Economy

The Fed started its easing cycle with a bang, cutting the policy rate by 50 basis points in September, above consensus expectations but in line with odds embedded in the futures and OIS curves. Our US Bond strategists had highlighted it is unusual for the…

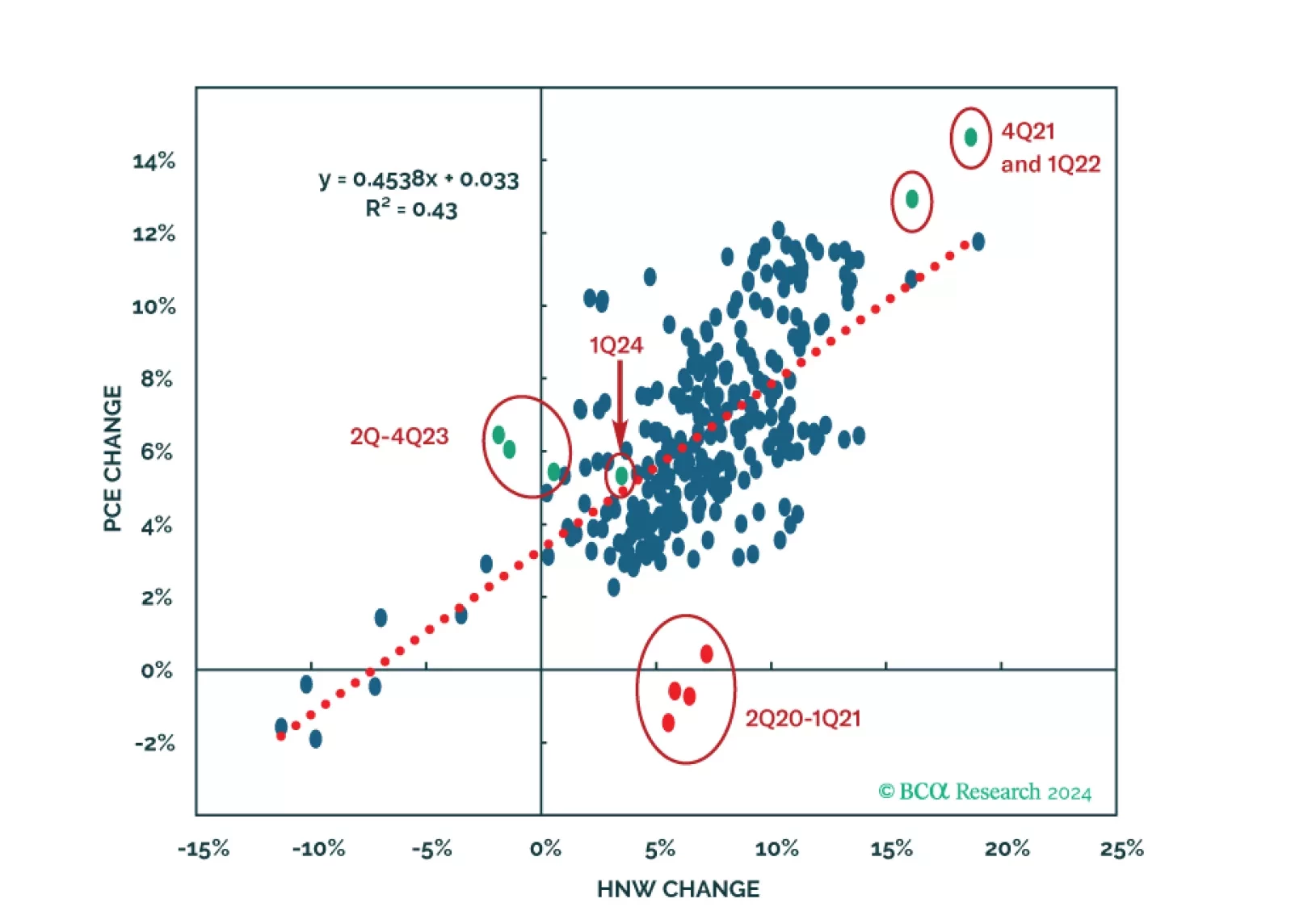

Stress among lower-income households is often cited as an early indication of deteriorating aggregate consumer fundamentals. The data indeed suggests that this cohort’s cash holdings are depleting. However, the Fed’s quarterly estimates of household wealth…

Despite the recent correction, US equity leadership remains intact. The MSCI US index has outperformed global markets by 3.8% in 2024YTD. A 7.8% expansion in forward earnings drove the MSCI US index’ 2024YTD gains which was higher than the increases in…

