Economy

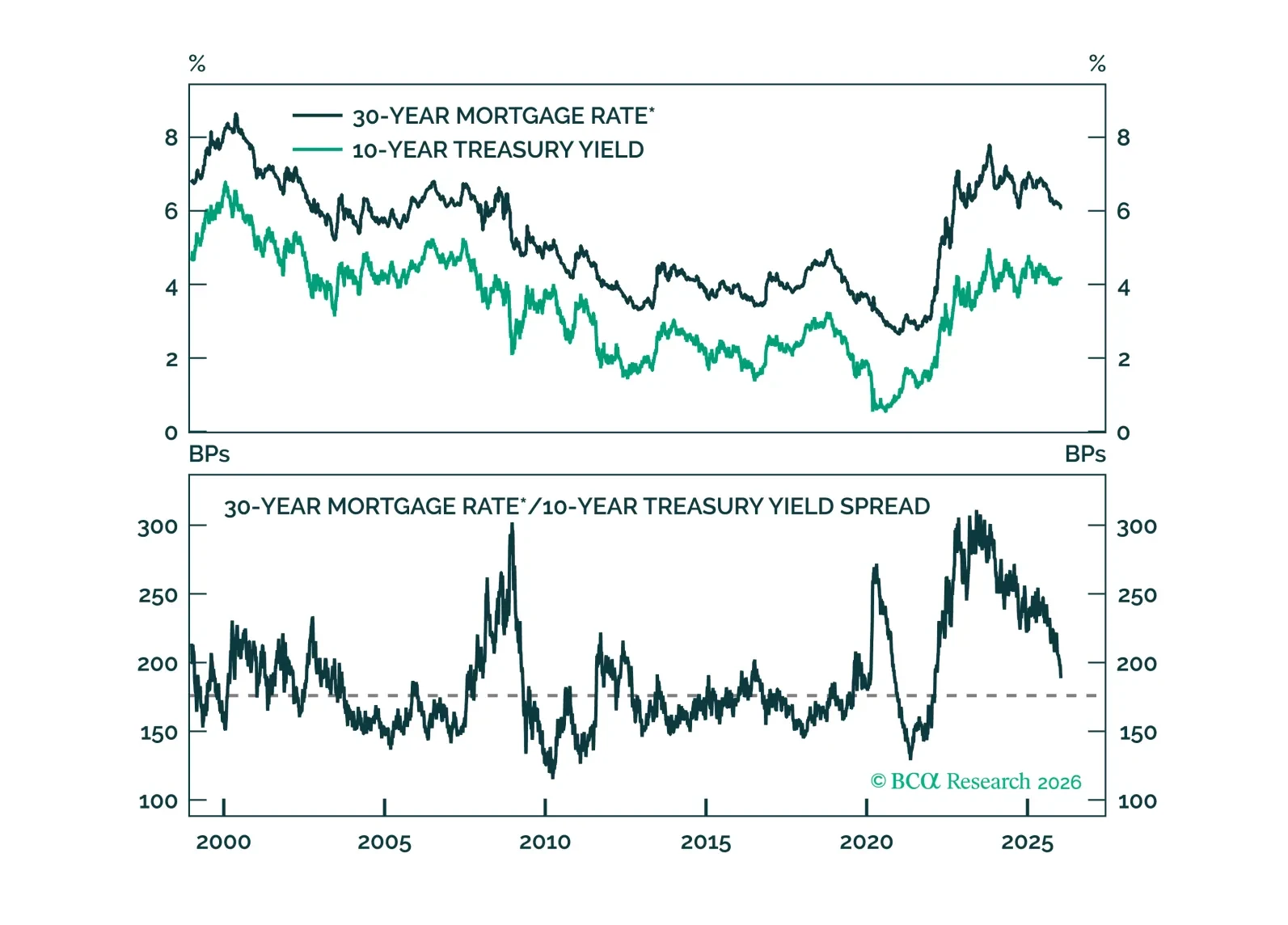

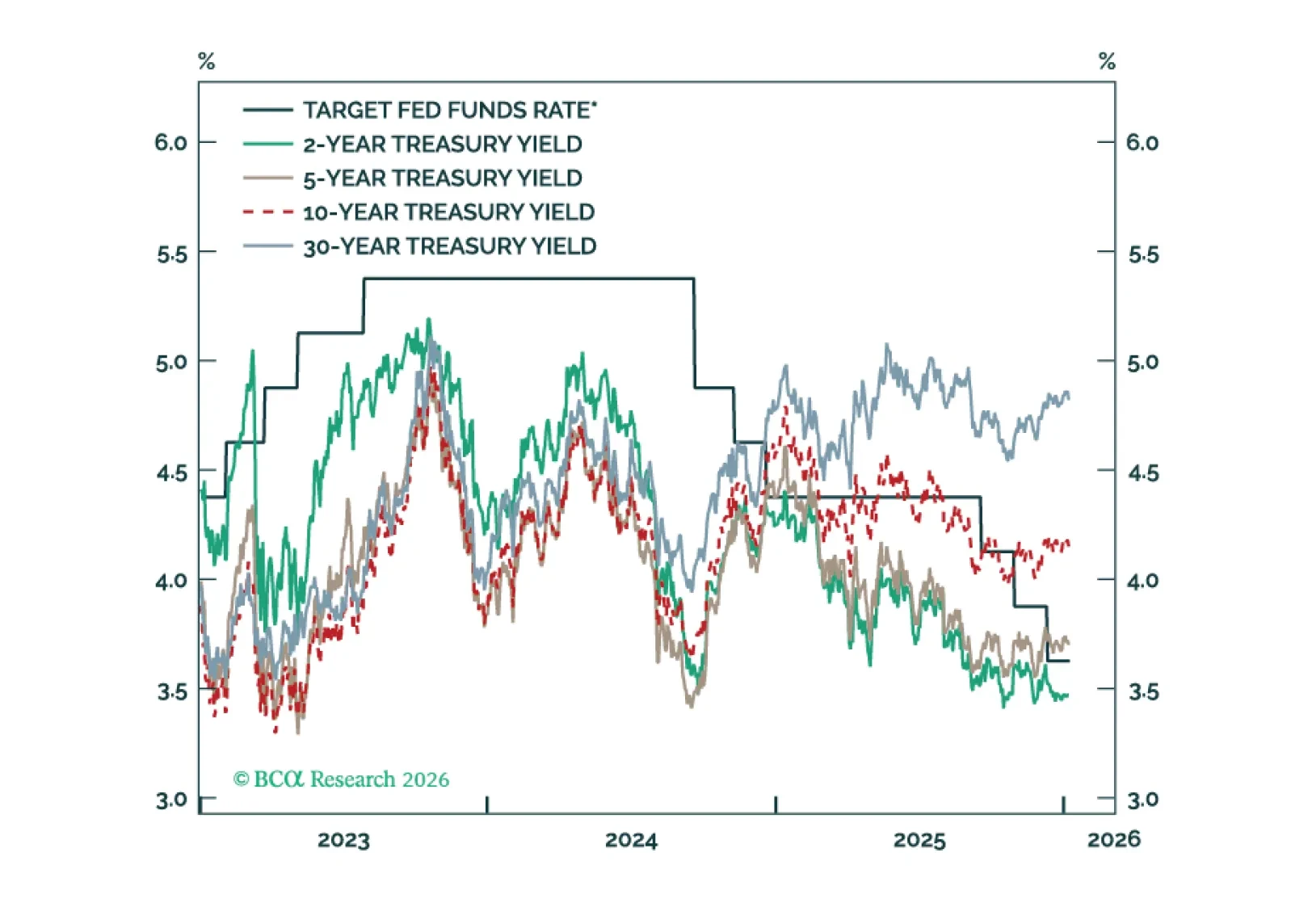

Mortgage spread tightening has run its course. Any further drop in mortgage rates will necessitate lower Treasury yields.

