Economic Growth

The US economy remains on a path towards a recession, most likely starting in late 2024 or early 2025. For now, investors should maintain a benchmark allocation to equities, but employ a barbell strategy of overweighting defensives and materials.

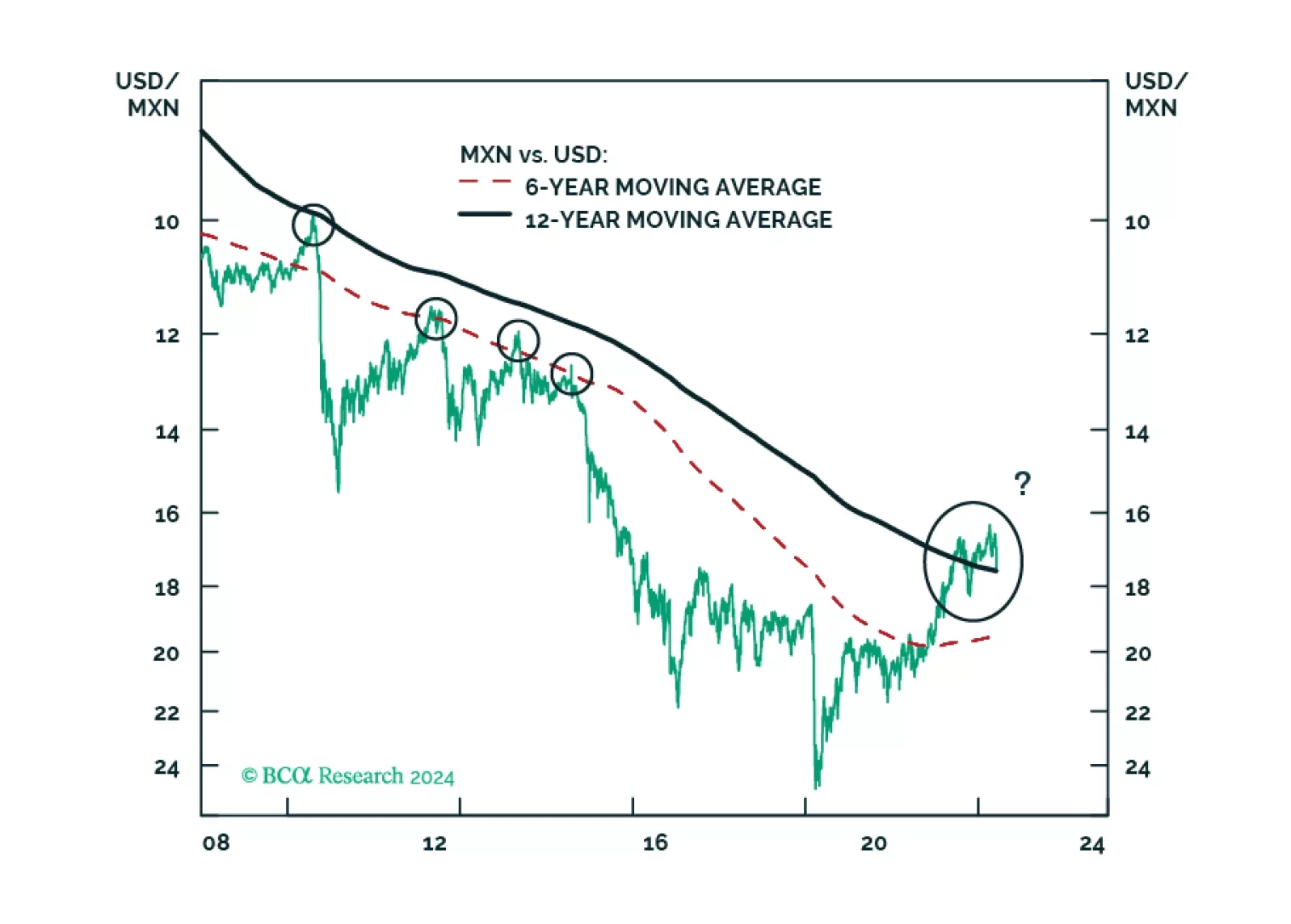

MORENA has once again swept the Mexican election: Claudia Sheinbaum will be president, with little to no constraint in Congress. All in all, Mexican politics will remain stable and overall supportive of markets. In the medium term, fiscal spending will return to conservatism and the constitutional reforms will lead to mixed fiscal and economic repercussions. In the long term, however, fiscal and institutional risks will rise. We advise investors to remain overweight Mexican risk assets relative to EM in cyclical and structural time horizons, but prepare for Mexican markets to sell off in absolute and relative terms in the next couple of months.

