Economic Growth

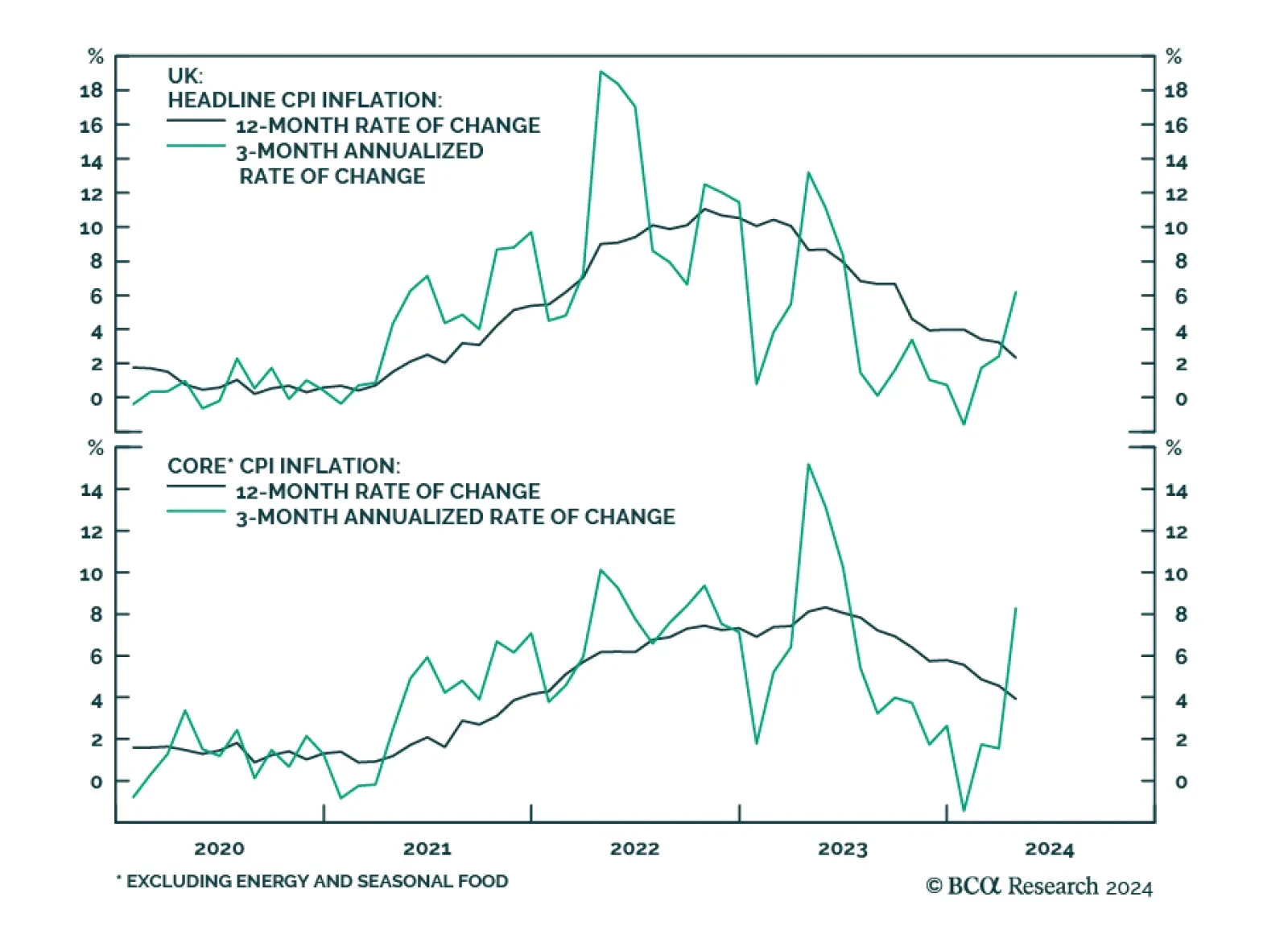

The UK CPI release surprised markets to the upside across the board on Wednesday. Headline CPI increased 2.3% year-on-year, above expectations of 2.1%. Core surprised to the upside as well, moderating from 4.2% to 3.9%y/y, less than the moderation embedded in…

We do not subscribe to the Goldilocks scenario in which price pressures continue to ease while economic growth remains robust. We expect that softening labor demand will eventually hinder consumption as wage and payrolls growth slows, at the same time that…

