Economic Growth

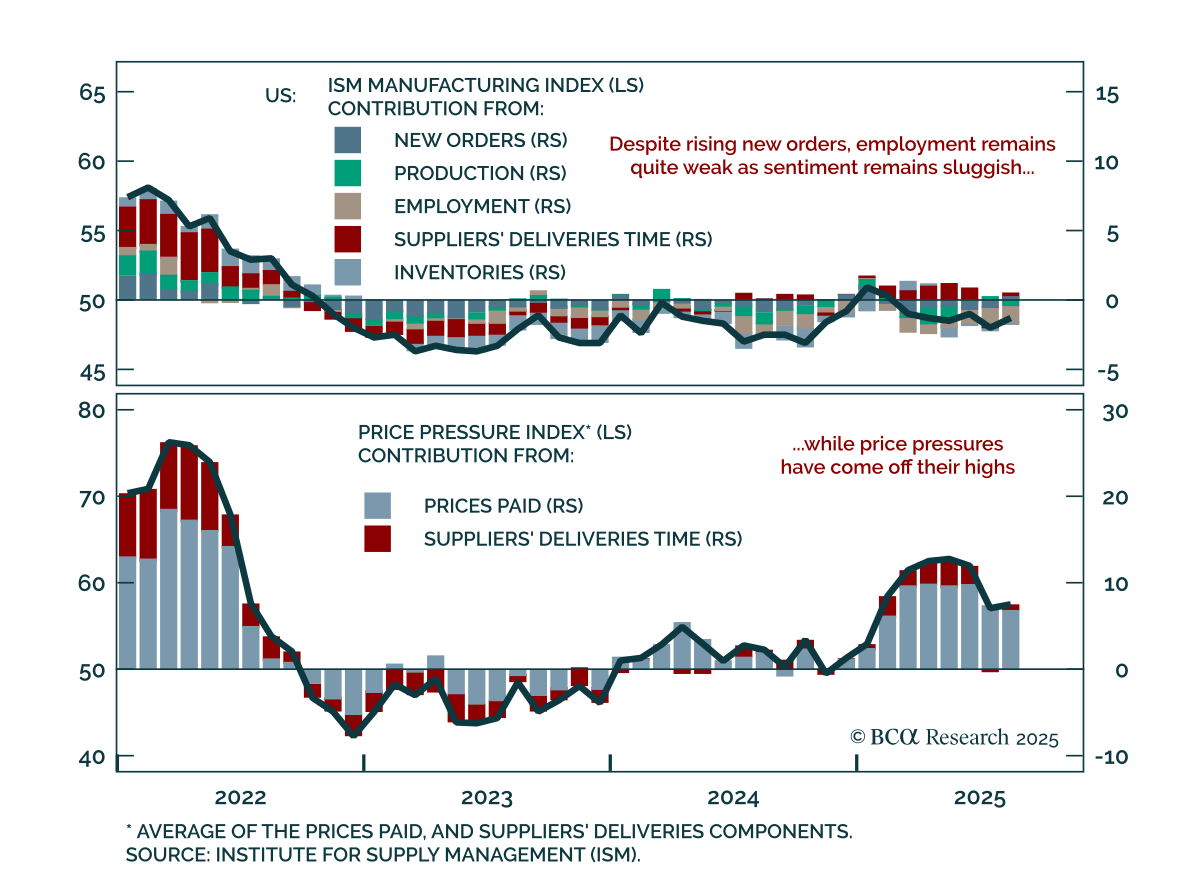

August ISM Manufacturing was mixed, with stronger orders offset by weak production and employment. The headline rose to 48.7 from 48.0, missing expectations. New orders beat estimates, rising into expansion at 51.4 and lifting the New…

