Economy

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

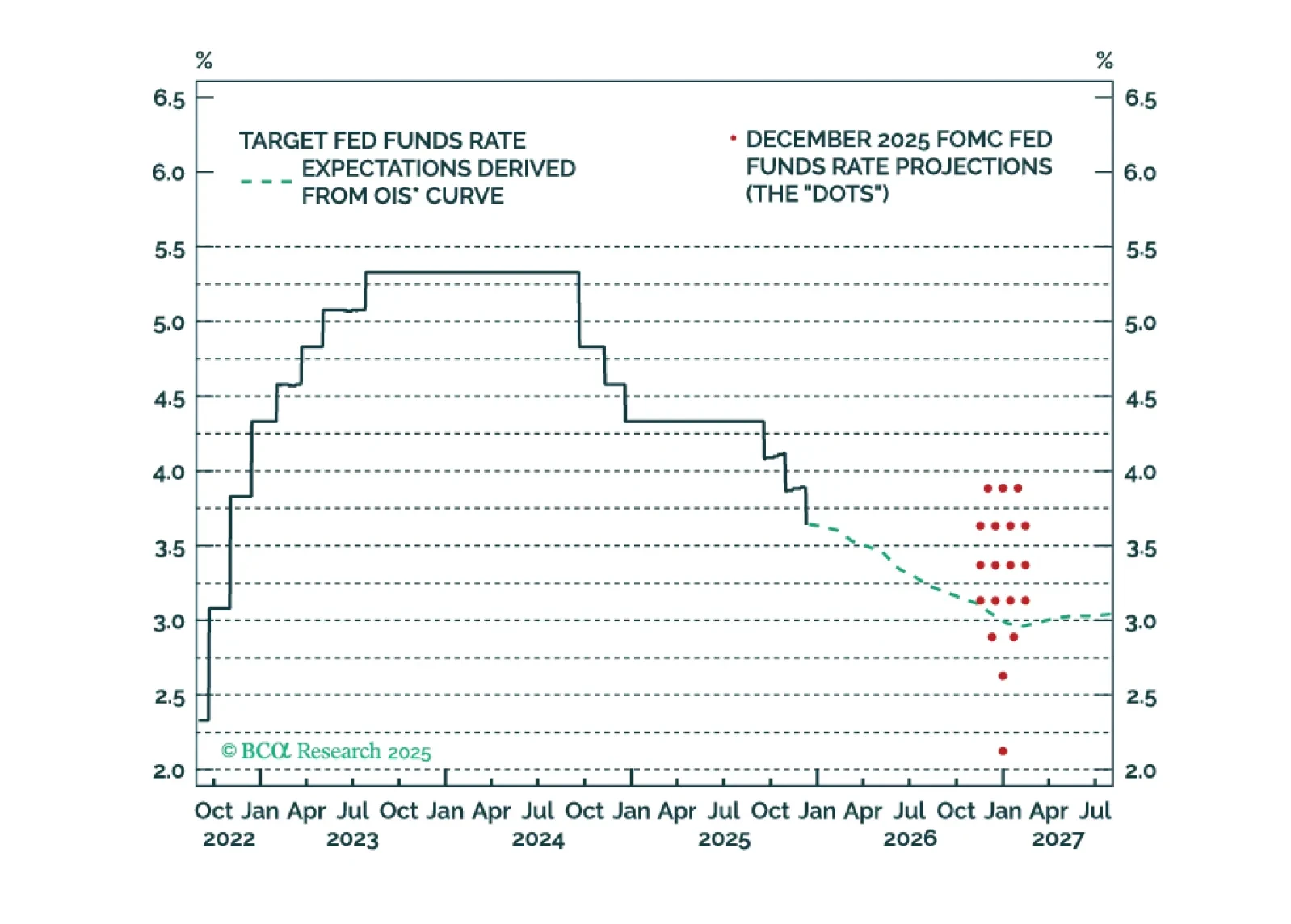

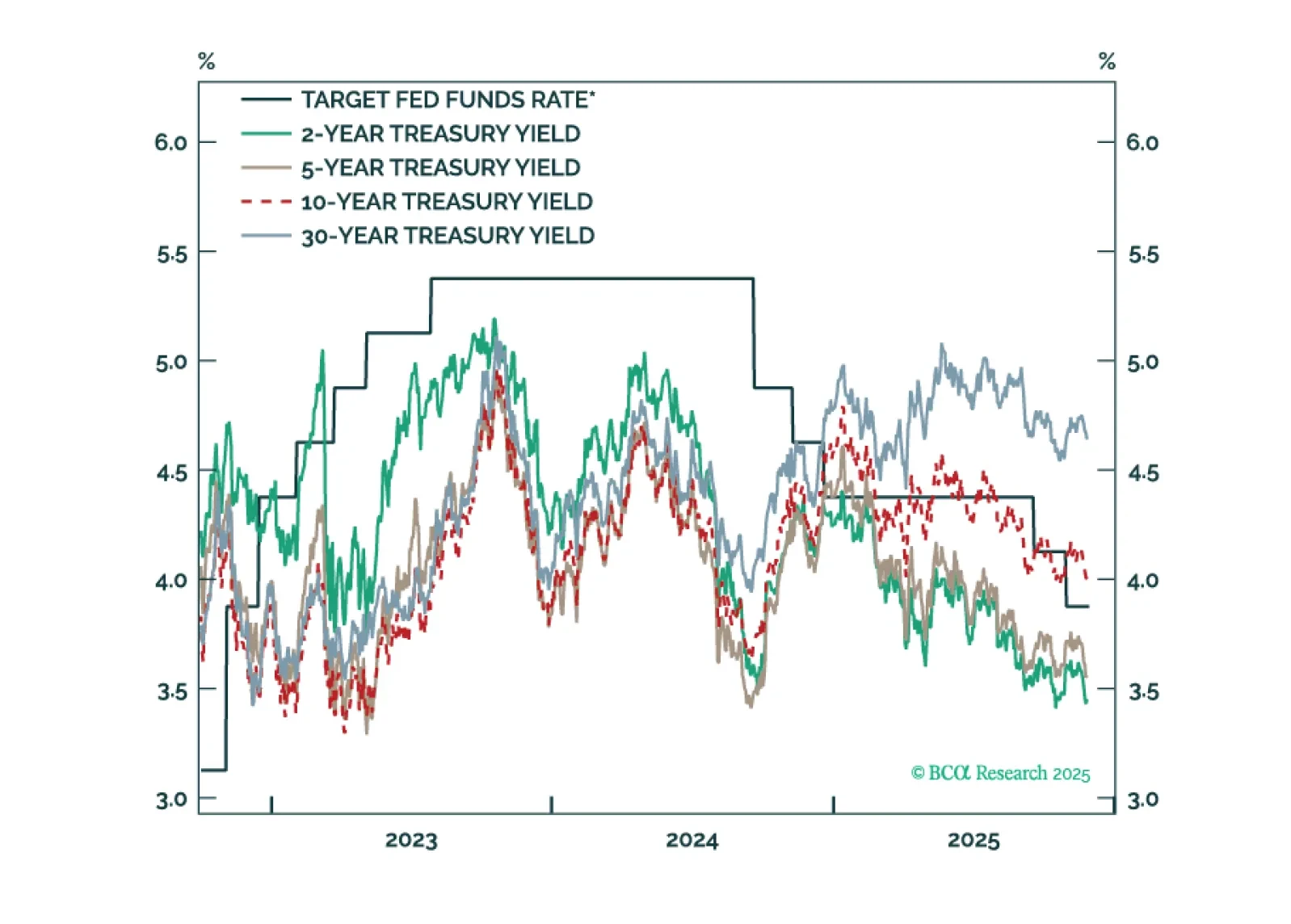

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

Our 2026 Outlook presents our five key views for Europe’s macro landscape and markets in 2026 —a year poised to reveal the true strength of the recovery.

