA Is Poor

The first factor weighing on the level of asset utilization and returns in Europe is the elevated level of capital stock. As Chart II-9 illustrates, the capital stock as a share of output in Italy, Spain and France dwarfs that of Japan, China or the U.S. Even Germany’s capital stock, which stands well below that of other large euro area economies, is nearly 100 percentage points of GDP larger than the U.S’s. Europe has too large a pool of assets to make any additional investments profitable, especially in light of its poor demographic profile.

Chart II-9

The second factor weighing on European asset utilization and returns is the poorer level of labor productivity. From the 1950s to the early 1980s, European GDP per worker rose relative to the U.S., albeit peaking at 92% of the levels across the Atlantic. Due to falling working hours in Europe relative to the U.S. since the 1980s, relative output per hour continued to rise until the mid-1990s, peaking at 105% of the U.S. level. However, since their respective zeniths, both relative productivity measures have collapsed (Chart II-10, top panel). Chart II-10Another Symptom Of Europe's Misallocation Of Capital In The 2000s

Another Symptom Of Europe's Misallocation Of Capital In The 2000s

Another Symptom Of Europe's Misallocation Of Capital In The 2000s

These collapses are in fact worse than Japan’s performance since its lost decades began. As the second panel of the chart shows, since the early 1990s, Japan’s relative output per hour and per worker have flattened – not declined – at around 65% and 72%, respectively, of U.S. levels. Instead, relative European productivity levels are currently converging toward Japanese levels (Chart II-10, third and fourth panels). The particularly poor level of European asset utilization and productivity principally reflects the duality between the peripheral as well as French economies on one side, and Germany as well as the Netherlands on the other side. The exceptionally large capital stock outside of Germany is a legacy of the years directly after the euro’s introduction. Back then, the ECB kept rates low to help Germany, the then-sick man of Europe. These rates were too low for the rest of Europe, encouraging large capital stock build-ups. Moreover, this capital was misallocated, as demonstrated by the tepid growth of output per hour and output per capita in Europe post 2000. Since funds were poorly allocated, the output-to-capital ratio in the periphery collapsed. In other words, the peripheral capital-stock-to-GDP ratios continued rising because the denominator, GDP, lagged. An additional problem for Europe’s asset utilization has been its large manufacturing sector. Even after declining, 20% of Europe’s GDP still comes from the secondary sector versus less than 12% in the U.S. (Chart II-11). This has two consequences for Europe’s asset utilization relative to the U.S. First, a large manufacturing sector requires a much larger asset base than a large service or tech sector. Second, the manufacturing sector is more exposed to competition from emerging markets than the tech sector, or than the domestically-focused service sector. Chart II-11Europe Is Left Exposed To EM Competition

Europe Is Left Exposed To EM Competition

Europe Is Left Exposed To EM Competition

In other words, not only has the U.S. experienced less capital misallocation than a large swath of the European economy, it has also re-aligned its economy to make it more robust in the face of competition from emerging economies, while Europe mostly has not. Consequently, hurt by foreign competition and unable or unwilling to re-invent itself, Europe has been left with dwindling relative productivity levels and poor degrees of asset utilization and returns. Why Did The U.S. Economy Transition Better than Europe To A Globalized World? There are many reasons why the U.S. has maintained higher RoAs and has been more successful at transitioning away from a manufacturing-led economy than the euro area. First, the level of product and service market regulation in Europe is highly punitive. As Chart II-12 illustrates, like Japan, most euro area countries fare poorly in the World Bank’s Ease of Doing Business survey. In fact, Italy scores even lower than China! Meanwhile, the U.S. ranks near the top, not far from Singapore. This means that starting new businesses, competing, and so on is easier in the U.S. than in Europe, helping foster a greater level of entrepreneurialism. Consequently, established businesses have been able to maintain the status quo longer in Europe than in the U.S., preventing creative destruction from purging the system of bad assets.

Chart II-12

Second, most large euro area economies are burdened by heavy taxes. As Chart II-13 shows, while the U.S. public sector extracts taxes equal to 27.1% of GDP, German, Italian and French taxes equal 37.5%, 42.4% and 46.2% of GDP, respectively, well above the OECD average of 34.2%. Such high levels of taxation disincentivize risk-taking. Lower levels of risk taking by individuals further prevented the degree of creative destruction necessary for Europe to better use its capital stock.