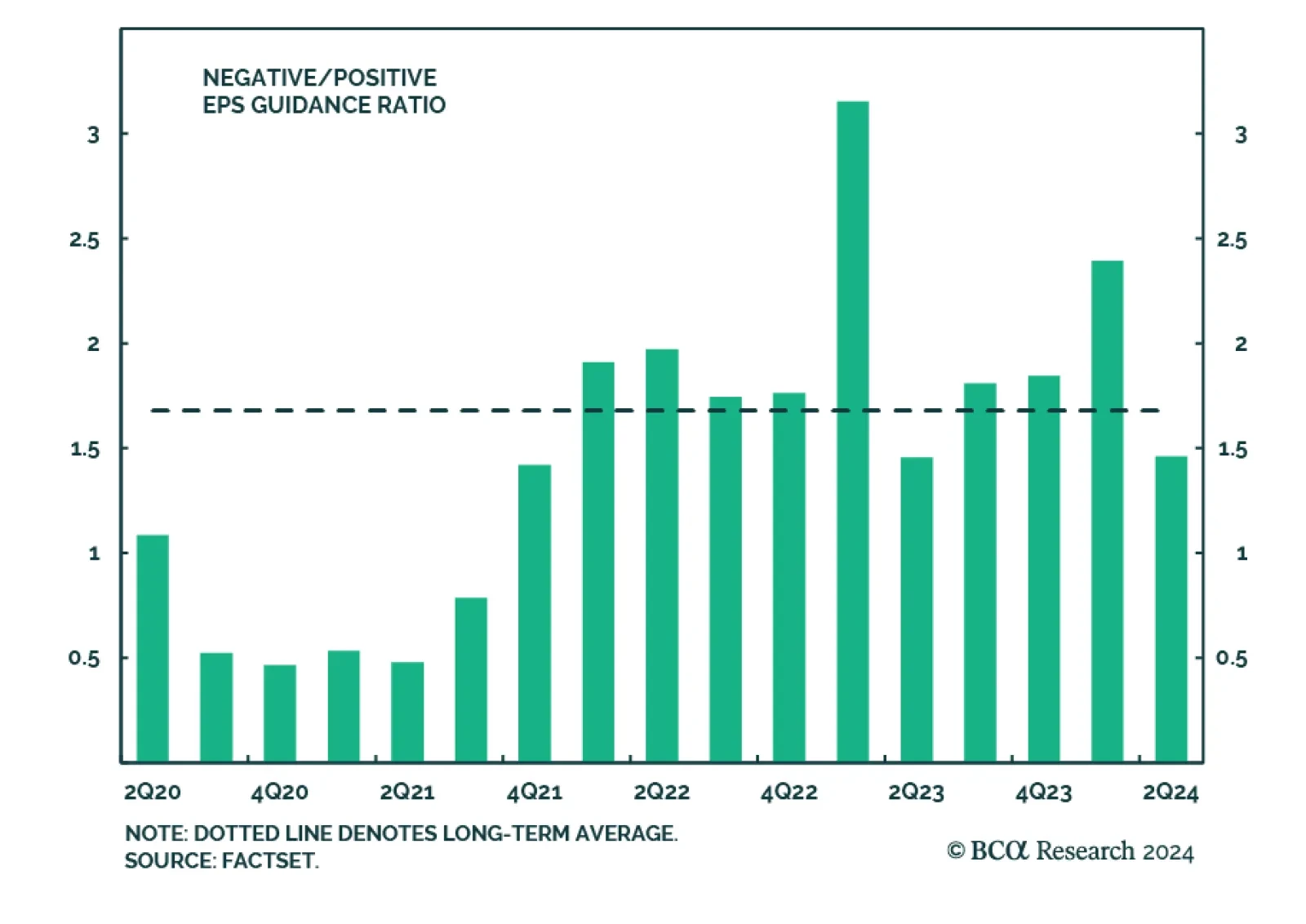

The Q1 2024 earnings season is drawing to a close with 93% of S&P 500 companies having reported results as we go to press. Three-quarters (two-thirds) of companies have topped earnings (sales) expectations in Q1, according to Factset. Next quarter’s…

