Economic Growth

Highlights Await the U.K. parliament to coalesce a majority on a on a credible strategy for Brexit that is also acceptable to the EU27. At that point, buy the pound, the FTSE250, and U.K. homebuilder shares. An eerie calm has descended over developed economy currencies. But the Chinese yuan has rebounded sharply. Stay tactically overweight emerging market currencies, cyclical equity sectors, and equities versus bonds. But don’t expect these rallies to last beyond the summer. Feature Chart of the WeekAn Eerie Calm Has Descended Over The Currency Markets. Why?

An Eerie Calm Has Descended Over The Currency Markets. Why?

An Eerie Calm Has Descended Over The Currency Markets. Why?

End Of The Road For May From the moment almost three years ago that the U.K. voted to leave the EU, it was clear that a rational and measured Brexit would require the U.K. to remain in a customs union with the EU. Rational and measured because a customs union would protect the cross-border supply chains which are vital to so many U.K. businesses. Rational and measured because a customs union would avoid a hard customs border on the island of Ireland, and thereby prevent a break-up of the U.K. Rational and measured because a customs union would best deliver on the narrow 52:48 vote to leave the EU, which was driven by a desire to control migration and the supremacy of the European Court of Justice – both of which are compatible with remaining in a customs union – rather than a desire to strike independent trade deals – which is not. Yet Theresa May did not steer to this rational and measured Brexit, because she knew it would rip apart the Conservative party, a hard minority of which sees the sovereignty of trade policy as its Holy Grail. Beholden to this minority, May put her party interest above the national interest. But now, May has run out of road. Her Brexit deal has been rejected twice by huge parliamentary majorities. In the coming days, parliament, through a series of indicative votes, is likely to wrest control of the Brexit process from the government. So far, parliament has expressed what it is against (a no-deal Brexit), but it has yet to express what course of action it is for. We await the U.K. parliament to coalesce a majority on a credible strategy for Brexit that is also acceptable to the EU27. At that point, irrespective of the exact strategy, we will buy the pound, the FTSE250, and U.K. homebuilder shares. Important Message From The Currency Markets An unusually eerie calm has descended over the currency markets (Chart of the Week). For the past six months, GBP/USD has drifted within a tight 5 percent range, USD/JPY has also moved within a similarly narrow range, and EUR/USD has been trapped within an even tighter 3 percent range (Chart I-2 and Chart I-3). Chart I-2GBP/USD And EUR/USD Have Been Very Calm Recently

GBP/USD And EUR/USD Have Been Very Calm Recently

GBP/USD And EUR/USD Have Been Very Calm Recently

Chart I-3USD/JPY Has Also Been Very Calm Recently

USD/JPY Has Also Been Very Calm Recently

USD/JPY Has Also Been Very Calm Recently

The calm is eerie because Brexit tensions have actually intensified as the Article 50 clock has run down without a breakthrough; the Federal Reserve has made a dramatic volte-face from its sequential rate hikes; the ECB has pivoted back to dovish after the German economy narrowly avoided a technical recession; and the Japanese economy contracted sharply in the third quarter of 2018. Adding to the eeriness of the calm in currency markets, the equity and bond markets have experienced wild gyrations. Global equities plunged 20 percent before quickly recovering most of the losses, while long bond prices moved by close to 15 percent1 (Chart I-4 and Chart I-5).1 Chart I-4While Equities Have Been Turbulent, Currencies Have Been Calm

While Equities Have Been Turbulent, Currencies Have Been Calm

While Equities Have Been Turbulent, Currencies Have Been Calm

Chart I-5While Bonds Have Been Turbulent, Currencies Have Been Calm

While Bonds Have Been Turbulent, Currencies Have Been Calm

While Bonds Have Been Turbulent, Currencies Have Been Calm

Given all of this turbulence, why have currency markets remained a relative oasis of calm? The simple answer is that exchange rates are, by definition, relative prices. And in the major economies, growth and inflation rates have moved in the same direction by the same amount at roughly the same time. In fact, looking at quarter-on-quarter growth rates, the major economies have all recently experienced identical 1.5 percent slowdowns: from 4 to 2.5 percent in the U.S.; and from 2.5 percent to around 1 percent in both the euro area and the U.K.2 (Chart I-6 - Chart I-8). Chart I-6U.S. GDP Growth Slowed By 1.5 Percent

U.S. GDP Growth Slowed By 1.5 Percent

U.S. GDP Growth Slowed By 1.5 Percent

Chart I-7Euro Area GDP Growth Slowed By 1.5 Percent

Euro Area GDP Growth Slowed By 1.5 Percent

Euro Area GDP Growth Slowed By 1.5 Percent

Chart I-8U.K. GDP Growth Slowed By 1.5 Percent

U.K. GDP Growth Slowed By 1.5 Percent

U.K. GDP Growth Slowed By 1.5 Percent

Markets do not care about the level of growth. They care much more about the change in growth. Financial markets are a discounting mechanism, and what matters most to the price is the change in the assumptions that are embedded within it. For example, if the price were discounting a major economy to grow at 4 percent and that rate of growth subsequently fell to 2.5 percent, then the seemingly benign outcome of respectable growth would cause interest rate expectations to decline. In another major economy, if growth slowed from 2.5 percent to 1 percent, it would precipitate a broadly similar decline in interest rate expectations. In this situation of synchronised and meaningful slowdowns across major economies, and the consequent policy responses, equity and bond absolute prices would experience wild gyrations. By contrast, currencies are relative prices. So if the decline in major economy growth rates and interest rate expectations were broadly similar, currency markets would remain a relative oasis of calm. Which perfectly describes the observation of the last six months. This observation of near-identical slowdowns in the major economies supports our thesis that their genesis came from outside the developed economies, which we expounded in A European Cycle ‘Made In China’. And now we present the smoking gun. While an eerie calm has descended over developed economy currencies, all the action has been in emerging economy currencies, especially the Chinese yuan which has rebounded sharply. The message from the currency markets reinforces our thesis: last year’s growth downswing and the current upswing were made in China (see final chart). Never Focus On Levels Of Economic Growth It is worth repeating that a head-to-head comparison of growth rates across different economies is a meaningless exercise. Here’s a simple way to grasp this crucial point: a 1.5 percent growth rate would be a very pleasing outcome for Europe, it would be a very unpleasing outcome for the U.S., and it would be a catastrophic outcome for China. The reason is that if a population is growing, the economy needs to generate real growth well in excess of the rate of population growth to improve (per person) living standards. That excess comes from productivity growth which lifts standards of living and wellbeing. In the case of Germany or Japan where the population is not growing, or is indeed shrinking, the GDP growth rate that is consistent with these rising standards of living is much lower than in those economies where the population is growing (Chart I-9 and Chart I-10). Chart I-9The Same Productivity Growth In The Euro Area And The U.S. ...

The Same Productivity Growth In The Euro Area And The U.S. ...

The Same Productivity Growth In The Euro Area And The U.S. ...

Chart I-10... Generates Different GDP Growth

... Generates Different GDP Growth

... Generates Different GDP Growth

Necessarily, an economy with weaker demographics – like Germany or Japan – will flirt with technical recessions much more often than one with population growth – like the U.S. or China. But this is just Arithmetic 101. It doesn’t mean that Germany or Japan are in a fundamentally worse shape when it comes to all-important productivity growth and improving wellbeing. Just as important for investors, earnings per share (eps) growth depends on productivity growth and not on GDP growth. Granted, higher GDP from an increasing population will boost a firm’s sales, but without increasing productivity, the firm will have to hire more staff to produce those sales. In essence, the firm will have to employ more capital – issue more shares – which means than earnings per share will not grow. To reemphasise, levels of GDP growth, in themselves, do not drive financial markets. The Perils Of Data-Dependency Recently, the world’s major central banks have become even more wedded to ‘data-dependency’, for two reasons: first, under ever increasing external scrutiny, objectivity to the economic data boosts the transparency and rationale of central bank policy; second, data-dependency acts as a foil to politicians who might want to influence or interfere with the independence of monetary policy. No names mentioned! We applaud the central banks for their good intentions. Yet enhanced data-dependency also carries perils, as it increases the amplitude of the ever-present and natural oscillations in economic growth. The reason is that the high-profile hard data on which monetary policy ‘depends’ such as CPI inflation and GDP growth record what happened in the past, and sometimes in the distant past. Meanwhile, a monetary policy shift today will act on the economy in the future due to the unavoidable lags in transmission. It follows that enhanced data-dependency is akin to a crop farmer who uses last season’s depressed price, from oversupply, to justify planting much less seed for next season. The inevitable undersupply at next season’s harvest will then cause the crop price to surge. Making the farmer plant much more for the following season, at which point the price will collapse again. And the oscillations will continue ad infinitum. Unfortunately, the more backward the data on which policy actions depend, the higher the amplitude of the price and output oscillations. Right now, growth sensitive investment positions are midway through exactly such an up-oscillation, justifying a near-term overweight in emerging market currencies, cyclical equity sectors, and equities versus bonds. But these rallies are highly unlikely to last beyond the summer (Chart I-11). Chart I-11The Recent Mini-Cycle Is ‘Made In China’