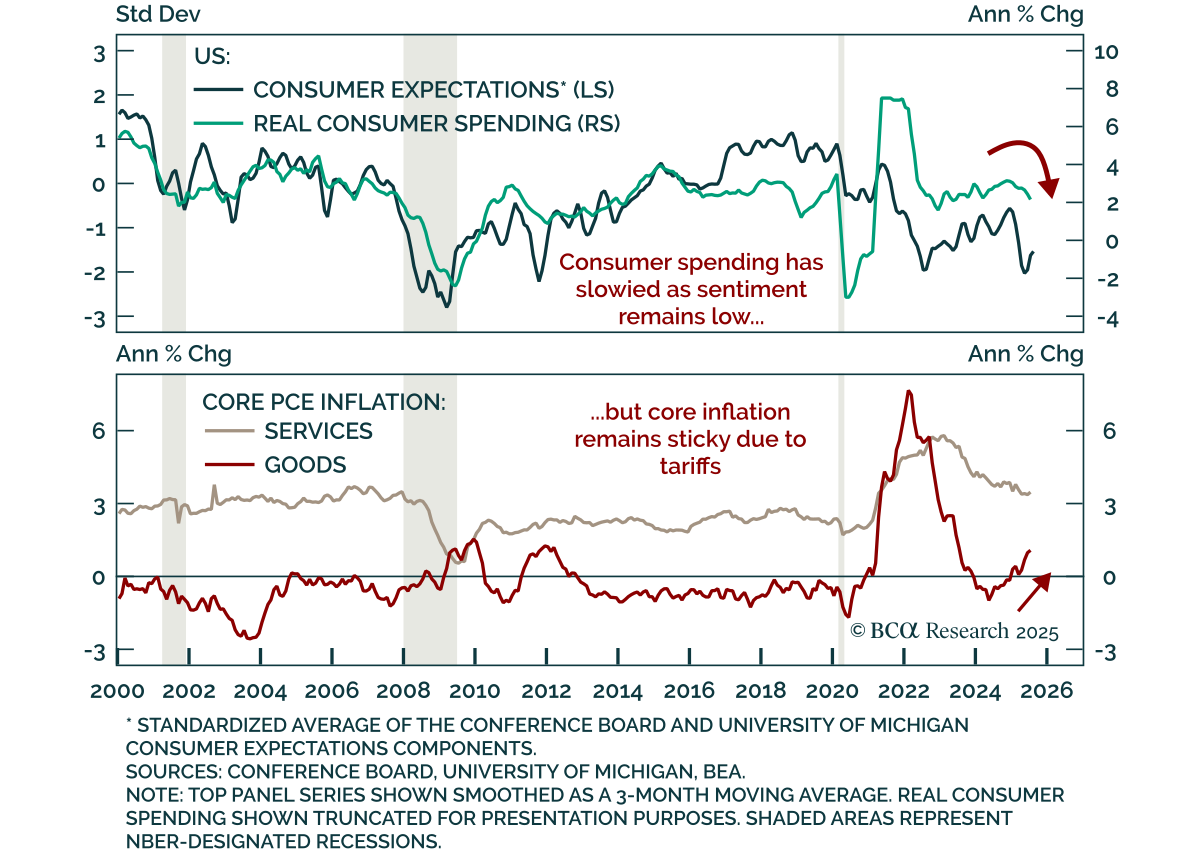

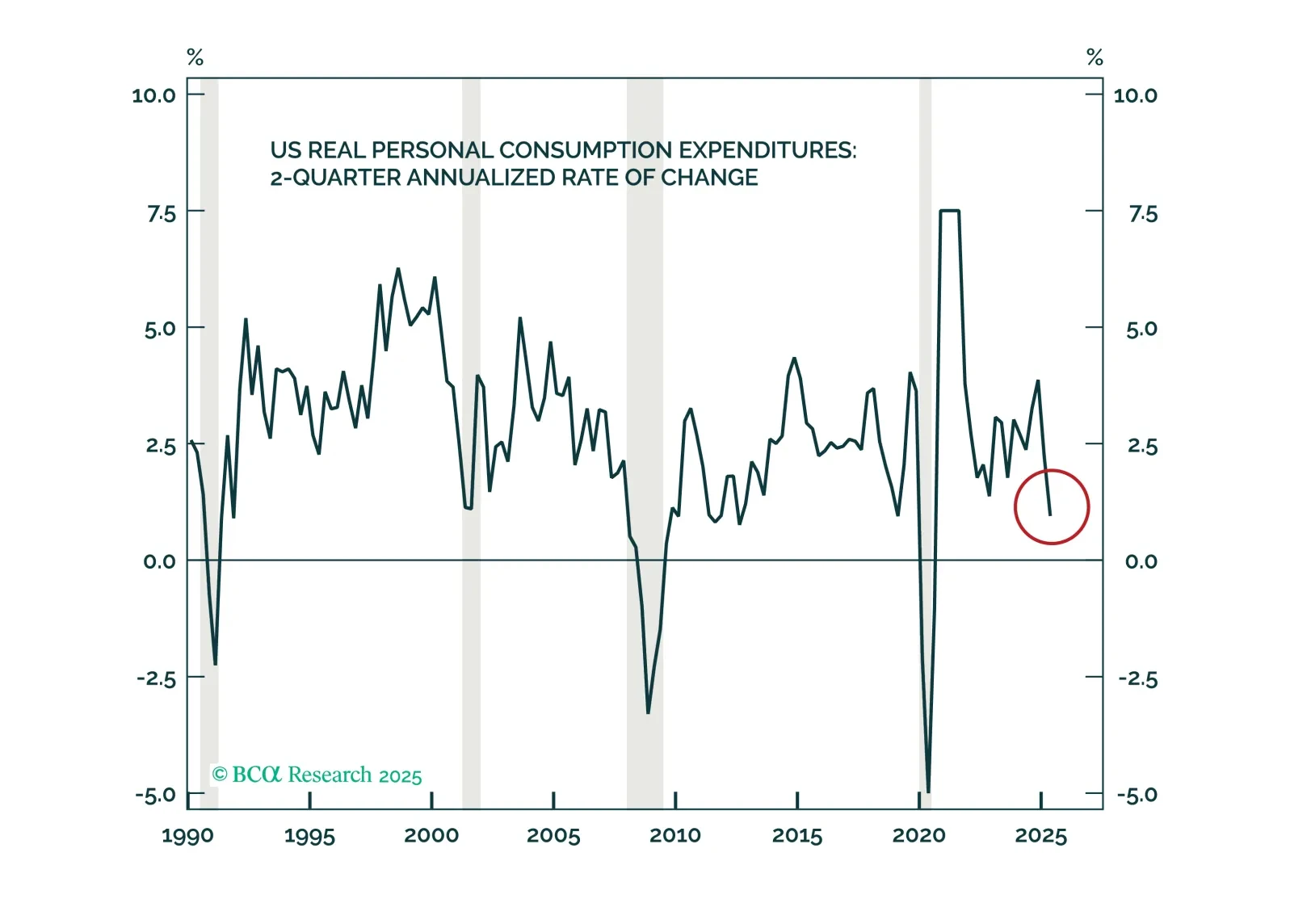

July income and spending data confirmed resilient consumption and sticky inflation, however, slowing labor momentum keeps us defensive. Real personal spending increased 0.3% m/m. Personal income rose 0.4% m/m, with real income ex-transfer payments…