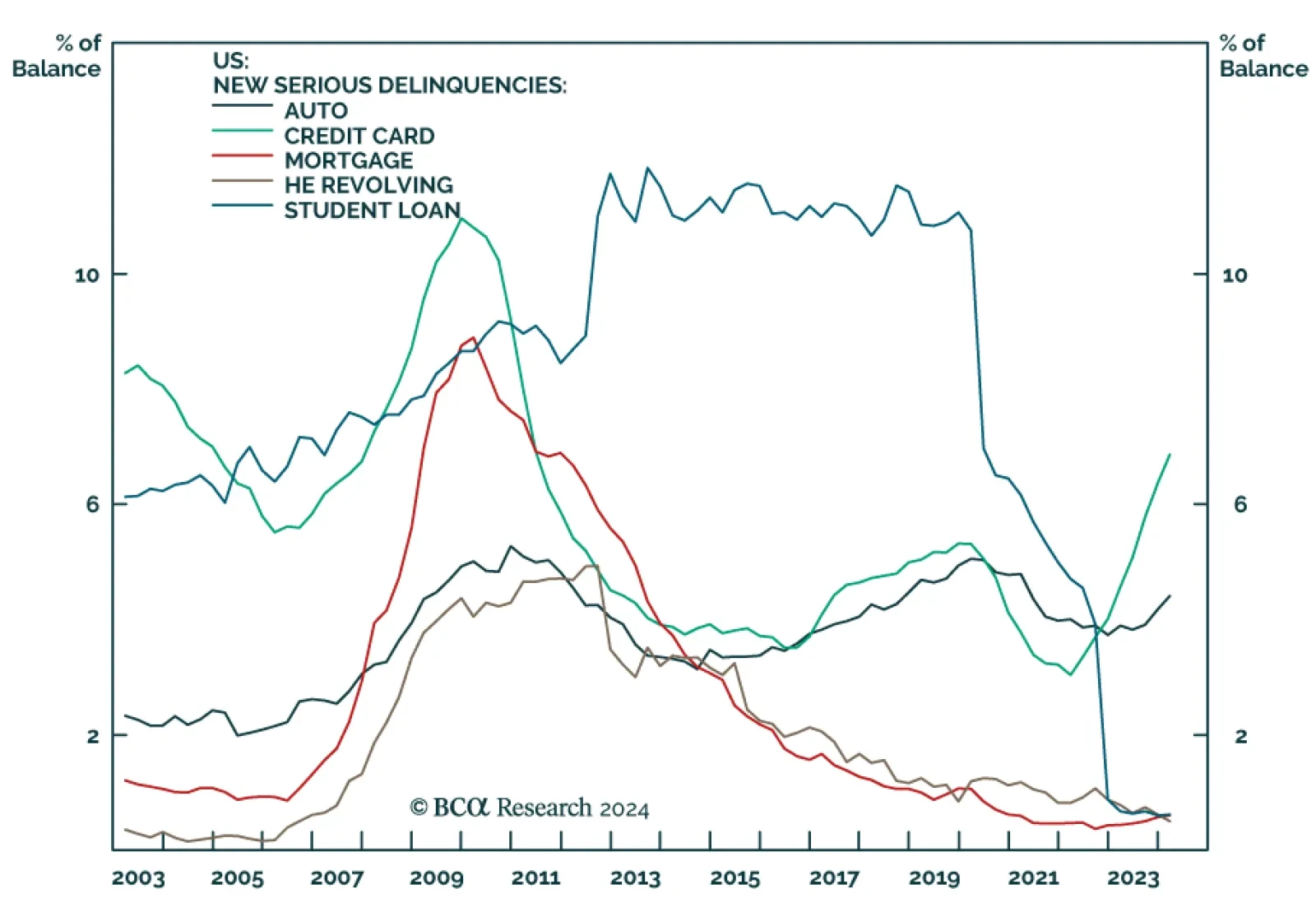

The New York Fed Quarterly Report on Household Debt and Credit indicates that US household debt rose 1.1% q/q in Q1 to $17.7 trillion. Higher mortgage, home equity loan and auto loan balances drove the bulk of the Q1 increase, while credit card balances…

