Economic Growth

The Fed started its easing cycle with a bang, cutting the policy rate by 50 basis points in September, above consensus expectations but in line with odds embedded in the futures and OIS curves. Our US Bond strategists had highlighted it is unusual for the…

US retail sales grew 0.1% m/m in August and beat expectations of a 0.2% monthly contraction. The positive surprise seemingly spurred equity market gains on Tuesday morning. However, details do not paint as rosy a picture as the headline number…

The ZEW survey of both German business expectations and current situation largely disappointed in September, decreasing by 15.6 points to 3.6 and by 7.2 points to -84.5, respectively. The ZEW survey of expectations for the broader Eurozone also fell…

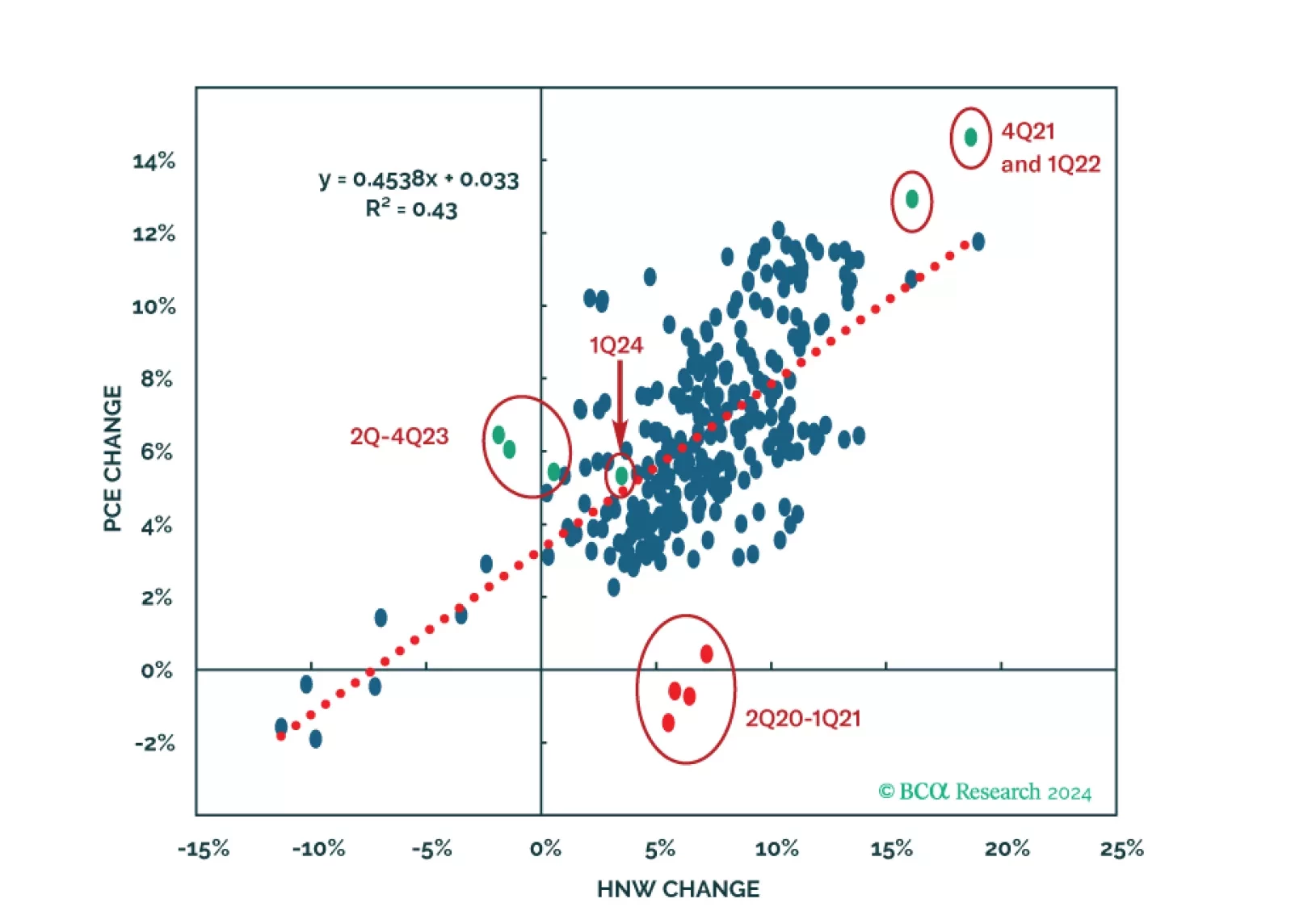

This Special Report examines the post-pandemic evolution of consumption growth, relative equity sector and subindustry performance and recent commentary from consumer-facing companies to assess the likelihood that softer spending among lower-income households will spread to middle- and upper-income households.

