Economy

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

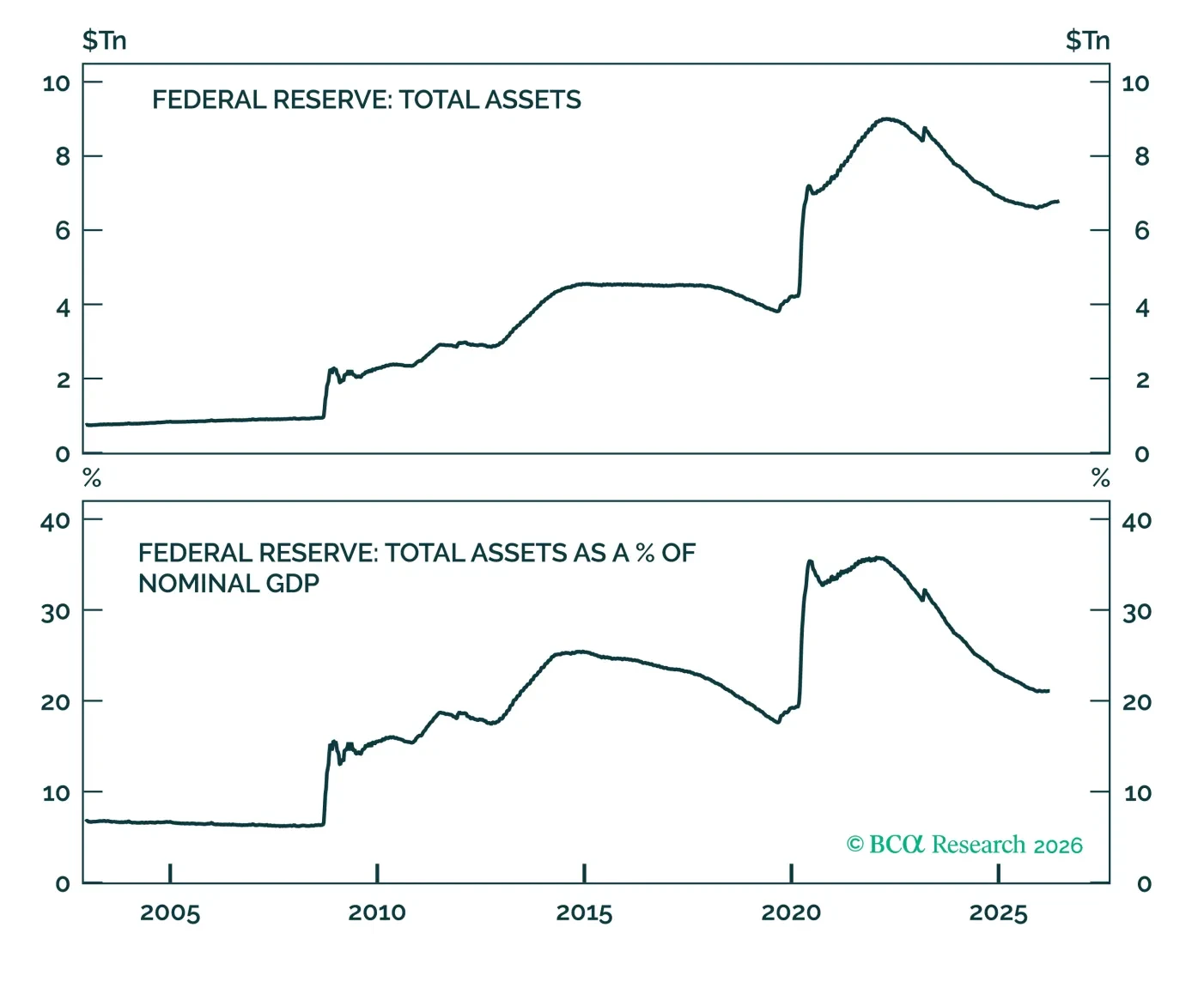

We discuss what recommendations to expect from the Fed’s balance sheet task force. We conclude that any future balance sheet consolidation will be smaller than many anticipate.