The Recent Mini-Cycle Is 'Made In China'

The Recent Mini-Cycle Is 'Made In China'

Stay tuned for the next turn. Fractal Trading System* We are pleased to report that long DAX versus the 30-year bund achieved its 2.5 percent profit target which is now crystallised and closed. This week we note that the sharp sell-off in AUD/CNY is close to the limit of tight liquidity that has signaled recent reversals in this cyclical currency cross. Accordingly, this week’s recommended trade is to go long AUD/CNY. Set a profit target of 1.5 percent with a symmetrical stop-loss. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment’s fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart I-12

Long AUD/CNY

Long AUD/CNY

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report “Fractals, Liquidity & A Trading Model,” dated December 11, 2014, available at eis.bcaresearch.com Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Footnote 1 The German 30-year bund. 2 Based on annualised quarter-on-quarter real GDP growth rates. Fractal Trading System Recommendations Asset Allocation Equity Regional and Country Allocation Equity Sector Allocation Bond and Interest Rate Allocation Currency and Other Allocation Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights Dovish Central Banks & Duration: Bond markets have shifted rapidly in recent weeks, pricing out any and all rate hikes expected over the next year in the major developed economies. With global growth likely to rebound in the latter half of the year, bond yields are now exposed to a hawkish repricing and recovery in inflation expectations, especially in the U.S. Stay below benchmark on overall portfolio duration on a medium-term basis. Model Bond Country Allocations: We are sticking with our current country tilts in our model bond portfolio, as the recent shift in central banker biases has done little to change the relative fundamental drivers between countries. Stay underweight the U.S., Canada & Italy, and overweight core Europe, Japan, the U.K., Spain & Australia, in currency-hedged global government bond portfolios. Feature Well, That Escalated Quickly With global growth remaining soggy, an increasing number of major central banks have been forced to rapidly shift in a more dovish direction. This past week alone, the European Central Bank (ECB), the Bank of Canada (BoC) and the Reserve Bank of Australia (RBA) all signaled that interest rates would be on hold for some time. The ECB went the extra step of announcing a new bank funding program (TLTRO-3), as we predicted last week, to prevent a deeper euro area growth downturn at a time of, as ECB President Mario Draghi described it, “pervasive uncertainty”. Government bond yields declined sharply in all three regions, as markets digested the dovish message from more cautious policymakers. Our Central Bank Monitors for the major developed economies are all decelerating, in line with the soft patch of global growth. Yet only the RBA Monitor has fallen to a level clearly signaling a need for easier monetary policy in Australia. For the other major countries, the Monitors are indicating that an unchanged monetary policy stance is appropriate, and all for the same reason – the loss of economic momentum has not been enough to loosen tight labor markets and drive core inflation rates lower. Government bond yields have already responded to a loss of global growth momentum by pricing out any rate hikes that were expected over the next year, most notably in the U.S. and Canada. Inflation expectations have also adjusted downwards in response to both diminished growth expectations and last year’s sharp plunge in global energy prices. We expect global growth to rebound in the latter half of 2019, alongside higher oil prices, leaving bond yields exposed to upside data surprises and a repricing of expectations for inflation and rate hikes (Chart of the Week). We continue to recommend a below-benchmark overall portfolio duration stance on a 6-12 month horizon, as government bond yields are likely to rise above the very flat forwards in most markets. Chart 1A Bottoming Out Process For Bond Yields

A Bottoming Out Process For Bond Yields

A Bottoming Out Process For Bond Yields

While maintaining a below-benchmark duration stance, the synchronized shift in central bank forward guidance justifies a review of the recommended country allocations in our model fixed income portfolio. Taking Stock Of Our Country Tilts In Our Model Bond Portfolio Global government bond yields peaked back in early November and have fallen in all of the major developed economies (Chart 2). Decomposing the move in benchmark 10-year yields into inflation expectations (using CPI swap rates) and real yields (the difference between nominal yields and CPI swap rates) shows that the bulk of that decline has come from lower real rates in the countries with positive policy rates (U.S., Canada, U.K. and Australia). For countries with zero or negative policy rates (core Europe, Japan), most of the yield decline has been due to falling inflation expectations. Yet the drivers of the decline in yields have changed from the latter two months of 2018 to the first few months of 2019. Generally speaking, the late-2018 bond market rally reflected falling inflation expectations, while recent changes have been a function of moves in real yields. Only in Australia have real yields and inflation expectations both declined steadily since the early November peak in global bond yields.

Chart 2

The greater influence of the real component of yields makes sense, as markets now discount fewer rate hikes and more accommodative monetary policy. Currently, our recommended country allocation in the Governments portion of our model bond portfolio includes underweights in the U.S., Canada and Italy and overweights in Australia, the U.K., Japan, Germany, France and Spain (the latter is a position versus Italy within an overall underweight stance on Peripheral European debt). In light of the more ubiquitously neutral/dovish global policy bias, we are reevaluating those country tilts per the following indicators: 1. Cyclical growth indicators: Both manufacturing purchasing managers indices (PMIs) and the leading economic indicators (LEIs) produced by the OECD are well off the cyclical peaks (Chart 3). In terms of levels, the PMIs are holding above the 50 threshold, suggesting expanding manufacturing activity, in the U.S., U.K., Canada and Australia, but are below 50 in the euro area and Japan. Chart 3Growth Has Lost Momentum Everywhere

Growth Has Lost Momentum Everywhere

Growth Has Lost Momentum Everywhere

2. Market-based inflation expectations: 10-year CPI swap rates have generally stabilized alongside energy prices, after the sharp drops seen in the latter months of 2018 (Chart 4). Australia is the lone exception where expectations continue to drift lower. The correlations between CPI swap rates and oil prices denominated in local currency are strongest in the U.S. and Canada and weakest in Australia. There is great diversity of the levels of CPI swap rates, however, from as low as 0.2% in Japan to as high as 3.5% in the U.K. Chart 4Inflation Expectations Are Stabilizing Outside Of Japan & Australia

Inflation Expectations Are Stabilizing Outside Of Japan & Australia

Inflation Expectations Are Stabilizing Outside Of Japan & Australia

3. Our Central Bank Monitors vs. our 12-month discounters: Except for Australia, our Monitors are all hovering very close to the zero line, indicating no pressure on policymakers to move policy rates (Chart 5). Our 12-month discounters, which measure the interest rate changes over the next year priced into Overnight Index Swap (OIS), are all close to zero, as well (again, with the exception of Australia, where a full 25bp rate cut is already priced). Chart 5Our Central Bank Monitors Are Calling For Stable Policy (ex Australia)

Our Central Bank Monitors Are Calling For Stable Policy (ex Australia)

Our Central Bank Monitors Are Calling For Stable Policy (ex Australia)

Just looking at these indicators, the ideal combination would be to underweight countries where yields are vulnerable to an upward repricing (PMIs still above 50, higher oil/CPI swaps correlations and no rate hikes priced) and to overweight countries where yields are less likely to rise (PMIs below 50, lower oil/CPI swaps correlations and where our 12-month discounters are not priced for rate cuts). Under these criteria, underweights in the U.S. and Canada are still justified, as are overweights in core Europe and Japan. The surprising firmness of the U.K. manufacturing PMI relative to the persistent downtrend in the U.K. LEI muddies the message a bit on Gilts, although the relatively high level of our 12-month discounter (still 13bps of hikes priced) is a bullish sign with our BoE Monitor now sitting right near zero. In Australia, the manufacturing PMI is also surprisingly firm but, the underlying weak momentum in overall Australian growth is leaving the door open to potential RBA rate cuts later this year. For all our country recommendations within our model bond portfolio framework, we always look at yields and returns on a currency-hedged basis in U.S. dollar terms. We do this to separate the fixed income component of global bond returns from the currency component. Yet when looking at the government bond yield curves in our model bond portfolio universe, hedged into USD, there is very little differentiation among those countries with the higher credit ratings (Chart 6). Only Spain (A-rated) and Italy (BBB-rated) have hedged yields that are outside the 2-3% range seen in the other major developed economies.

