Economy

What do the mixed signals sent by the UK economy mean for the Bank of England, and what are the implications for Gilts and the British pound?

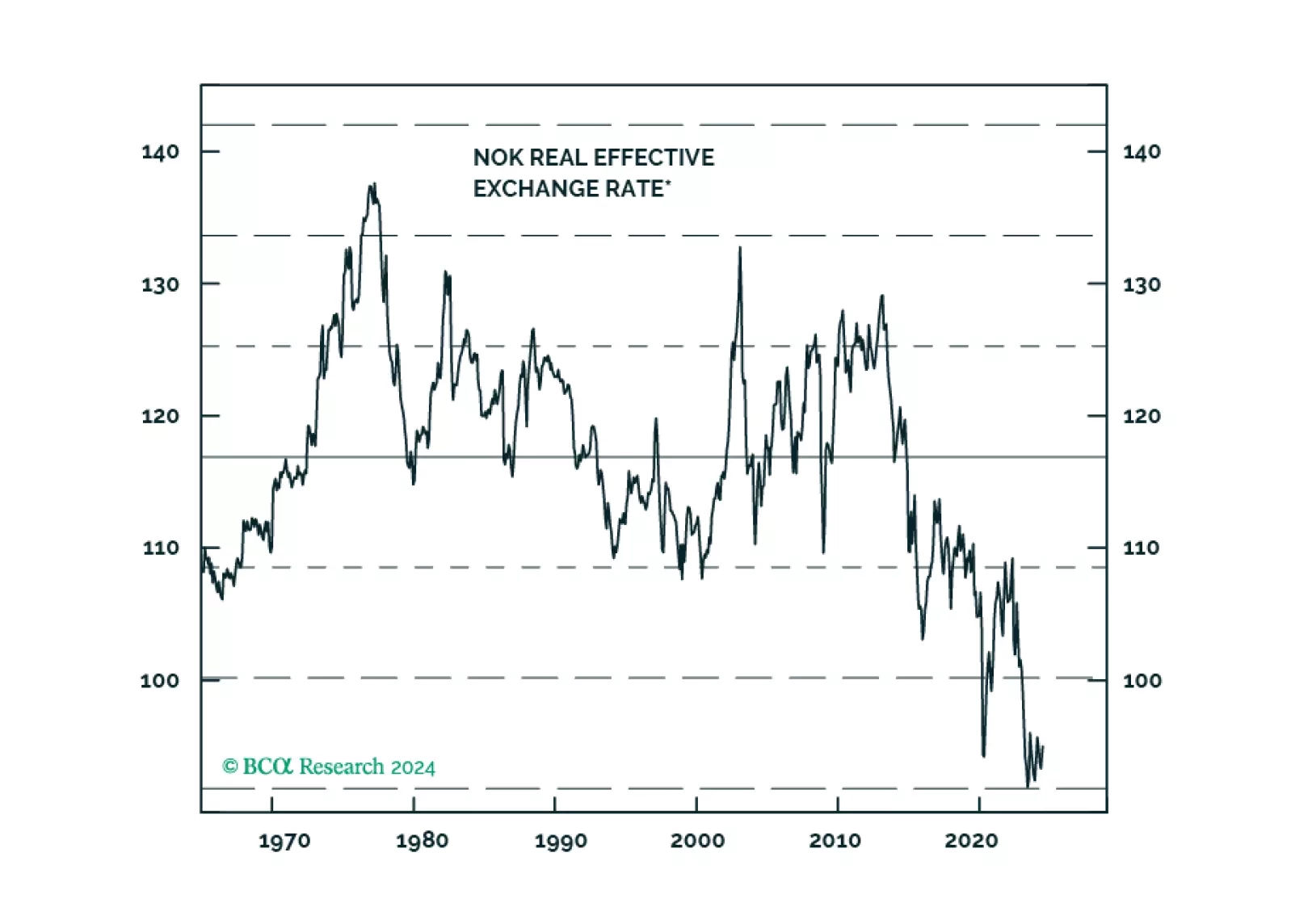

In this report, we gauge the reasons behind the persistently weak Norwegian krone, despite what appears to be benign domestic economic conditions.