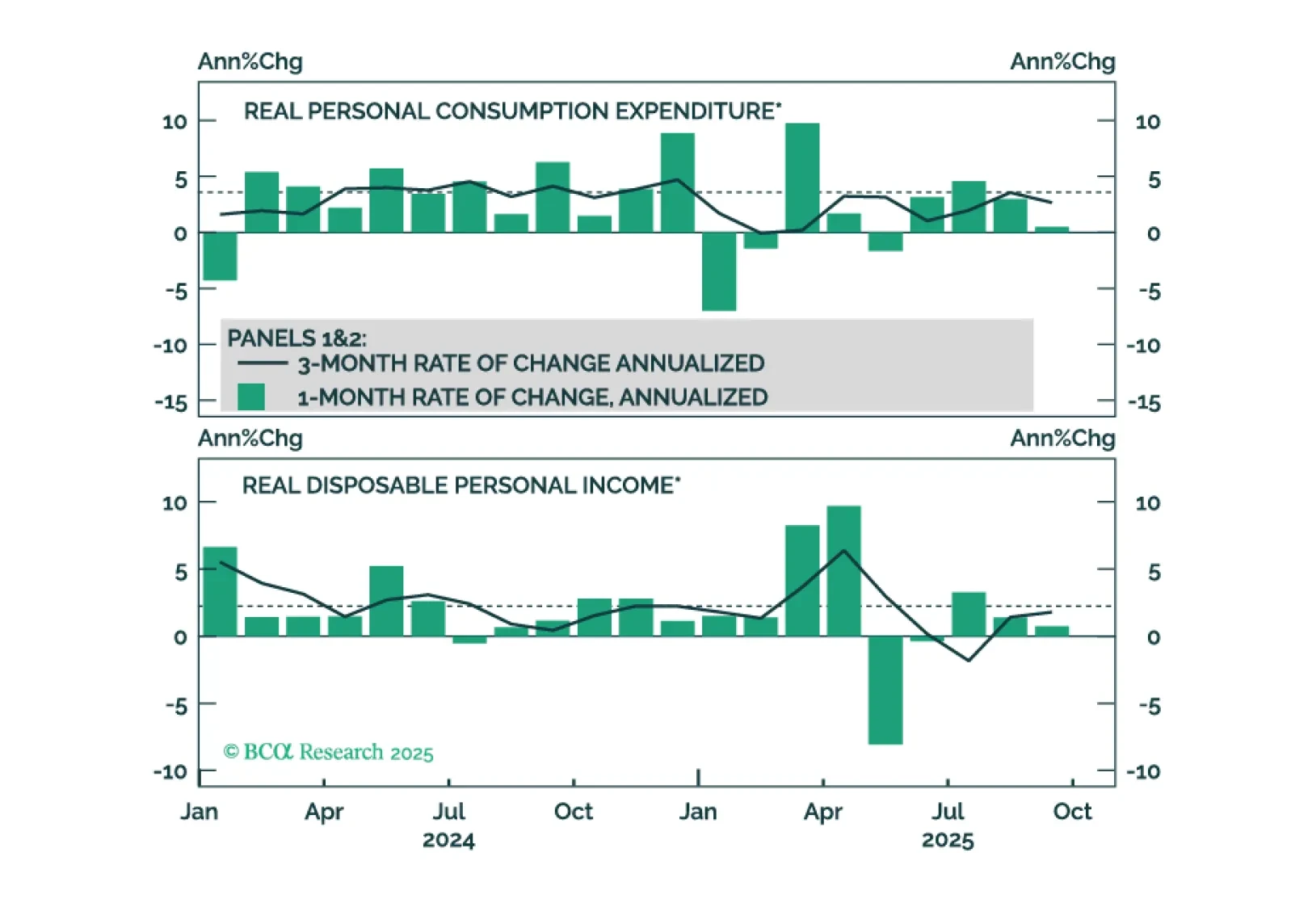

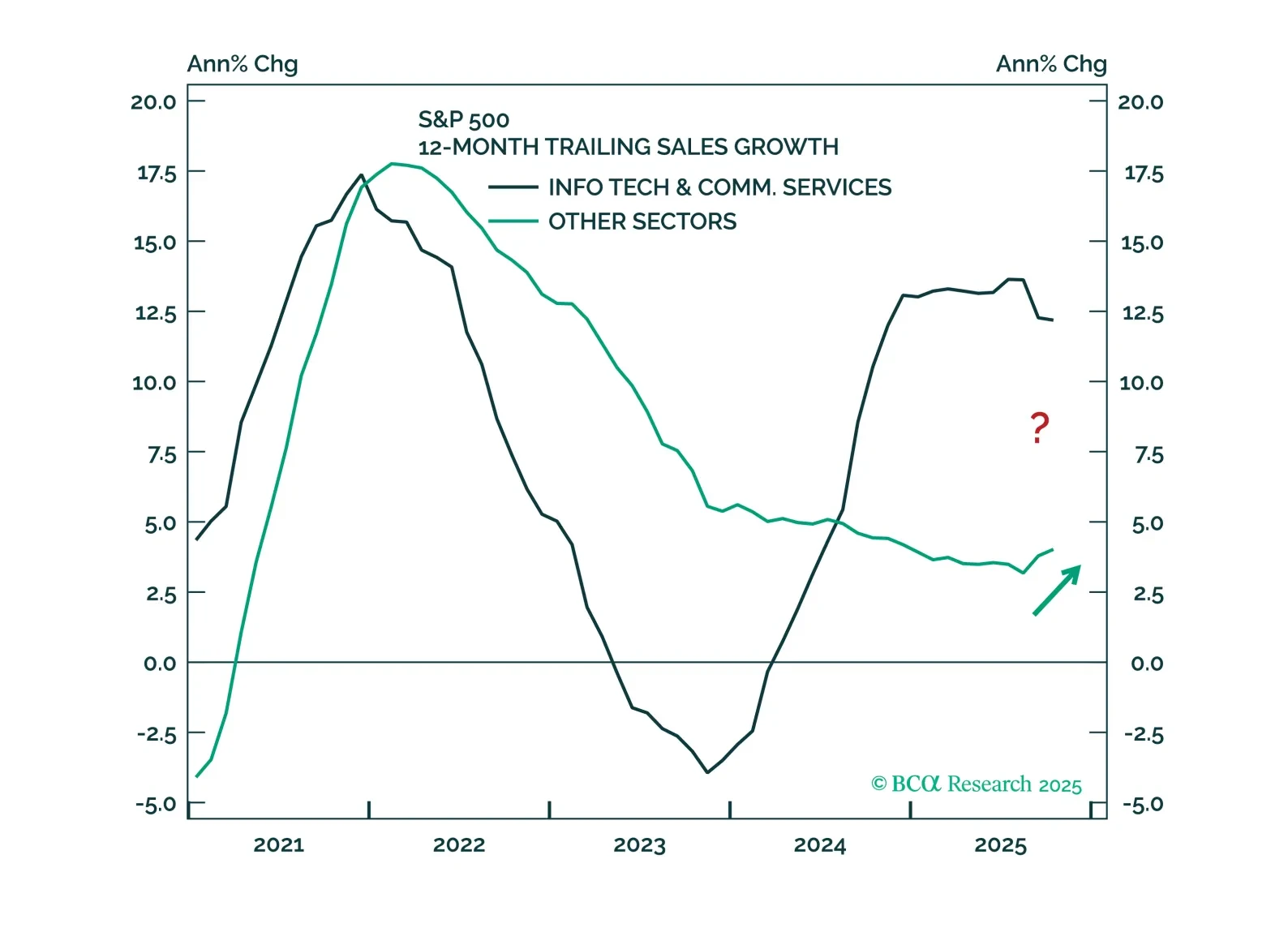

September’s weak consumer spending data challenge the K-shaped recovery narrative and suggest that spending will slow to match already-weak employment growth.

Our Portfolio Allocation Summary for December 2025.