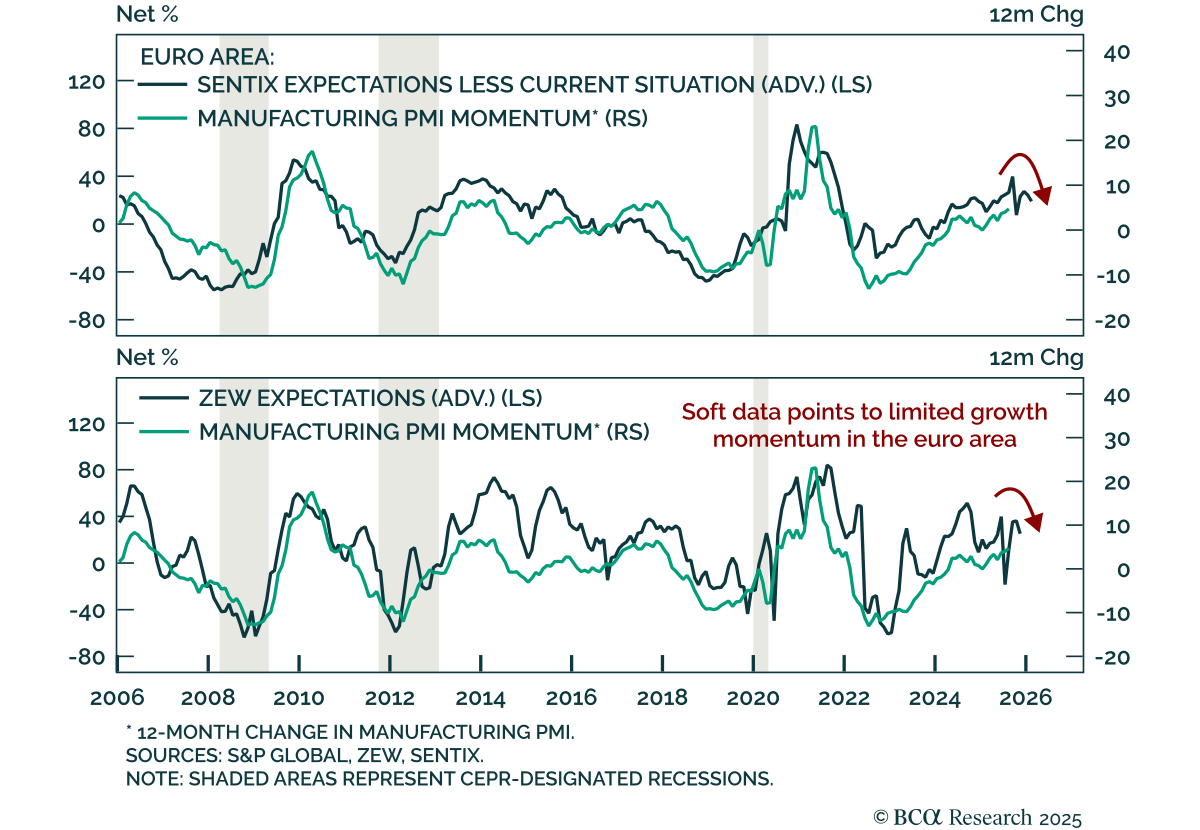

Weak Euro Area sentiment data and tight financial conditions support the case for a tactical US outperformance over Europe. July monetary data came in slightly below expectations, with M3 growth only edging up to 3.4% y/y from 3.3%. Household loan growth…

