Economic Growth

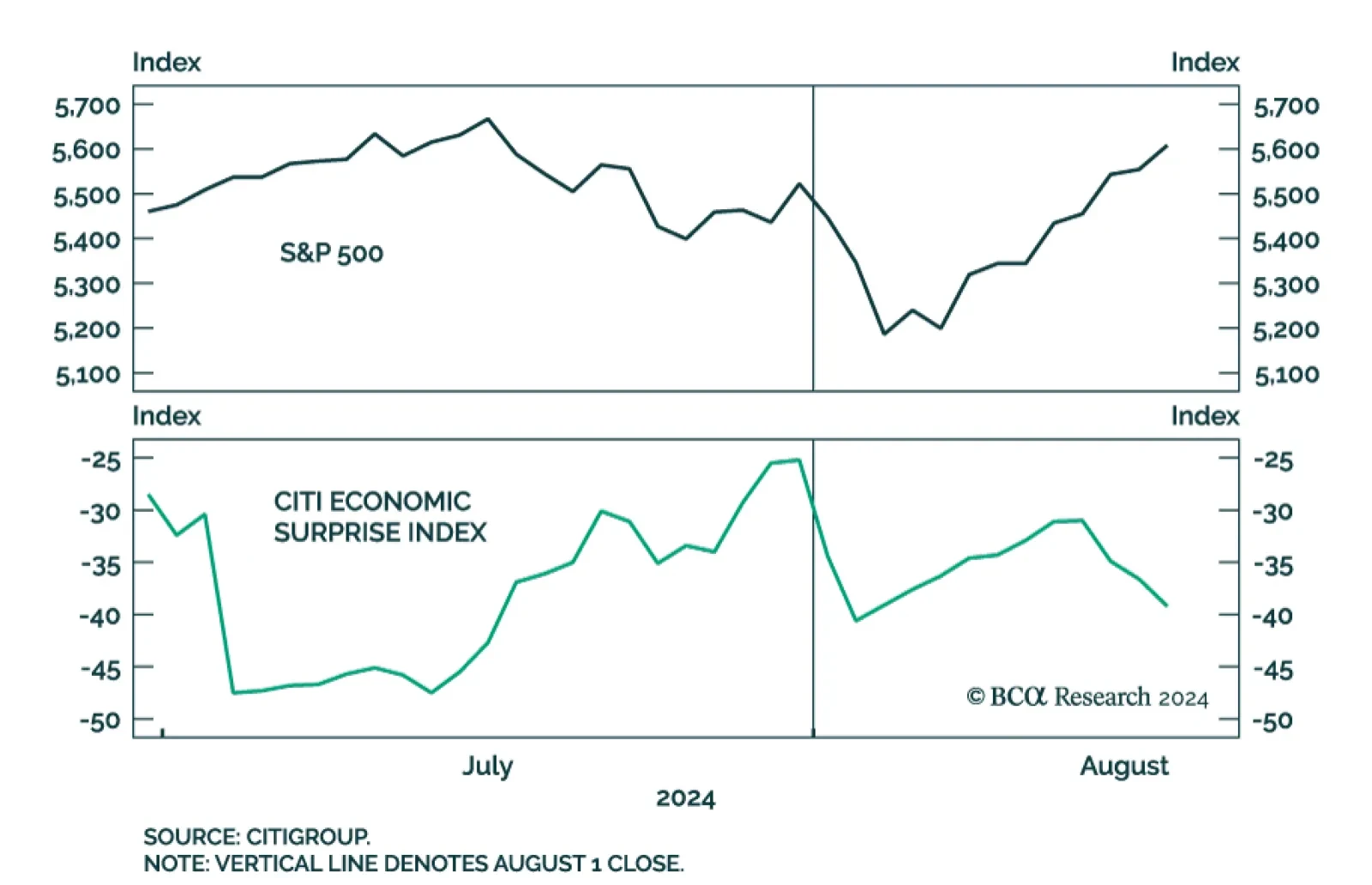

It didn't take long for markets to utterly shrug off the surprise rise in July's unemployment rate. On Tuesday, the S&P 500 closed higher than it was the day before the July Employment Situation report was released. The Russell 2000 gained 5.2% since…