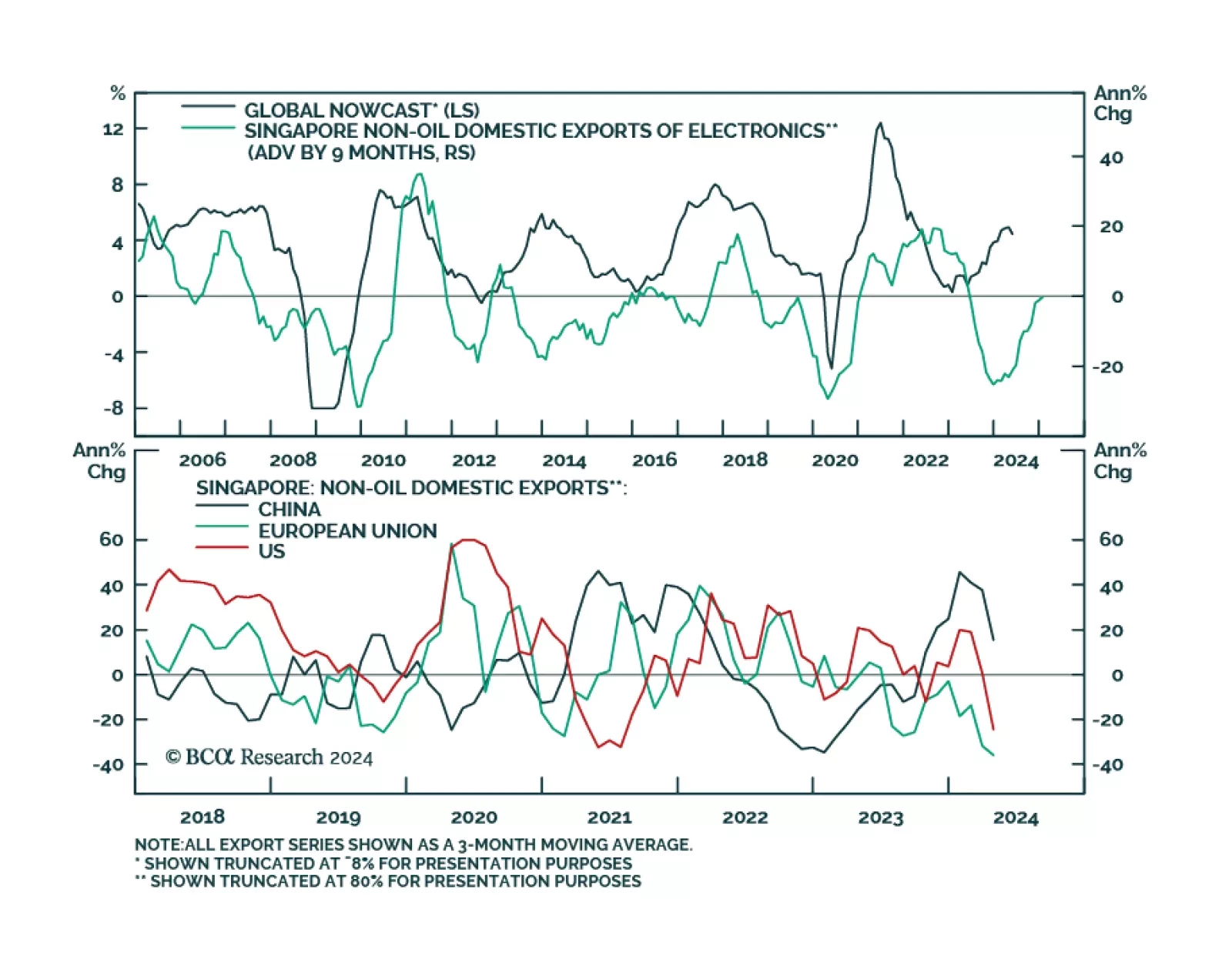

Export dynamics from small open economies are bellwethers for global trade and recent export data out of Taiwan and South Korea suggested robust global growth momentum in March. In April, Singapore’s electronics exports, which are particularly sensitive to…