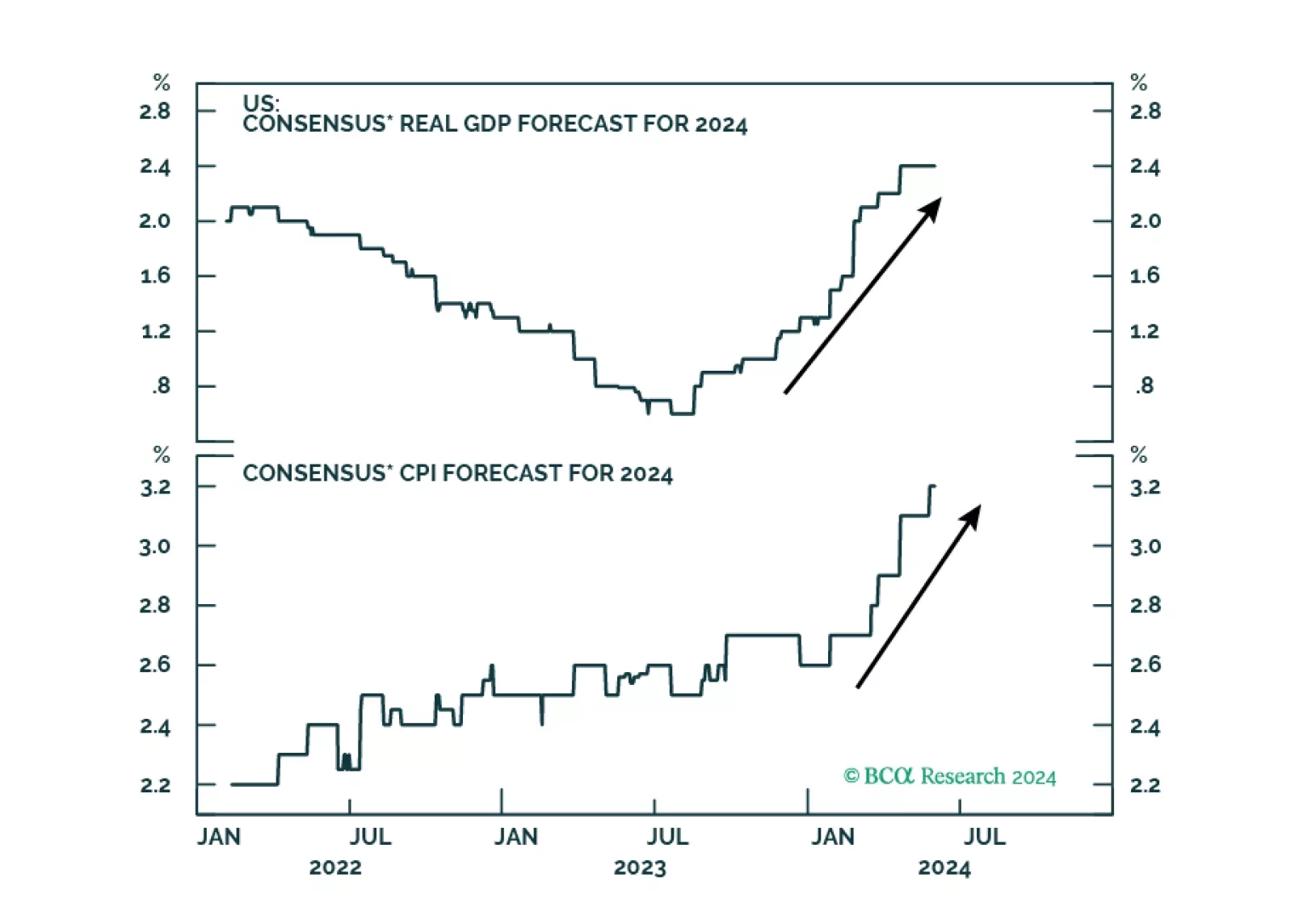

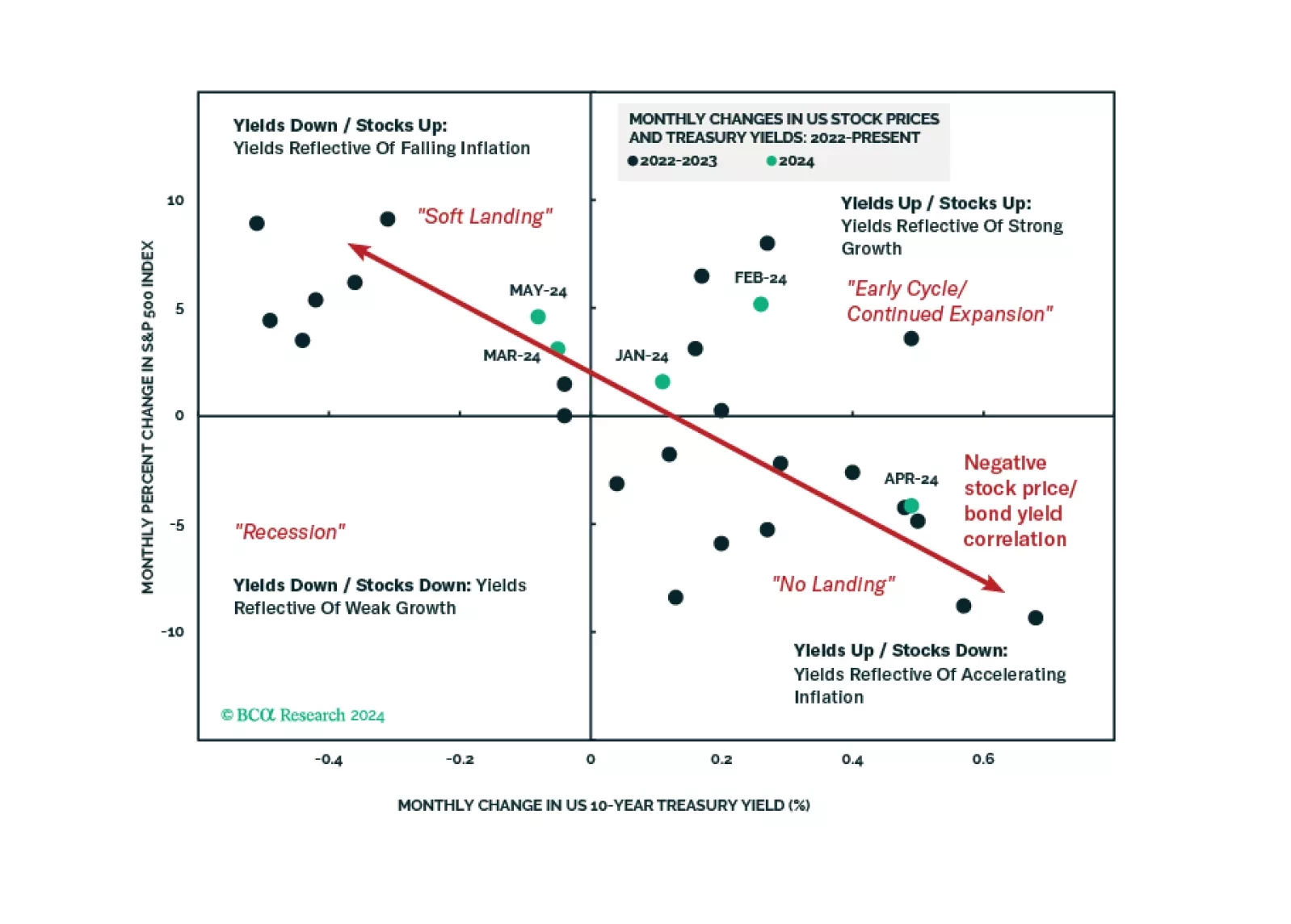

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.

In Section I, we argue that global investors have been lulled into a false sense of security concerning the resiliency of the US economy. Tight monetary policy means that something must change for a recession to be avoided, and developed market rates cuts will likely be too modest and come too late to save the day. Nimble investors or those highly sensitive to tracking error should not be underweight stocks over the coming 3-6 months. Over a 6-12 month time horizon, we continue to recommend that investors remain underweight global equities versus US$-hedged long-maturity developed market government bonds. Section II is a guest report written by Martin Barnes, BCA’s former Chief Economist. Martin revisits the idea of the Debt Supercycle and discusses how its true end may emerge in response to a fiscal crisis in the US over the coming few years.