Economy

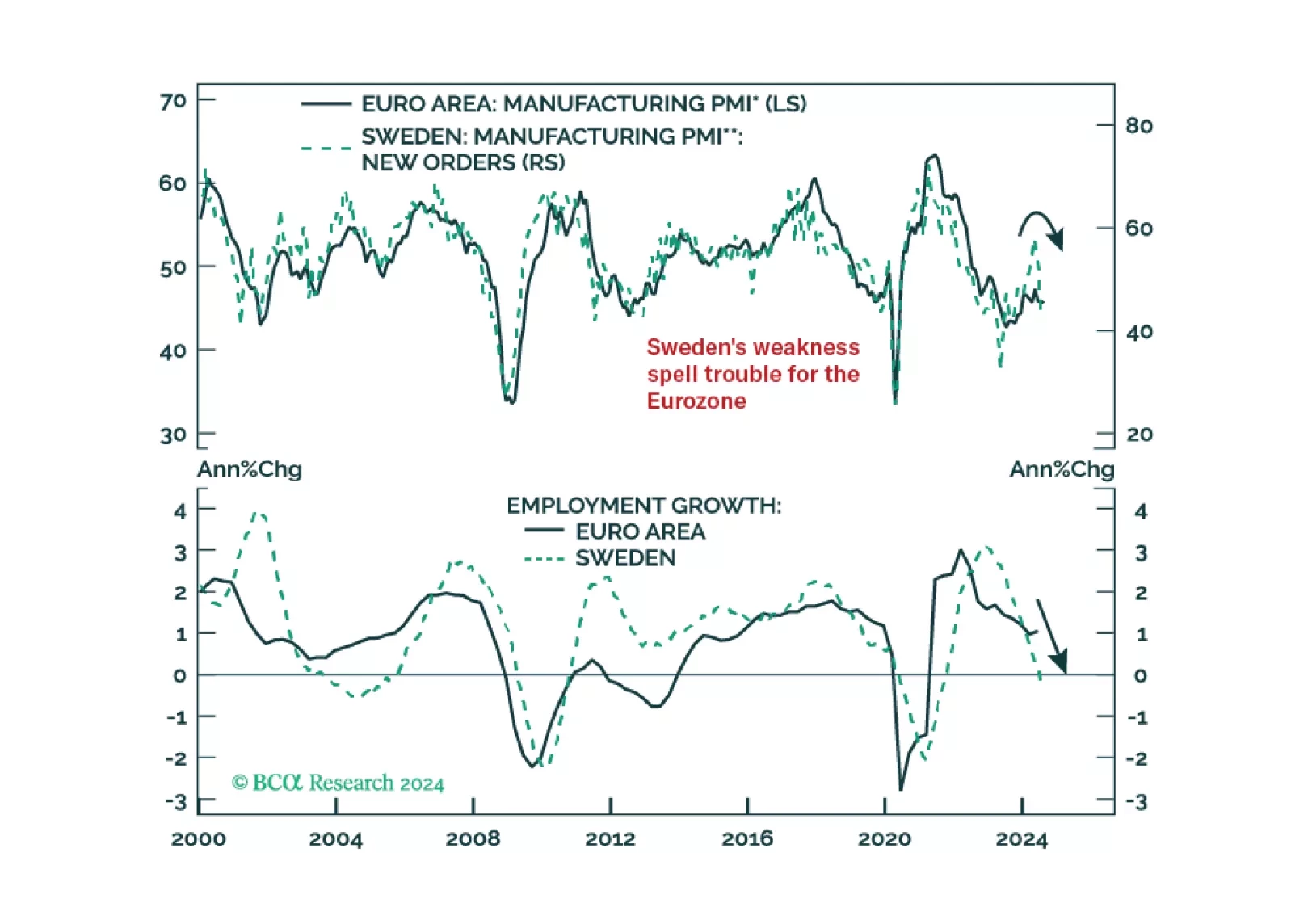

Our negative stance on European growth and assets is not devoid of risks. To gauge whether these risks warrant upgrading our growth outlook, we monitor Sweden closely. So, what is the current message from this Nordic economy?