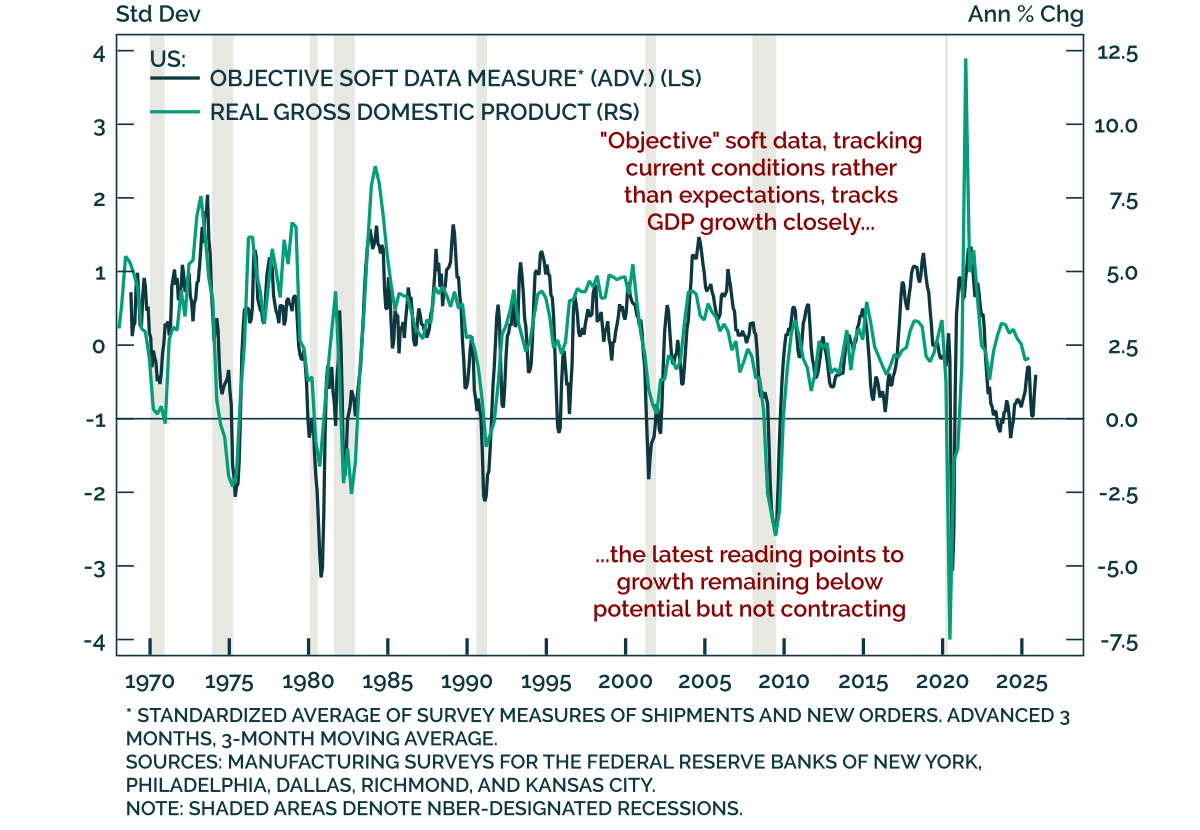

Regional Fed surveys point to low GDP growth, not an outright recession, which tactically supports low growth plays such as duration and tech. These timely surveys provide a snapshot of current month activity, combining “objective” indicators such as…