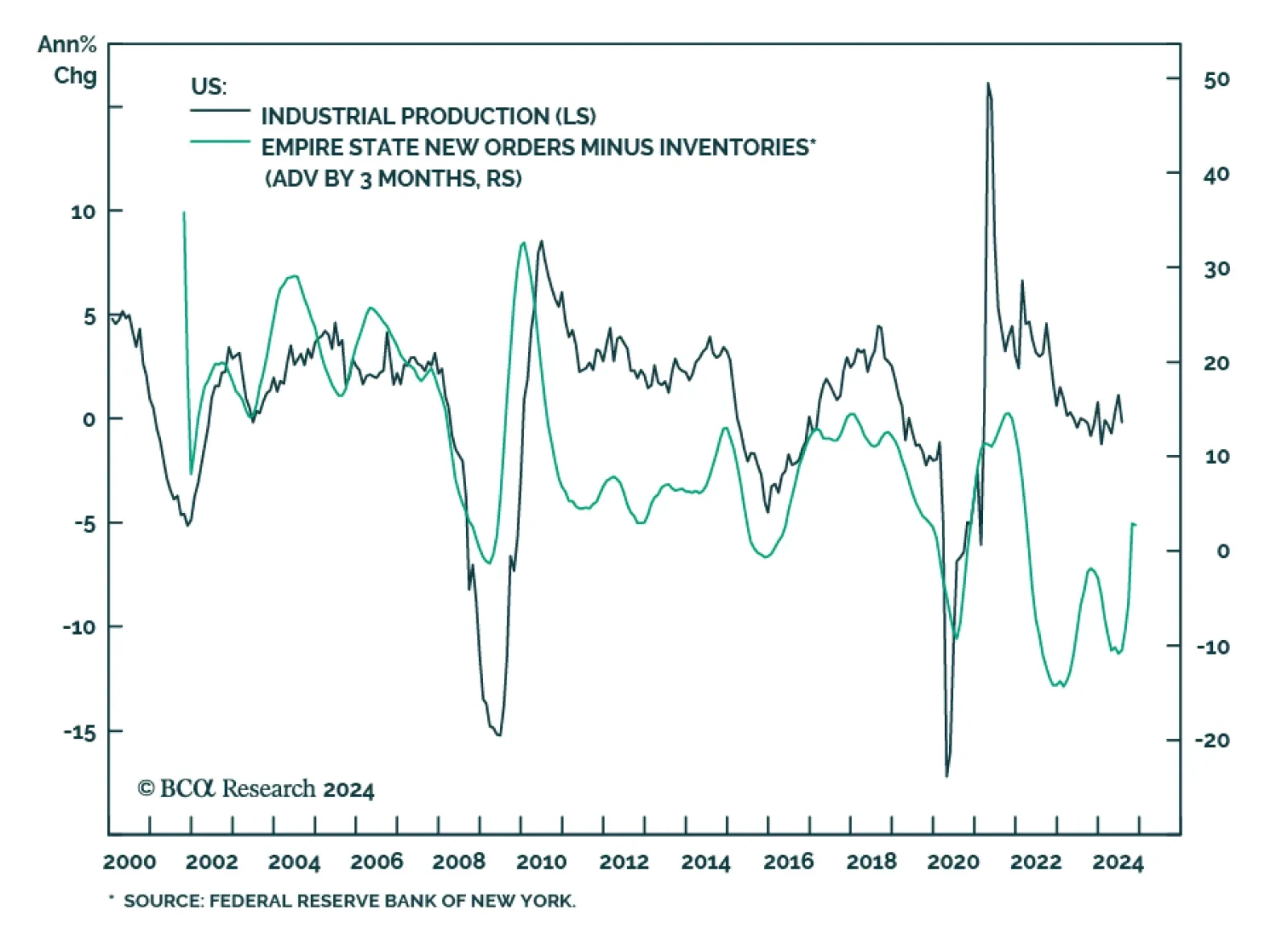

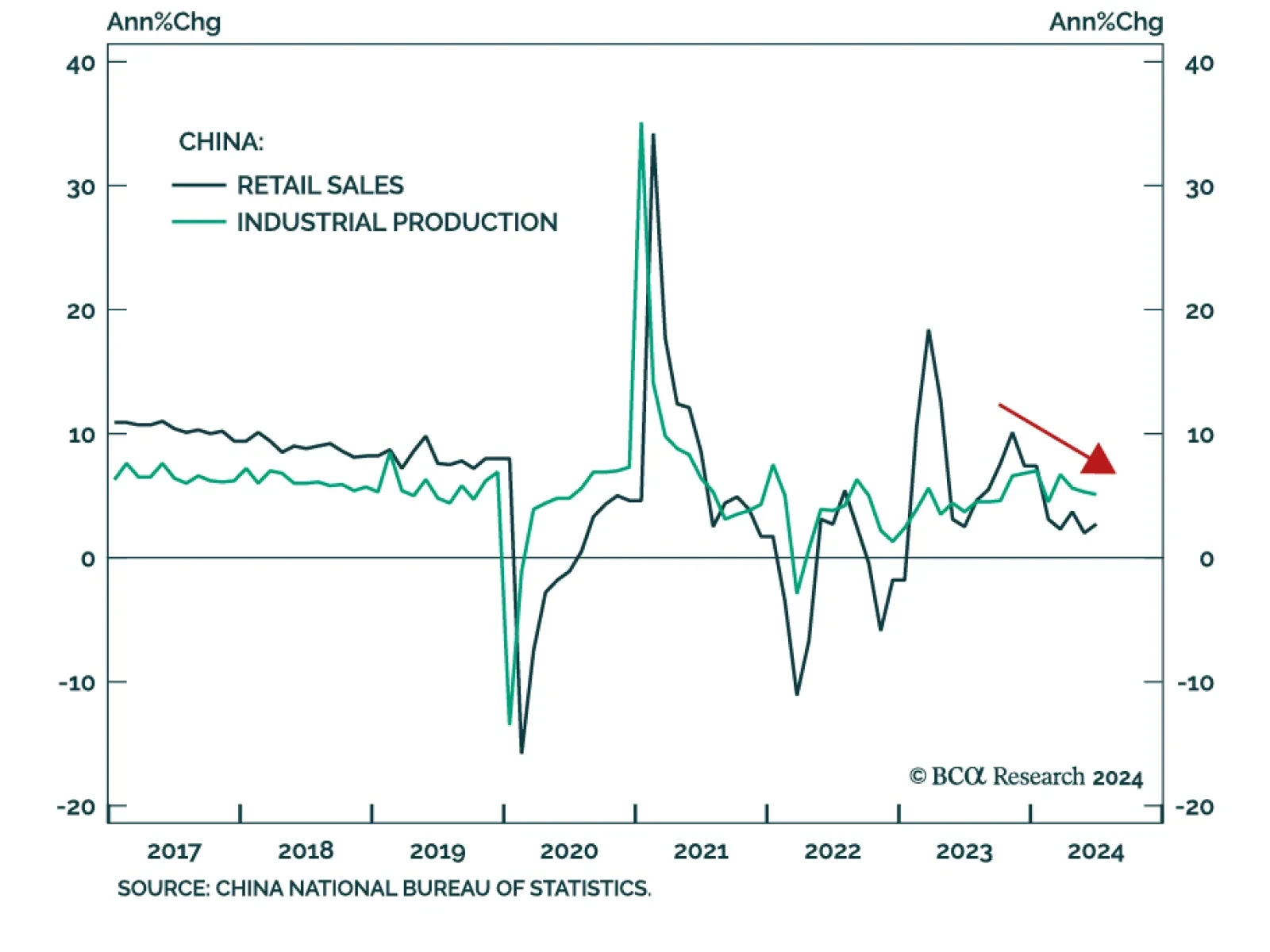

The current Fed easing cycle will likely be a “buy the rumor, sell the news” phenomenon. The basis is our expectation that the US economy is heading into a rough landing. The primary driver of EM currencies is not US interest rates but the global manufacturing cycle.