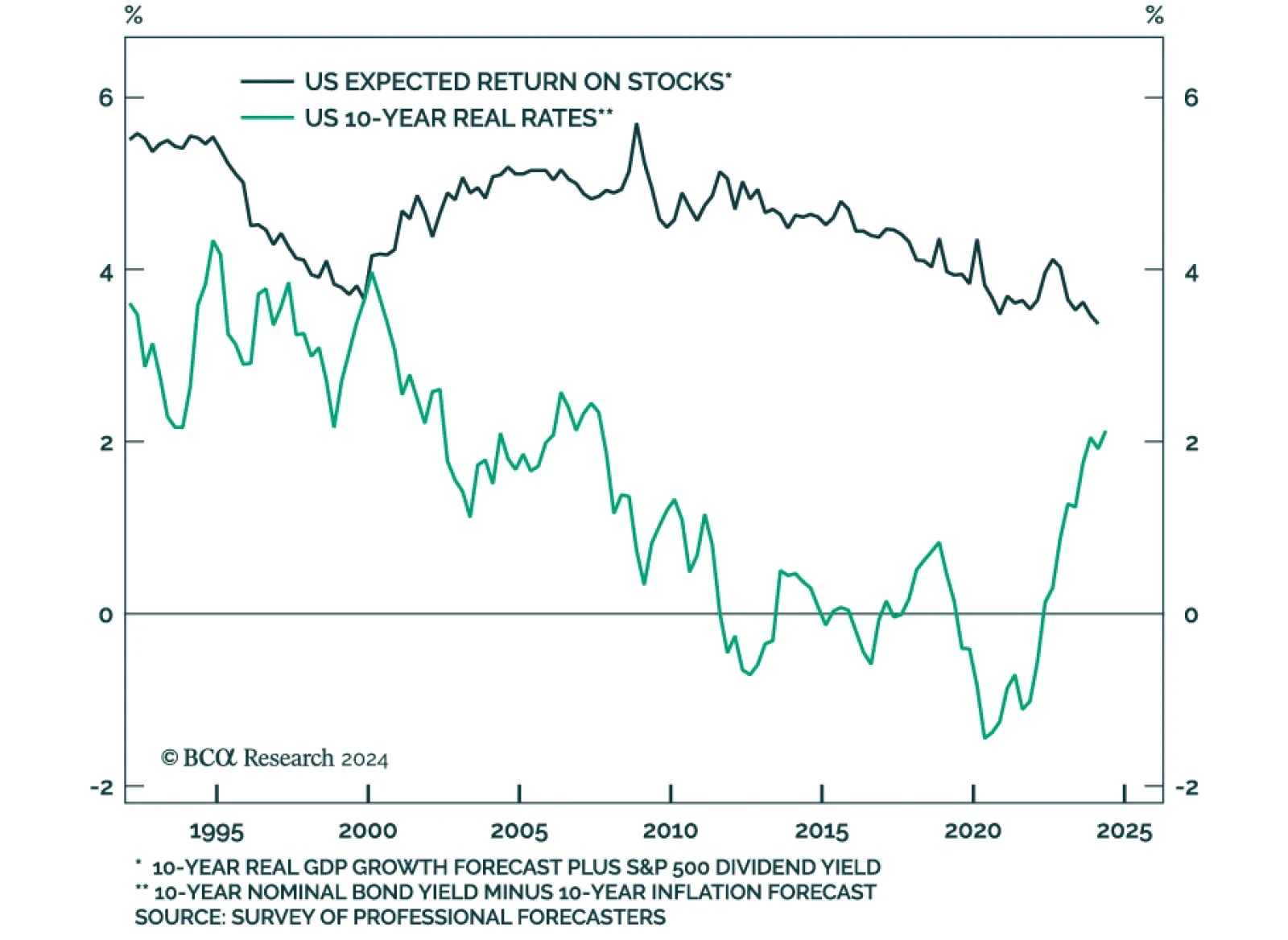

According to BCA Research’s US Investment Strategy and US Bond Strategy services, the drivers of the structural downtrend in real interest rates include: demographic trends (declining fertility rates, longer life expectancy and a rising dependency…