Chart 6

From a fundamental point of view, those narrow yield differentials among the higher-rated markets largely reflect the convergence of trend economic growth rates. In a recent Weekly Report, we looked at the long-run growth rates of potential GDP and labor productivity for the U.S., euro area and Japan and noted that the differences between them were fairly modest.1 This justified narrow currency-hedged yield differentials between U.S. Treasuries, German Bunds and Japanese government bonds (JGBs). When we add Canada, Australia and the U.K. to the mix (Chart 7), we can see similar convergence of potential GDP growth to rates between 1-2% and long-run productivity growth around 0.5% (using OECD data for both). Chart 7No Major Differences In Long-Run Growth Rates

No Major Differences In Long-Run Growth Rates

No Major Differences In Long-Run Growth Rates

The convergence is largely complete for all countries except Australia, where potential GDP growth is estimated to be 2.4%. Yet the long-run downtrend in potential growth is powerful and full convergence to the sub-2% levels seen in the other countries appears inevitable (and goes a long way in explaining the historically low level of Australian bond yields versus global peers). We can also see convergence in looking at the more recent history of the market pricing of the expected long-run neutral interest rate, using our real terminal rate proxy (the 5-year OIS rate, 5-years forward minus the 5-year CPI swap rate 5-years forward). Those measures for all of the major developed markets in our model bond portfolio are shown in Chart 8. The markets are pricing in real policy rate convergence, as well, with real rates expected to stay in a range between -0.5% (core Europe) and +0.5% (Canada). The U.K. is the one outlier, with the market pricing in a terminal real rate of -2%, although this likely reflects the markets discounting in the long-run effects of Brexit on the U.K. economy. Chart 8Markets Expect Near-Zero Real Terminal Rates (ex the U.K.)

Markets Expect Near-Zero Real Terminal Rates (ex the U.K.)

Markets Expect Near-Zero Real Terminal Rates (ex the U.K.)

So what does all this mean for our recommended country allocations in our model bond portfolio? In Chart 9, we show the relative performance of the each country, hedged into U.S. dollars and duration-matched) versus the Bloomberg Barclays Global Treasury Index. Our overweight tilts are in the top panel, while our underweight tilts are in the bottom panel. Chart 9Sticking With The Country Allocations In Our Model Bond Portfolio

Sticking With The Country Allocations In Our Model Bond Portfolio

Sticking With The Country Allocations In Our Model Bond Portfolio

Generally speaking, are recommendations have done well. Given our read on the indicators above, we see little reason to change the allocations. Our biggest concerns would be the underweights in Canada and Italy, given the sharp weakening of growth in both countries. For Italy, however, we view that as a negative given Italy’s high debt levels that require faster nominal growth to ensure debt sustainability. A more dovish ECB should help keep European bond volatility low, to the benefit of carry trades like Italian government bonds. However, we prefer to play that through our overweight in Spain while we await signs of stabilization in the Italian LEI before upgrading Italy in our model bond portfolio. As for Canada, we plan on doing a deeper dive on their economy and inflation trends in next week’s report before considering any changes to our allocation. Bottom Line: We are sticking with our current country tilts in our model bond portfolio, as the recent shift in central banker biases has done little to change the relative fundamental drivers between countries. Stay underweight the U.S., Canada & Italy, and overweight core Europe, Japan, the U.K., Spain & Australia, in currency-hedged global government bond portfolios. Robert Robis, CFA, Chief Fixed Income Strategist rrobis@bcaresearch.com 1 Please see BCA Global Fixed Income Strategy Weekly Report, “Europe & Japan: The Anchor Weighing On Global Bond Yields”, dated February 26, 2019, available at gfis.bcaresearch.com Recommendations The GFIS Recommended Portfolio Vs. The Custom Benchmark Index

Pervasive Uncertainty, Persuasive Central Banks

Pervasive Uncertainty, Persuasive Central Banks

Duration Regional Allocation Spread Product Tactical Trades Yields & Returns Global Bond Yields Historical Returns

Highlights Duration: With rate hikes more likely than cuts over the next 12 months, it makes sense to maintain below-benchmark duration in U.S. bond portfolios. However, timing the next up-move in Treasury yields is difficult. We recommend that investors initiate positive carry yield curve trades to boost returns while we wait for Treasury yields to bottom alongside the CRB/Gold ratio. Corporates: The Fed’s pause is leading to improvement in our global growth indicators. The end result is a window where corporate spreads will tighten during the next few months. Remain overweight corporate bonds, but be prepared to downgrade when spreads reach our targets. CMBS: We upgrade our allocation to non-agency CMBS from underweight to neutral, due to elevated spreads relative to other Aaa-rated sectors. While spreads are currently attractive, the macro back-drop is also fairly bleak. If spreads tighten to more reasonable levels or CMBS delinquencies start to rise we will be quick to downgrade. Feature Green Shoots For Global Growth Since 1994 the Global (ex. U.S.) Leading Economic Indicator (LEI) has contracted relative to its 12-month trend six times. In all six episodes it eventually dragged the U.S. LEI down with it (Chart 1). As we predicted last August, the U.S. economy cannot remain an oasis of prosperity when the rest of the world is in turmoil.1 However, to focus on the weakening U.S. data right now is to miss the bigger picture. Chart 1U.S. Follows The Rest Of The World

U.S. Follows The Rest Of The World

U.S. Follows The Rest Of The World

Corporate bond spreads already reacted to the global slowdown by widening near the end of last year. Then, the Federal Reserve reacted to tighter financial conditions by signaling a pause in its rate hike cycle. We took that opportunity to turn more bullish on spread product, and now, there are budding signs of improvement in the global growth outlook. While the Global LEI (including the U.S.) remains in a downtrend, our Global LEI Diffusion Index is well off its lows (Chart 2). Historically, the Diffusion Index has a good track record leading changes in the overall indicator. Chart 2Global LEI Diffusion Index Is Back Above 50%

Global LEI Diffusion Index Is Back Above 50%

Global LEI Diffusion Index Is Back Above 50%

Similarly, the timeliest indicators of global growth that called the early-2016 peak in credit spreads are starting to improve (Chart 3). The CRB Raw Industrials index is breaking out, the BCA Market-Based China Growth Indicator has recovered and Global Industrial Mining Stock prices are heading up. Chart 3Global Growth Checklist

Global Growth Checklist

Global Growth Checklist

All told, it appears that the Fed’s pause and related dollar weakness, along with less restrictive fiscal and monetary policies in China, are starting to pay dividends.2 The end result is a window where leading global growth indicators will improve and financial conditions will ease. We recommend that investors maintain an overweight allocation to corporate bonds during this supportive window, though we also note that the continued rapid pace of corporate re-leveraging is a cause for concern. We will be quick to downgrade our recommended allocation to corporate bonds when our near-term spread targets are hit. Our spread target for Aa-rated corporates is 57 bps, the current spread level is 61 bps. Our spread target for A-rated corporates is 85 bps, the current spread level is 92 bps. Our spread target for Baa-rated corporates is 128 bps, the current spread level is 159 bps. Our spread target for Ba-rated corporates is 188 bps, the current spread level is 243 bps. Our spread target for B-rated corporates is 297 bps, the current spread level is 400 bps. Our spread target for Caa-rated corporates is 573 bps, the current spread level is 827 bps. We recommend avoiding Aaa-rated corporate bonds, which already look expensive. We explore the universe of Aaa-rated spread product in more detail below. Implications For Treasury Yields The Fed’s pause and the nascent improvement in global growth are both obvious positives for corporate spreads. The impact on Treasury yields is somewhat less obvious. We contend that once financial conditions ease sufficiently, the market will start to price-in further Fed rate hikes and this will pressure Treasury yields higher at both the short and long ends of the curve. The ratio between the CRB Raw Industrials index and the gold price can help clarify this concept. Chart 4 shows that the 10-year Treasury yield tends to rise when the CRB index outpaces gold, and vice-versa. The rationale for this correlation is that the CRB index is a proxy for global growth and gold is a proxy for the stance of monetary policy. Chart 4Timing The Next Treasury Sell-Off