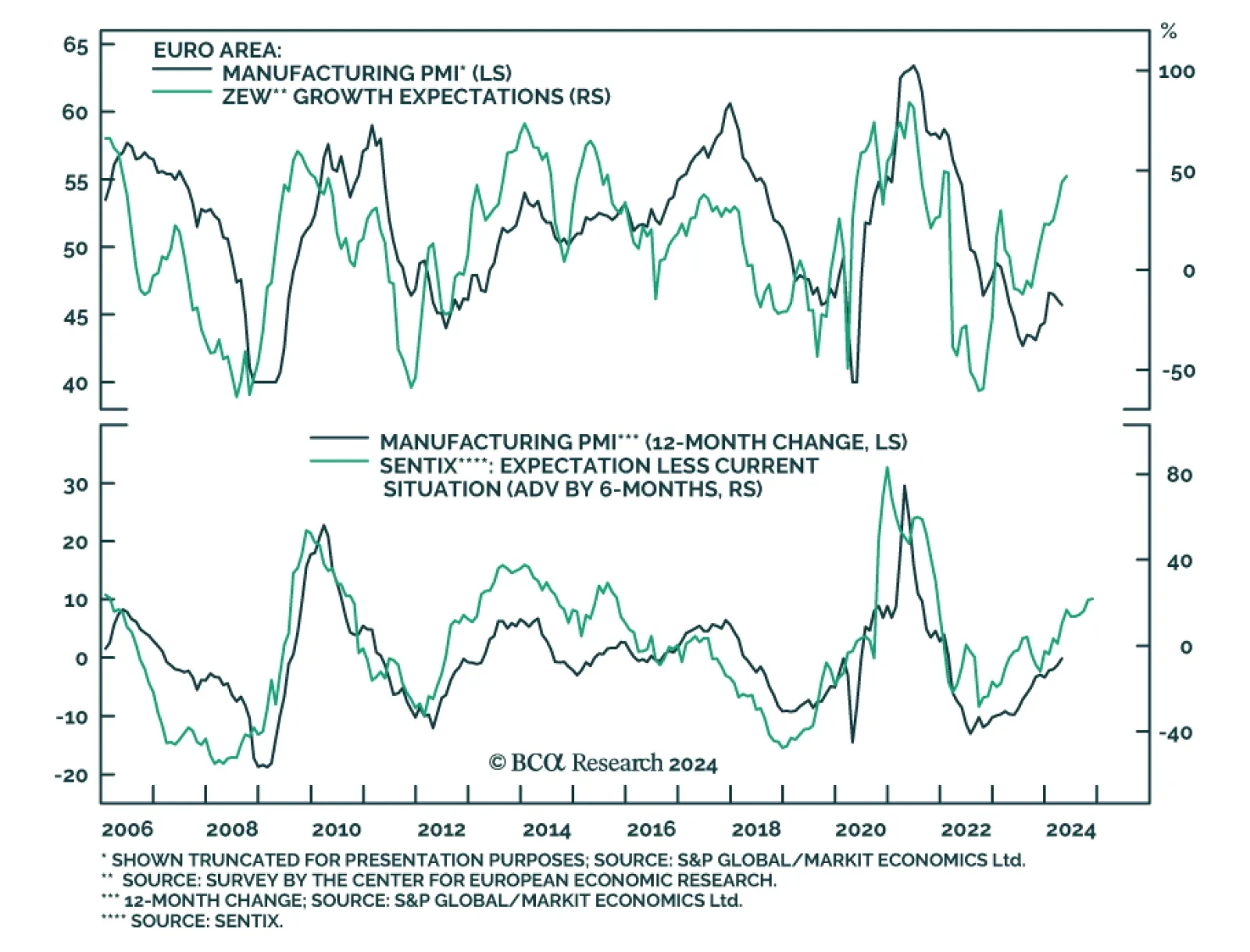

Investor and business sentiment continues to improve in the Eurozone. The ZEW Expectations series for the Eurozone (+3.1 to 47 in May) and Germany (+4.2 to 47.1, above expectations) strengthened to 27-month highs. Moreover, the spread between the expectations…