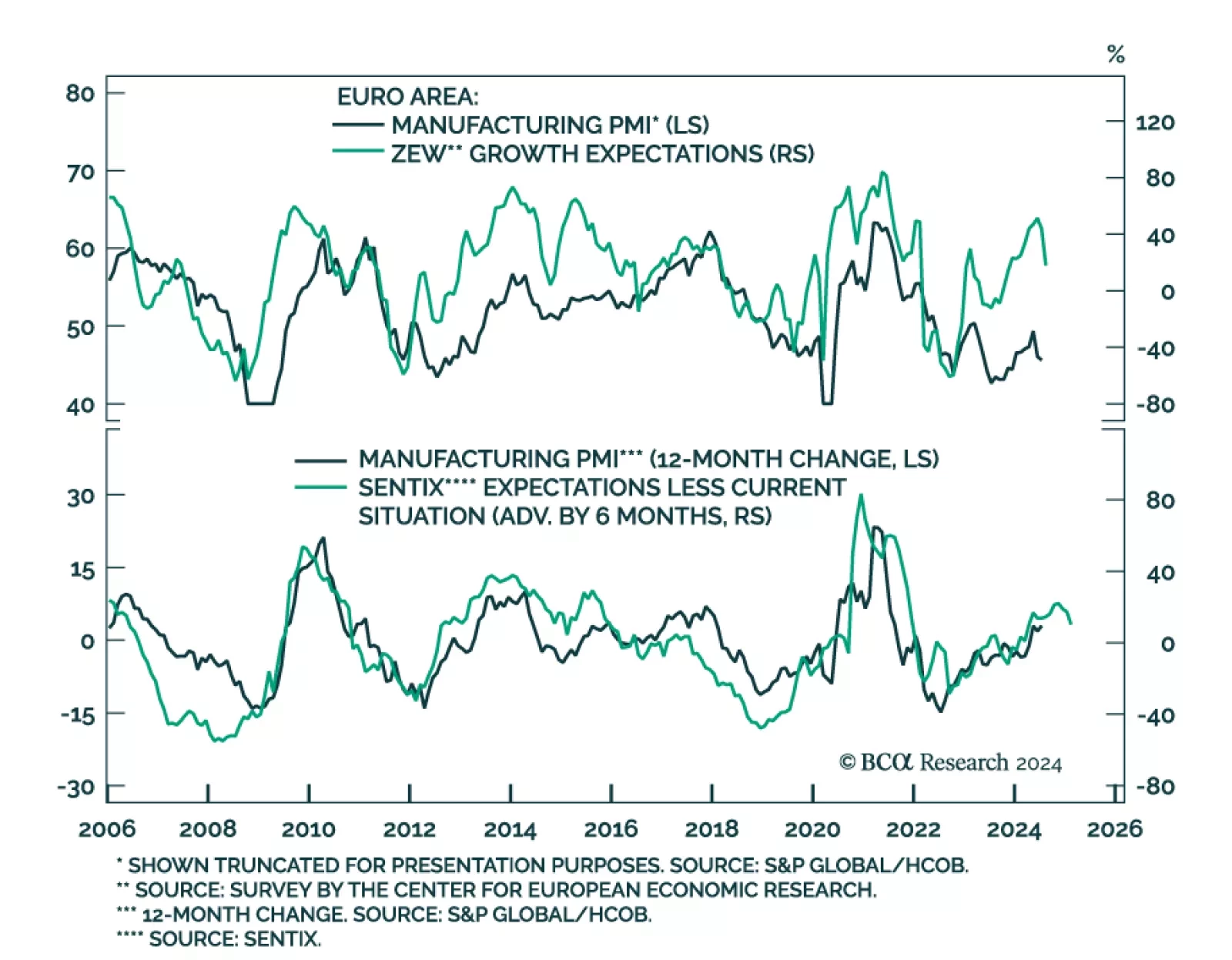

The ZEW survey of Eurozone business expectations decreased by a whopping 25.8 points to 17.9 in August. Notably, expectations for Germany’s current situation disappointed, worsening from an already depressed -68.9 level to -77.3, and expectations of future…