Timing The Next Treasury Sell-Off

Timing The Next Treasury Sell-Off

A rising gold price suggests that monetary policy is becoming increasingly accommodative. This eventually leads to an improvement in global growth and a rising CRB index. But Treasury yields do not rise alongside the CRB index. They only increase once the improvement in global growth is sufficient for the market to discount a tighter monetary policy. That moment occurs when the CRB index rises more quickly than the gold price. The bottom line is that with rate hikes more likely that cuts over the next 12 months it makes sense to maintain below-benchmark duration in U.S. bond portfolios. However, timing the next up-move in Treasury yields is difficult. We recommend that investors initiate positive carry yield curve trades to boost returns while we wait for Treasury yields to bottom alongside the CRB/Gold ratio.3 Checking In On The Labor Market Based on the number of emails we’ve received on the topic, the last two U.S. employment reports have stoked some confusion among investors. This is not surprising given the volatility in the headline numbers: Nonfarm payrolls increased +311k in January and only +20k in February. The U3 unemployment rate jumped to 4% in January, then fell back to 3.8% in February. The U6 unemployment rate jumped to 8.1% in January, then fell back to 7.3% in February. Much of the volatility is likely explained by data collection issues related to the partial government shutdown, which makes it useful to look through the noise and focus on a few important trends. Trend #1: Slow Growth In Q1 The employment data clearly point to a U.S. growth slowdown in the first quarter of 2019. Real GDP growth can be proxied by looking at the sum of the growth rate in aggregate hours worked and the growth rate in labor force productivity (Chart 5). The recent steep decline in hours worked suggests that first quarter growth is going to be weak. Chart 5Employment Data Point To Slow Growth In Q1

Employment Data Point To Slow Growth In Q1

Employment Data Point To Slow Growth In Q1

But as was noted in the first section of this report, weak Q1 GDP is the result of the global growth slowdown dragging the U.S. lower. Crucially, the market has already discounted this eventuality and the budding improvement in leading global growth indicators suggests that the U.S. slowdown will prove temporary. Trend #2: No More Slack A broad set of indicators now all point to the fact that the U.S. economy is at full employment (Chart 6). The implication is that we should expect wage growth to accelerate and payroll growth to decelerate as we move deeper into the cycle. Chart 6At Full Employment

At Full Employment

At Full Employment

Some investors may retain the belief that a rising labor force participation rate will keep wage growth capped, but even here the prospects are dim. The participation rate for people of prime working age (25-54) has risen rapidly during the past few years, but that has only led to a small bounce in overall participation (Chart 7). This is because the aging of the population has pushed more and more people out of that prime working age demographic bucket. Chart 7Labor Force Participation

Labor Force Participation

Labor Force Participation

The dashed line in the top panel of Chart 7 shows where the labor force participation rate would be, based on current demographics, if the participation rate for each narrow age cohort reverted to its July 2007 level. The message is that the scope for a further increase in labor force participation is limited. Trend #3: No Recession Risk Yet The full employment state of accelerating wage growth and decelerating employment growth can last for some time before a recession hits. In our research we have noted that, from a financial markets perspective, one of the best leading indicators is the change in initial jobless claims. Typically, a bottom in initial jobless claims coincides with an inflection point in Treasury excess returns (Chart 8). Chart 8Jobless Claims Have Called Troughs In Treasury Returns

Jobless Claims Have Called Troughs In Treasury Returns

Jobless Claims Have Called Troughs In Treasury Returns

Initial jobless claims have risen somewhat during the past few weeks, and while this trend is worth monitoring, it is premature to flag it as a concern. The 4-week moving average in claims has already fallen back to 226k from a recent high of 236k, and next week an elevated print of 239k will roll out of the 4-week average. Any initial claims print below 239k next week will cause the 4-week average to decline further. Bottom Line: The U.S. labor market has reached full employment. Going forward we should expect a continued acceleration in wage growth and deceleration in payroll growth. This situation can persist without causing a recession until initial jobless claims start to head higher. We see no evidence of this as of yet. Aaa-Rated Spread Products In this week’s report we consider the risk/reward trade-off on offer from the major Aaa-rated spread products. Specifically, we consider corporate bonds, agency and non-agency CMBS, conventional 30-year residential MBS and consumer ABS (both credit cards and auto loans). Focusing purely on expected returns, we find that non-agency CMBS offer the highest option-adjusted spread of 73 bps. This is followed by 65 bps from corporates, 50 bps from Agency CMBS, 41 bps from MBS, 35 bps from auto ABS and 31 bps from credit card ABS. But this is just one side of the equation. Chart 9 shows each sector’s spread relative to the likelihood that it will experience losses versus Treasuries. To measure the risk of losses we use our measure of Months-To-Breakeven. This is defined as the number of months of average spread widening that each sector requires before it starts to lose money relative to a duration-matched position in Treasury securities. Essentially, the Months-To-Breakeven measure is each sector’s 12-month breakeven spread adjusted by its spread volatility since 2014. We only calculate spread volatility since 2014 because that it is when data for Agency CMBS start.

Chart 9

Chart 9 shows that while Aaa corporate bonds offer elevated expected returns compared to the other sectors, they also offer a commensurate increase in risk. Similarly, consumer ABS offer lower expected returns than the other sectors but with considerably less risk. According to Chart 9, the only sector that offers an attractive risk/reward trade-off is non-agency CMBS. This warrants further investigation. Looking at spreads throughout history, we see that non-agency CMBS spreads also look relatively attractive. While Aaa-rated consumer ABS spreads are near all-time lows, non-agency CMBS spreads are still not quite one standard deviation below the pre-crisis mean (Chart 10). Chart 10CMBS Spreads Have Room To Narrow

CMBS Spreads Have Room To Narrow

CMBS Spreads Have Room To Narrow

We noted in last week’s report that consumer ABS look even worse when we incorporate the macro environment.4 All-time tight ABS spreads currently coincide with tightening consumer lending standards and a rising consumer credit delinquency rate. This is why we downgraded consumer ABS from neutral to underweight last week. The macro environment for CMBS is also fairly bleak (Chart 11). Commercial real estate lending standards are tightening, loan demand is waning and prices are decelerating. The one saving grace is that, so far, this has not translated into a rising CMBS delinquency rate (Chart 11, bottom panel). It is probably only a matter of time before CMBS delinquencies start to trend higher, but with spreads so attractive relative to the investment alternatives, the sector warrants better than an underweight allocation. Chart 11Delinquencies Biased Higher?

Delinquencies Biased Higher?

Delinquencies Biased Higher?

Bottom Line: We upgrade our allocation to non-agency CMBS from underweight to neutral. Spreads are currently attractive relative to other Aaa-rated sectors, but we will keep a close eye on the evolving macro backdrop. If spreads tighten to more reasonable levels or if CMBS delinquencies start to rise, we will be quick to downgrade. Ryan Swift, U.S. Bond Strategist rswift@bcaresearch.com Footnotes 1 Please see U.S. Bond Strategy Weekly Report, “An Oasis Of Prosperity”, dated August 21, 2018, available at usbs.bcaresearch.com 2 For further details on recent shifts in Chinese policy please see China Investment Strategy Weekly Report, “Dealing With A (Largely) False Narrative”, dated February 27, 2019, available at cis.bcaresearch.com 3 For more details on the attractiveness of positive carry yield curve trades please see U.S. Bond Strategy Weekly Report, “Paid To Wait”, dated February 26, 2019, available at usbs.bcaresearch.com 4 Please see U.S. Bond Strategy Portfolio Allocation Summary, “The Sequence Of Reflation”, dated March 5, 2019, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Rather ironically given its name, Modern Monetary Theory (MMT) plays down the influence of monetary policy over the economy. Its adherents argue that Congress, and not the Fed, should be responsible for maintaining full employment. A prolonged period of…

Highlights The deceleration in global growth that began in 2018 is entering a transition phase. The bottoming out process could prove to be volatile, warning against betting the farm too early on pro-cyclical currencies. Tactical short USD bets should initially be played via the euro1 and Swedish krona. The poor Canadian GDP report last week could be a harbinger for more data disappointments down the road. Meanwhile, the dovish shift by the ECB could paradoxically be bullish for the euro beyond the near term. Go short USD/SEK and buy EUR/CAD for a trade. Feature A currency exchange rate is simply a measure of relative prices between two countries. As such, the starting point for any currency forecast should be how those values are likely to evolve over time. For much of 2018, U.S. growth benefited from the impact of the Trump tax cuts, a boost to government spending agreed in January of that year, and the lagged effect of an easing in financial conditions from December 2016 to January 2018. Outside the U.S., what appeared to be idiosyncratic growth hiccups in both Europe and Japan finally morphed into full-blown slowdowns. Slower Chinese credit growth and the U.S.-China trade war were the ultimate straws that broke the camel’s back, deeply hurting global growth (Chart I-1). Consequently, the greenback surged. Chart I-1The Global Growth Slowdown Persists

The Global Growth Slowdown Persists

The Global Growth Slowdown Persists

Fading U.S. Dollar Tailwinds At first glance, the picture remains largely similar today, with global growth still slowing and U.S. growth still outperforming. However, a key difference from last year is that U.S. growth leadership is set to give way to the rest of the world. The U.S. ISM manufacturing PMI peaked last August and has been steadily rolling over relative to its trading partners. The U.S. economic surprise index tells a similar story, with last month’s disappointing retail sales numbers nudging the series firmly below zero. Relative leading economic indices also suggest that U.S. growth momentum has slowed relative to the rest of the world. Historically, the relative growth differential between the U.S. and elsewhere has had a pretty good track record of dictating trends in the dollar (Chart I-2). Chart I-2U.S. Growth Leadership Might Soon End