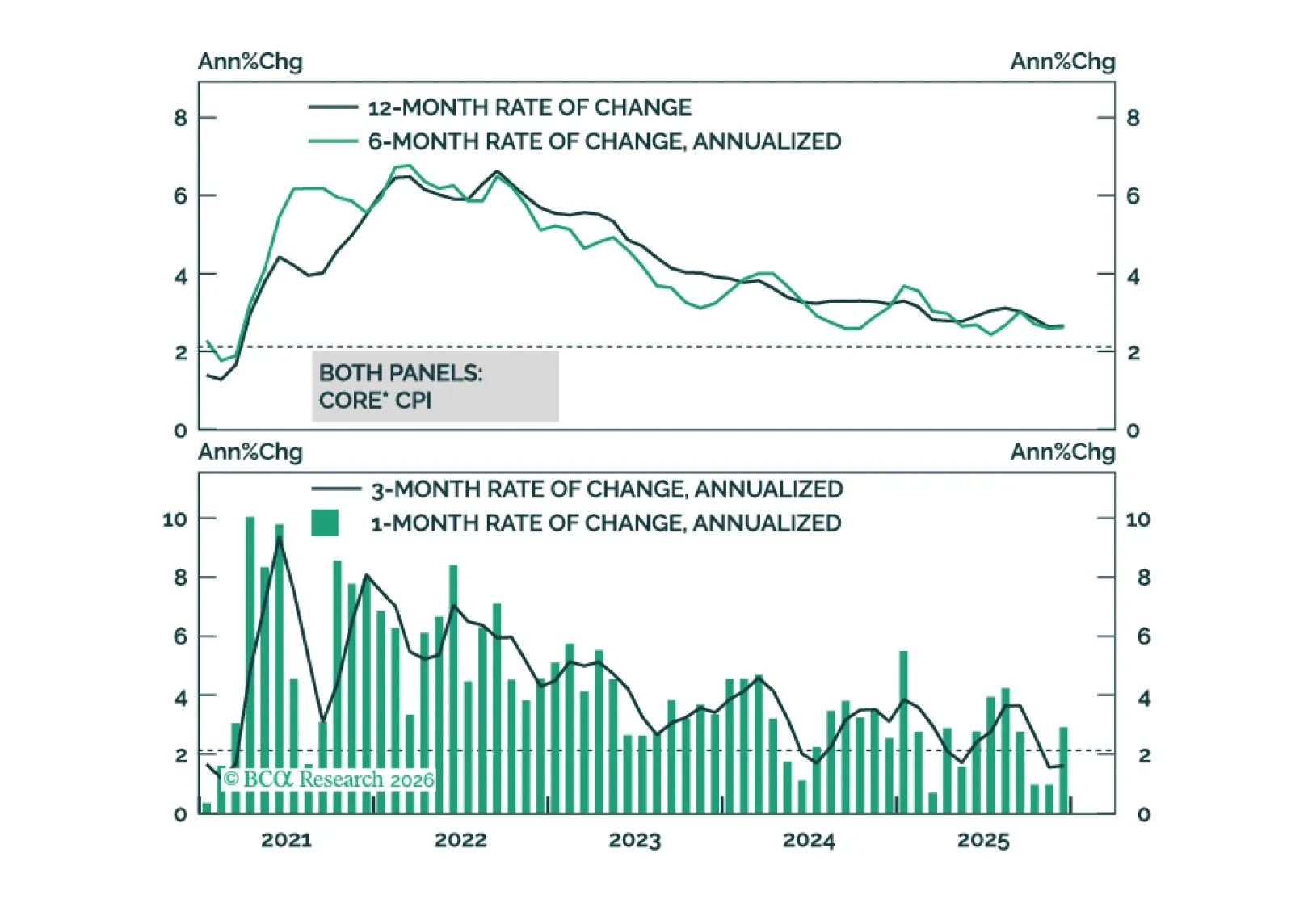

This morning’s CPI report signals that the worst of the tariff impact on inflation may already be in the rearview mirror.