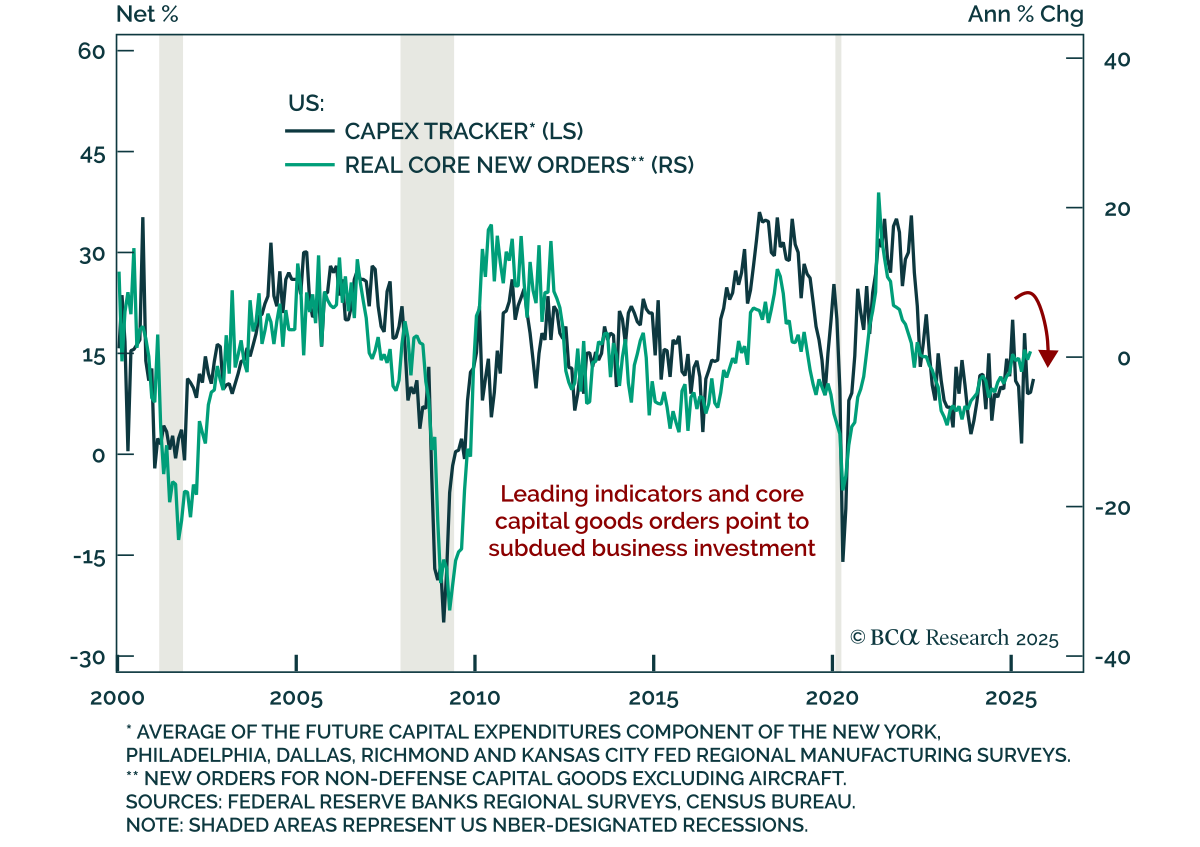

July US durable goods orders rebounded, but investment signals remain subdued and favor duration and tech. Orders fell 2.8% m/m after a 9.4% June drop, better than expected. Core measures excluding volatile components were stronger, with nondefense…