U.S. Growth Leadership Might Soon End

U.S. Growth Leadership Might Soon End

Whether or not these trends persist beyond the first quarter will depend on the sustainability of China’s recent stimulus efforts. On the positive side, typical reflation indicators such as commodity prices, emerging market currencies, and industrial share prices have perked up in response to a nascent upturn in the credit impulse. On the other hand, policy shifts affect the economy with a lag, suggesting it is too early to tell whether the latest credit injection has been sufficient to turn around the Chinese economy, let alone the rest of the world. What is clear is that the bottoming processes tend to be volatile and protracted, suggesting it is still too early to bet the farm on pro-cyclical currencies. In the interim, investors could track the following indicators to help time a definitive turning point: Whether or not easing liquidity conditions will lead to higher growth is often captured by the CRB Raw Industrial index-to-gold, copper-to-gold, and oil-to-gold ratios. It is encouraging that these also tend to move in lockstep with the U.S. bond yields, another global growth barometer. The power of the signal is established when all three indicators peak or bottom at the same time, as is the case now (Chart I-3). The next confirmation will come with a clear break-out in these ratios. Chart I-3Reflation Indicators Are Perking Up

Reflation Indicators Are Perking Up

Reflation Indicators Are Perking Up

Chinese M2 relative to GDP has bottomed. Historically, this ratio has lit a fire under cyclical stocks and, by extension, pro-cyclical currencies (Chart I-4). The growth rate is still at zero, meaning excess liquidity is not accelerating on a year-over-year basis. Meanwhile, our Emerging Markets team argues that broad credit growth is still decelerating.2 A break above the zero line, probably in the second half of this year, could be a catalyst to shift fully to a pro-cyclical currency stance. Chart I-4Chinese Excess Liquidity Improving

Chinese Excess Liquidity Improving

Chinese Excess Liquidity Improving

On a similar note, currencies in emerging Asia that sit closer to the epicenter of stimulus appear to have bottomed. If those in Latin America can follow suit, it would indicate that policy stimulus is sufficient, and the transmission mechanism is working (Chart I-5). Chart I-5EM Currencies Are Trying To Bottom

EM Currencies Are Trying To Bottom

EM Currencies Are Trying To Bottom

Finally, China-sensitive industrial commodities, especially metals and building materials, appear to have troughed and are perking up nicely. There was a supply-related issue with the Vale dam bursting in Brazil and a subsequent surge in iron-ore prices, but it is now clear that the entire industrial commodity complex has stopped falling (Chart I-6). Chart I-6Chinese Industrial Commodities Are Rallying

Chinese Industrial Commodities Are Rallying

Chinese Industrial Commodities Are Rallying

Be Selective On USD Shorts Our strategy is to be selective as U.S. dollar tailwinds shift to headwinds, by initially expressing tactical USD shorts via the euro and the Swedish krona. Last week, we highlighted the fact that investors are currently too pessimistic on Europe’s growth prospects. More importantly, most of the factors that toppled European growth domestically – the implementation of new auto-emission standards in Germany, the rising cost of capital in Italy via exploding bond yields, and the populist Gilets Jaunes protests in France – are mostly behind us. Fiscal policy is also set to be loosened this year, and last year’s weakness in the euro will contribute to easier financial conditions. The improvement in European investor sentiment relative to current conditions could be a harbinger of positive euro area data surprises ahead (Chart I-7). Chart I-7Euro Zone Data Might Surprise To The Upside

Euro Zone Data Might Surprise To The Upside

Euro Zone Data Might Surprise To The Upside

The European Central Bank left rates unchanged at yesterday’s policy meeting but the decision for a new Targeted Long Term Refinancing Operation (TLTRO III – or in other words, cheap loans), could be paradoxically bullish for the euro. If a central bank eases financing conditions at a time when growth is hitting a nadir, it is tough to argue that this is bearish for the currency. Our Global Fixed Income team nailed the move by the ECB in this week’s report.3 European banks have been in the firing line of sluggish growth, negative interest rates, and increased regulatory scrutiny. In the case of Italy, an NPL ratio 9.4% is nearly triple that of the euro area. And with circa 10% of total bank lending in Spain and Italy funded by TLTROs, re-funding by the ECB is exactly what the doctor ordered. In the case of the Sweden, the undervaluation of the krona has begun to mitigate the effects of negative interest rates – mainly a buildup of household leverage and an exodus of foreign direct investment. The GDP report last week was well above expectations, with year-on-year growth of 2.4%. Encouragingly, this was driven by net exports rather than consumption. The Swedish manufacturing PMI release for February was also very encouraging. Orders jumped from 50.4 to 54.0 while export orders jumped from 51.5 to 53.4. The growth in wages is beginning to catch up to new borrowings, meaning domestic consumption could be increasingly financed through income. This will alleviate the need for the Riksbank to maintain an ultra-accommodative policy. On a relative basis, the Swedish economy appears to have bottomed relative to that of the U.S., making the USD/SEK an attractive way to play USD downside. From a technical perspective, the cross is facing strong resistance at the triple top established from the 2009 highs around 9.45 (Chart I-8). Aggressive investors should begin accumulating short positions, while being cognizant of the negative carry. Chart I-8The Swedish Krona Looks Like A Buy

The Swedish Krona Looks Like A Buy

The Swedish Krona Looks Like A Buy

Bottom Line: Our favorite indicator for gauging ultimate downside in the dollar is the gold-to-bond ratio. Ever since the global financial crisis, gold has stood as a viable threat to dollar liabilities, capturing the ebb and flow of investor confidence in the greenback tick-for-tick (Chart I-9). Any sign that the balance of forces are moving away from the U.S. dollar will favor a breakout in the gold-to-bond ratio. For now, USD short positions should be played via the euro and Swedish krona. Chart I-9Pay Close Attention To The Gold-To-Bond Ratio

Pay Close Attention To The Gold-To-Bond Ratio

Pay Close Attention To The Gold-To-Bond Ratio

Buy EUR/CAD For A Trade Last week saw an extremely disappointing GDP report out of Canada, which prompted the Bank of Canada to keep interest rates on hold this week, followed by quite dovish commentary. In a 90-degree maneuver from its January policy statement that rates will need to rise over time, BoC Governor Stephen Poloz said the path for future increases had become “highly uncertain.” Like many central banks around the world, the BoC has been blindsided by the depth of the negative growth impulse outside its borders, which has begun to seep into the domestic economy. The economy grew at an annualized pace of 0.4% in the fourth quarter, the lowest in over two years. Capital expenditures collapsed at a rate of 2.7%, marking the third consecutive quarter of declines. The forward OIS curve is pricing in no rate hikes for Canada this year, meaning sentiment on the loonie is already depressed. However, our contention is that even if growth bottoms by the second half of this year, the Canadian dollar will offer little value to play this cyclical rebound. Our recommendation is to play the loonie’s downside via the euro. First, valuations and balance-of-payment dynamics favor the euro versus the CAD on a long-term basis. Second, we estimate there is more scope for long-term interest rate expectations to rise in the euro area than in Canada (Chart I-10). European rates are further below equilibrium, and the ECB’s dovish shift will help lift the growth potential of the euro area. Meanwhile, the Canadian neutral rate will be heavily weighed down by the large stock of debt in the Canadian private sector, exacerbated by overvaluation in the housing market. This means that expectations in the 2-year forward market are likely to favor the euro versus the CAD. Chart I-10Buy EUR/CAD For A Trade

Buy EUR/CAD For A Trade

Buy EUR/CAD For A Trade

The biggest risk to this view is the price of oil. The EUR/CAD exchange rate is not as negatively correlated with oil as the USD/CAD, but nonetheless the CAD benefits more from rising oil prices than the euro does. BCA’s bullish oil view is a risk over the next six months. On the downside, the EUR/CAD could potentially test the bottom of the upward trending channel that has existed since 2012. This would put EUR/CAD in the vicinity of 1.45 (currently trading at 1.5049). However, initial upside resistance rests at the triple top a nudge above 1.6 (Chart I-11). Chart I-11EUR/CAD Technicals: Limited Downside

