Economic Growth

Investors should think probabilistically about the economy and financial markets. In the face of non-linear effects, the range of possible outcomes can be very large. A systematic application of Bayes’ rule can help improve decision-making.

Numerous divergences have opened up between global risk assets and global business cycle variables. These gaps are unsustainable, and odds are that the recoupling will occur to the downside with risk assets selling off.

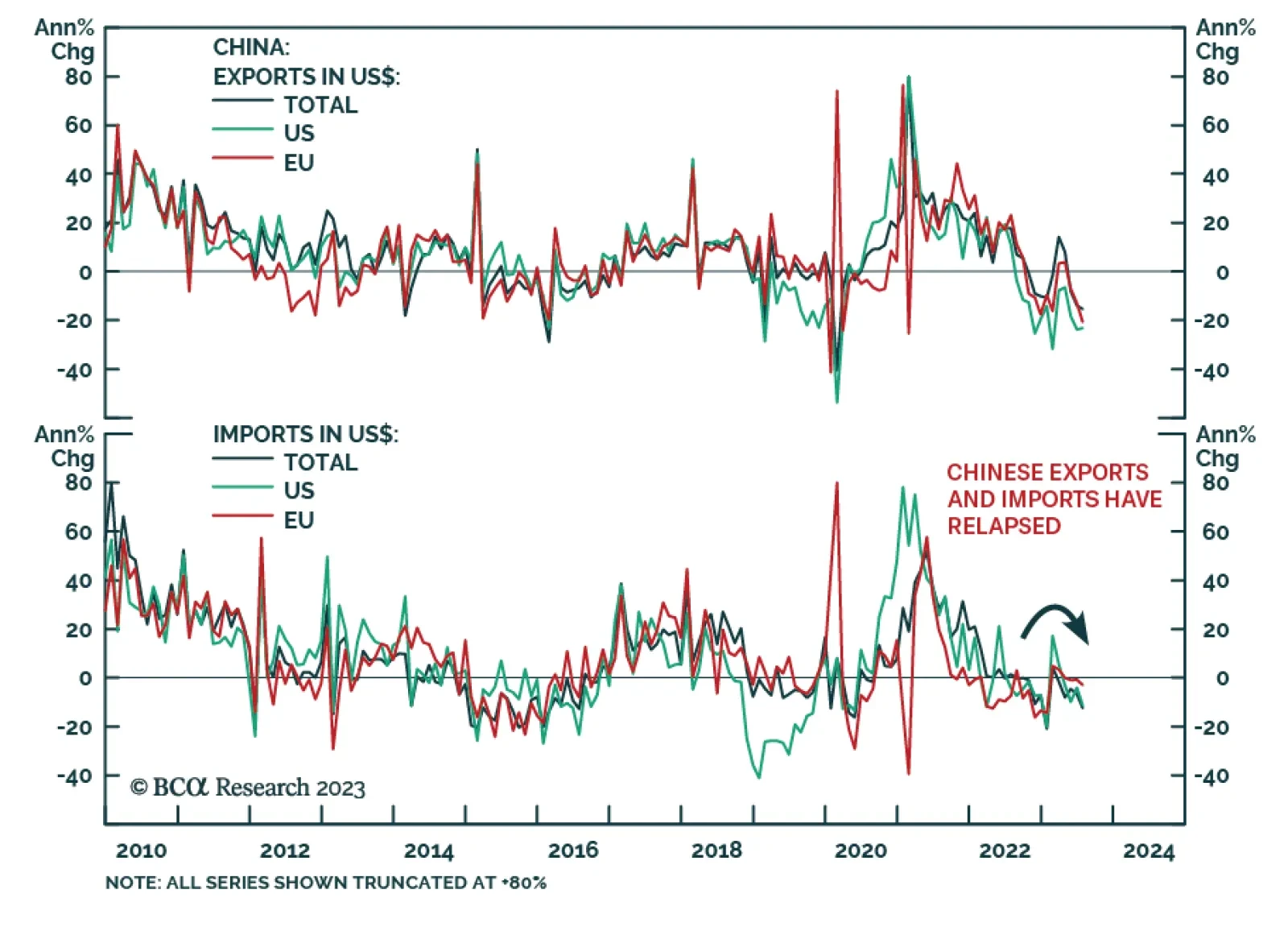

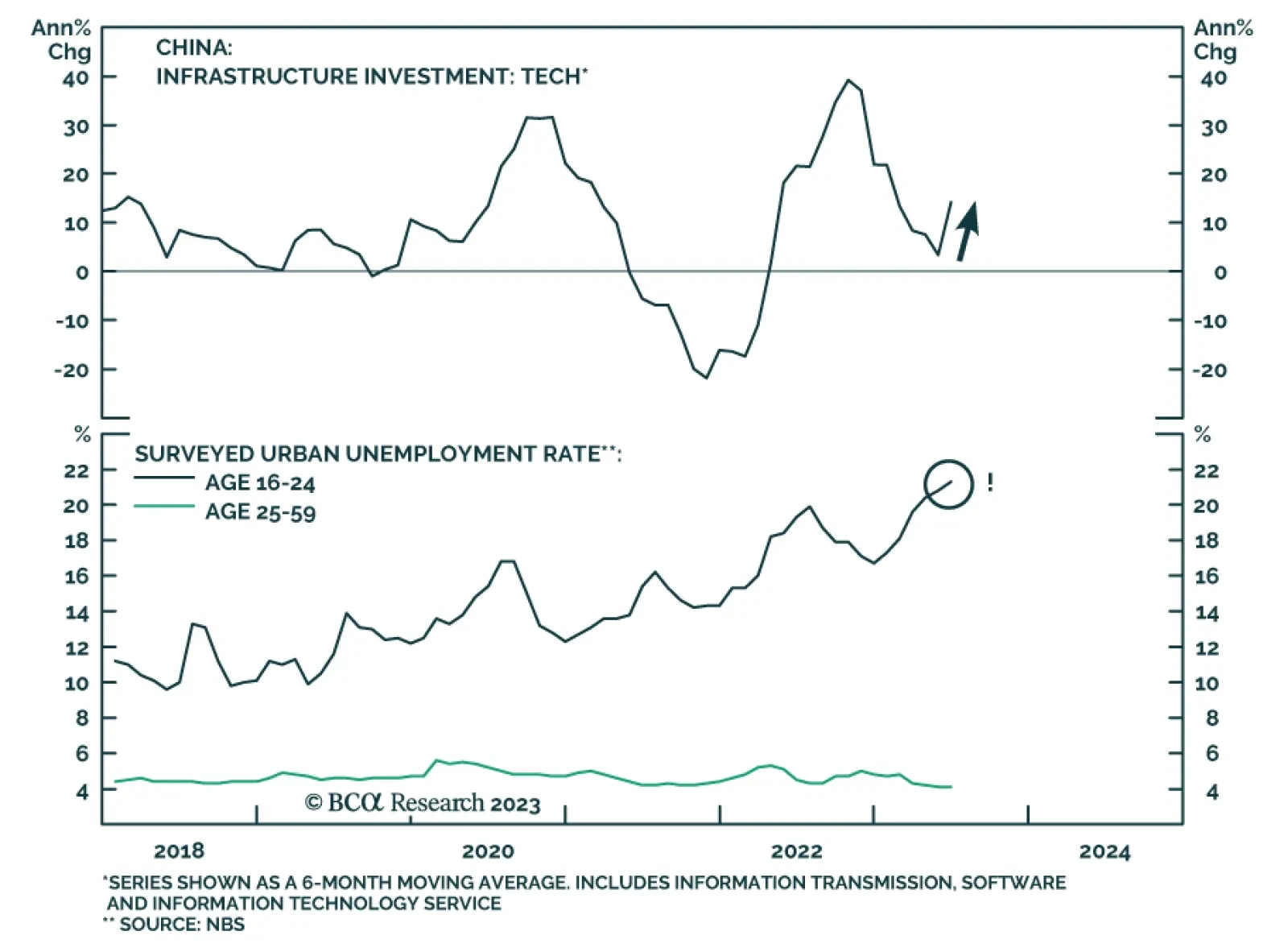

China has generated 41 percent of the world’s economic growth through the past ten years, al-most double the 22 percent contribution from the US. Now that the Chinese growth engine is failing, we explain why it is arithmetically impossible for world growth to maintain the altitude of the past few decades. And we discuss an important investment implication.

Although the RMB has cheapened, macro conditions are not yet favorable for the Chinese currency. We expect the RMB to decline by at least another 5% in the next six months. A weak currency and subdued economic growth lead us to maintain a cautious stance on Chinese equities.

The global economy will not enjoy an “immaculate disinflation” but will suffer a very maculate one due to China’s growth slowdown and restrictive monetary policy in the developed world. Investors should stay overweight low-beta assets.