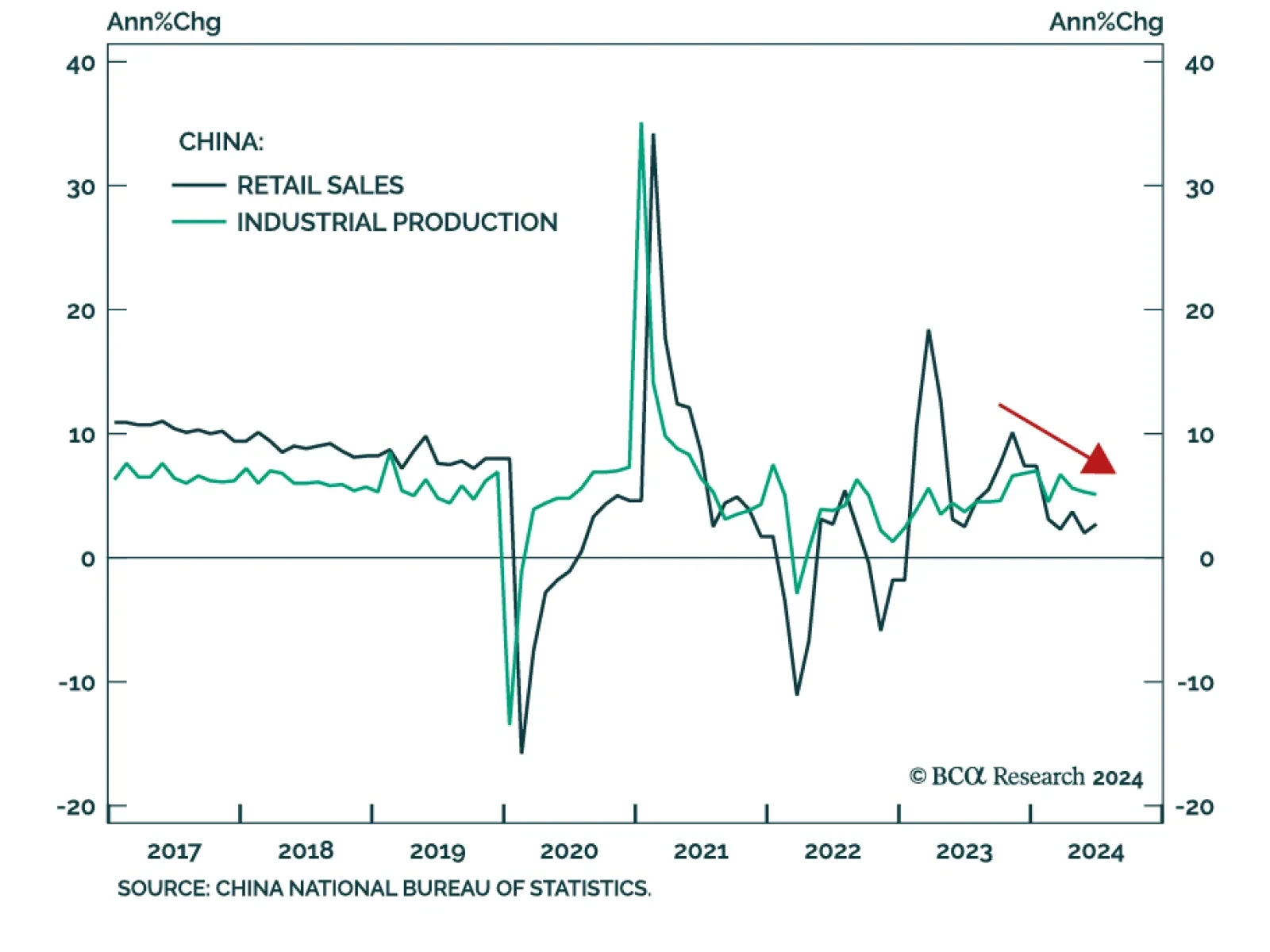

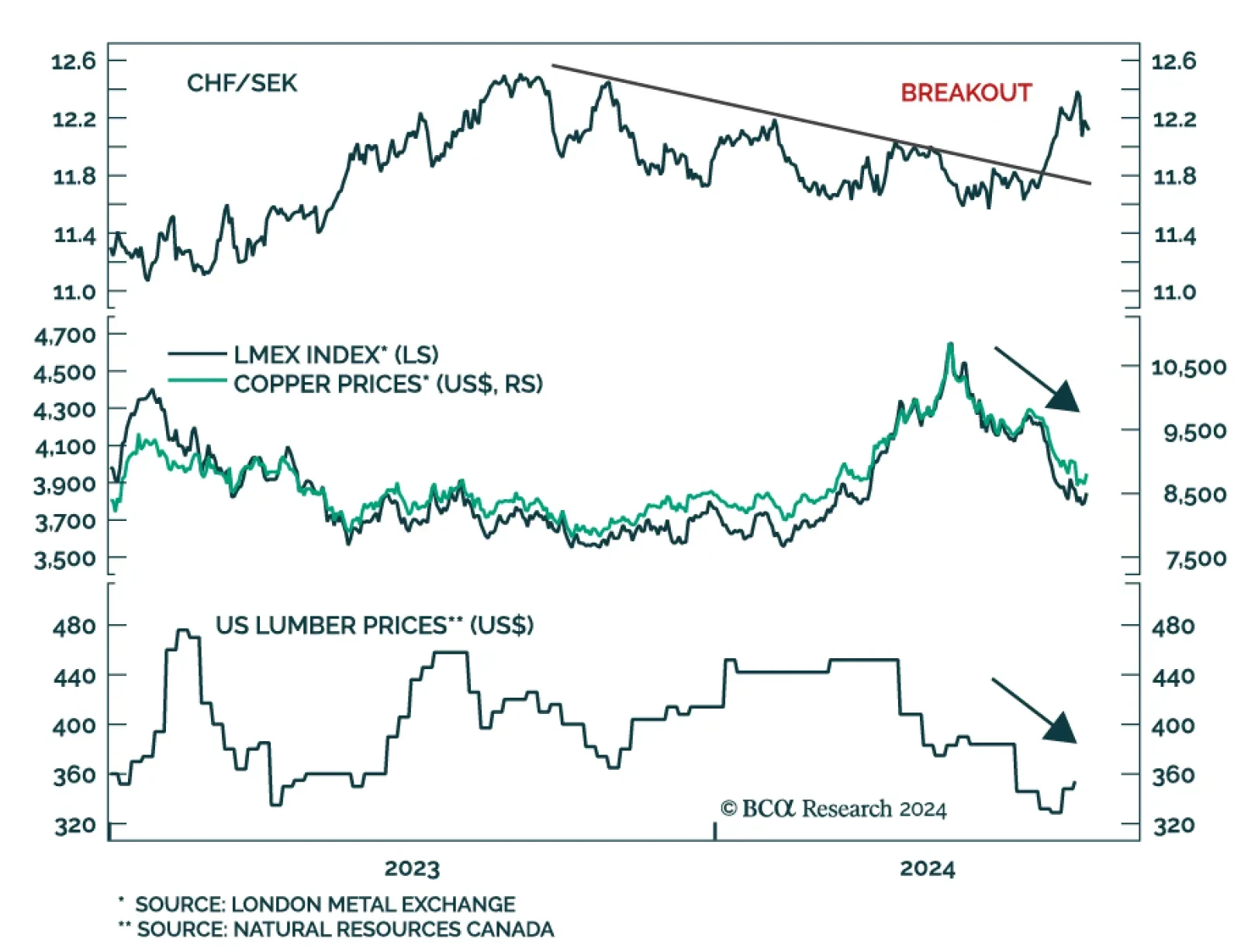

China’s economic malaise extended through the month of July. The contraction in property investment worsened (-10.2% YTD y/y) and disappointed expectations of a slower pace of decline. Residential property sales remained dismal (-25.9% YTD y/y). Industrial…

