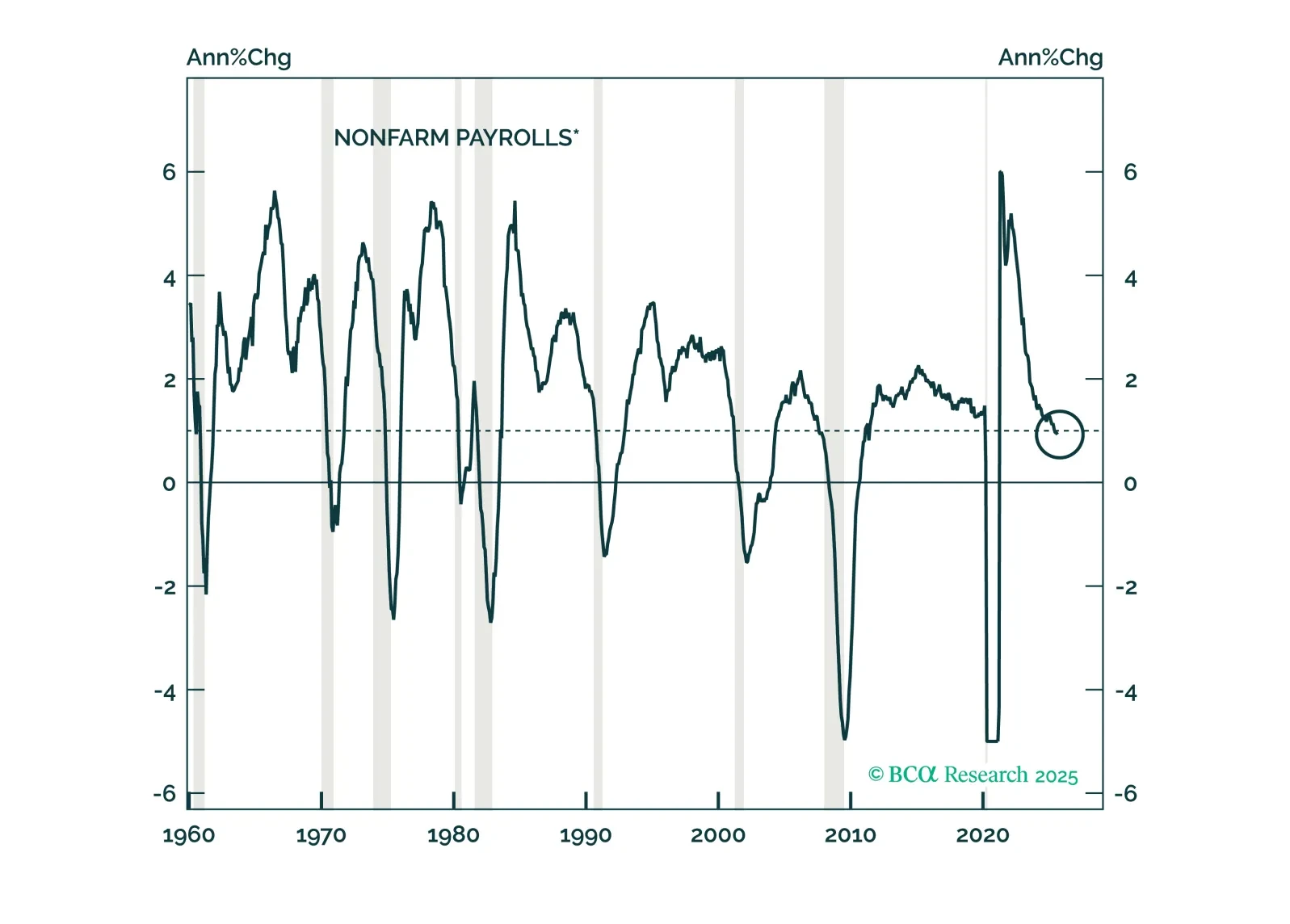

Economic Growth

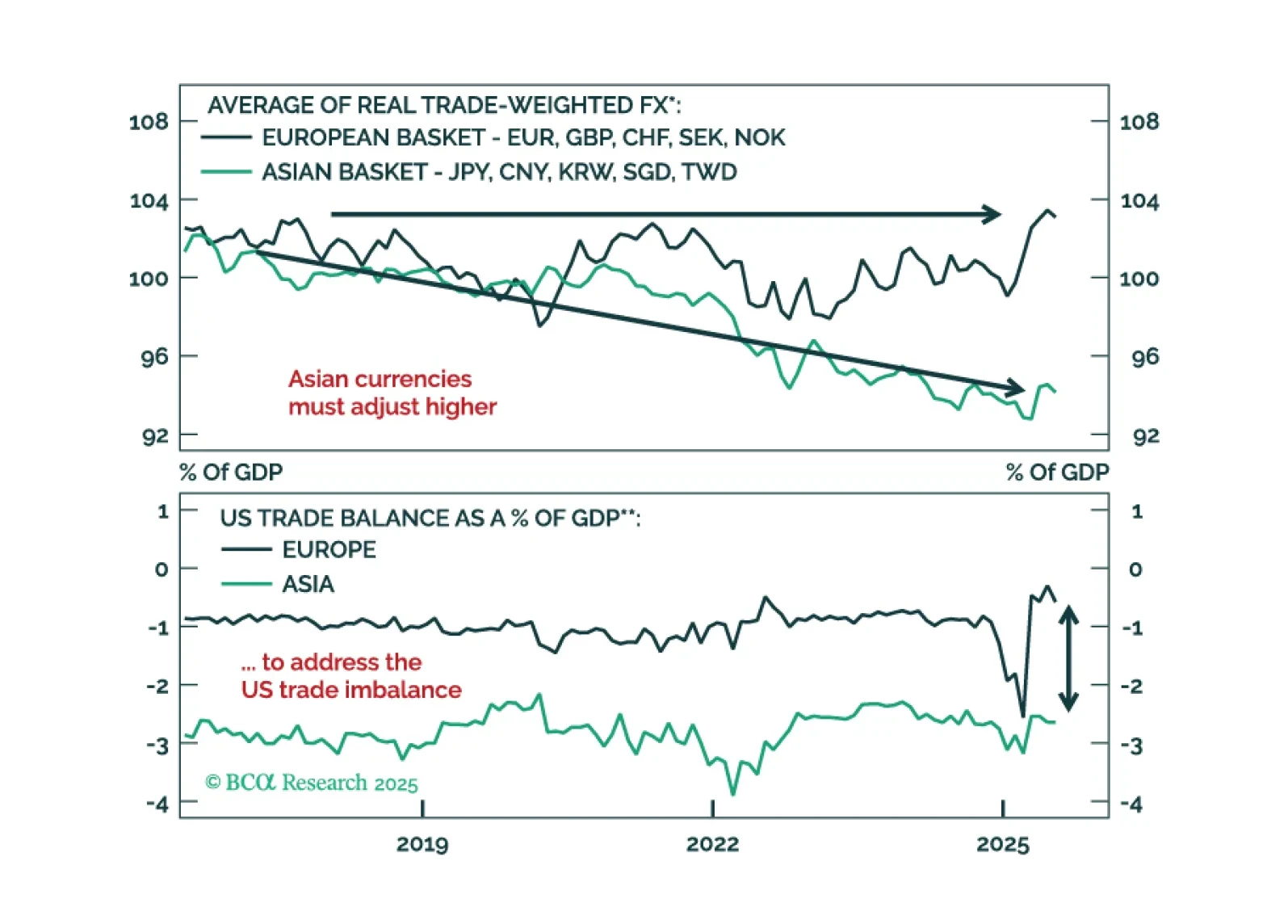

A fleeting greenback rally post Fed rate cut will offer a final chance to reset short dollar exposures. See why undervalued Asian FX are poised to lead the next leg lower in USD and how to position now.