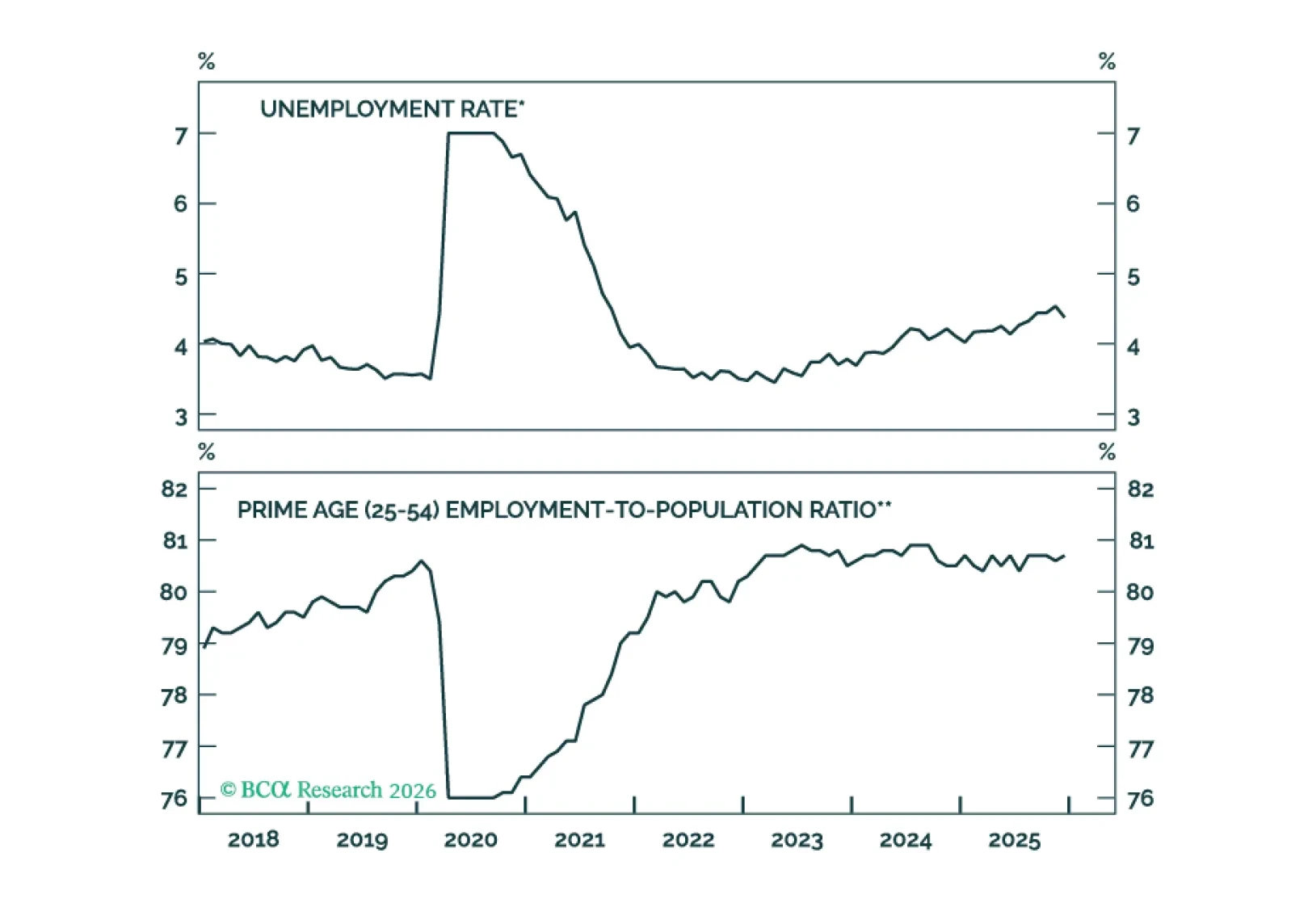

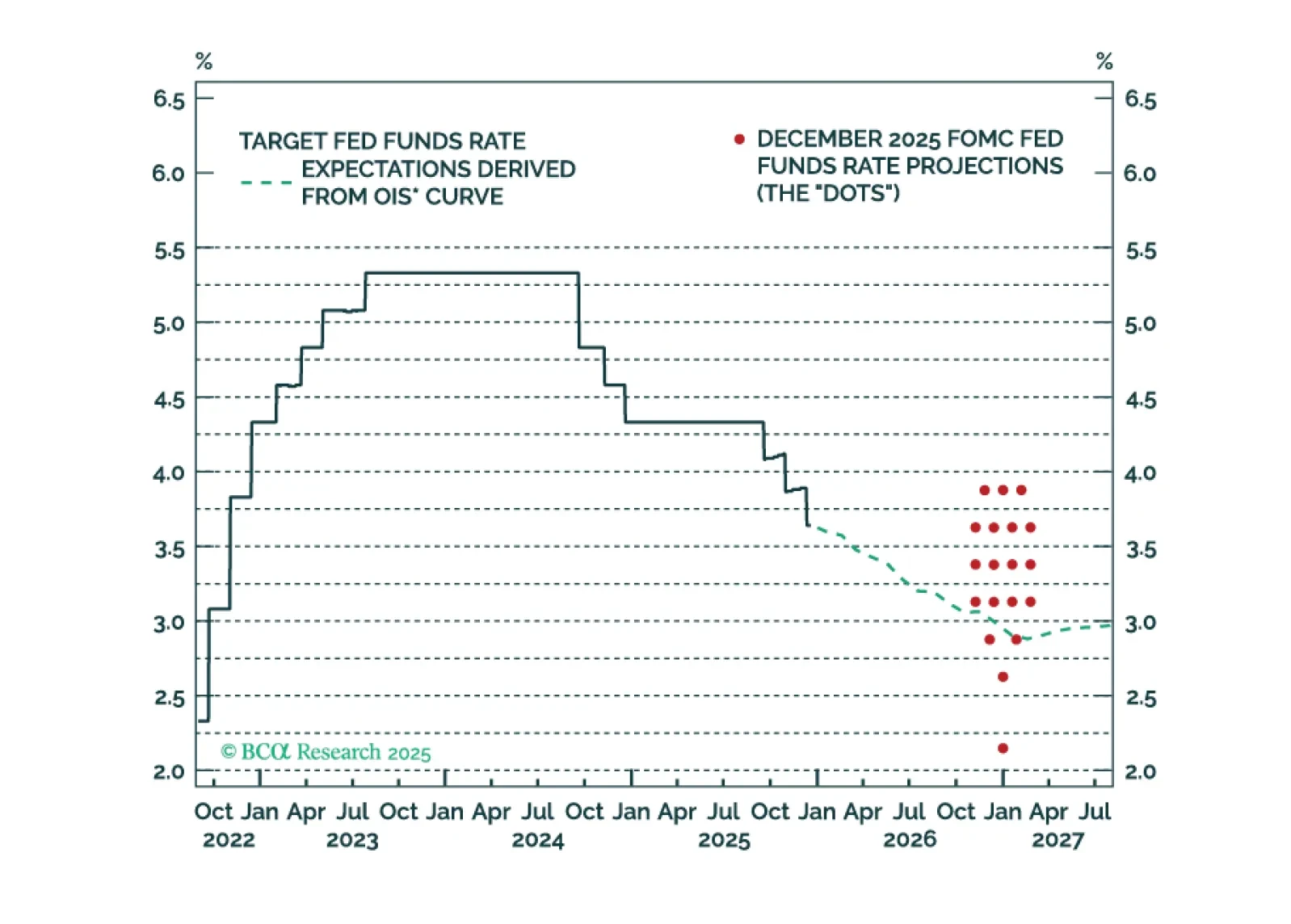

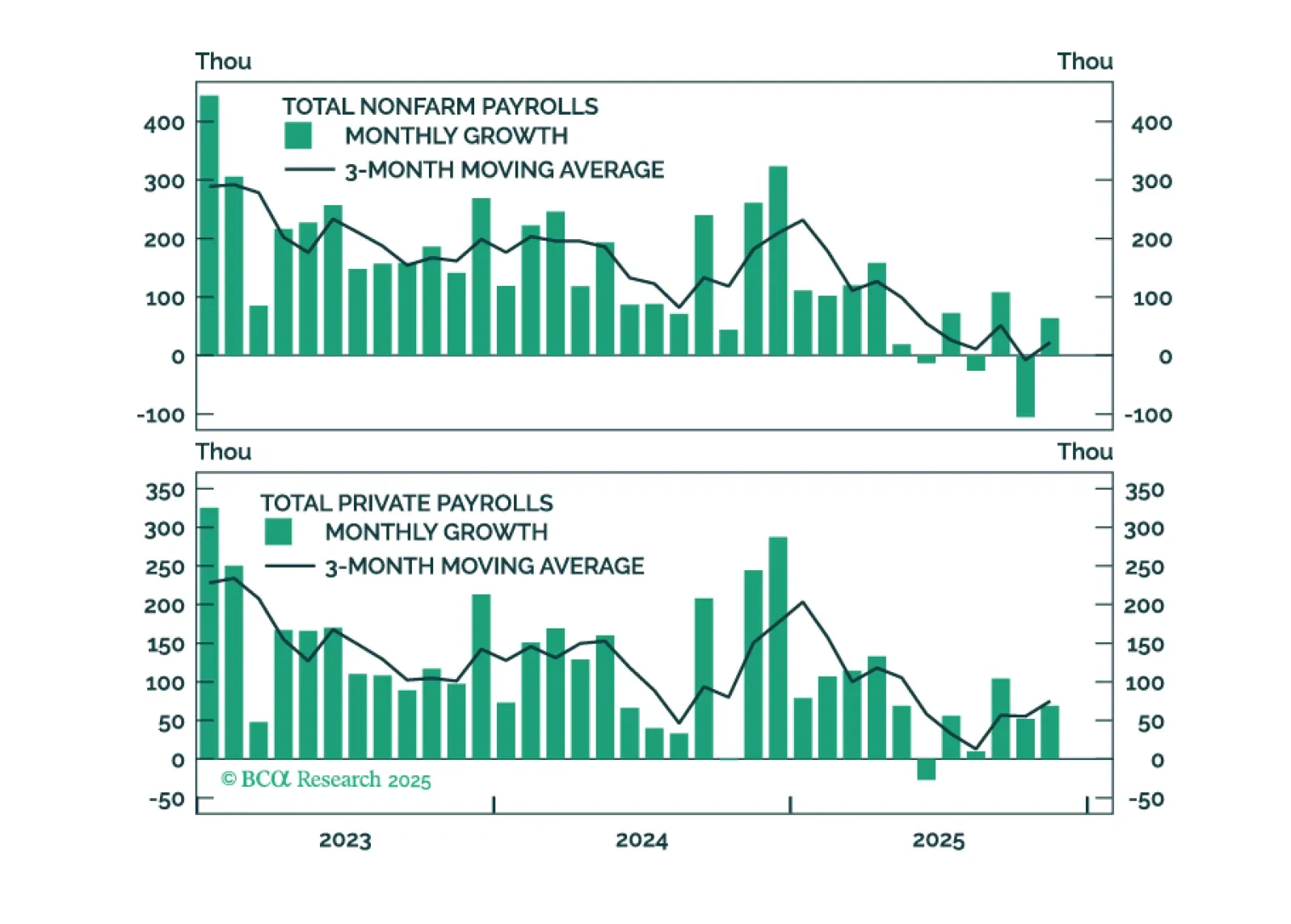

Measures of labor market utilization improved in December, ruling out a January cut and significantly reducing the odds of a March cut.

To start 2026, we answer what we believe are the most important questions facing investors surrounding the labor market, monetary and fiscal policy, and AI stocks. Overall, we reiterate our overweight views on risk assets and highlight the risks surrounding the upcoming tariff decision.

Our Portfolio Allocation Summary for January 2026.

Our outlook for Fed policy in 2026.