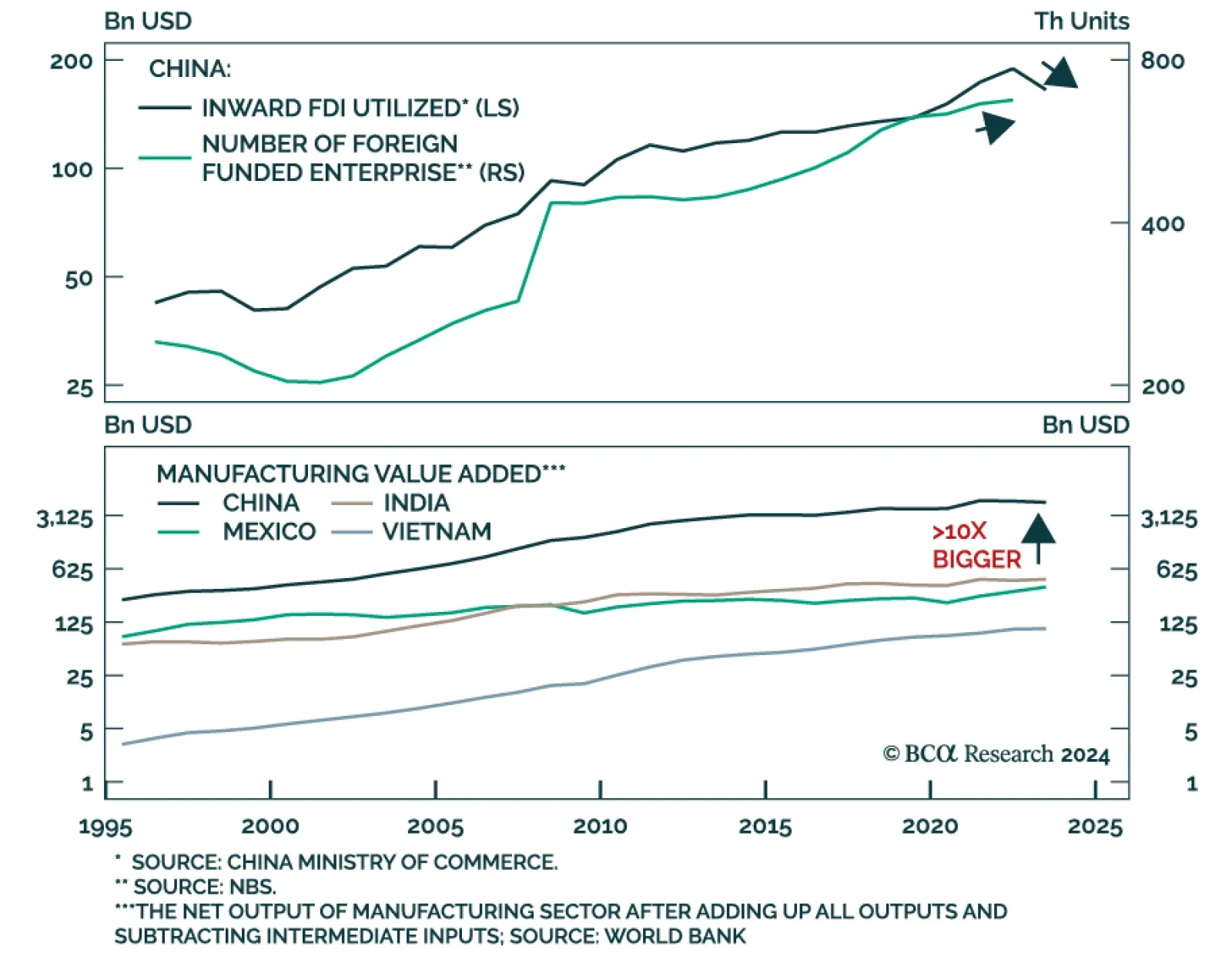

"There's no supply chain in the world that's more critical to us than China." — Tim Cook, CEO of Apple, March 2024 According to BCA Research’s China Investment Strategy and Emerging Market Strategy services, while high-profile multinational companies…