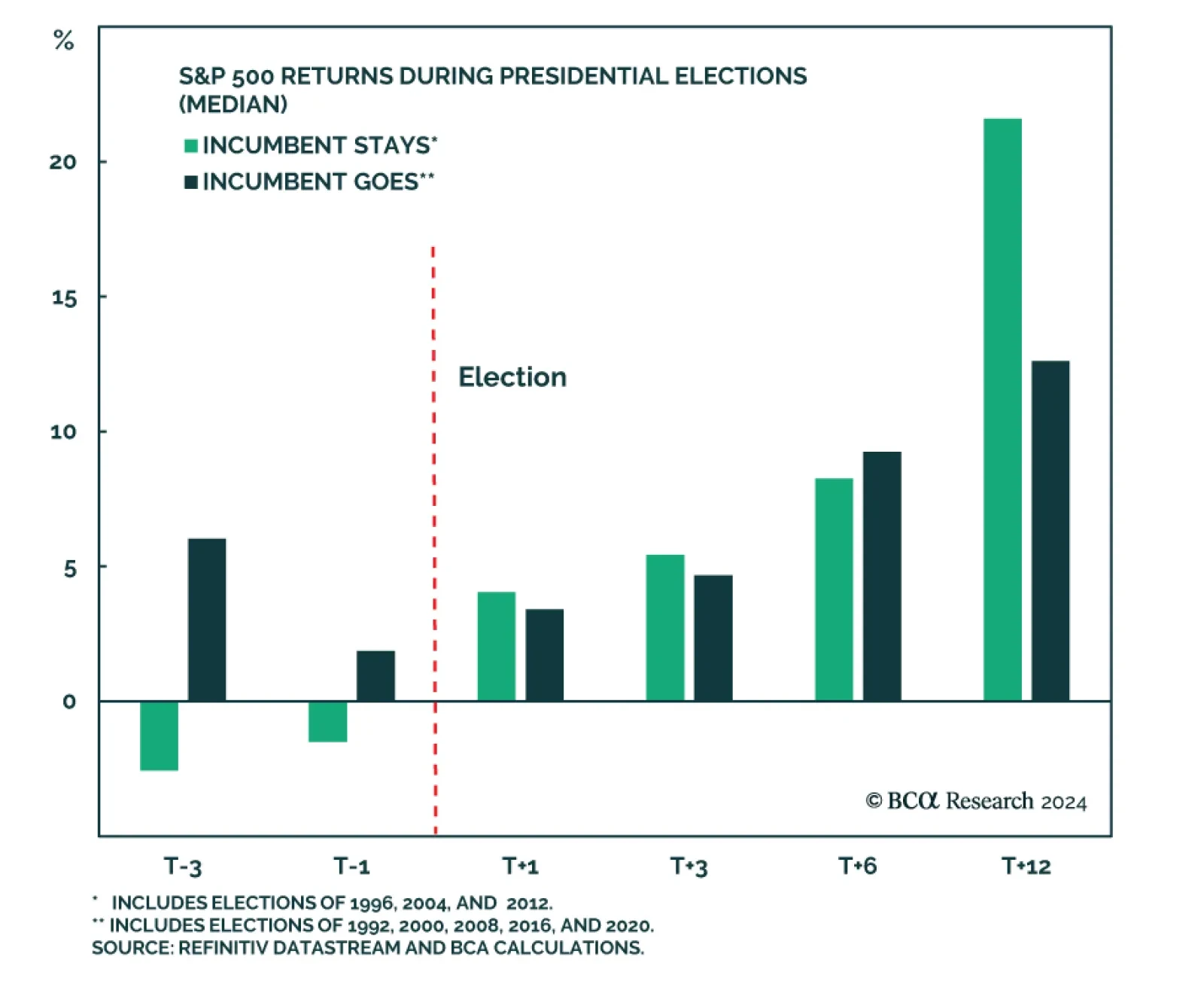

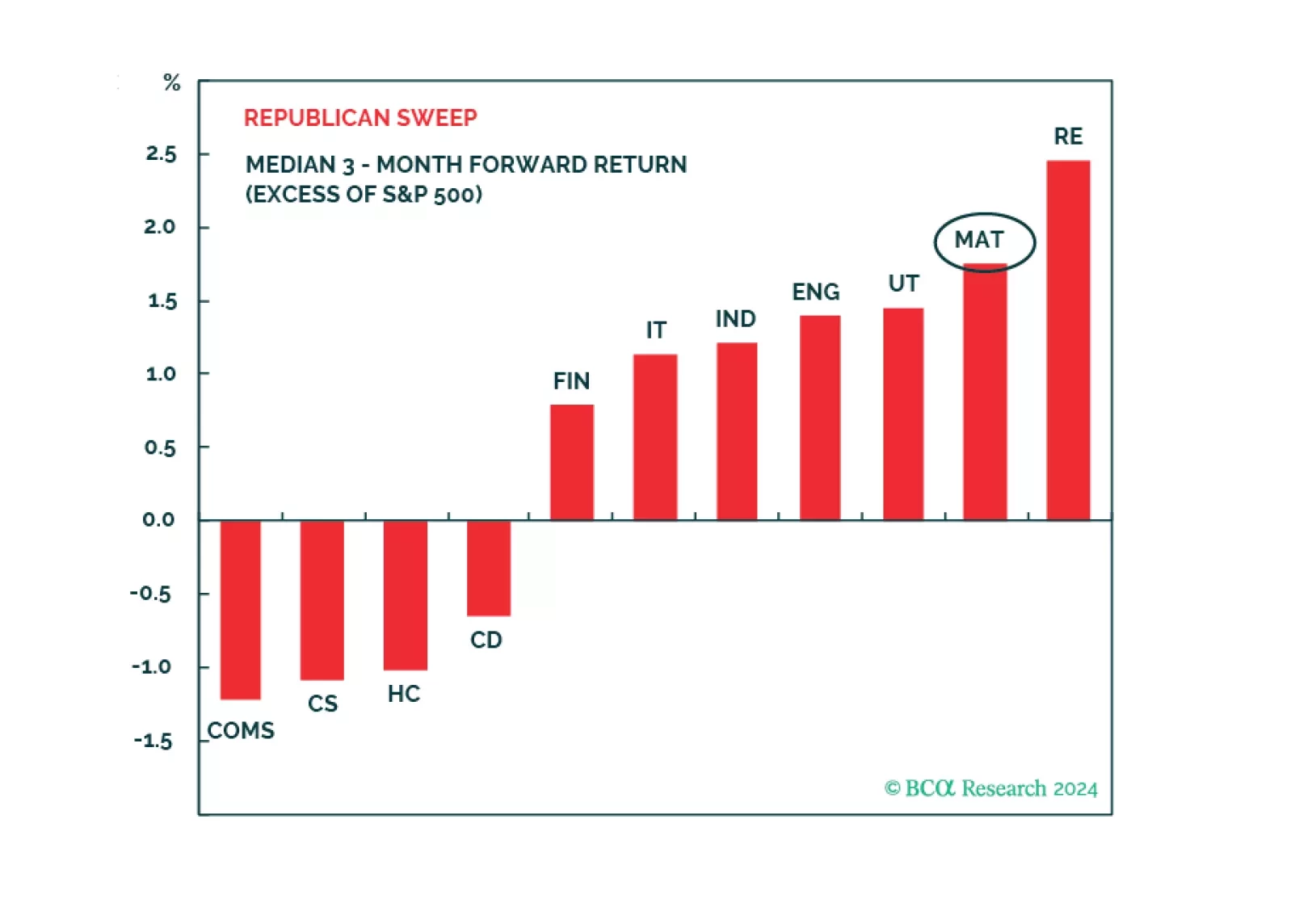

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.