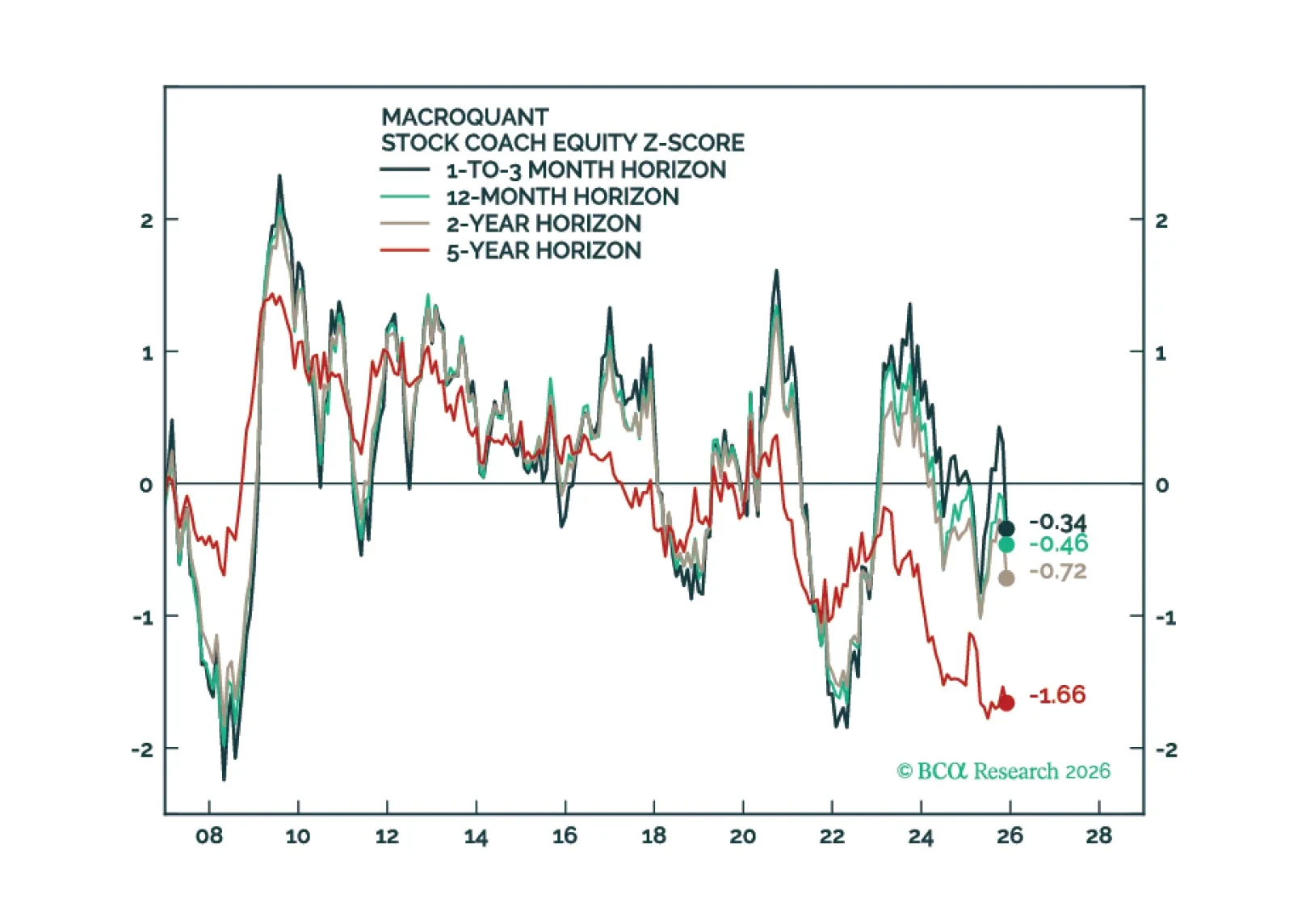

MacroQuant has downgraded equities to underweight, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is still bullish on gold.

Our outlook for Fed policy in 2026.

Every year, the Global Asset Allocation team compiles a list of our favorite books, essays, and articles from our strategists ahead of the holiday season. This year, we focus on writings by practitioners in the world of finance, business, and beyond. While diverse in their backgrounds, one theme stands out: Adaptation.