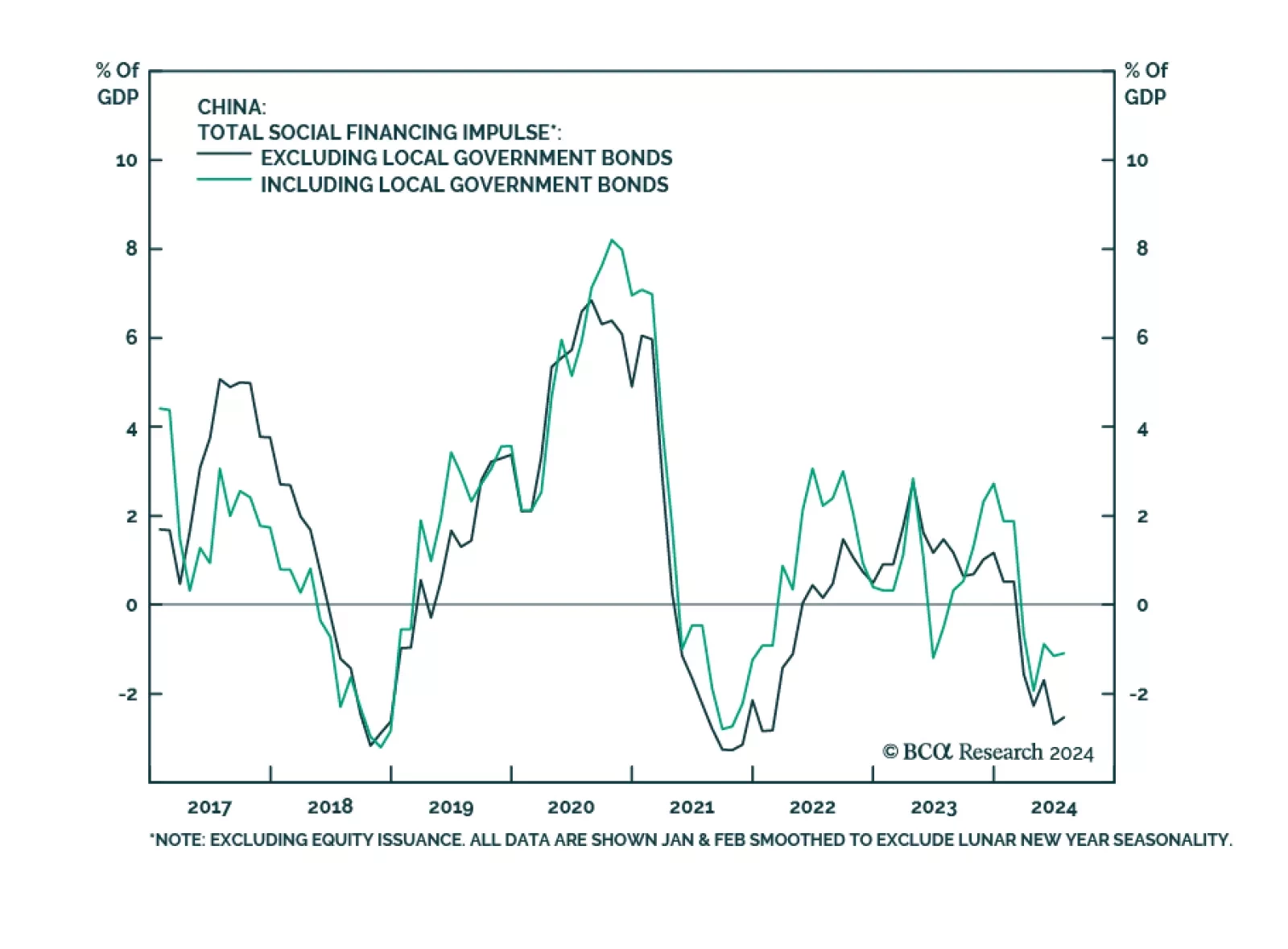

Subdued demand for credit among Chinese private-sector businesses and households persisted through July. Aggregate financing missed expectations, growing CNY 0.8bn to CNY 18.9bn in July on a YTD basis. New loans grew CNY 0.2bn to CNY 13.5bn, below the CNY…