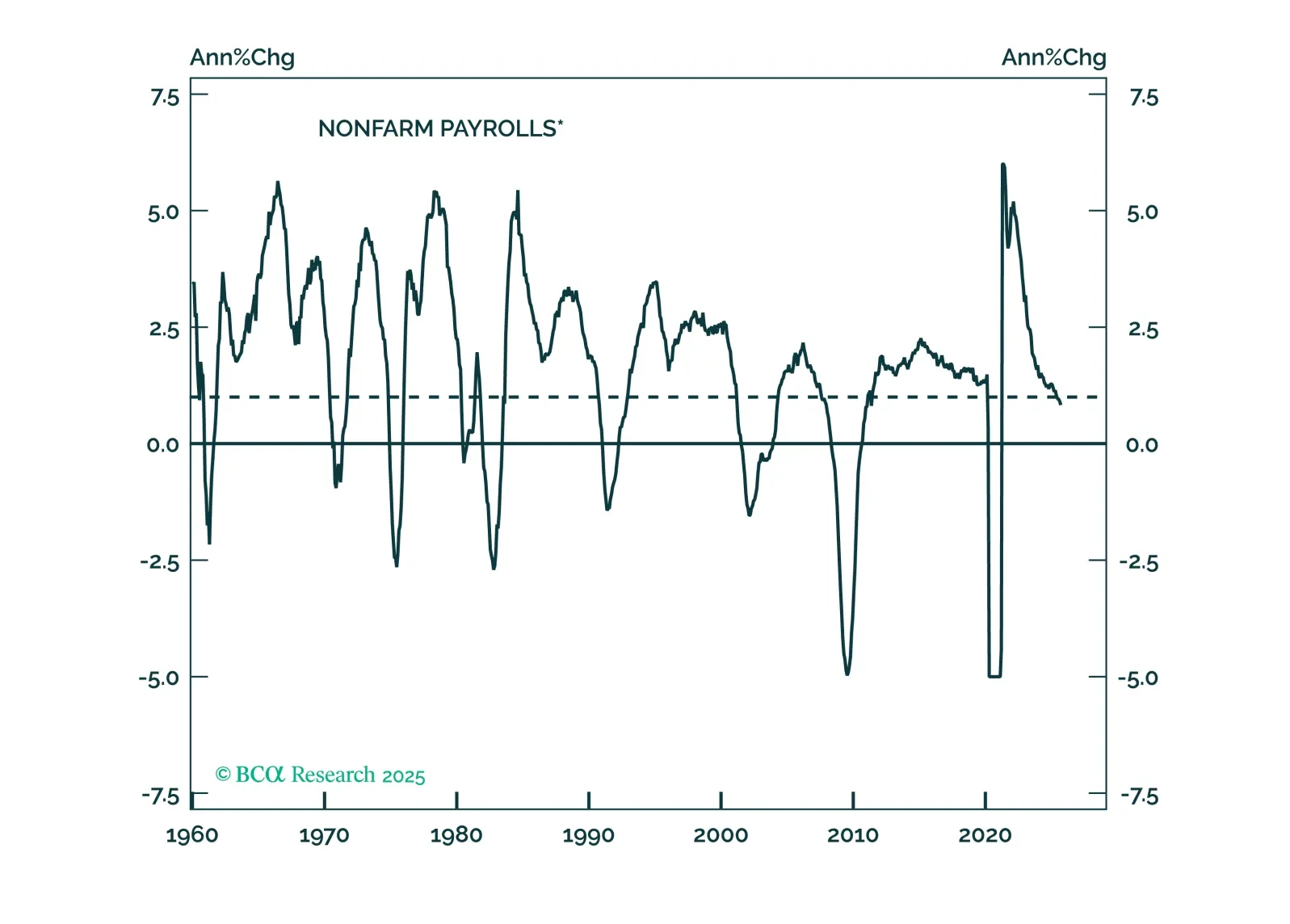

September job gains topped modest expectations, but year-over-year payrolls growth appears to have fallen below stall speed. We remain concerned about US activity.

The K-shaped economy will likely reverse in 2026, with the cyclical parts of the economy doing better. Upgrade Financials and Materials from neutral to overweight. Downgrade Communication Services and Utilities from overweight to neutral. Favor value stocks. Upgrade Bitcoin from neutral to overweight.