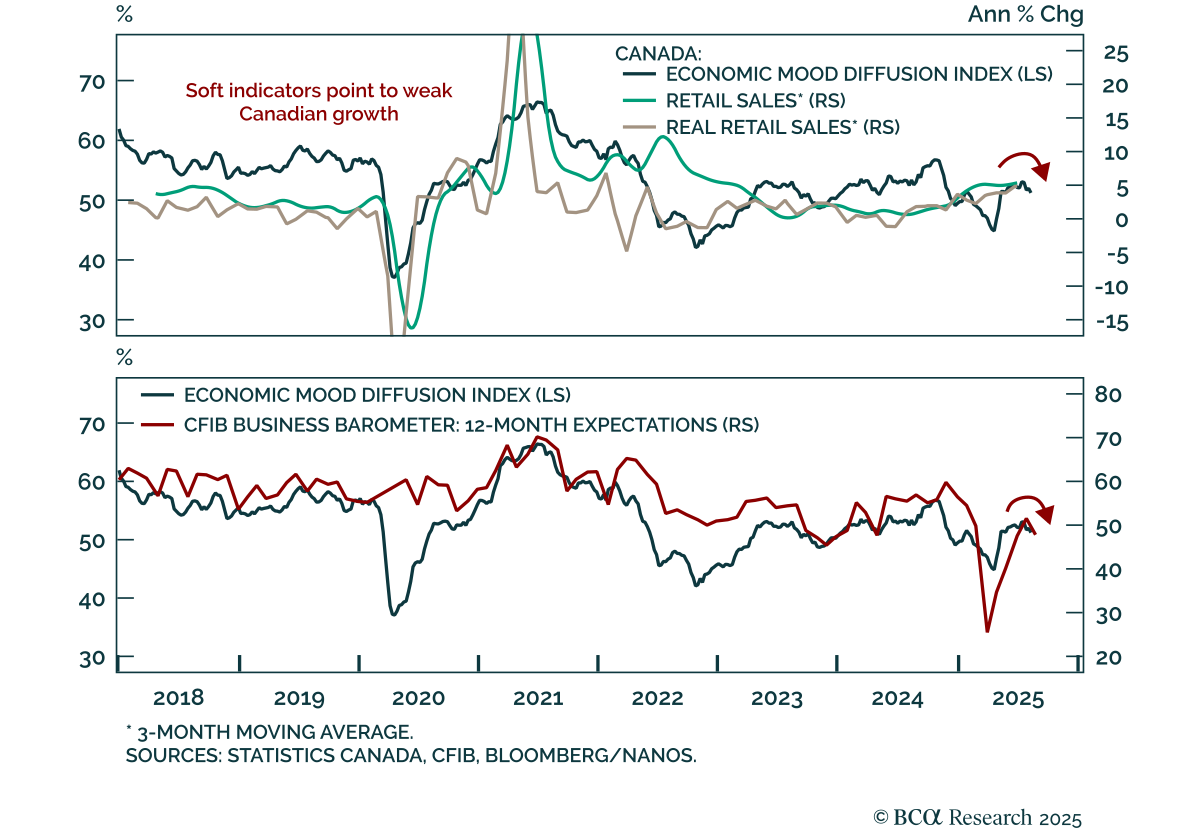

Canada’s fragile growth backdrop reinforces the case for more BoC easing than markets price. June retail sales rose 1.5% m/m, in line with expectations. Excluding autos, sales were stronger at 1.9%. However, the advance estimate for July points to a 0.8%…

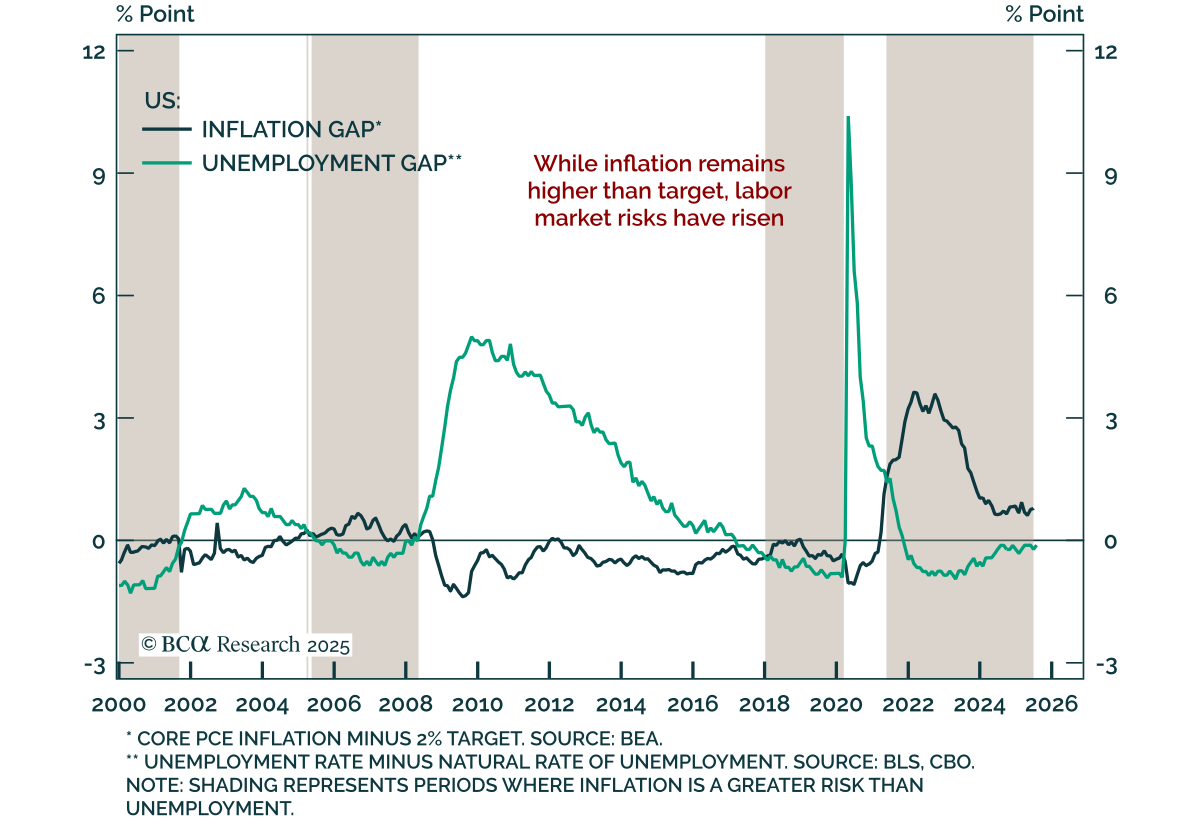

Powell’s Jackson Hole speech was misread, and points to cautious dovishness. Some commentators called it hawkish, others suggested the Fed abandoned its 2% target. Neither is accurate. Central bank communication is rarely binary; it operates across…

Economic activity plainly slowed in the first half, led by decelerating consumption and payrolls growth, but financial markets didn’t care. If the next two weeks of data don’t indicate that the May-June slowdown stretched into July and August, we will likely drop our defensive recommendations.