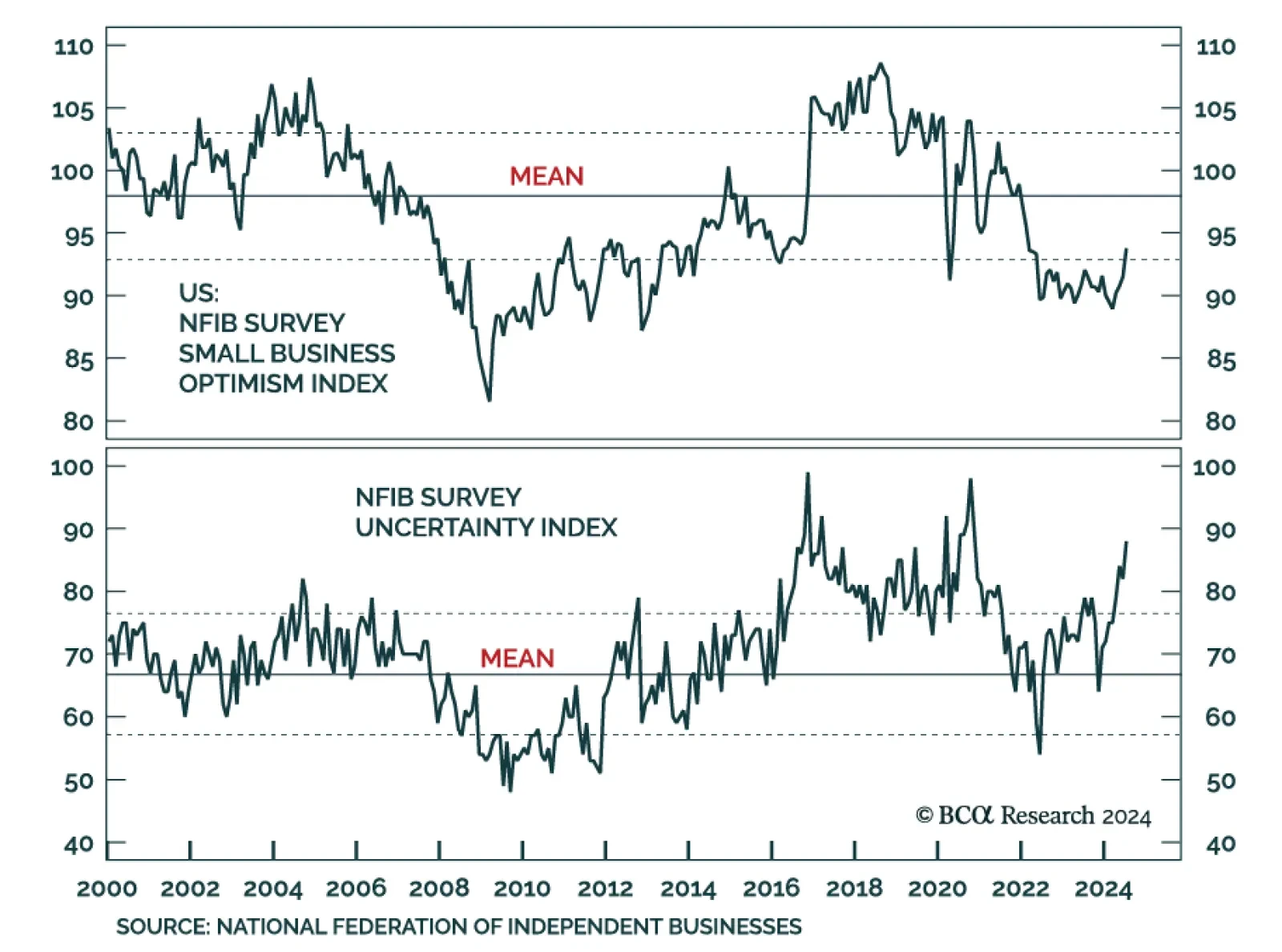

Tuesday morning’s NFIB Small Business Survey release surprised to the upside. The Small Business Optimism Index increased to 93.7 from 91.5, above expectations of remaining flat. The July reading was the highest since February 2022, the last release before…