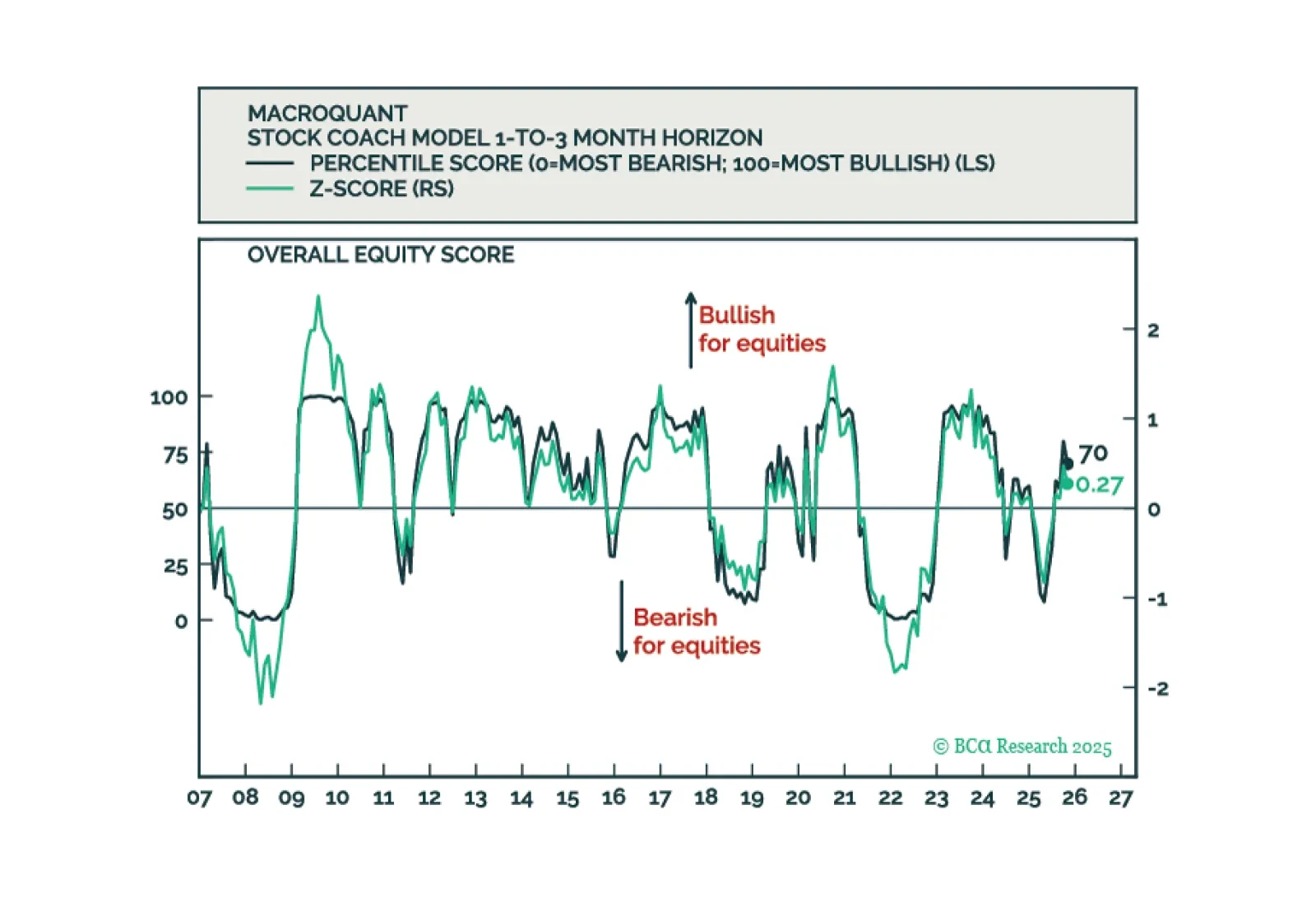

MacroQuant remains tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold.