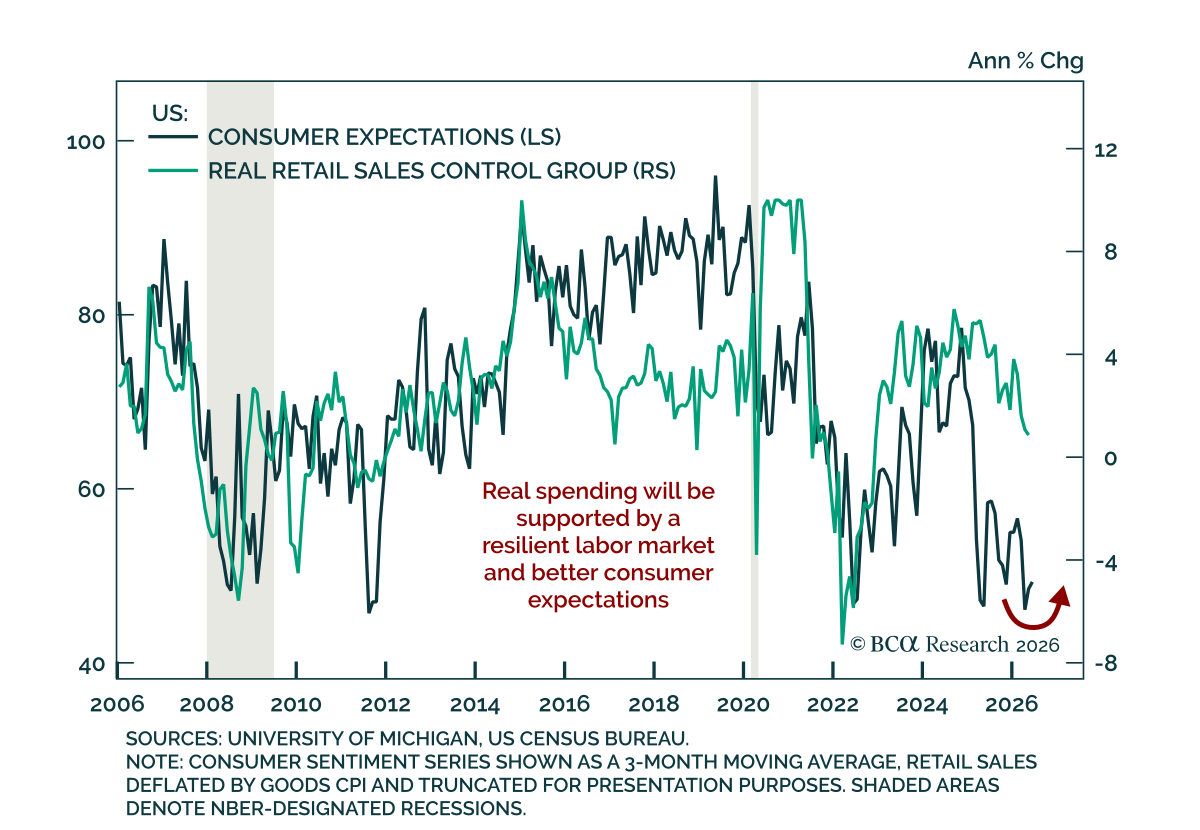

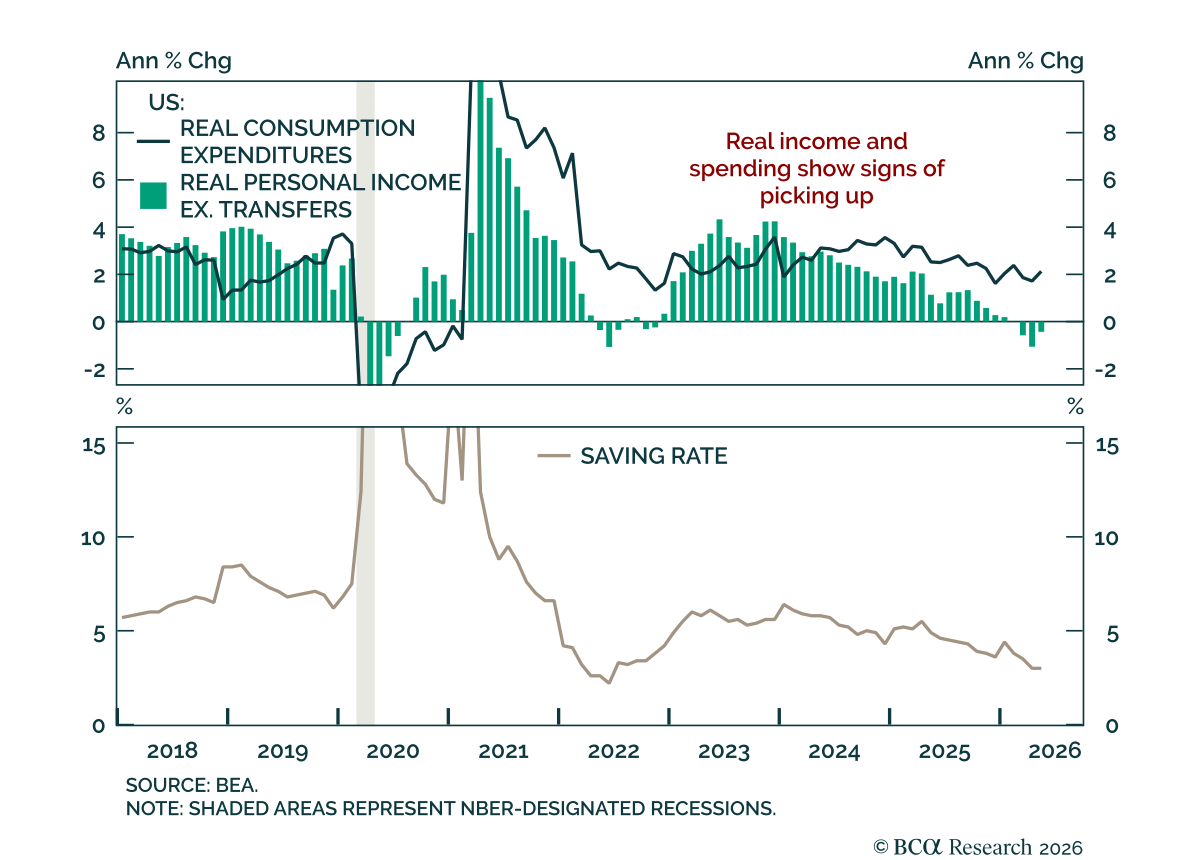

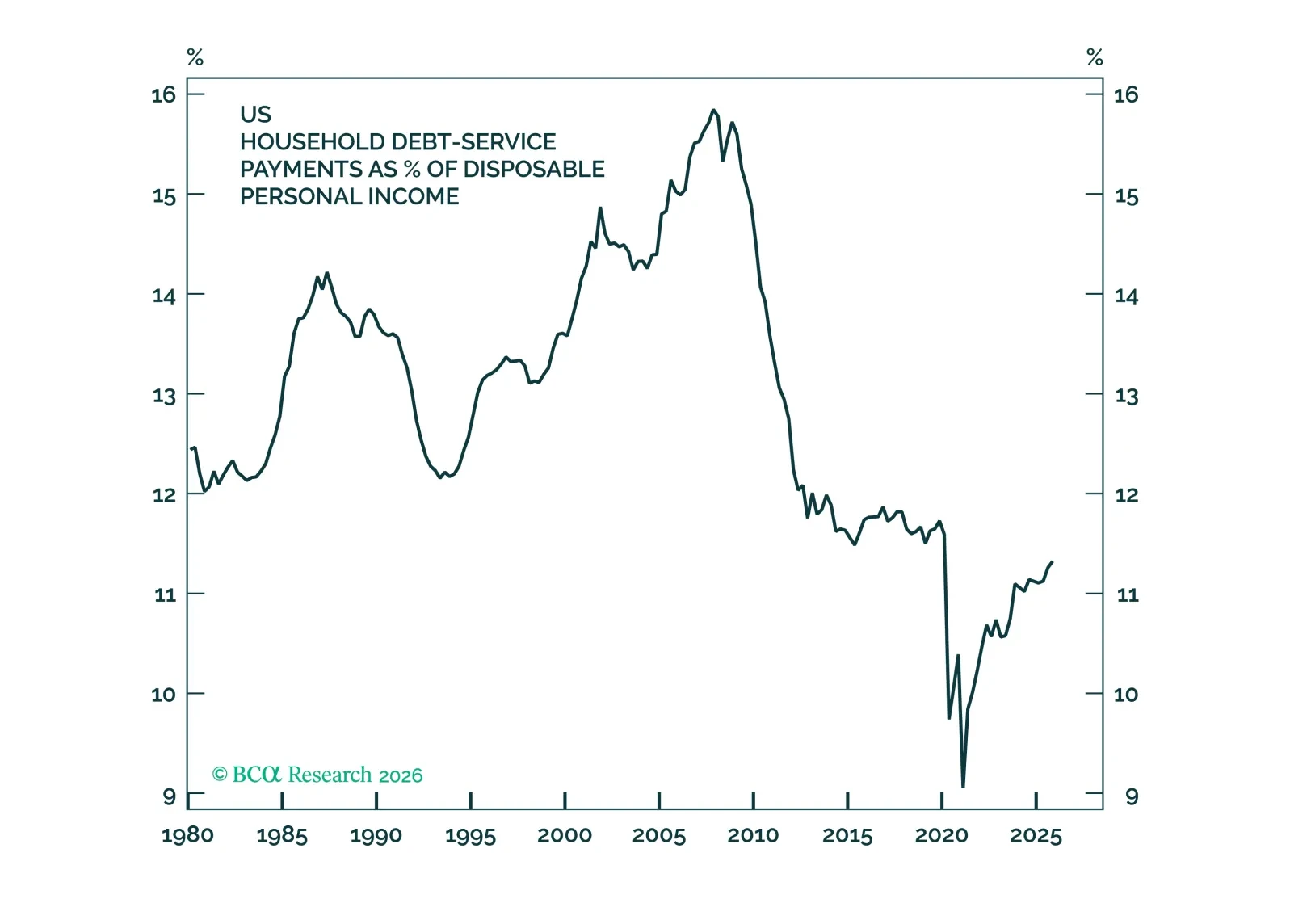

The most vulnerable households have whittled down