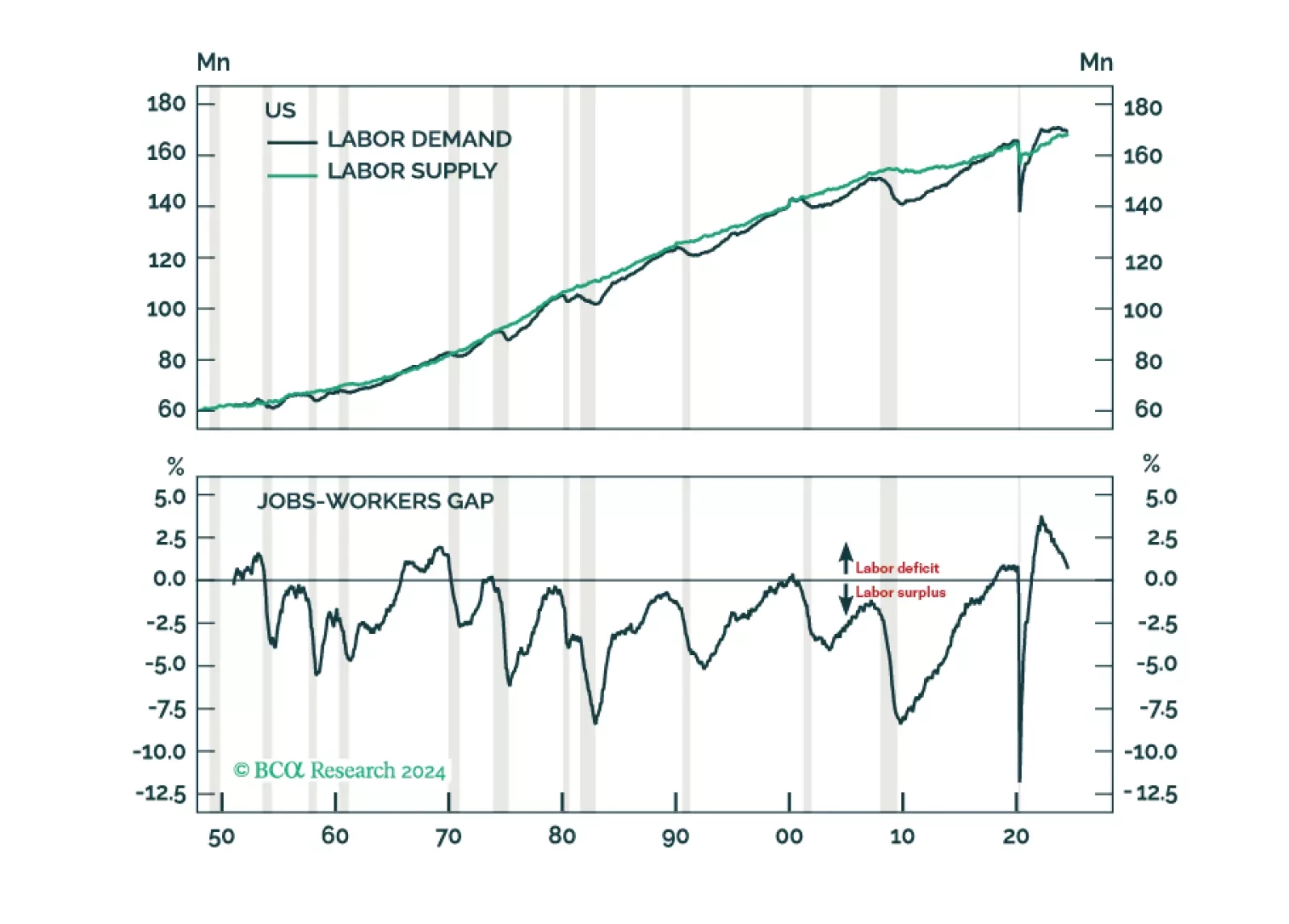

The great US labor market shortage is over. Labor demand will likely fall short of supply by the end of this year, causing unemployment to soar. Neither fiscal nor monetary policy will be able to prevent the coming recession. Investors should underweight stocks and overweight Treasuries.