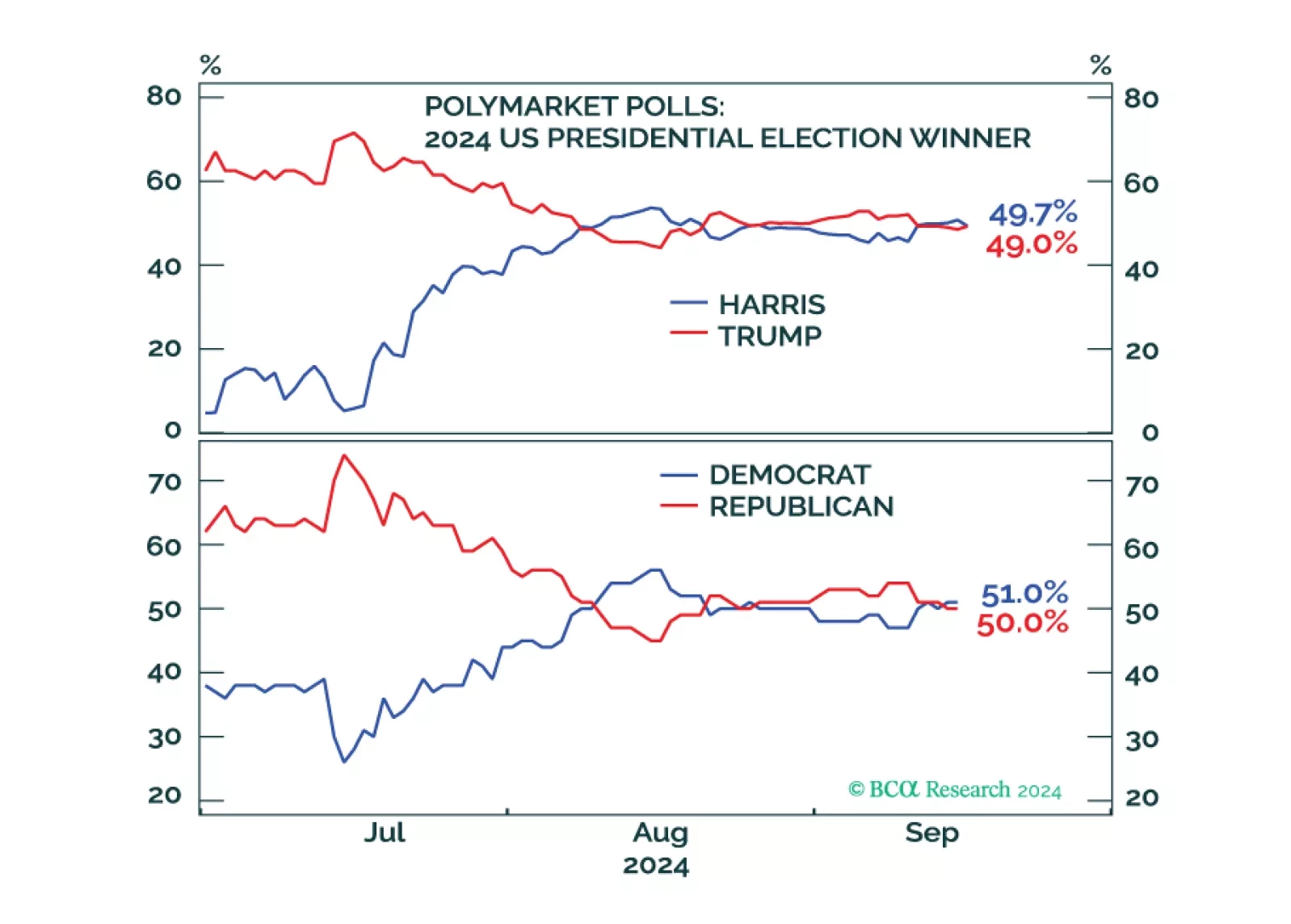

Investors should de-risk tactically in expectation of shocks and surprises ahead of the US election and an uncertain aftermath. Democratic victory with a gridlocked Congress is our base case but would bring minor tax hikes and nuclear brinksmanship with Russia. A Republican single-party sweep offers huge tax cuts but also a global trade war. Recession looms regardless.

The timeliest of the regional Fed manufacturing surveys sent a positive signal about the state of US manufacturing activity in September. The Empire State manufacturing general business conditions index surprised positively. It improved markedly from -4.7…

The Chinese economic data in its totality was uninspiring in August. Industrial production and retail sales growth decelerated year-on-year and corroborate the message from August’s import and credit growth data that domestic demand remains lackluster.…

Trade data from small open economies act as a bellwether for global growth developments. In August, Korean exports expanded by 11.4% y/y in USD and 5.7% y/y in KRW terms, marking their eleventh and eighth consecutive month of expansion, respectively.…

Investors are pricing in a soft landing in the US. Notably, we noted that pro-cyclical assets topped the performance ranking in August. At the same time, the S&P 500 is currently trading only 1% below its all-time highs. However, investors are…

Subdued demand for credit among Chinese private-sector businesses and households persisted through August. Outstanding loan growth decelerated from 8.7% y/y to 8.5%. Moreover, M1’s contraction deepened, from 6.6% to 7.3%. The lackluster appetite for…