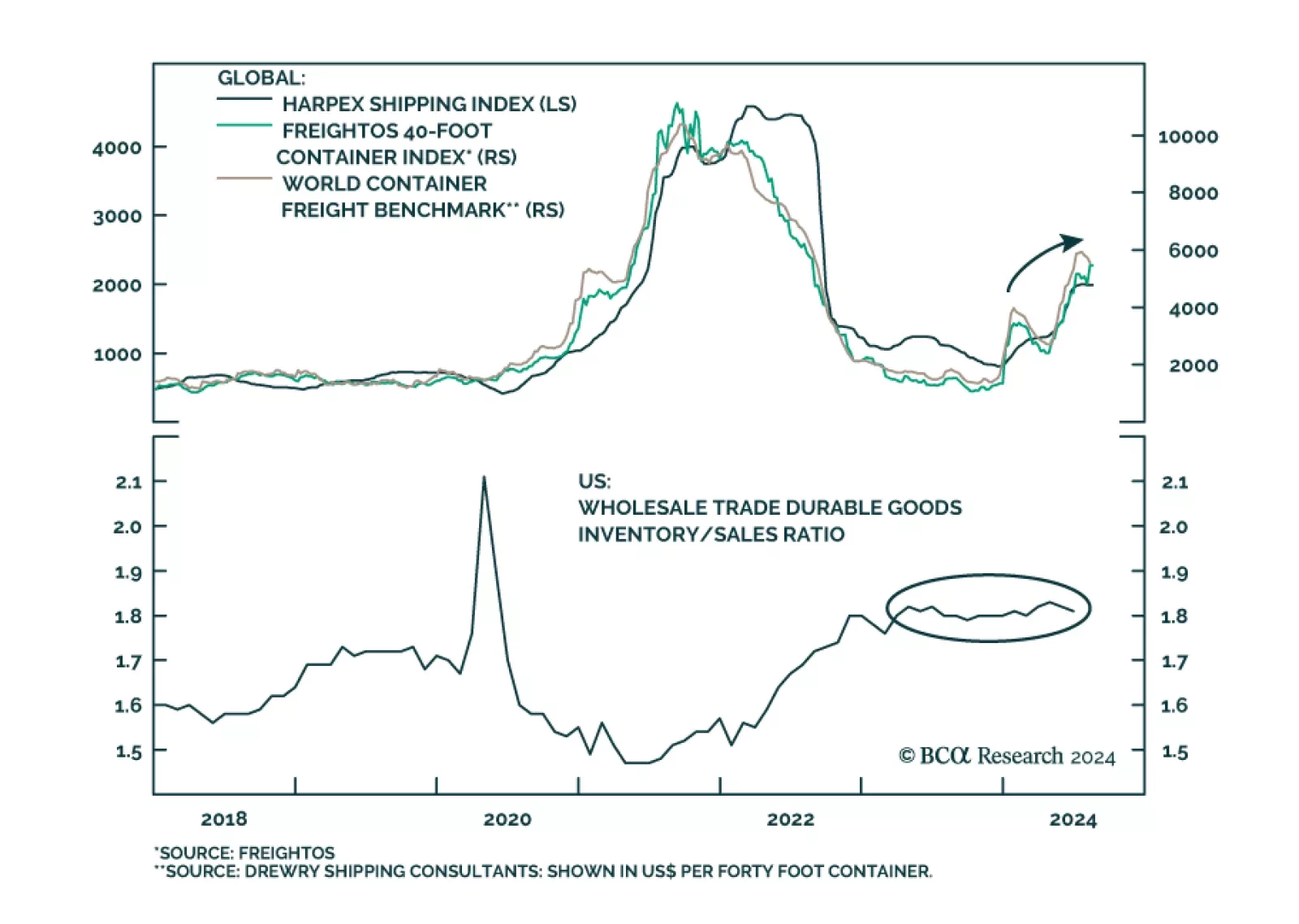

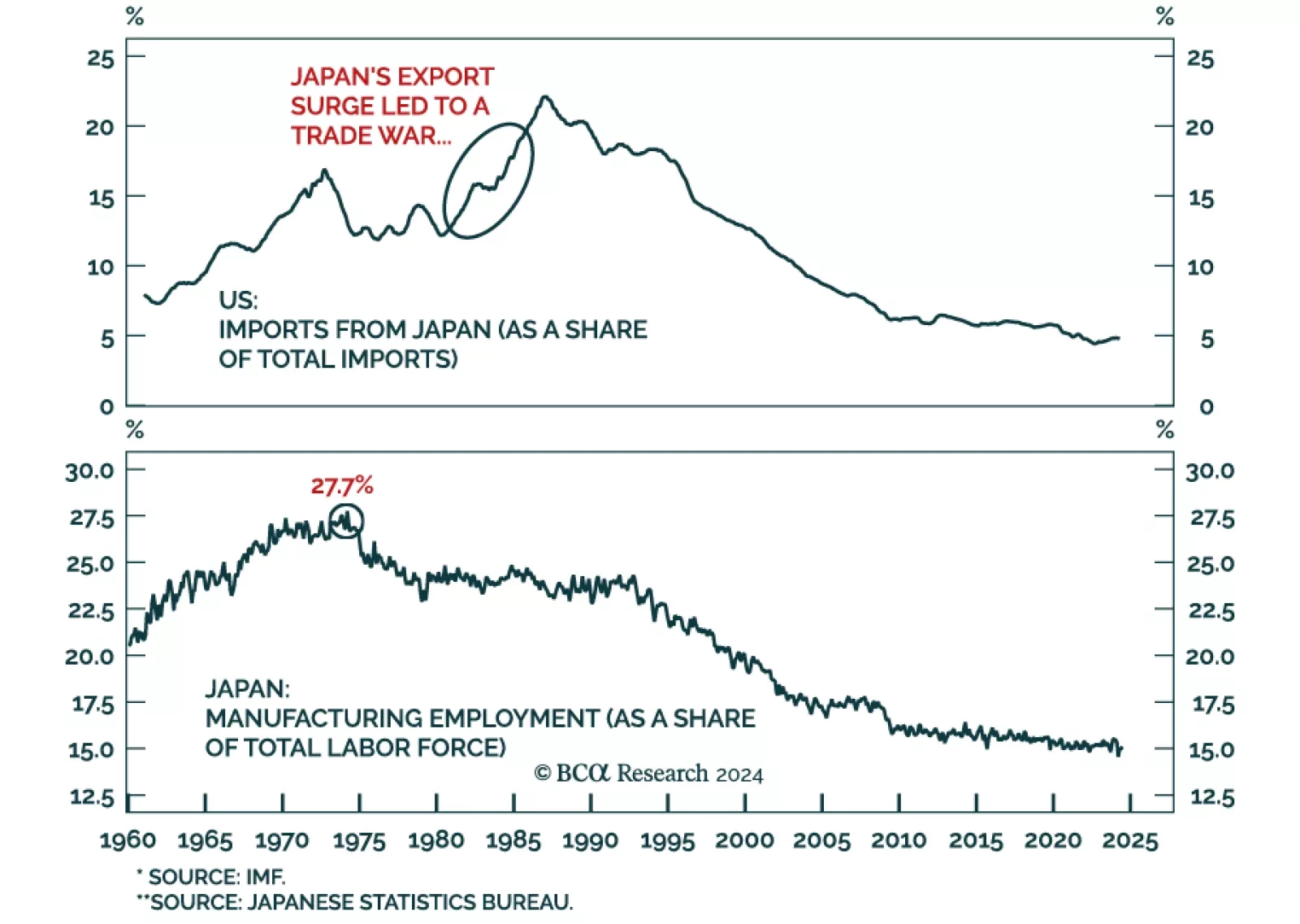

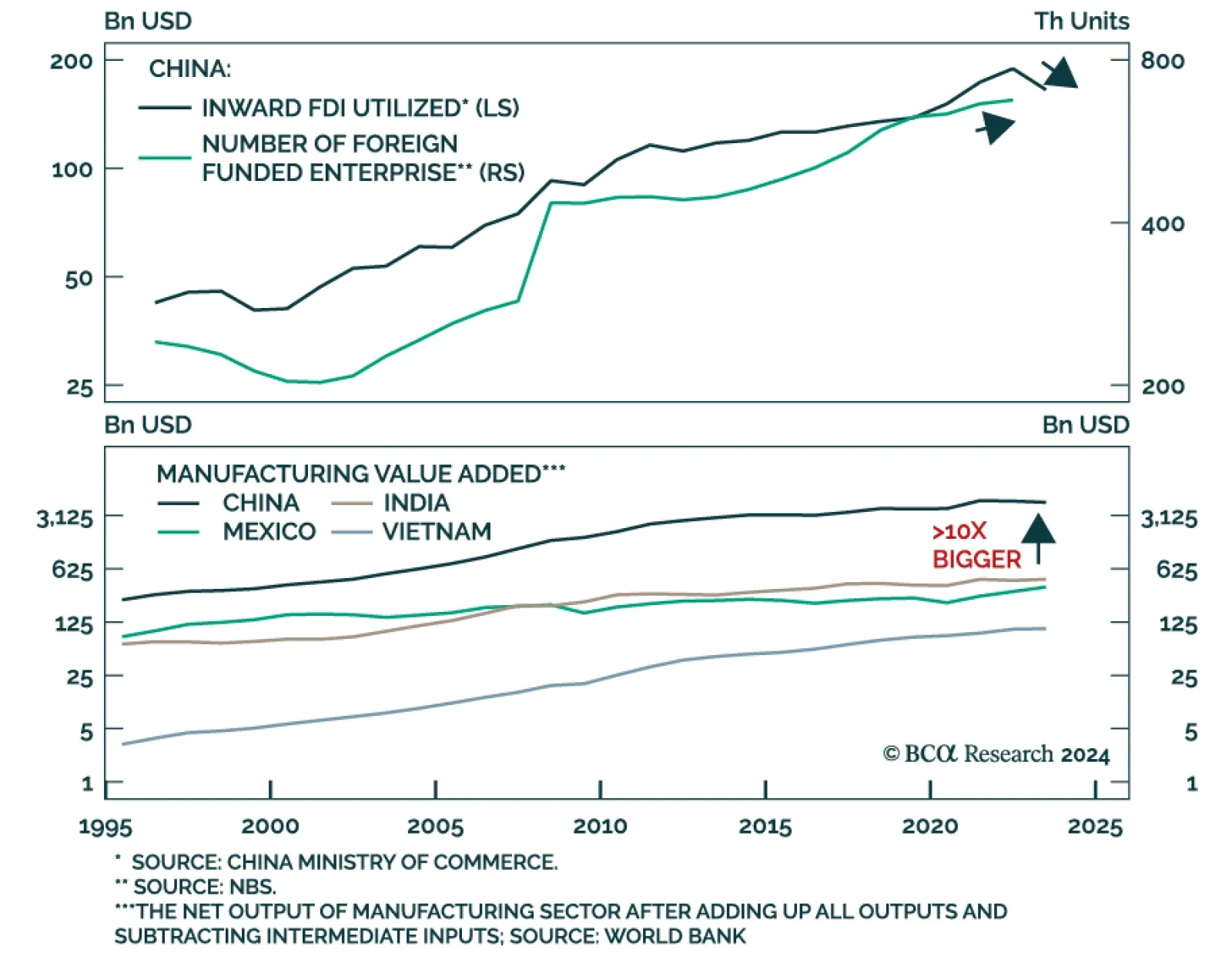