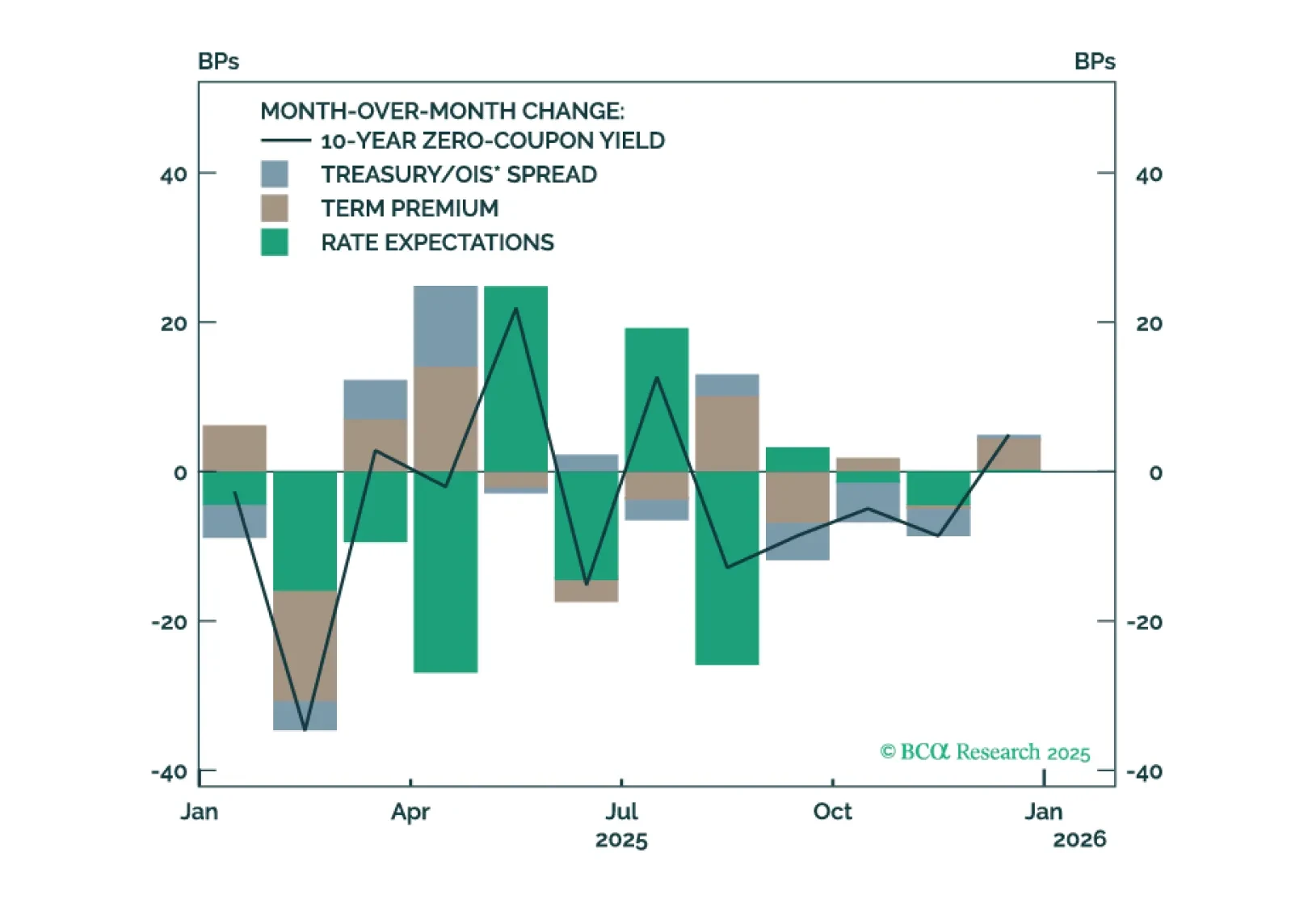

Our key US fixed income views for 2026.