EUR/CAD Technicals: Limited Downside

EUR/CAD Technicals: Limited Downside

Meanwhile, economically, Canada is benefiting less from oil prices today than it has in the past. First, the Canadian oil benchmark trades at a large discount to Brent, and second, Canada is having trouble shipping its own oil at a moderate cost due to lack of pipeline capacity.4 Bottom Line: Investors should buy the EUR/CAD for a trade. The Canadian dollar is likely to outperform its antipodean counterparts, but faces limited upside versus the U.S. dollar. There are better opportunities to play USD downside, namely via the Swedish krona and the euro. Stand Aside On The Australian Dollar For more than two decades, the Australian dollar has tended to be mostly driven by external conditions, especially the commodity cycle. But for the first time in several years, domestic factors have joined in to exert powerful downward pressure on the currency. The Australian Prudential Regulation Authority (APRA) has been on a mission to surgically deflate the overvalued housing market, while engineering a soft landing in the economy. Initially, their macro-prudential measures worked like a charm, as owner-occupied housing activity remained resilient relative to “investment-style” housing. What has become apparent now is that the soft landing intended by the authorities is rapidly morphing into a housing crash (Chart I-12). Chart I-12Australia: Anatomy Of A Hard Landing

Australia: Anatomy Of A Hard Landing

Australia: Anatomy Of A Hard Landing

In addition, the upcoming general election could exacerbate the risks to the country’s banks and the housing market.5 The center-left Labour Party, which has moved further to the left in this electoral cycle, has promised several regulatory changes. First, the Labour government would want to get rid of “negative gearing,” the practice of using investment properties that are generating losses to offset one’s income tax bill. Second, the capital gains tax exemption from selling properties will be reduced from 50% to 25%. Third, the Labour government would end the policy of reimbursing investors for the corporate tax paid by the company. This would end the incentive for retirees to own high dividend yielding equities, such as those of Australian banks. This week, the Reserve Bank of Australia kept rates on hold and acknowledged risks to the housing market, but bank stocks suggest they remain well behind the curve (Chart I-13). The futures market is already pricing in 23 basis points of rate cuts by the end of the year, and the contention of our fixed income team is that more might be needed down the road. First, all the preconditions for a rate hike – underemployment below 8%, a rebound in Chinese economic activity and core CPI in the range of 2-3% – have not been met. The reality is that core CPI has lagged the target range since late-2015, and now faces downside risks. Chart I-13Australian Bank Stocks Are Pricing In A Curve Inversion

Australian Bank Stocks Are Pricing In A Curve Inversion

Australian Bank Stocks Are Pricing In A Curve Inversion

That said, a lot of the bad news already appears priced into the Australian dollar, which is down 14% from its 2018 peak, and 37% from its 2011 peak. This suggests outright short AUD bets are at risk from either upside surprises in global growth, or simply the forces of mean reversion (Chart I-14). Chart I-14Stand Aside On The Australian Dollar For Now

Stand Aside On The Australian Dollar For Now

Stand Aside On The Australian Dollar For Now

Bottom Line: Sentiment on the Aussie dollar is already bearish, warning against putting on fresh shorts. Our short AUD positions, expressed via the NZD and the CAD, are currently 6.74% and 1.99% in the money, respectively. Investors should hold onto these positions, but tighten stops to protect profits. Chester Ntonifor, Foreign Exchange Strategist chestern@bcaresearch.com Footnotes 1 Please see Foreign Exchange Strategy Special Report titled “A Contrarian Bet On The Euro,” dated March 1, 2019 available at fes.bcaresearch.com 2 Please see Emerging Markets Strategy Weekly Report titled “EM: A Sustainable Rally Or False Start?,” dated March 7, 2019 available at ems.bcaresearch.com 3 Please see Global Fixed Income Strategy Special Report, titled “The ECB’s Next Move: Taking Out Some Insurance,” dated March 5, 2019, available at gfis.bcaresearch.com 4 Please see Commodity & Energy Strategy Weekly Report, titled “Oil Price Diffs: Global Convergence,” dated March 7, 2019, available at ces.bcaresearch.com 5 Please see Geopolitical Strategy Special Report, titled “A Year Of Change In Australia?,” dated December 5, 2018, available at gps.bcaresearch.com Currencies U.S. Dollar Chart II-1USD Technicals 1

USD Technicals 1

USD Technicals 1

Chart II-2USD Technicals 2

USD Technicals 2

USD Technicals 2

Recent data in the U.S. have been mixed: Annualized Q4 GDP growth came in line with expectations at 2.6%, but both the Atlanta and New York Fed models suggest sub 1% growth in Q1 this year. ISM manufacturing PMI missed expectations, falling to 54.2, while the non-manufacturing PMI increased to 59.7. Q4 unit labor costs increased to 2%, surprising to the upside. The DXY index has gained 1.17% this week. Upside on the dollar will be based on Fed’s capacity to continue tightening monetary policy later this year. However, there are increasing signs pointing to a weakening in leadership of U.S. growth this cycle, which could be a headwind for the counter-cyclical dollar. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Global Liquidity Trends Support The Dollar, But... - January 25, 2019 The Euro Chart II-3EUR Technicals 1

EUR Technicals 1

EUR Technicals 1

Chart II-4EUR Technicals 2

EUR Technicals 2

EUR Technicals 2

Recent data in the euro area show some specter of stabilization: Yearly consumer price inflation increased to 1.5%, in line with expectations. Q4 GDP growth on a year-on-year basis fell to 1.1%, marginally in line. Encouragingly, the Markit composite PMI increased to 51.9. The manufacturing PMI came in at 49.3, while services PMI came in at 52.8. Finally, retail sales grew higher than expected, with a reading of 2.2%. EUR/USD has fallen by 1.3% this week. The ECB kept interest rates on hold with a dovish tilt. Paradoxically, this could be bullish for the euro, if it allows growth to definitively bottom. Easing financial conditions in the euro area are reflationary and risks to the periphery have been curtailed. Report Links: A Contrarian Bet On The Euro - March 1, 2019 Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 The Yen Chart II-5JPY Technicals 1

JPY Technicals 1

JPY Technicals 1

Chart II-6JPY Technicals 2

JPY Technicals 2

JPY Technicals 2

Recent data in Japan have been mixed: Yearly inflation surprised to the upside, coming in at 0.6%. The core inflation excluding fresh food also came in higher than expected at 1.1%. January unemployment rate missed expectations, climbing to 2.5%; while the jobs-to-applicants ratio stayed at 1.63. Nikkei manufacturing PMI surprised to the upside, coming in at 48.9. USD/JPY has risen by 0.4% this week. While we are positive on the safe-haven yen on a structural basis, we struggle to see any near-term upside amid significant Japanese stock and bond outflows. We will be discussing the outlook for the yen in an upcoming report. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Yen Fireworks - January 4, 2019 British Pound Chart II-7GBP Technicals 1

GBP Technicals 1

GBP Technicals 1

Chart II-8GBP Technicals 2

GBP Technicals 2

GBP Technicals 2

Recent data in the U.K. have been improving: February consumer confidence came in at -13, slightly higher than expectations. Markit manufacturing PMI came in at 52, in line with expectations; while the services PMI surprised to the upside, coming in at 51.3. The Halifax house price index surprised to the upside, rising 5.9% mom in February. GBP/USD has fallen by 1.2% this week. During the speech on March 5, the Bank of England governor Mark Carney highlighted the market underestimates the potential for interest rate hikes. Overall, we remain bullish on the pound in the long-term, but volatility is set to rise in the near term as we approach the Brexit March 29 deadline. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Deadlock In Westminster - January 18, 2019 Australian Dollar Chart II-9AUD Technicals 1

AUD Technicals 1

AUD Technicals 1

Chart II-10AUD Technicals 2

AUD Technicals 2

AUD Technicals 2

Recent data in Australia have been dismal: The RBA commodity price index advanced by 9.1% year-on-year in February, but this was supply related. Building permits continue to contract at 29% year-on-year. Finally, the annualized Q4 GDP growth fell to 0.2%, more than 50% below expectations. AUD/USD fell by 1.2% this week. The RBA kept the interest rate unchanged at 1.5%. Governor Philip Lowe acknowledged the downside risks to the housing market and overall economy, and warned about the “significant uncertainties around the forecast.” That said, AUD/USD has fallen by a 13% since the January 2018 highs, warning against establishing fresh shorts at this juncture. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 CAD And AUD: Jumping Higher To Plunge Deeper - February 1, 2019 New Zealand Dollar Chart II-11NZD Technicals 1

NZD Technicals 1

NZD Technicals 1

Chart II-12NZD Technicals 2

NZD Technicals 2

NZD Technicals 2

Recent data in New Zealand have been mixed: Seasonally adjusted building permits increased 16.5% month-on-month in January, a huge jump. However, the ANZ activity business confidence dropped to -30.9. Most importantly, terms of trade fell to -3% in the fourth quarter, underperforming expectations. NZD/USD depreciated by 0.9% this week. The key for the Kiwi will be a pickup in agricultural commodity prices, which remain in a definitive bear market. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Updating Our Intermediate Timing Models - November 2, 2018 Canadian Dollar Chart II-13CAD Technicals 1