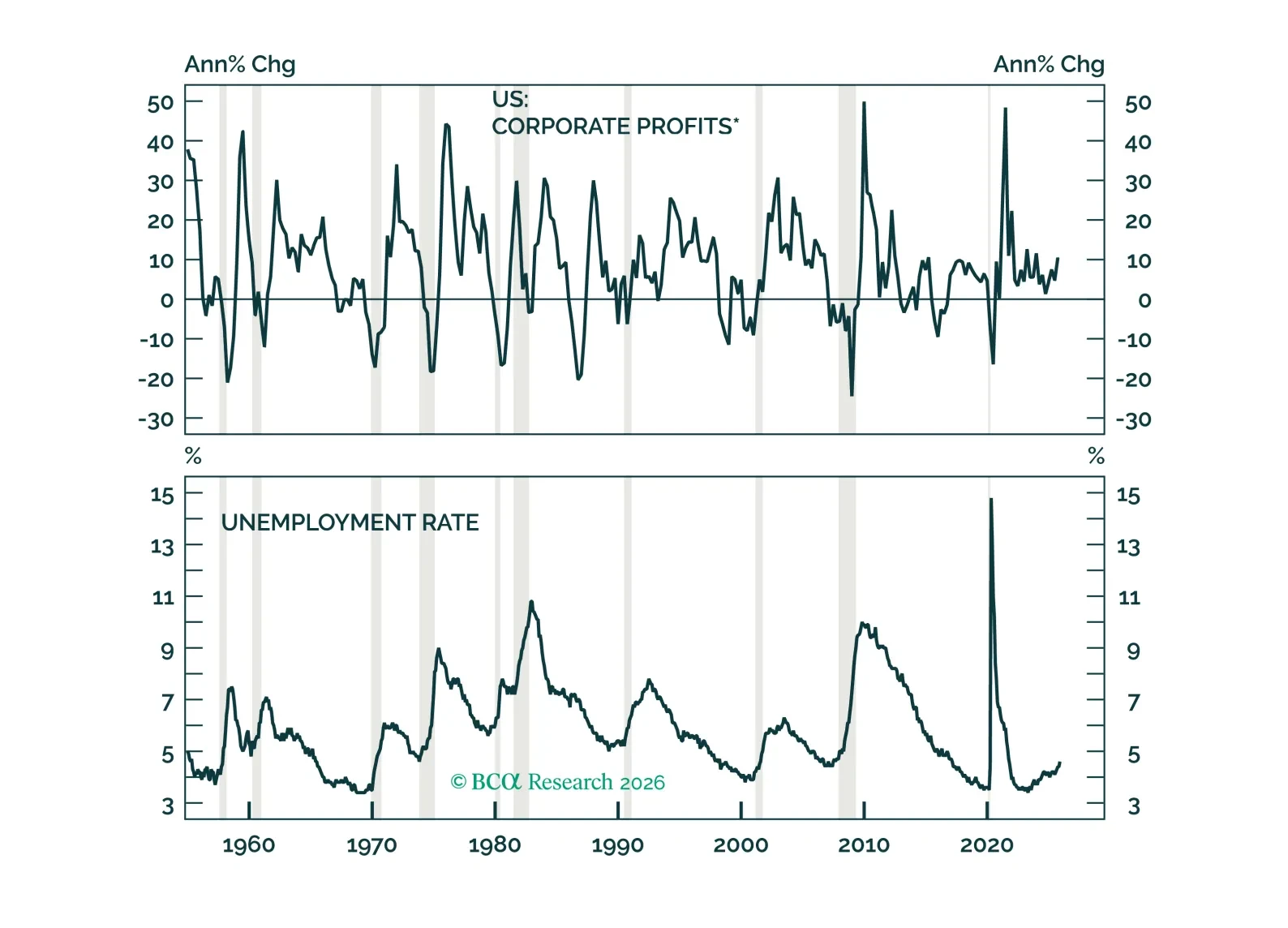

Employment Data Point To Dovish Policy Surprises In 2026