Economic Growth

Despite a couple of rate cuts in H2 2024, borrowing costs will remain elevated in real terms amid lower inflation in the US and Europe. This and tightening fiscal policy will hinder domestic demand in advanced economies. Domestic demand in China and EM ex-China will remain very tepid, with risks skewed to the downside.

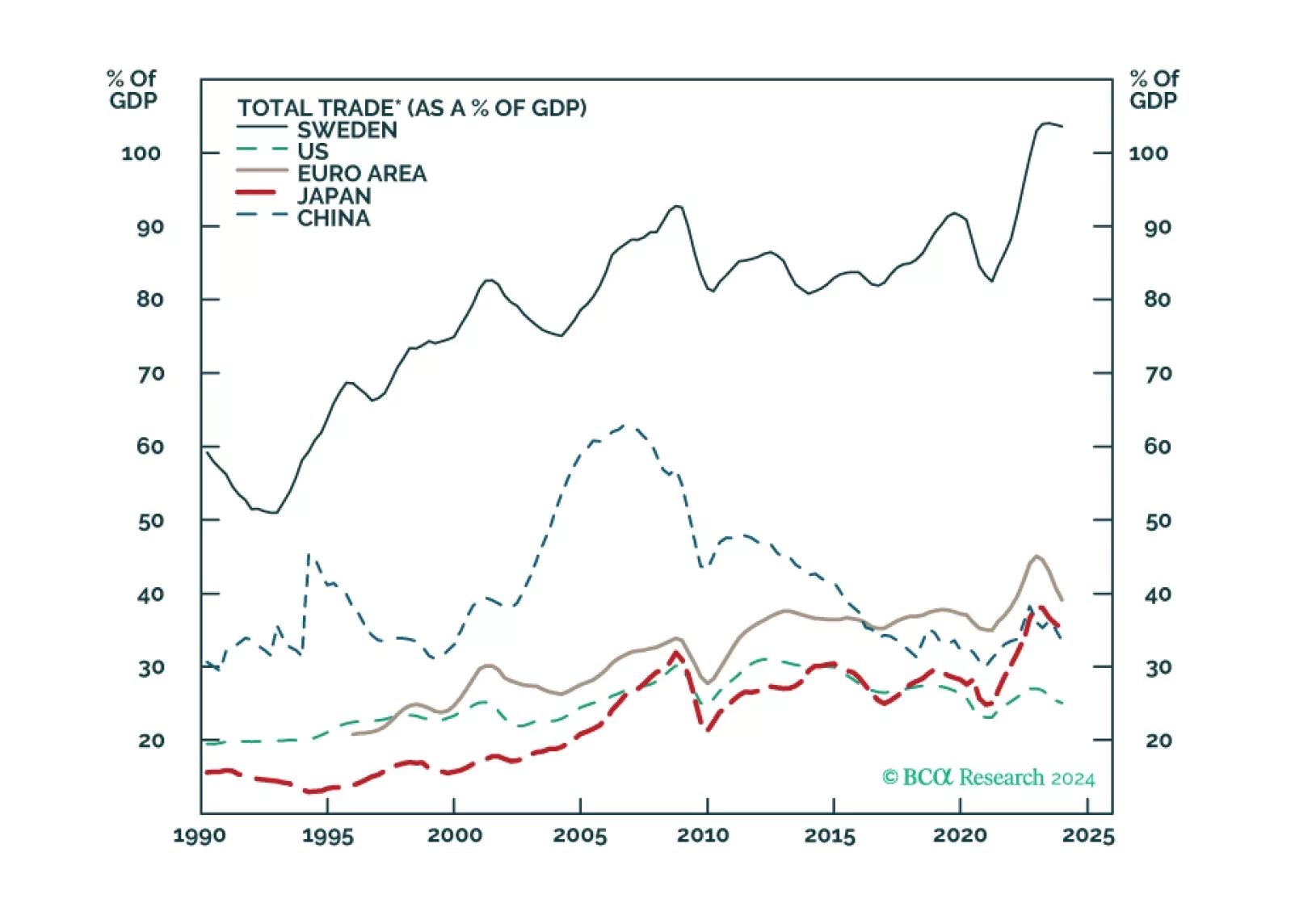

In this joint Foreign Exchange Strategy and Global Investment Strategy Special Report, we assess economic activity in Sweden, a highly cyclical and trade-oriented economy, and its implications for the global growth outlook.