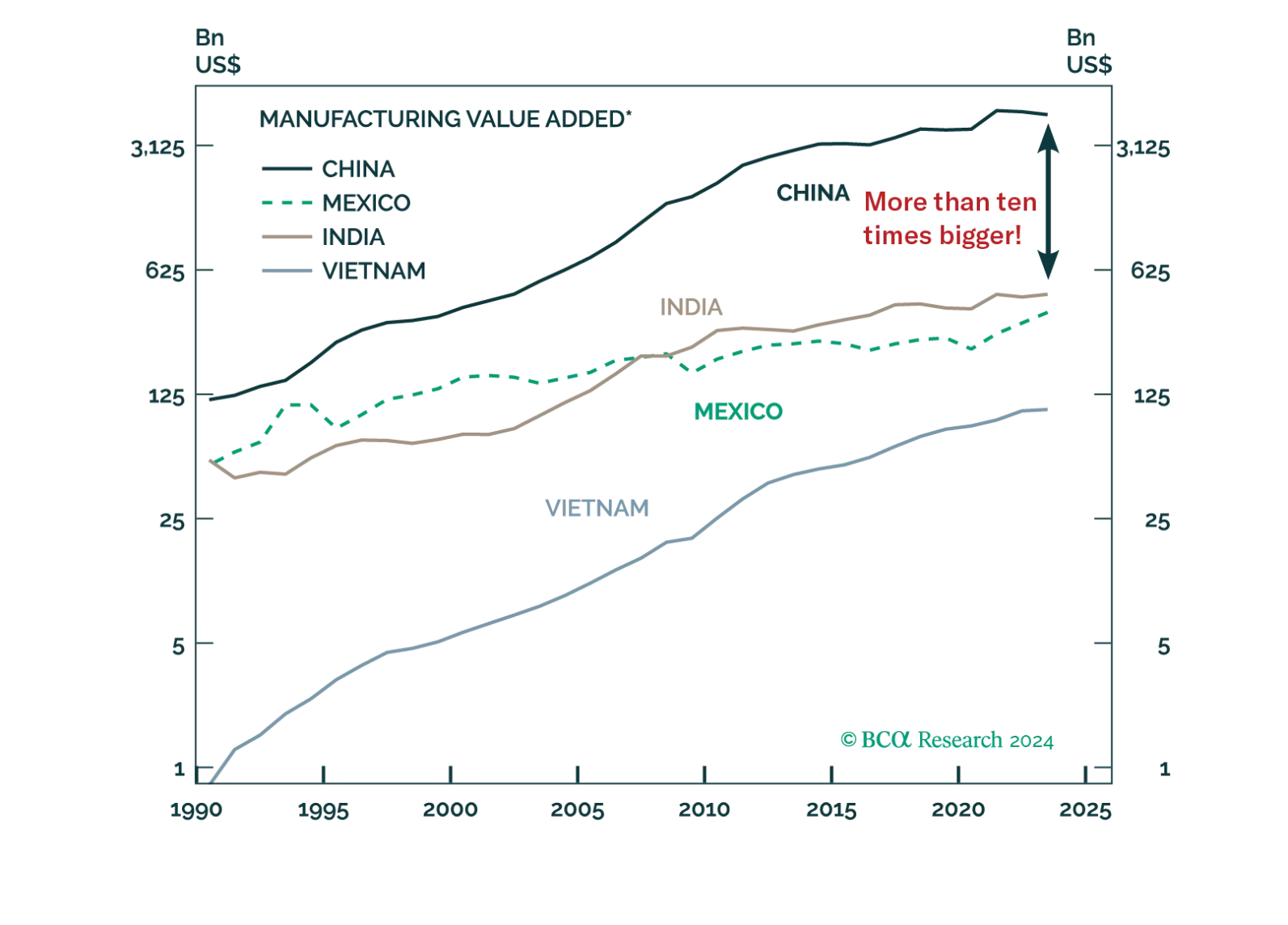

Multinationals are attempting to expand their supply chains beyond China, but the relocation process has been slower than expected. In the coming years, however, geopolitical tensions, changes in China’s business environment, and rising competition from Chinese producers could accelerate multinationals' departure from China.