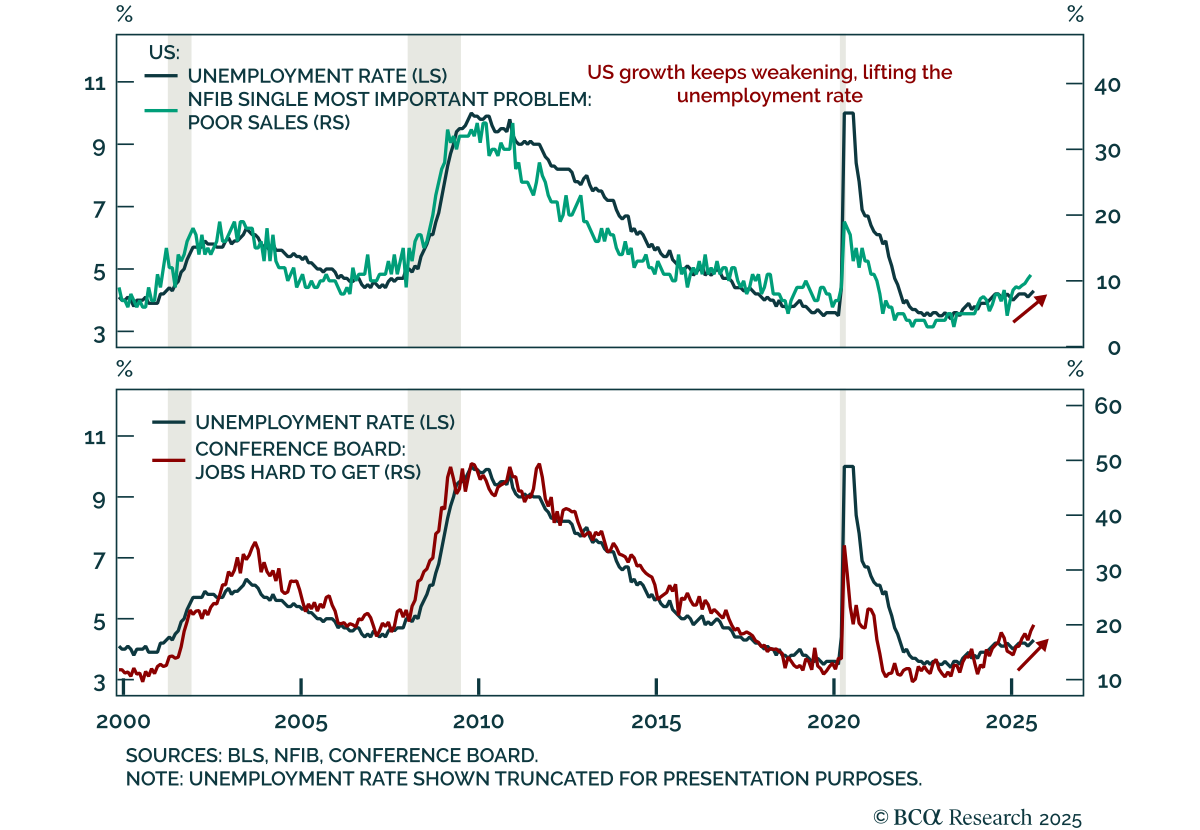

Although our recession conviction has risen, we conclude our strategy review by closing our equity underweight and our fixed income and cash overweights. AI momentum is too strong to have anything more than modest exposure to an equity decline via a small SPY put position.

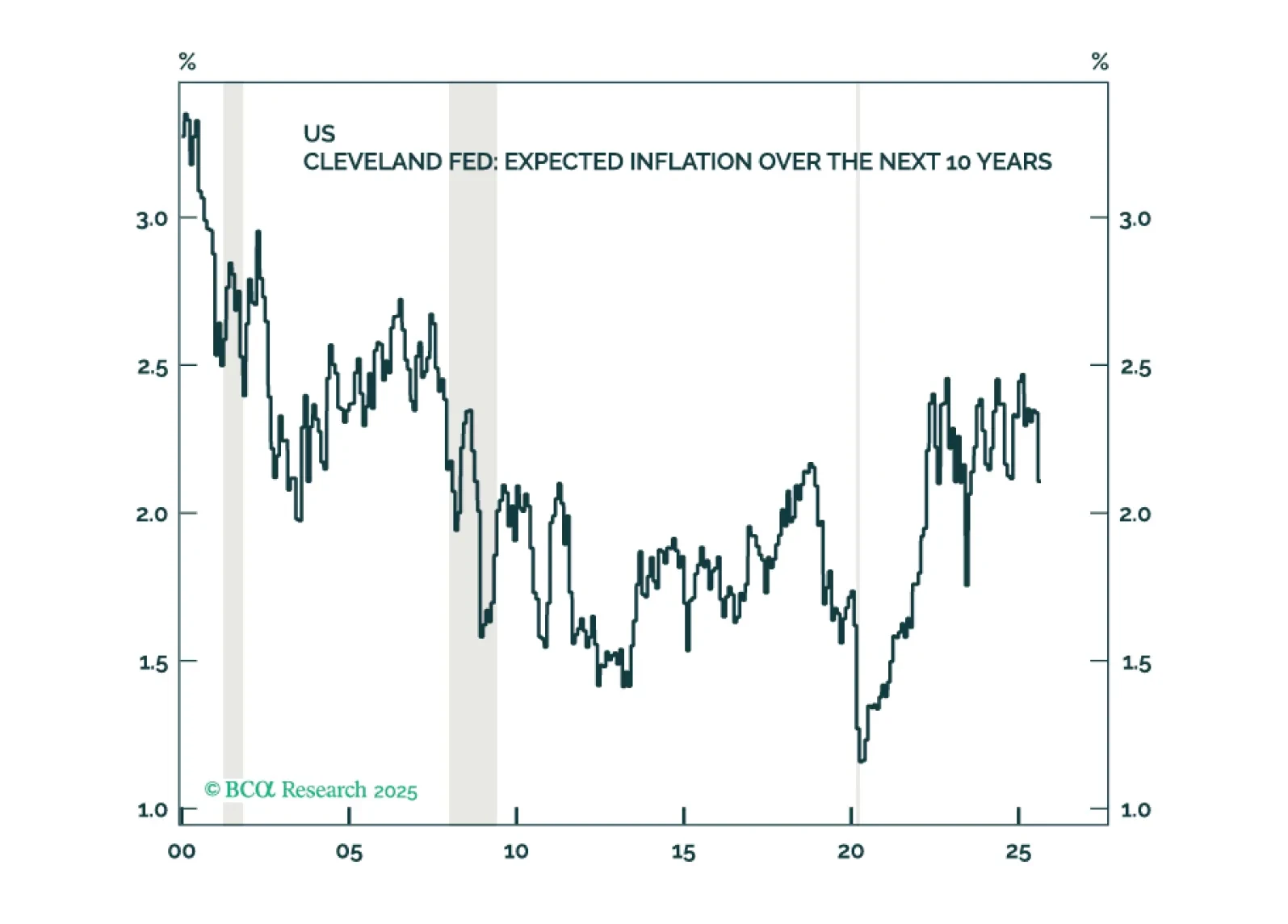

Inflation expectations in the US remain reasonably well anchored and there are few signs of a brewing wage-price spiral. Thus, the near-term risks to growth outweigh the risks of higher inflation. Looking beyond the next year or two, however, we are worried about stagflation.