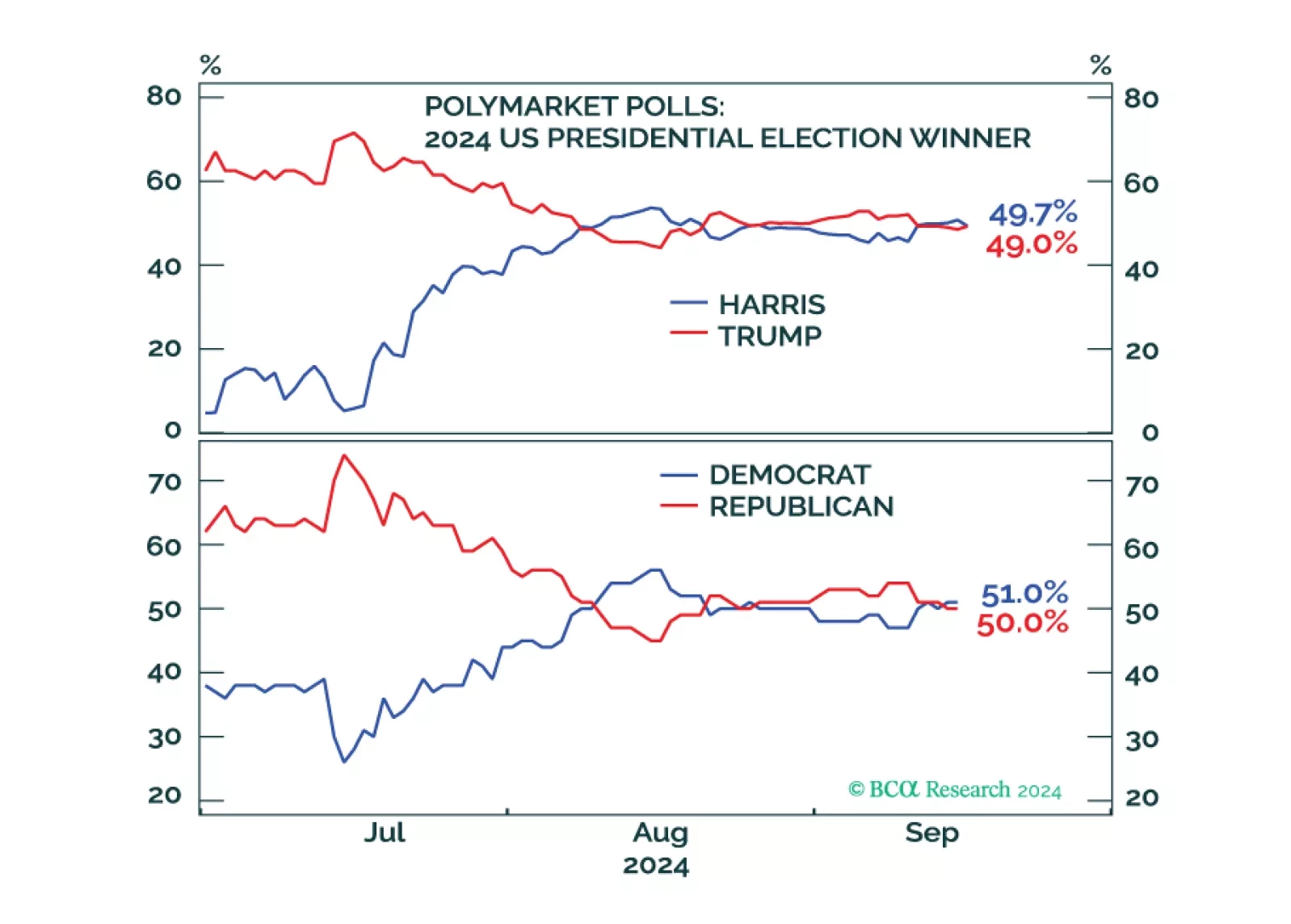

According to BCA Research’s Geopolitical Strategy service, seven surprises with non-negligible odds could tip the scale in favor of Republicans for the White House by November 5. One of them is a war between Israel and Iran. Iran is still highly likely to…

US retail sales grew 0.1% m/m in August and beat expectations of a 0.2% monthly contraction. The positive surprise seemingly spurred equity market gains on Tuesday morning. However, details do not paint as rosy a picture as the headline number…

Canadian headline CPI inflation decelerated at a faster-than-anticipated pace from 2.5% y/y to 2.0% in August, the slowest since 2021. Notably, core median and trimmed-mean CPI ticked 0.1 ppt and 0.3 ppt lower to 2.3% and 2.4%, respectively. Lower oil…

The ZEW survey of both German business expectations and current situation largely disappointed in September, decreasing by 15.6 points to 3.6 and by 7.2 points to -84.5, respectively. The ZEW survey of expectations for the broader Eurozone also fell…

Stocks are a forward discounting mechanism and routinely top before recessions begin, even if they typically do not swoon until the recession has taken hold. According to BCA Research’s US Investment Strategy service, if consumers were losing momentum and a…

This Special Report examines the post-pandemic evolution of consumption growth, relative equity sector and subindustry performance and recent commentary from consumer-facing companies to assess the likelihood that softer spending among lower-income households will spread to middle- and upper-income households.

Investors should de-risk tactically in expectation of shocks and surprises ahead of the US election and an uncertain aftermath. Democratic victory with a gridlocked Congress is our base case but would bring minor tax hikes and nuclear brinksmanship with Russia. A Republican single-party sweep offers huge tax cuts but also a global trade war. Recession looms regardless.