CAD Technicals 1

CAD Technicals 1

Chart II-14CAD Technicals 2

CAD Technicals 2

CAD Technicals 2

Recent data in Canada have been disappointing: Q4 current account balance has deteriorated, coming in at C$ -15.48 billion. Moreover, annualized Q4 GDP growth missed analysts’ forecast, coming in at 0.4%. Finally, the Markit manufacturing PMI weakened to 52.6 in February. USD/CAD has gained 2.1% this week. The BoC kept interest rates on hold at 1.75% given that domestic economic conditions have now coupled to the downside with a bleak external picture. The caveat for the Canadian dollar is that rising oil prices could provide some support. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 CAD And AUD: Jumping Higher To Plunge Deeper - February 1, 2019 Swiss Franc Chart II-15CHF Technicals 1

CHF Technicals 1

CHF Technicals 1

Chart II-16CHF Technicals 2

CHF Technicals 2

CHF Technicals 2

Recent data in Switzerland have been negative: Annualized Q4 GDP growth missed analysts’ expectations by 50%, coming in at 0.2%. In addition, the retail sales contracted 0.4% year-on-year. Lastly, CPI was in line at 0.6%, but this is a far cry from the March 2018 peak. EUR/CHF has been flat this week. Overall, we are bullish EUR/CHF on a cyclical basis. Stabilization in global growth will make safe-haven currencies like the franc less attractive. In addition, the foreign direct investment and portfolio investment outflows from Switzerland should put more downward pressure on the franc. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Waiting For A Real Deal - December 7, 2018 Norwegian Krone Chart II-17NOK Technicals 1

NOK Technicals 1

NOK Technicals 1

Chart II-18NOK Technicals 2

NOK Technicals 2

NOK Technicals 2

Recent data in Norway have been mixed: Monthly unemployment rate fell to 2.5%, in line with expectations. However, the Q4 current account balance fell to 46.8 billion from 91.36 billion in Q3. The manufacturing PMI has been stable for a few months now, coming in at 56.3 for the month of February. USD/NOK increased by 2.2% this week. We are optimistic on the NOK on a structural basis, given the positive outlook for oil prices. Moreover, the NOK is undervalued and trading at a large discount to its long-term fair value. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Global Liquidity Trends Support The Dollar, But... - January 25, 2019 Swedish Krona Chart II-19SEK Technicals 1

SEK Technicals 1

SEK Technicals 1

Chart II-20SEK Technicals 2

SEK Technicals 2

SEK Technicals 2

Recent data in Sweden have been positive: Retail sales was in line with expectations at 0.8% month-on-month. However, annualized Q4 GDP growth was double expectations at 1.2%. The February manufacturing PMI also came in higher at 52.5. In addition, industrial production yearly growth came in higher at 3.4%. Lastly, the Q4 current account balance increased to 39.6 billion. USD/SEK increased by 2% this week. The SEK is still trading at a large discount to its long-term fair value. We remain bearish on USD/SEK on a structural basis as we see many signs pointing to a recovery in the Swedish economy, which is a tailwind for the Swedish krona. Report Links: Balance Of Payments Across The G10 - February 15, 2019 A Simple Attractiveness Ranking For Currencies - February 8, 2019 Global Liquidity Trends Support The Dollar, But... - January 25, 2019 Trades & Forecasts Forecast Summary Core Portfolio Tactical Trades Closed Trades

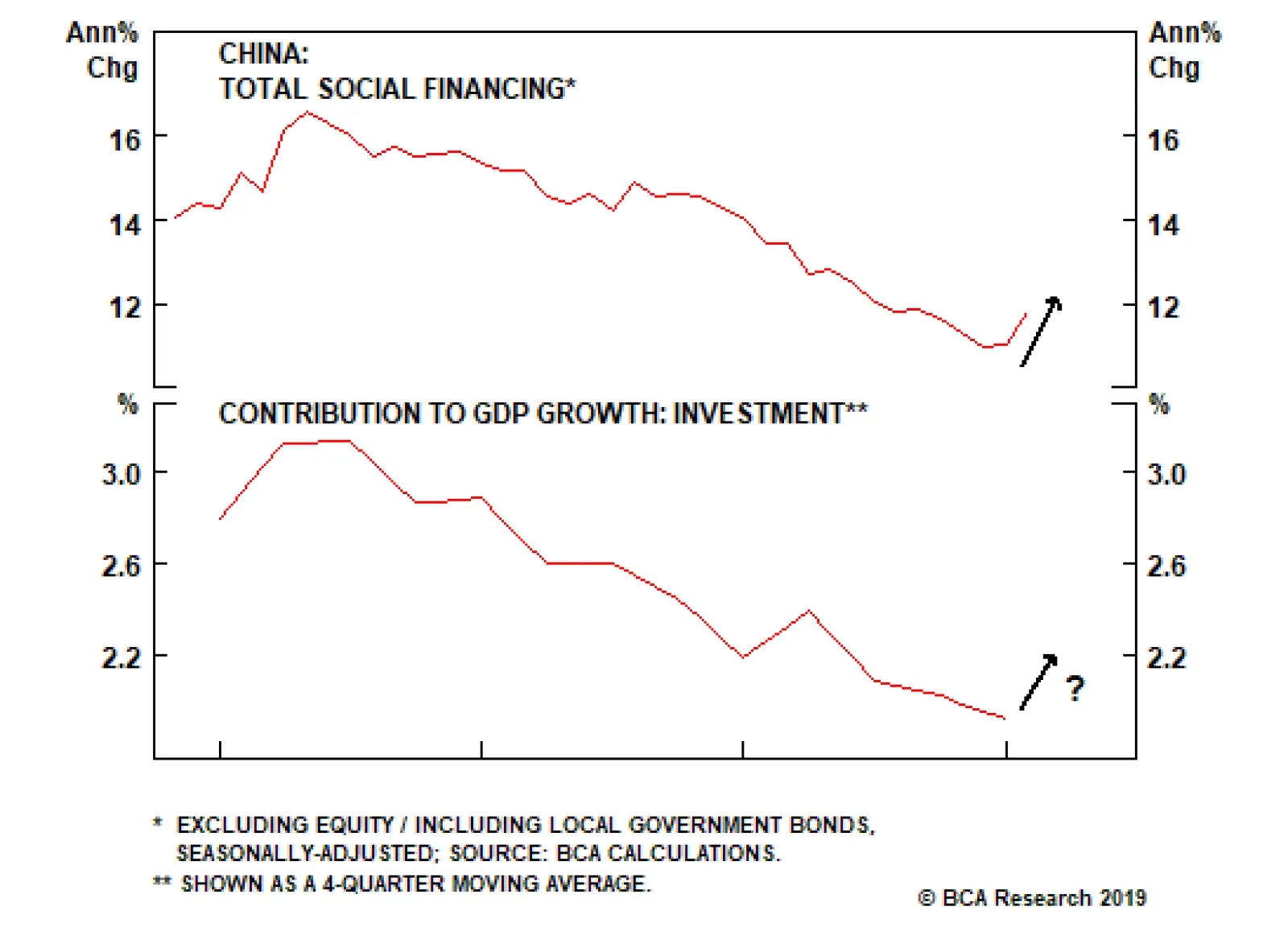

Fixed investment spending in China is generally financed through credit markets. The above chart shows that the contribution of investment spending to GDP growth has declined in tandem with decelerating credit growth. Chinese credit growth has typically…

Highlights Analysis on Indonesia is available below. EM financial markets have diverged from the global growth indicators they have historically correlated with. This raises doubts about the sustainability of this rally. In China, broad bank credit has not accelerated at all, while non-bank credit growth rose sharply in January. The lack of recovery in broad bank credit growth is corroborated by lingering sluggishness in broad money growth. This refutes widespread perception in the global investment community that Chinese banks have re-opened the credit spigots again. Feature The headline news has all been positive for emerging markets over the past two months: The Federal Reserve is going on hold, China is stimulating its economy, the U.S. and China are nearing a trade agreement and risk-on market dynamics are permeating worldwide. Nevertheless, EM stocks have failed to outperform the global equity benchmark (Chart I-1, top panel). Notably, EM relative equity performance rolled over in late December when global share prices bottomed. Chart I-1EM Stocks Have Underperformed DM Ones Since Late December