their real debt balances while achieving significant real wealth gains. The combination has made consumption more resilient to income hiccups than in past cycles.

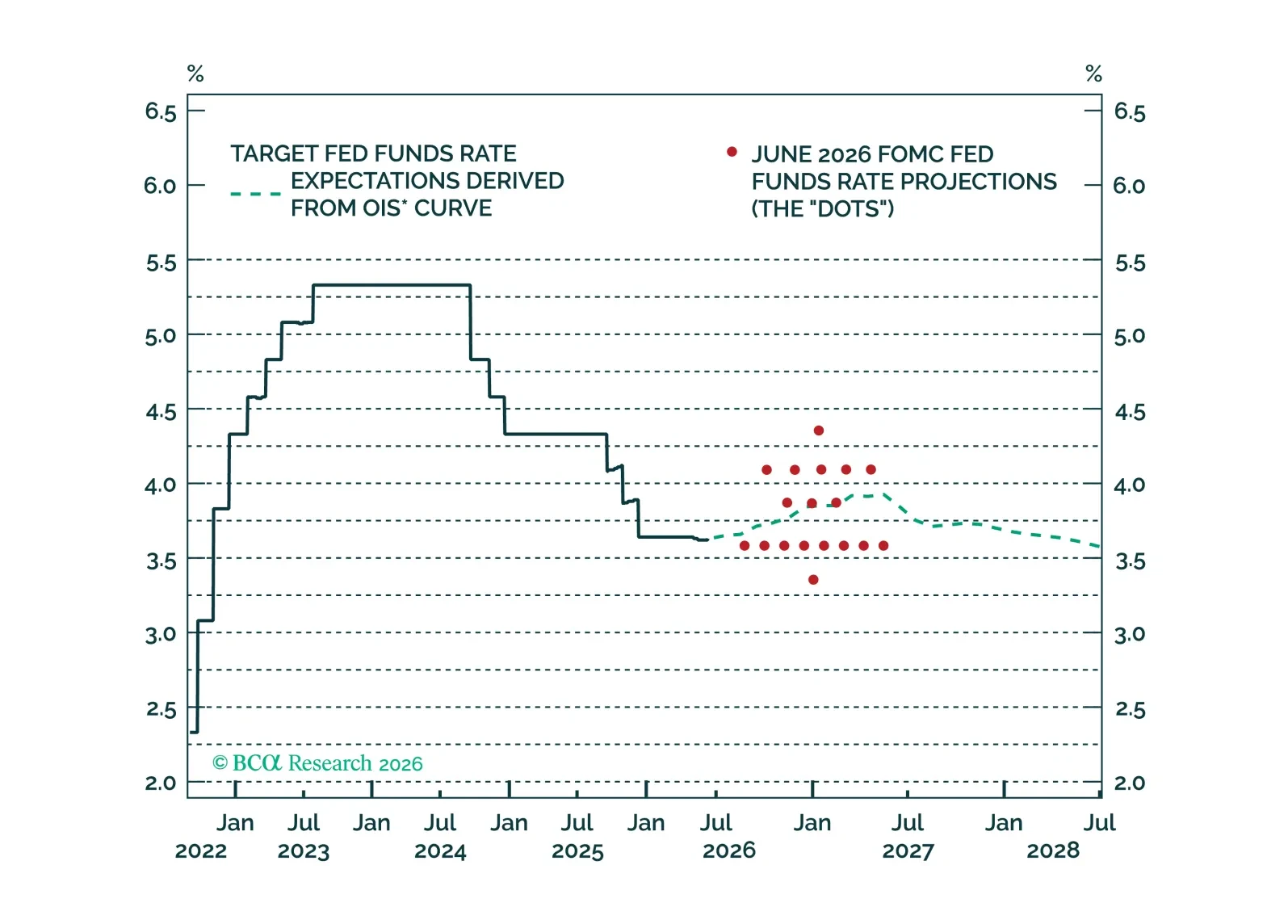

Kevin Warsh announced an ambitious reform agenda for the Federal Reserve. We discuss the potential impact and the current outlook for interest rates.