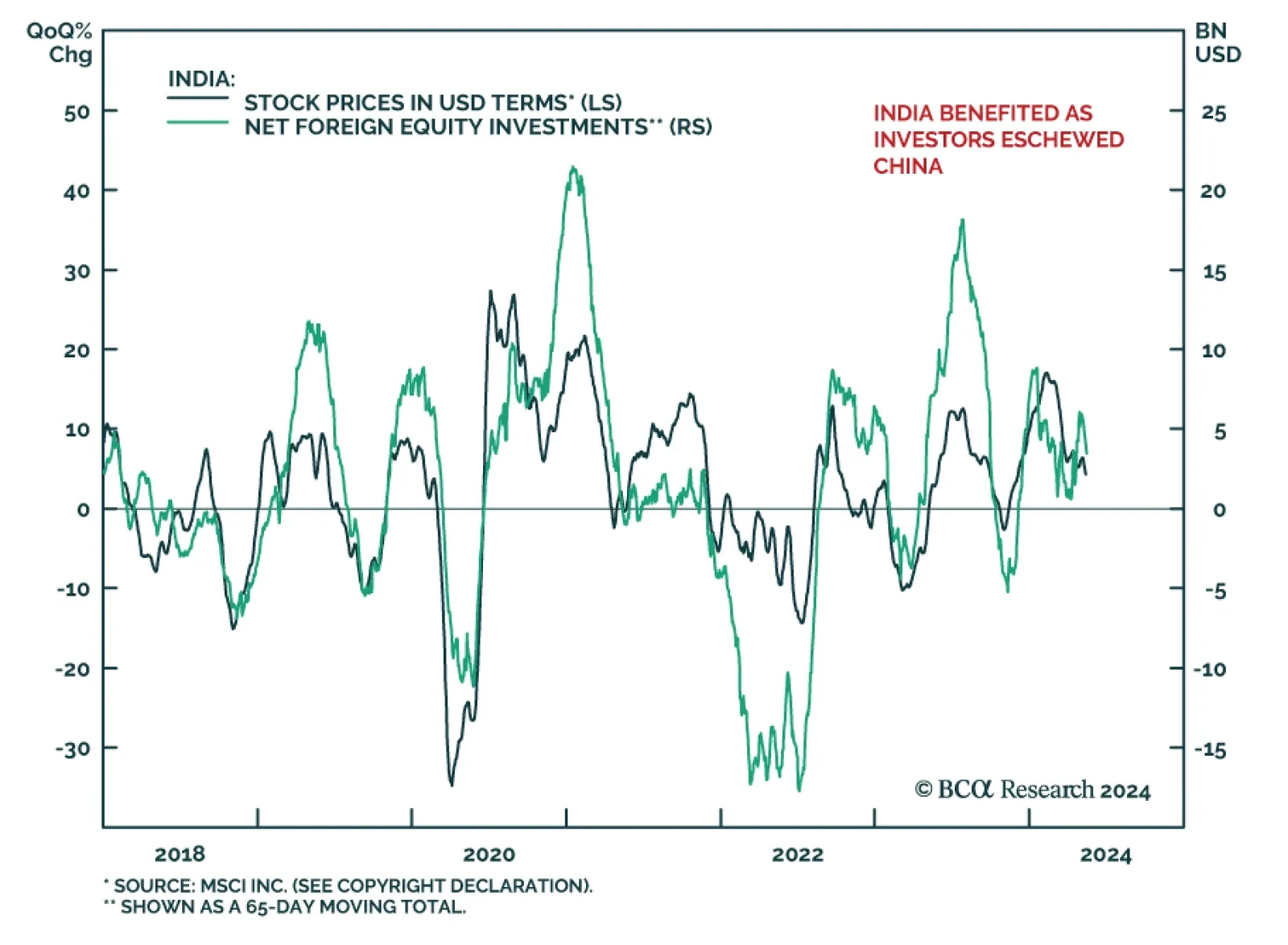

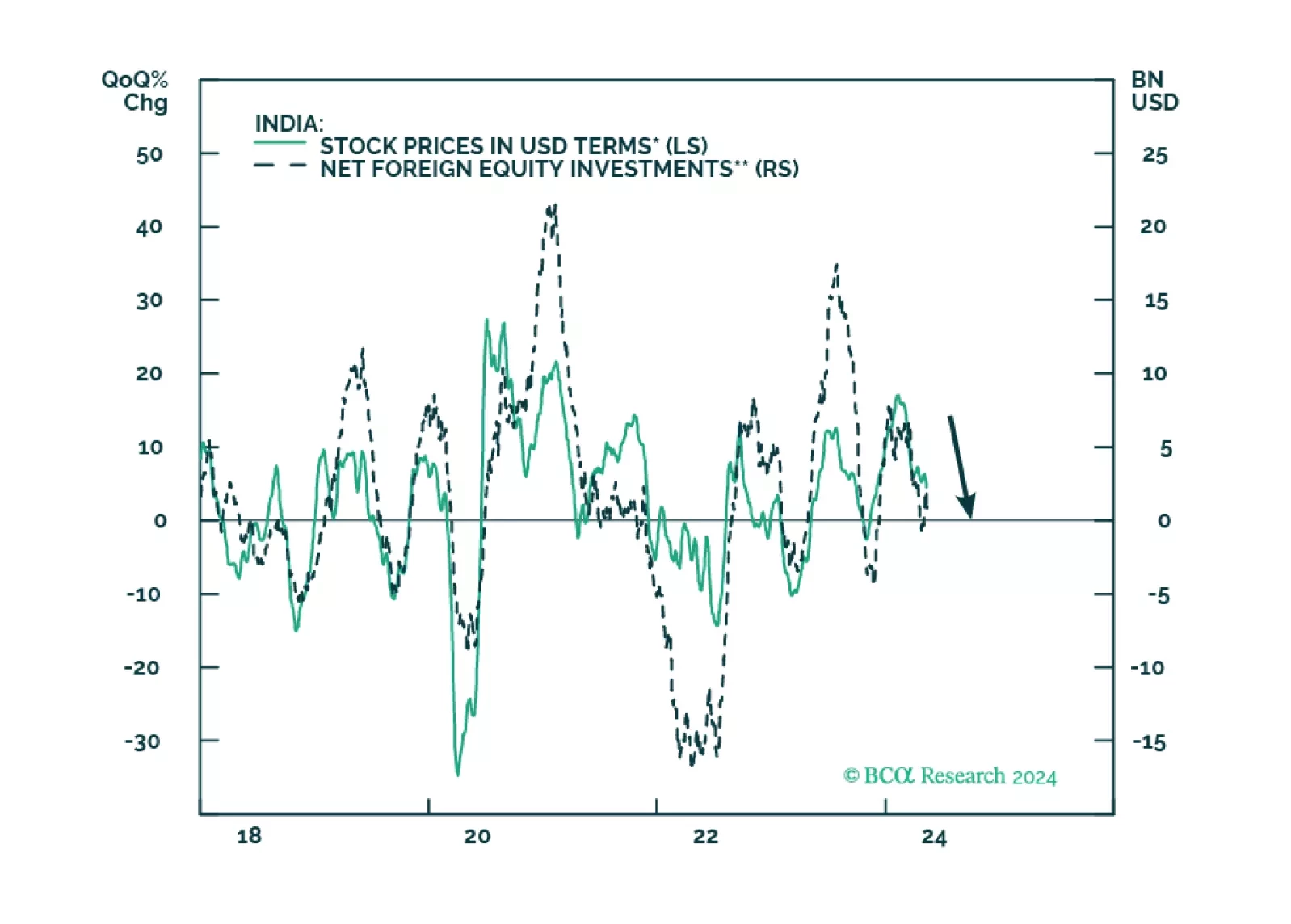

According to BCA Research’s Geopolitical Strategy service, Indian Prime Minister Modi is on track to be reelected for his third term, with the latest polls in April averaging 385 seats for the National Democratic Alliance, which includes his Bharatiya Janata…

Modi and the BJP are at or near the peak of their political dominance, and their third term will be challenging as they must deal with harder reforms