Chart II-13

Third, and linked to the previous point, government spending equals 34.9% of GDP in the U.S., compared to 48.2% and 56.0% in Italy or France, respectively. A large government has historically stifled innovation and favored the status quo. By no means does this implies that the U.S. system is free of imbalances, but it highlights that compared to two of the three largest European economies, the U.S. public sector has had a less deleterious impact on growth conditions and entrepreneurialism. Moreover, Italy and France have been in deep need of structural reforms that have been lacking. On this front, while the outlook is improving in France under Macron’s presidency, Italy remains mired in immobilism. Europe has too large a pool of assets to make any additional investments profitable, especially in light of its poor demographic profile. Fourth, the financing structure in the U.S. favors investing in new businesses and industries, especially when compared to the euro area. Equities represent 78% of the capital structure of nonfinancial corporations in the U.S. while they represent only 61% in the euro area. Moreover, within debt-financing, capital markets account for 68% of sourced funds in the U.S. compared to 28% in the euro area. In fact, junk bond market capitalization only accounts for 2.2% of GDP in Europe compared to 6.0% in the U.S. This suggests that financing risky ventures – and entrepreneurialism is inherently risky – is tougher in Europe than in the U.S. In fact, as a share of GDP, the European venture capital business is less than a sixth the size of the U.S.’s (Chart II-14), a gap that has existed for more than 30 years. Chart II-14U.S. Financing Allows For Greater Risk Taking

U.S. Financing Allows For Greater Risk Taking

U.S. Financing Allows For Greater Risk Taking

With all these hurdles, it is unsurprising that Europe has taken more time to make its economy more dynamic in the globalized economy of the 21st century. It also explains why Europe might be suffering more from EM competition than the U.S. Interestingly, this last point may be changing as U.S. voters seem to want to move back toward a larger manufacturing sector. This transition is unlikely to happen without more protectionism. This is a topic for another report. Is Europe Doomed To Japanification… Or Worse? It is easy to see why Europe cannot hope to grow as fast as the U.S., and therefore why the ECB will not be able to lift rates as high as the Fed and why bund yields are likely to lag Treasurys for years to come. Europe has a much more dire demographic profile than the U.S. It needs to purge its capital stock and invigorate its economy through reforms, a smaller public sector, and more diversified financing channels. But can the euro area fare better than Japan has over the past 30 years? On three fronts, the euro area looks better than Japan. First, as Chart II-15 shows, the overall European nonfinancial private sector entered its crisis in 2008 with lower leverage than Japan’s in the early 1990s. Additionally, European stocks were much cheaper in 2007 than the Nikkei was in 1989 (Chart II-16, top panel). Even Spanish real estate was more reasonably valued in 2007 than Japanese real estate in the early 1990s (Chart II-16, bottom panel). This combination means that now that the acute part of the crisis is over, the hole in the European private sector’s balance sheet is much smaller than the one Japan needed to plug 30 years ago. Thus, from a balance-sheet perspective, the need to rebuild savings is lower in Europe than Japan, and we could expect the current period of elevated savings to be shorter in the euro area than it has been in Japan.

Chart II-15

Chart II-16...And European Assets Were Not As Expensive As Japanese Ones At The Onset Of The Crisis

...And European Assets Were Not As Expensive As Japanese Ones At The Onset Of The Crisis

...And European Assets Were Not As Expensive As Japanese Ones At The Onset Of The Crisis

Second, despite former ECB President Jean-Claude Trichet’s policy mistake of raising interest rates in 2011, the ECB was much quicker to implement extreme easing policy measures than the Bank of Japan was in its day. It took 10 years for the BoJ to cut rates to zero after the Nikkei peaked in December 1989. It took one year for the ECB to do so after stock prices peaked in 2007. It took nine years for the BoJ to expand its balance sheet aggressively, but it took less than two years for the ECB to do so. One of the key benefits of this greater European proactivity has been to keep European inflation expectations much higher than in Japan, curtailing real interest rates in the process. Third, Europe purged economic excesses much more quickly than Japan. The Japanese unemployment rate increased from 2% to 6% between 1990 and 2010. In peripheral Europe, where the worst pre-crisis excesses existed, unemployment rose from 7.5% in 2008 to 18% in 2013 (Chart II-17, top panel). Meanwhile, real wages never adjusted in Japan, but fell 27.0% at their worst in Spain and 32.5% in Greece (Chart II-17, bottom panel). Moreover, the Rajoy reforms in Spain and the Macron reforms in France show that outside of Italy, European governments have been reforming their economies faster than Japan did after the bubble burst in 1990. Chart II-17Bigger Labor Market Purge In Europe Than Japan