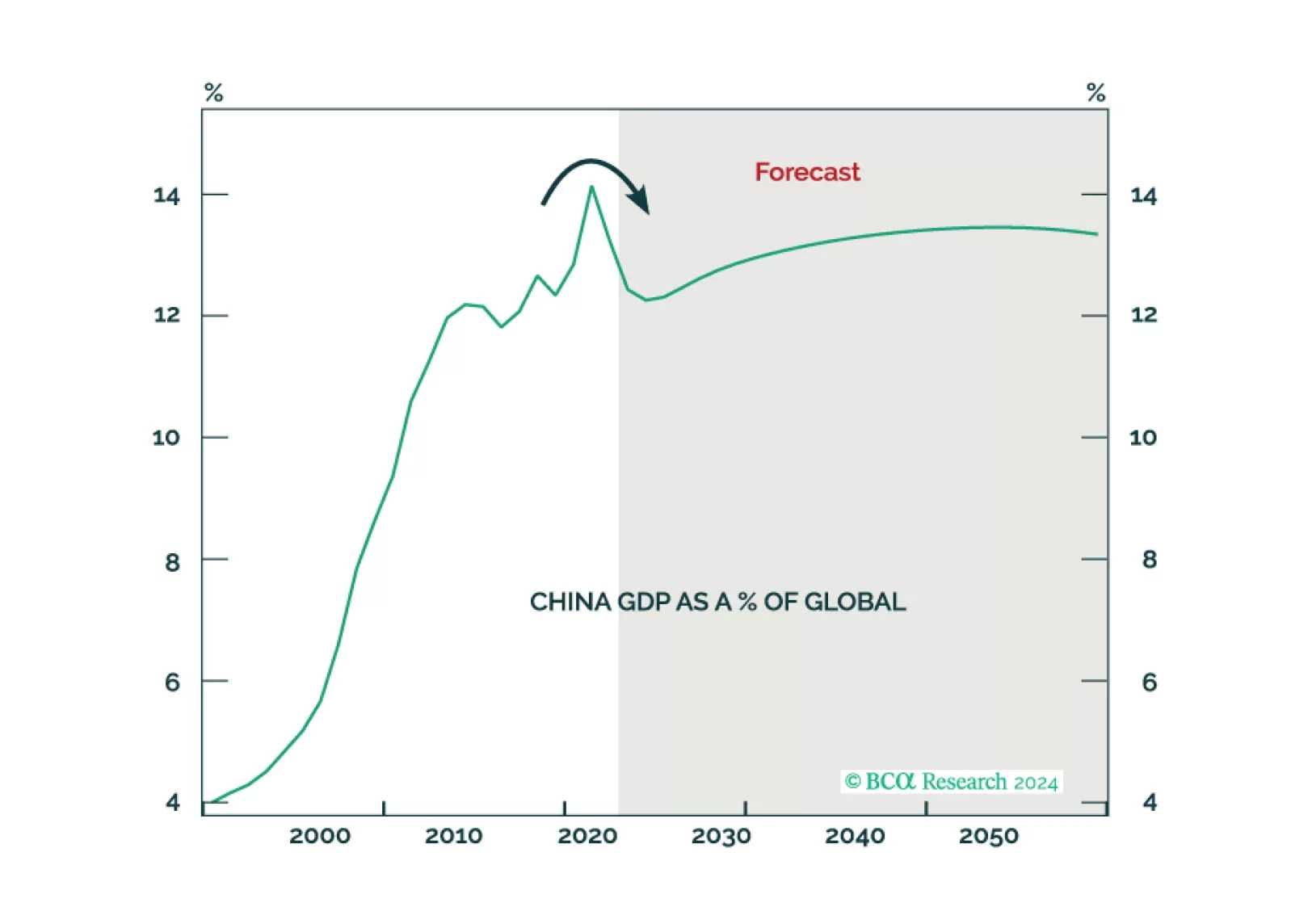

China missed the chance to change course on economic policy and now it faces rising social instability and western protectionism. This policy approach implies it is not afraid of escalating strategic conflicts in East Asia. Investors should continue to underweight Greater Chinese assets. Any US-China détente will come later rather than sooner.

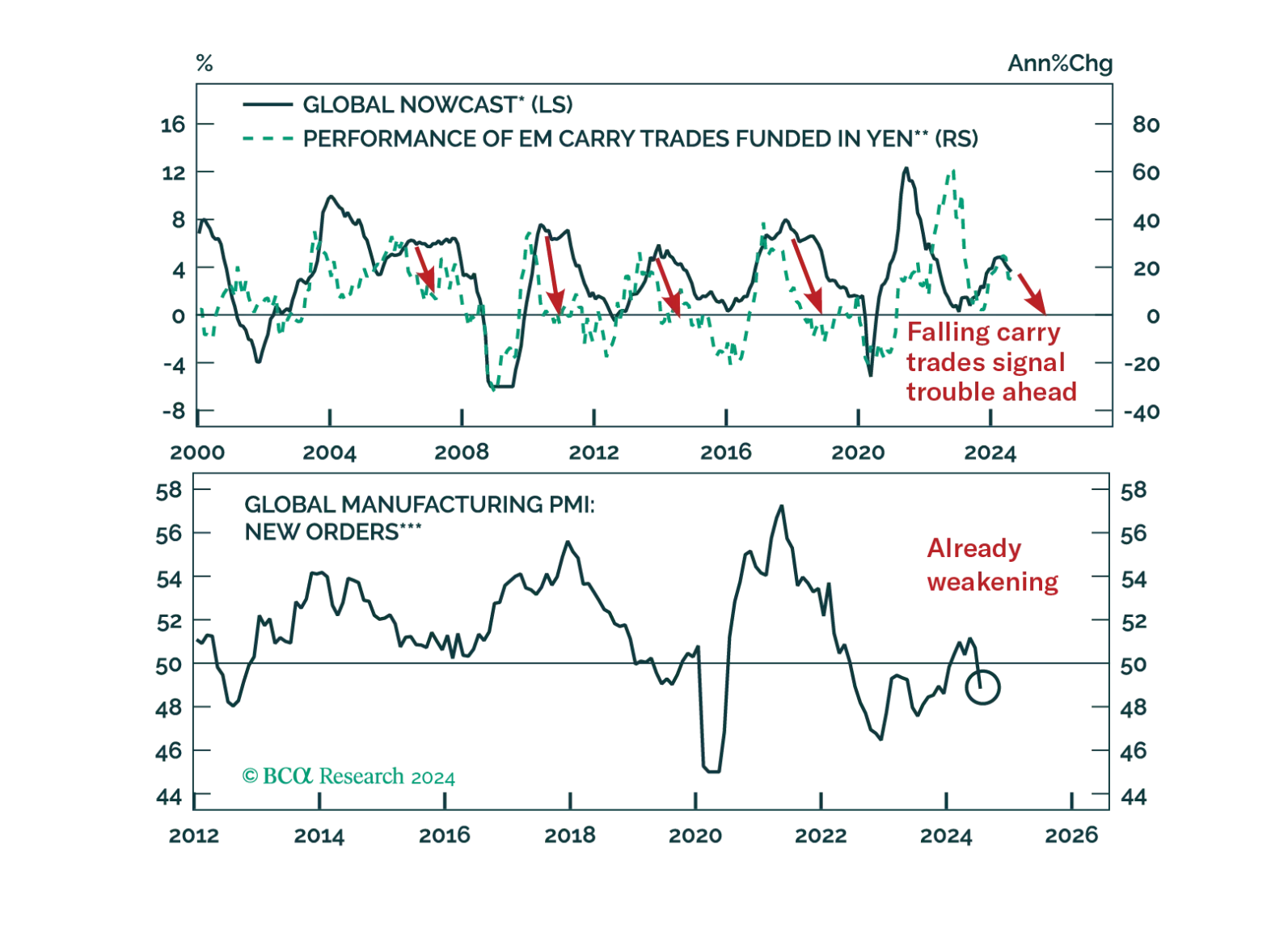

Regular readers are familiar with our expectation that the stabilization in global growth this year will be fleeting. The US has been the main source of demand in this cycle. We view the latest string of US employment data as further evidence the US…

The unwind of yen carry trades caused violent tremors across the globe. Was this shock a one-off event or the prelude to more troubles?