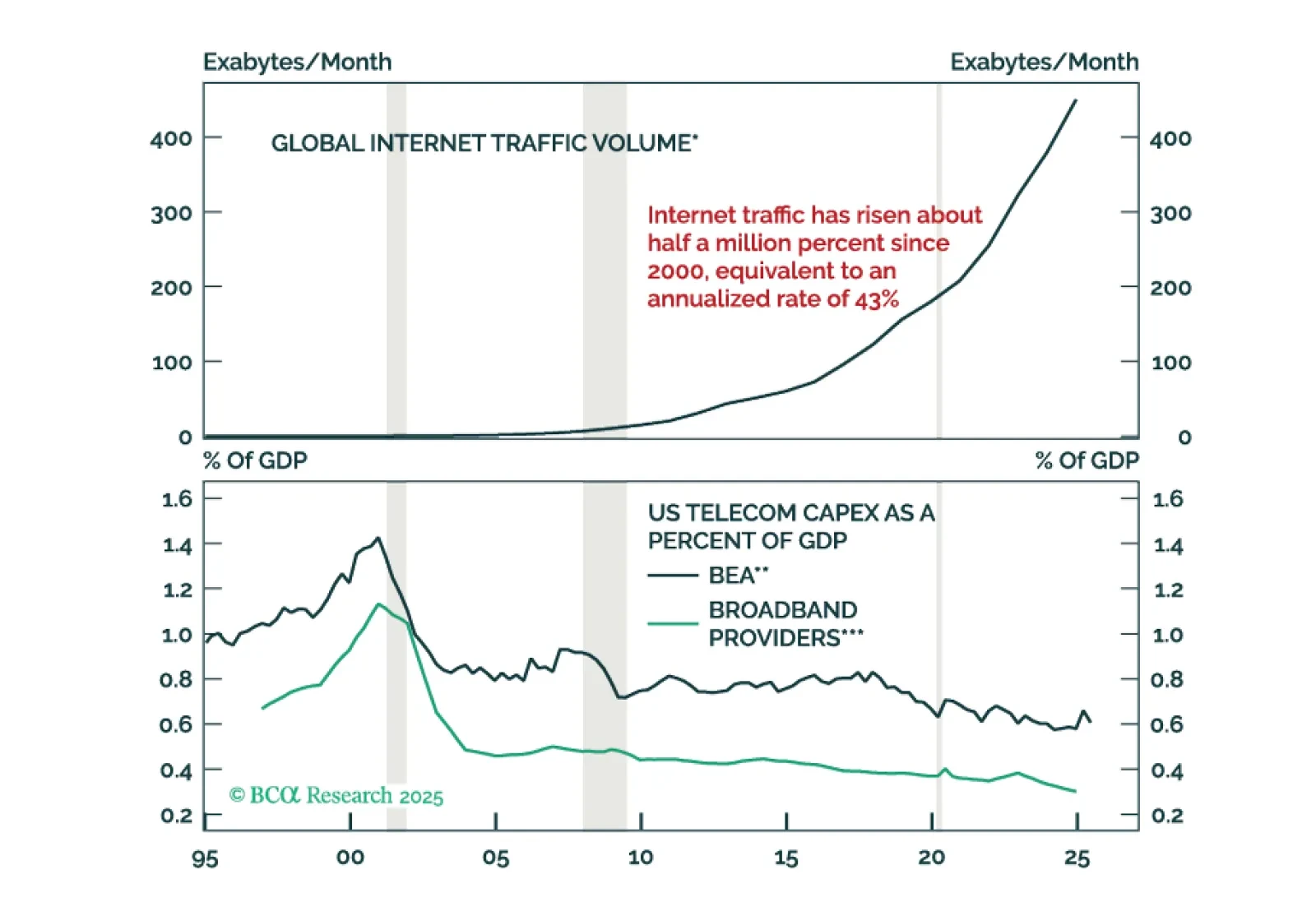

The odds have risen that we have reached a “Metaverse Moment” – a situation where investors punish AI companies for increasing capex. This warrants greater caution towards AI stocks specifically, and the broader S&P 500 more generally.