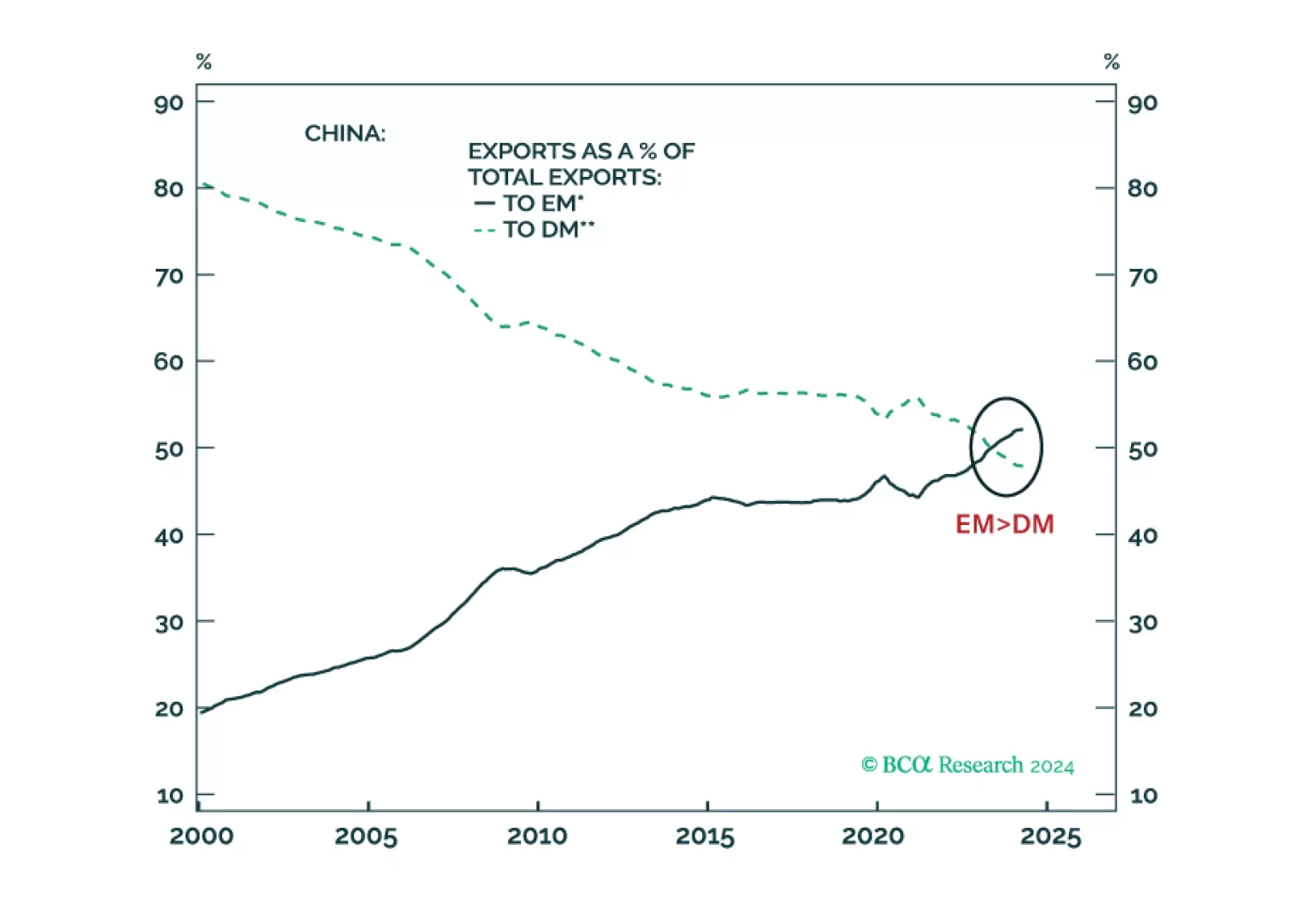

China has become less reliant on exports to advanced economies, and its products have successfully penetrated developing economies. Exports to the US make up 3% of Chinese GDP, while exports to all developing economies account for 10% of its GDP. China’s trade pivot from advanced to developing economies has economic, political, and geopolitical ramifications.

In this Special Report, we assess the impact of monetary policy tightening on major economies. Interest rate sensitive GDP already slowed significantly in response to the aggressive rate hiking cycle. Despite the beginning of policy easing, our forward-looking indicators suggest monetary policy will continue to weigh on the economy.