Economy

The Bank of Japan’s policy normalization has been accompanied by exceptional outperformance by Japanese banks. Japanese banks have outperformed both the country’s broader market as well as the MSCI ACW Banks index by 10.3% and 2.6%, respectively, so far this…

According to BCA Research’s Emerging Markets Strategy service, investor sentiment in Vietnamese markets has soured significantly since 2022, when the authorities' sweeping crackdown on alleged corruption in the real estate sector expanded to political…

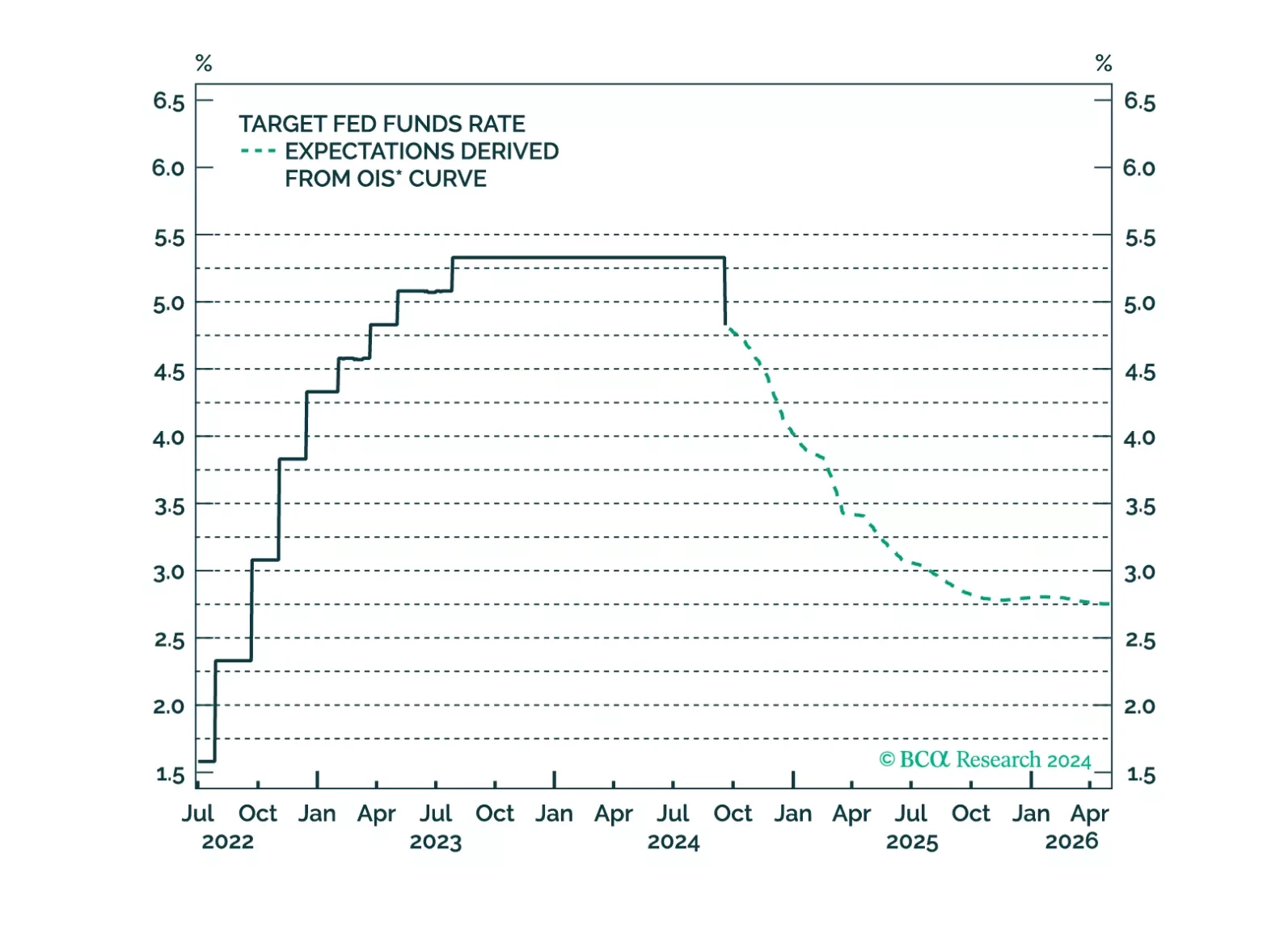

The 10-year Treasury yield rose in the aftermath of the Fed’s jumbo rate cut on Wednesday. Our US Bond strategists noted that this move reflects the fact that the downward revisions to the dots still fall short of the magnitude of cuts embedded in the…

Singapore is a small open economy sensitive to global trade dynamics. Its non-oil exports (NODX) are thus a good bellwether for global growth conditions. Overall exports, which are highly volatile on a month-on-month basis, decelerated at a…