amidst a slowing domestic and global economic environment. In the long run, however, we remain constructive on India’s prospects, as its geopolitical and economic positioning are favorable and improving.

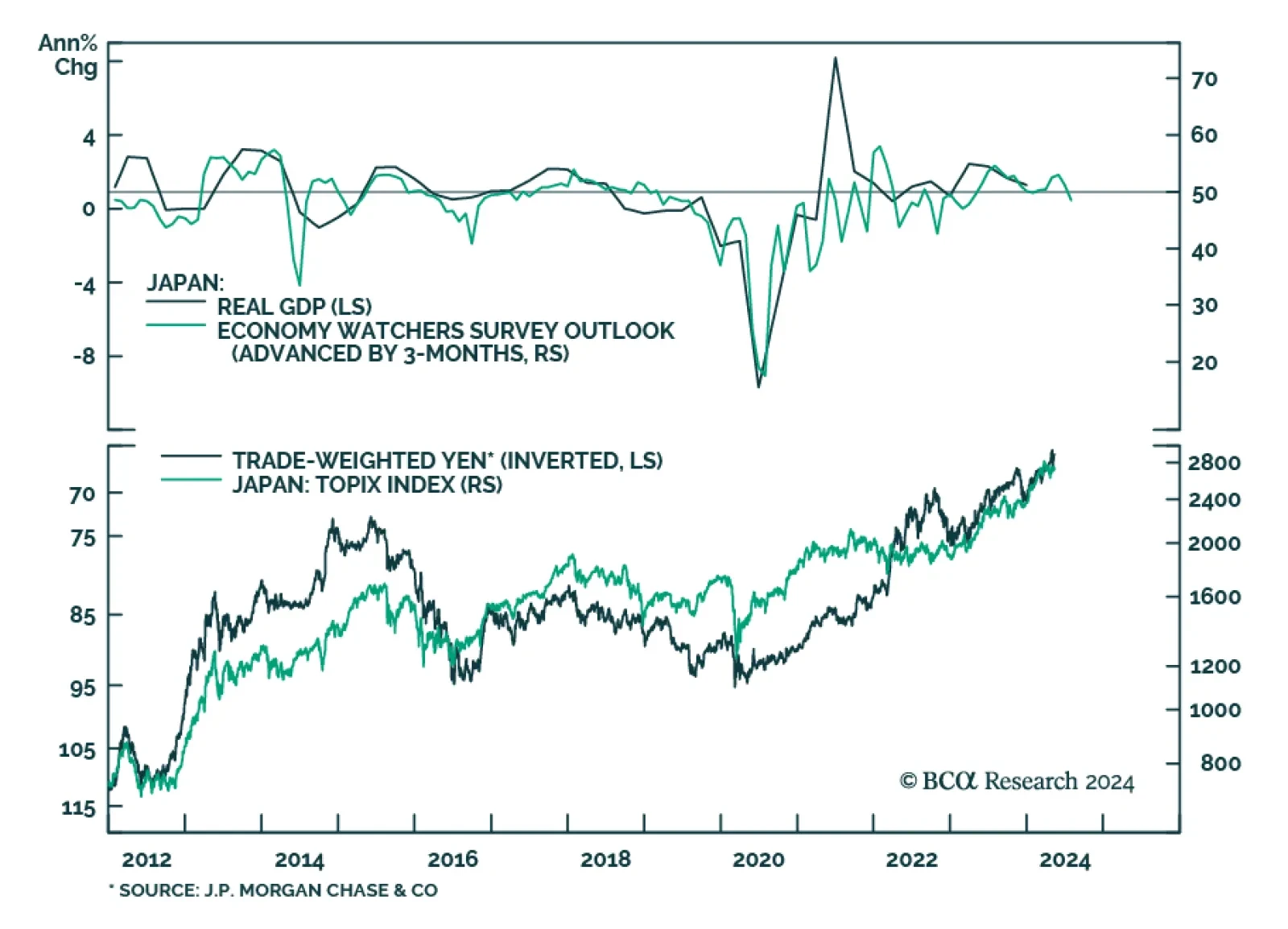

The Bank of Japan’s Economy Watchers Survey – a gauge of sentiment among business owners – disappointed in April. The Current Conditions and the Outlook indices deteriorated from 49.8 to 47.4 (20-month low) and from 51.2 to 48.5 (16-month low), below…