Bigger Labor Market Purge In Europe Than Japan

Bigger Labor Market Purge In Europe Than Japan

However, on three fronts Europe is faring worse than Japan. First, up until the last 10 years, Japan benefited from a robust global economy where trade grew strongly. Europe is entering its second decade of low growth in an environment where global economic activity is much weaker, as potential U.S. GDP growth has slowed and China is not growing at a double-digit pace anymore. Moreover, budding protectionism in the U.S. is creating another hurdle for European economic output. Second, the excess capital stock in the European periphery is in fact greater than was the case in Japan in 1990. This suggests that the periphery needs to curtail investments by a greater margin than Japan did. Consequently, peripheral growth will continue to exert downward pressure on aggregate European activity for an extended period. Third, the European fiscal response will not match Japan’s. Investors often decry Japan’s large government debt of 238.2% of GDP as a sign of profligacy. It is not. It is mainly a mirror image of the private sector’s savings surplus. The Japanese government’s ability to run large deficits has prevented a larger fall in output – one that would have equaled the annual savings of the private sector. Without the government’s dissaving, the Japanese private sector would have found its debt load even more onerous to service, and the need to curtail spending would have been even greater as economy-wide cash flows would have been even smaller. Europe does not have a unified fiscal authority that can run such large-scale deficits. Instead, each nation’s government has a limited capacity to accumulate debt as investors worry that overly-indebted governments may very well redenominate what they have borrowed in much weaker currencies than the euro. This risk is made even greater by the fact that there is no euro-area wide deposit insurance scheme. Since Italian and Spanish banks hold large amounts of BTPs and Bonos, respectively, a so-called doom-loop exists that links the health of banks in those countries to the health of their governments, further limiting the public sector’s ability to act as a spender of last resort. This makes the efforts of the private sector in Italy, France, and Spain to increase its savings and bring down its excess capital stock more difficult, and thus, likely to last longer. Even if 10 years after the crisis first emerged, Europe has done more to purge its economy from its pre-crisis excesses than Japan had after its first lost decade, a lack of unified fiscal lever in Europe nullifies this positive. Thus, so long as the European integration efforts remain on the backburner, euro area growth, inflation, and interest rates will continue to look more like Japan’s have over the past 30 years than the U.S. This is likely to cause a big problem once the next recession emerges. Europe will enter that slowdown without any ammunition to reflate growth. Therefore, the next recession is likely to prove very deflationary and test the recent improvement in support for the euro seen across all euro area nations (Chart II-18). If the euro area survives this crisis, and we suspect it will, the probability of a fiscal union will only grow.2 After all, it has been through various crises that Europe has moved closer together, and the rise of a multipolar geopolitical environment dominated by large countries makes this imperative ever more vital. Chart II-18Support For The Euro Is Resilient

Support For The Euro Is Resilient

Support For The Euro Is Resilient

Bottom Line: We expect European growth and inflation to continue to lag well behind the U.S. for years to come if not a full decade. Ultimately, bringing down the expensive capital stock in the European periphery will be a slow process, especially if governments remain tight fisted. Investment Implications First, core euro area interest rates are likely to remain well below U.S. levels. As long as the European private sector pares back investments in order to normalize its capital stock-to-GDP ratio - a phenomenon that will be most pronounced in the periphery and France - European growth and inflation will lag behind the U.S. This also means that as long as European governments remain shy spenders and do not compensate for the lack of spending from the private sector, in the euro area periphery, European banks will suffer from depressed net interest margins and be structural underperformers. Second, the euro is likely to experience a structural upward drift. The euro is trading at a 10.5% discount to its purchasing power parity. Moreover, high private sector savings not only weigh on inflation, they will also push Europe’s net international investment position higher via an accumulated current account surplus. Both these factors are long-term bullish for the euro. Moreover, the fact that the euro area will soon become a net creditor nation, along with a lack of room to stimulate growth via monetary easing in times of recessions, means that the euro could increasingly become a counter-cyclical currency like the yen. So long as the European integration efforts remain on the backburner, euro area growth, inflation, and interest rates will continue to look more like Japan’s have over the past 30 years than the U.S. Third, European equities are trading at a discount to U.S. equities, but we do not think this guarantees long-term outperformance. European equities are cheap because European growth prospects are poor. If Japan is any guide, European stocks may be set to continue underperforming. This is especially true as financials are over-represented in European equity benchmarks, and banks stand at the epicenter of the European economic malaise. Fourth, European stocks will remain slaves to the global business cycle. Since the crisis, European growth has become hypersensitive to global growth, making European equities very responsive to the global business cycle. The same phenomenon happened in post-1990 Japan. In other words, the beta of European stocks is likely to continue to rise. This phenomenon could be exacerbated if the euro indeed does become a counter-cyclical currency, in which case the euro and European equities would become negatively correlated, like the yen and the Nikkei. Finally, the period from 1999 to 2005 showed how ECB policy targeted at supporting Germany resulted in imbalances that boosted real estate and equity returns in the periphery – in Spain and Ireland in particular. Today, the periphery is the worst offender when it comes to poor bank health and private sector balance sheet rebuilding. This means that the ECB is likely to keep monetary conditions too accommodative for Germany, where balance sheets are more robust and where the capital stock is not as excessive. As a result, financial market plays linked to German real estate are likely to continue outperforming other European domestic plays. They therefore warrant an overweight within European portfolios. Mathieu Savary Vice President The Bank Credit Analyst Footnotes 1 Please see Global Asset Allocation Special Report "Euro Area Banks: Value Play Or Value Trap?" dated December 14, 2018, available at gaa.bcaresearch.com 2 The European Commission Eurobarometer Surveys show that Europeans overwhelmingly see Europe as a peace project and as a way to maintain a voice in a world dominated by huge players like the U.S., China, or Russia, a world where France, Germany, or Italy individually are marginal players. In 2016, the U.K. population did not share this opinion. Moreover, even after what amounts to a depression, the support for the euro continues to rise in Greece, showing the growing commitment of Europeans to the euro, and the resilience of this commitment to economic shocks.