Economic Growth

September nonfarm payrolls grew by 254 thousand, from 155 thousand in August, handily exceeding expectations of 150 thousand. Pro-cyclical manufacturing jobs declined by a lower-than-anticipated 7 thousand, while leisure and hospitality, as well as…

The S&P Global Canada Manufacturing PMI improved from 49.5 to 50.4 in September, breaking a 17-month contraction streak. It corroborated solid broad-based retail sales growth in July and August. Confidence in the outlook also improved. That said, we…

The JPM Global manufacturing PMI declined at an accelerating pace in September (49.6 to 48.8). Moreover, international trade flows deteriorated notably with the new export orders component falling from 48.4 to 47.5. A sector breakdown underscores broad-based…

The prospects of Fed rate cuts powered the S&P 500 Real Estate index’s rally. Real estate was the best-performing sector in Q3, outperforming the S&P 500 by nearly 12%. Can this sector pursue its lead now that expectations of monetary easing are…

The ISM manufacturing PMI remained constant in September at 47.2, against expectations of a slower pace of decline and extending a six-month contraction streak. Measures of production and domestic demand decelerated at a notably slower pace while foreign…

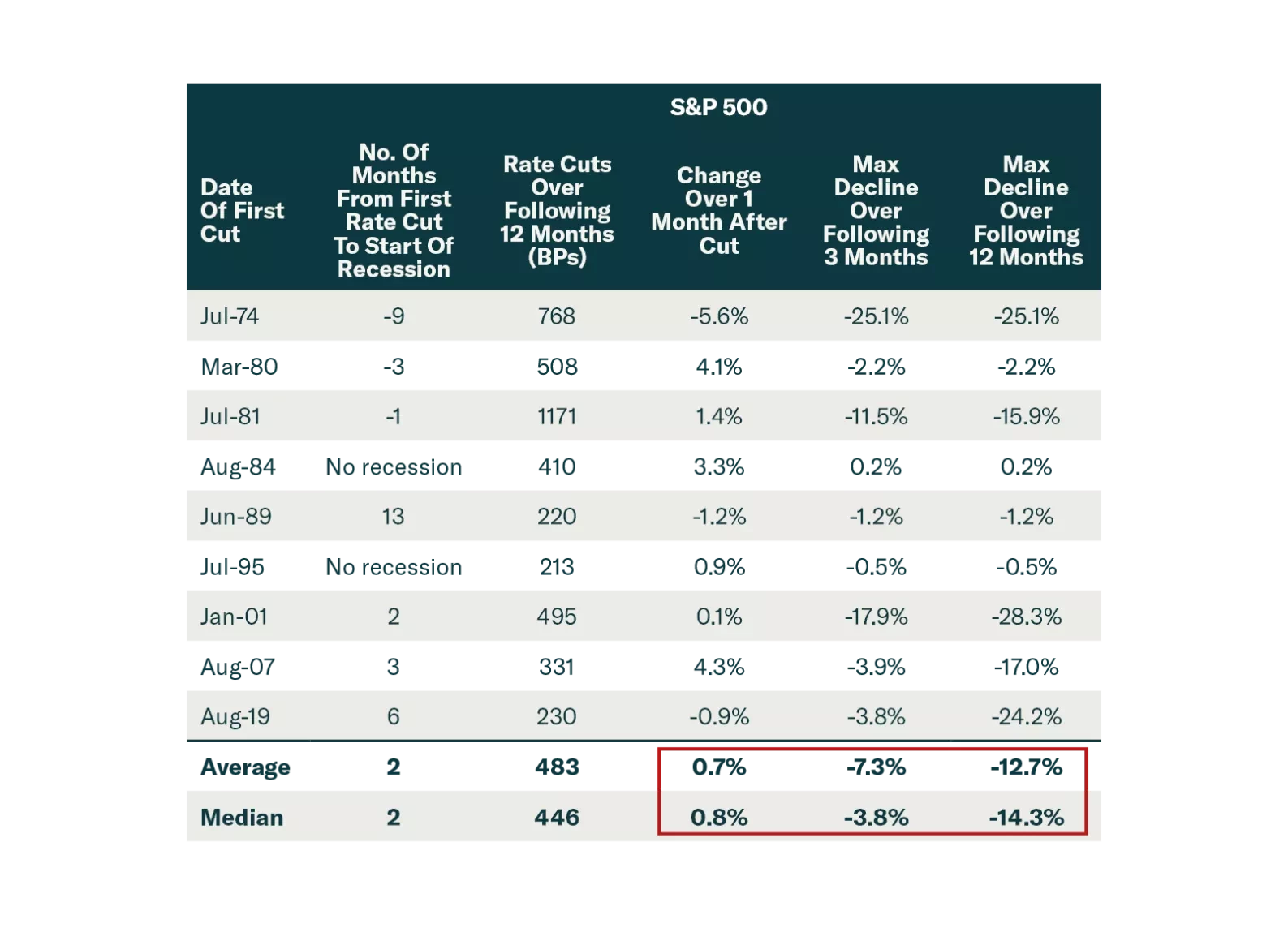

The market got excited by the 50 bps Fed cut and China stimulus. But these are a recognition that economies are slowing significantly. Stocks often rally after the first Fed cut, before falling sharply. Investors should stay defensive.

Preliminary estimates suggested that US durable goods orders stagnated in August after having surged 9.9% m/m in July, and beating expectations they would decline. Excluding the volatile transportation component, however, durable goods grew a robust 0.5%. …

Our expectation that a looming US recession will morph into a global recession remains intact. US monetary easing will only take effect with a lag and current deteriorating economic conditions are the product of past easing. Meanwhile, China’s…

According to BCA Research’s Emerging Market Strategy service, the monetary and fiscal policies announced last week are unlikely to produce a meaningful business cycle recovery in China. Below are actions the authorities need to undertake for our colleagues to…

US nominal personal income growth decelerated to a 0.2% pace in August, from 0.3% in July, missing expectations that it would accelerate. Nominal personal spending also disappointed, growing at a slower 0.2% pace from 0.5%. In real terms, spending barely…