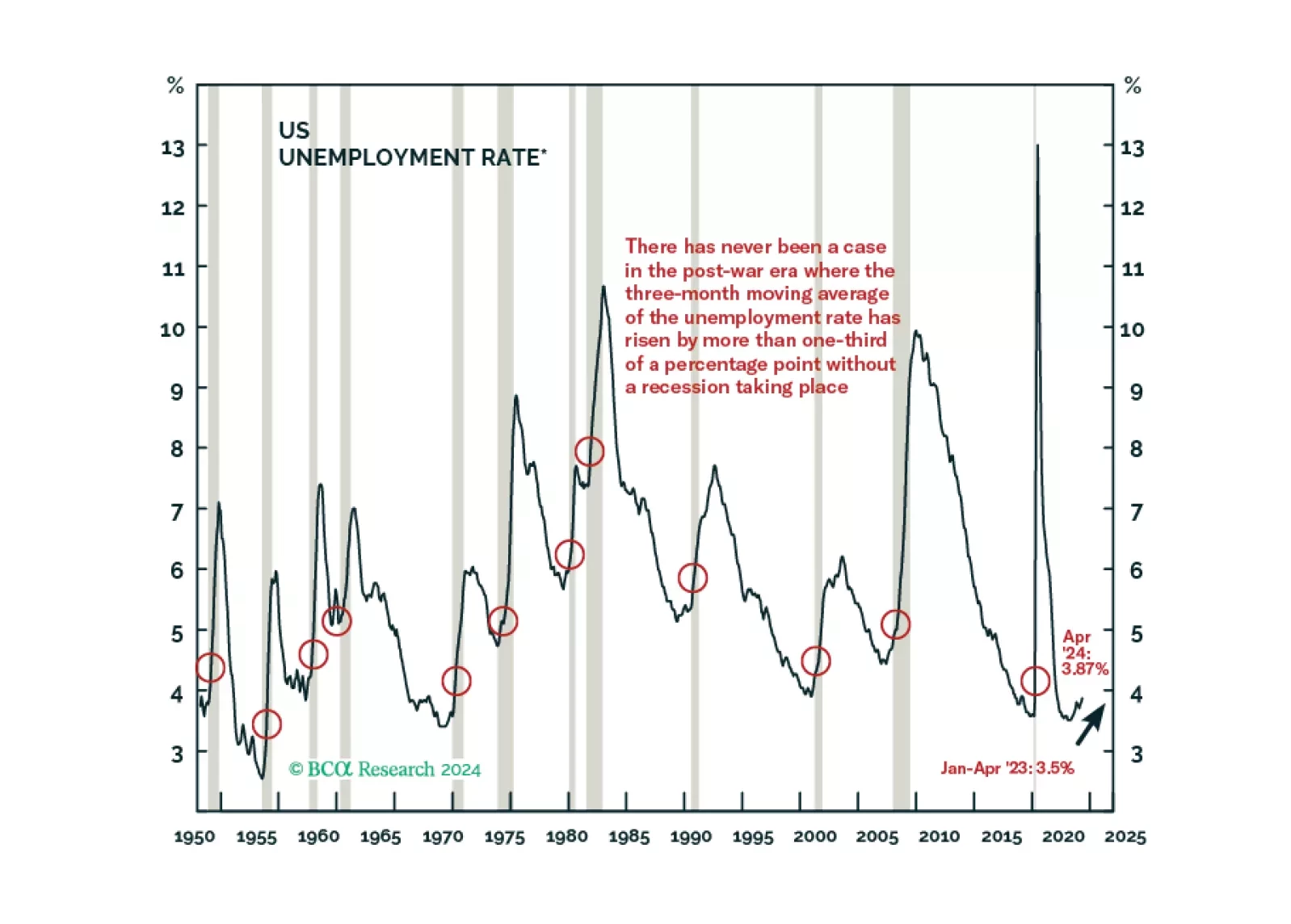

We marked the first X on our Equity Downgrade Checklist and the latest JOLTS, Employment Situation and SLOOS releases brought us closer to ticking some others. We remain tactically neutral on equities but expect that we will underweight them as excess savings are further depleted, leading labor market indicators continue to soften and consumer credit performance continues to fray.