EM Stocks Have Underperformed DM Ones Since Late December

EM Stocks Have Underperformed DM Ones Since Late December

In absolute terms, EM equities have been attempting to break above their 200-day moving average, but have so far failed to do so decisively (Chart I-1, bottom panel). When a market struggles to break out or outperform amid favorable news flows and buoyant investor sentiment, the odds are that it is facing formidable headwinds under the surface, and is at risk of relapsing. We sense EM currently fits this profile. Needless to say, investor consensus is very bullish on EM, and dominated by the above-mentioned narrative, specifically the Fed turning dovish and China stimulating, which is reminiscent of 2016 when EM staged a cyclical rally. Consequently, investors have rushed to pile into EM stocks and fixed-income. Chart I-2 illustrates that asset managers’ net holdings of EM ETF (EEM) futures have doubled since October 2018. Chart I-2Investor Consensus Is Very Bullish On EM

Investor Consensus Is Very Bullish On EM

Investor Consensus Is Very Bullish On EM

As of mid-February, EMs were by far the most overweight region within global equity portfolios, according to the most recent Bank of America/Merrill Lynch survey. The survey states that net 37% of global equity investors - who participated in the survey - were overweight EM. One of our clients that we met with on the road last week summed it up like this: “Investors have ‘recency bias’.” In other words, investors believe that 2019 will resemble 2016, and in turn have no appetite to bet against Chinese stimulus. We are in accord with this interpretation of investor behavior and the EM/China rally. Yet there are some noteworthy differences between today and 2016. First, in 2016, there was massive stimulus for China’s property market. At the time, the People’s Bank of China (PBoC) monetized the unsold housing stock in Tier-3 and -4 cities via its Pledged Supplementary Lending facility. At present, there is no stimulus for real estate. Second, by early 2016 EM profits had already contracted substantially. EM profits have yet to shrink in the current downtrend. Our thesis is that EM profits will contract this year for reasons we elaborated on in depth in our previous report, Mind The Time Gap. China’s credit and fiscal impulse leads EM/Chinese profits by about 12 months, and the recent improvement in this indicator, if sustained, suggests that a trough in EM/Chinese corporate earnings will only be reached in late 2019 (Chart I-3). Therefore, as EM profits shrink, investors will likely sell EM risk assets. Chart I-3EM Corporate Earnings Are Beginning To Contract

EM Corporate Earnings Are Beginning To Contract

EM Corporate Earnings Are Beginning To Contract

Altogether, these differences with 2016 make us reluctant to chase the current EM rally, and we continue to expect a meaningful reversal in EM risk assets in the months ahead. Monitoring Global Growth We maintain that EM is much more leveraged to global trade and China’s growth than to Fed policy. For a detailed discussion on this matter, please refer to EM: A Replay of 2016 or 2001? report from February 7, 2019. Therefore, the Fed’s dovish turn is not a sufficient reason to buy EM risk assets. To buy EM cyclically, we would need to change our outlook on global trade and Chinese imports. China influences the rest of the world via its imports. A closer look at the indicators that correlate with EM risk assets and commodities do not justify the recent EM rebound. In particular: The import sub-component of China’s NBS manufacturing PMI strongly correlates with EM share prices, excess returns in EM sovereign credit, and industrial metals prices and suggest that investors should fade this rebound (Chart I-4). Chart I-4EM Stocks, EM Credit Markets, As Well As Commodities Prices Are Driven By Chinese Imports

EM Stocks, EM Credit Markets, As Well As Commodities Prices Are Driven By Chinese Imports

EM Stocks, EM Credit Markets, As Well As Commodities Prices Are Driven By Chinese Imports

The Caixin manufacturing PMI for China was up in February, but the NBS manufacturing PMI fell. In turn, manufacturing PMI indexes in Korea, Taiwan, Japan and Singapore are all plunging, with several of them dropping well below the 50 boom-bust mark (Chart I-5). Chart I-5Asian Manufacturing Is Contracting

Asian Manufacturing Is Contracting

Asian Manufacturing Is Contracting

Korean, Taiwanese, Japanese and Singaporean shipments to China were shrinking in January, while their exports to the U.S. were resilient (Chart I-6). This confirms that global trade has been weak due to China, and that there are no signs of its reversal. Chart I-6Asian Exports To China And U.S.

Asian Exports To China And U.S

Asian Exports To China And U.S

Moreover, Korea released its February export data, and its aggregate outbound shipments are contracting (Chart I-7). Chart I-7Korean Exports: Deepening Contraction

Korean Exports: Deepening Contraction

Korean Exports: Deepening Contraction

Further, China’s container freight index – the price to ship containers – has rolled over again after picking-up late last year due to front-loading of shipments to the U.S. which were induced by the U.S. import tariffs. This signals ongoing weakness in global demand, and does not justify the latest rebound in EM financial markets in general and currencies in particular (Chart I-8). Chart I-8Global Trade Is A Risk To EM Currencies

Global Trade Is A Risk To EM Currencies

Global Trade Is A Risk To EM Currencies

Finally, even in the U.S. where manufacturing has been the most resilient globally, the odds point to notable weakness in this sector. Specifically, the continuous underperformance of U.S. high-beta industrial stocks to U.S. overall industrials beckons a further slowdown in American manufacturing (Chart I-9). Chart I-9U.S. Manufacturing Is In A Soft Spot

U.S. Manufacturing Is In A Soft Spot

U.S. Manufacturing Is In A Soft Spot

Bottom Line: Although financial markets are forward-looking, the recent rally has been too fast and has already gone too far. This has created conditions for a material setback as global/China growth will continue to disappoint in the months ahead. China: Credit Versus Money Growth We have been receiving questions from clients as to whether investors should heed to the message from China’s money or credit data, given they are presently sending contradictory messages (Chart I-10). Chart I-10China: Narrow, Broad Money, And Aggregate Credit

China: Narrow, Broad Money, And Aggregate Credit

China: Narrow, Broad Money, And Aggregate Credit

Even though narrow money (M1) has historically been an excellent indicator for China/EM business cycles, the most recent (January) print – M1 annual growth rate registered a record low – was distorted due to technical/seasonal factors, and should be ignored. Specifically, deposits by enterprises plunged in January and household deposits surged as companies paid out bonuses to employees in late January ahead of the Chinese New Year that began on February 5 (Chart I-11). Provided enterprise demand deposits are in M1 but household demand deposits are a part of M2, M1 was artificially depressed in January. It will rebound in February. Chart I-11China: Technical Reasons For M1 Plunge In January

China: Technical Reasons For M1 Plunge In January

China: Technical Reasons For M1 Plunge In January

Broad money provides a more comprehensive picture of money creation in China. As such, it is more relevant to compare broad money with aggregate credit. To compute aggregate credit, we add outstanding central and local government bonds to Total Social Financing (TSF). Chart I-12 illustrates the latest improvement in aggregate credit is not confirmed by either the PBoC’s broad money measure, M2, or our measure, M3 (M3 = M2 plus other deposits plus banks’ other liabilities excluding bonds). We created this M3 measure of broad money supply because in our opinion, M2 has been underestimating the extent of money creation in China in recent years due to financial engineering. Chart I-12The Recent Uptick In Aggregate Credit Is Not Confirmed By Broad Money

The Recent Uptick In Aggregate Credit Is Not Confirmed By Broad Money

The Recent Uptick In Aggregate Credit Is Not Confirmed By Broad Money

As discussed in Box I-1 on pages 12-13, lending or purchasing of securities by banks simultaneously creates money. Therefore, bank broad credit acceleration should be mirrored in a broad money upturn. Does the lack of revival in broad money mean the latest uptick in aggregate credit data has been driven by non-bank credit? Our analysis suggests yes – non-bank credit is responsible for the strong rise in the aggregate credit numbers in January. We deconstructed aggregate credit into broad bank credit and non-bank credit (Diagram I-1). Chart I-13 illustrates that broad bank credit has not accelerated at all, while non-bank credit growth rose in January.

Chart I-

Chart I-13China: Recent Credit Acceleration Is Due To Non-Bank Credit

China: Recent Credit Acceleration Is Due To Non-Bank Credit

China: Recent Credit Acceleration Is Due To Non-Bank Credit

The lack of recovery in broad bank credit growth is corroborated by lingering sluggishness in broad money (both M2 and M3) growth (Chart I-14). Chart I-14Broad Bank Credit Is Consistent With Broad Money (As It Should Be)

Broad Bank Credit Is Consistent With Broad Money (As It Should Be)

Broad Bank Credit Is Consistent With Broad Money (As It Should Be)

Consequently, this refutes the widespread perception in the global investment community that Chinese banks have re-opened the credit spigots. Chart I-15demonstrates the annual growth rate of each component of broad bank credit. While mainland banks’ loan growth to enterprises has accelerated, their lending to non-bank financial institutions has continued to shrink. Chart I-15Broad Bank Credit And Its Components

Broad Bank Credit And Its Components

Broad Bank Credit And Its Components