Turkey’s macro policy stance can hardly be called orthodox. And yet, corporate profit margins will contract meaningfully this year. The lira can also fall massively even if inflation eases from the extremely high levels – just as it did in the 1990s.

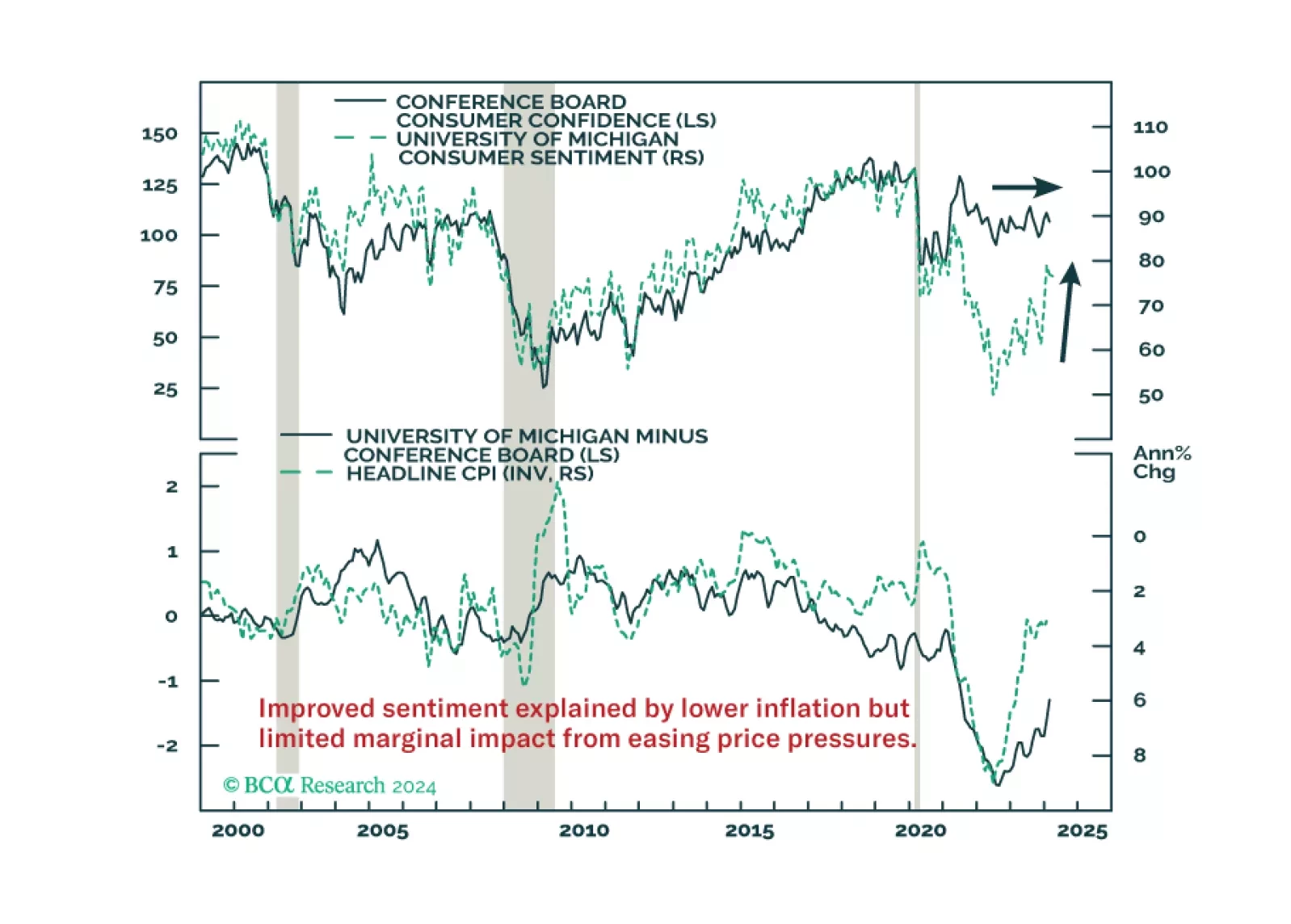

Improved consumer morale will not compensate for the fading tailwinds to consumption. Neither will the wealth effects from higher stocks and home prices.