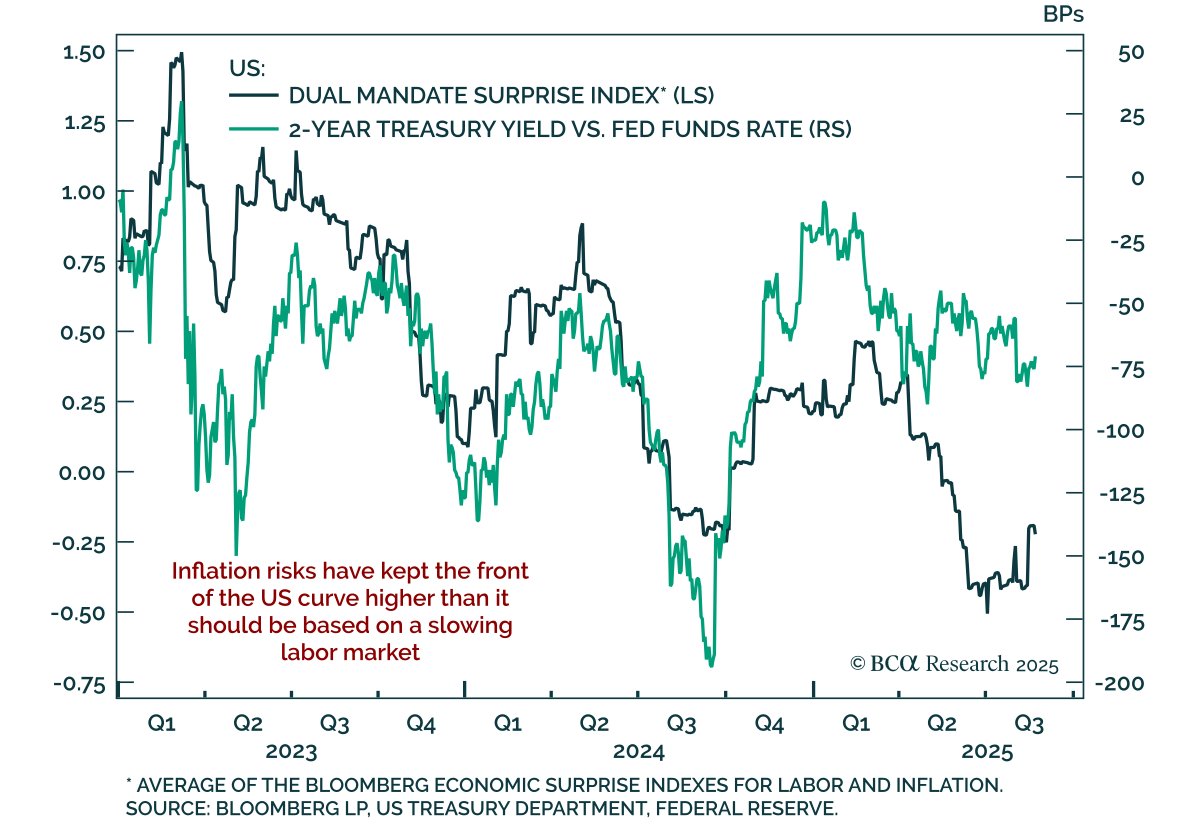

Powell’s final Jackson Hole speech signaled a dovish tilt, opening the door to a September cut. The Fed is under pressure to balance unemployment and inflation risks, with the FOMC split between “proactive” doves and “reactive” hawks. Recent data have not…

Although Euro area PMIs beat expectations in August, the growth outlook remains weak. The composite index rose to 51.1, driven by manufacturing returning to expansion at 50.5 from 49.8. Meanwhile the services PMI slipped 0.3 points to 50.7. The readings…