One key takeaway from Wednesday’s post-FOMC press conference is the Fed’s unshaken conviction that it can avoid a recession. A risk-on mood dominated markets on Thursday, with the S&P 500 breaching new all-time highs while the 10-year Treasury yield rose…

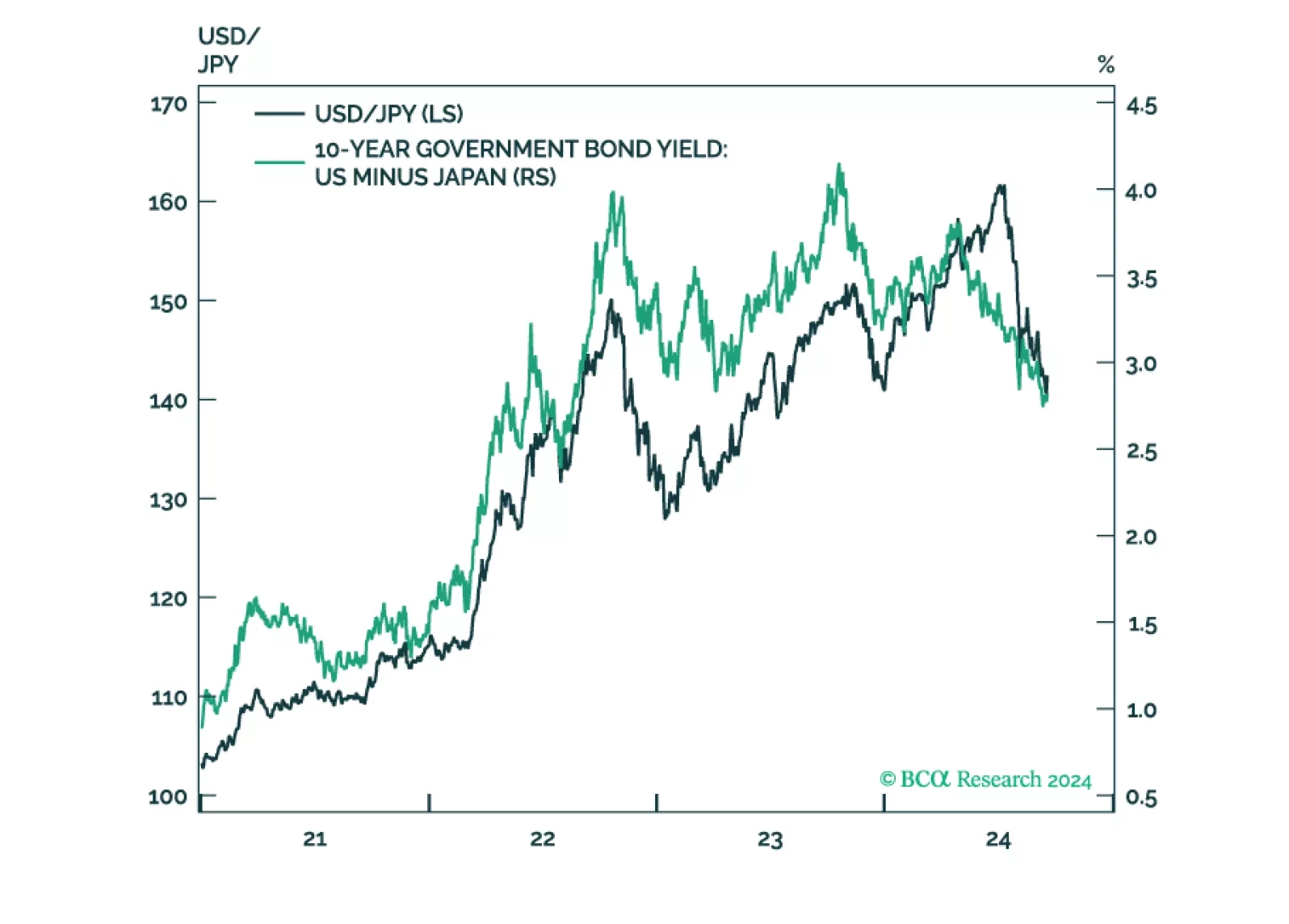

According to BCA Research’s Foreign Exchange Strategy and Global Investment Strategy services, most carry investors have covered their positions. Away from day-to-day noise, the longer-term trajectory of yen exchange rates will be driven by fundamentals. …

In this report, we argue that the Bank of Japan is unlikely to hike interest rates this week, but the relative trajectory of bond yields in Japan is higher. This warrants an underweight position in JGBs and a leveraged bet on a higher yen. The positioning for equity investors is murkier, as progress on corporate reforms is necessary for a rerating in Japanese shares. That is not yet very clear. The bottom line is: Stay long the yen.

We update our bond views following today’s 50 bps rate cut.

Despite the recent correction, US equity leadership remains intact. The MSCI US index has outperformed global markets by 3.8% in 2024YTD. A 7.8% expansion in forward earnings drove the MSCI US index’ 2024YTD gains which was higher than the increases in…