Economy

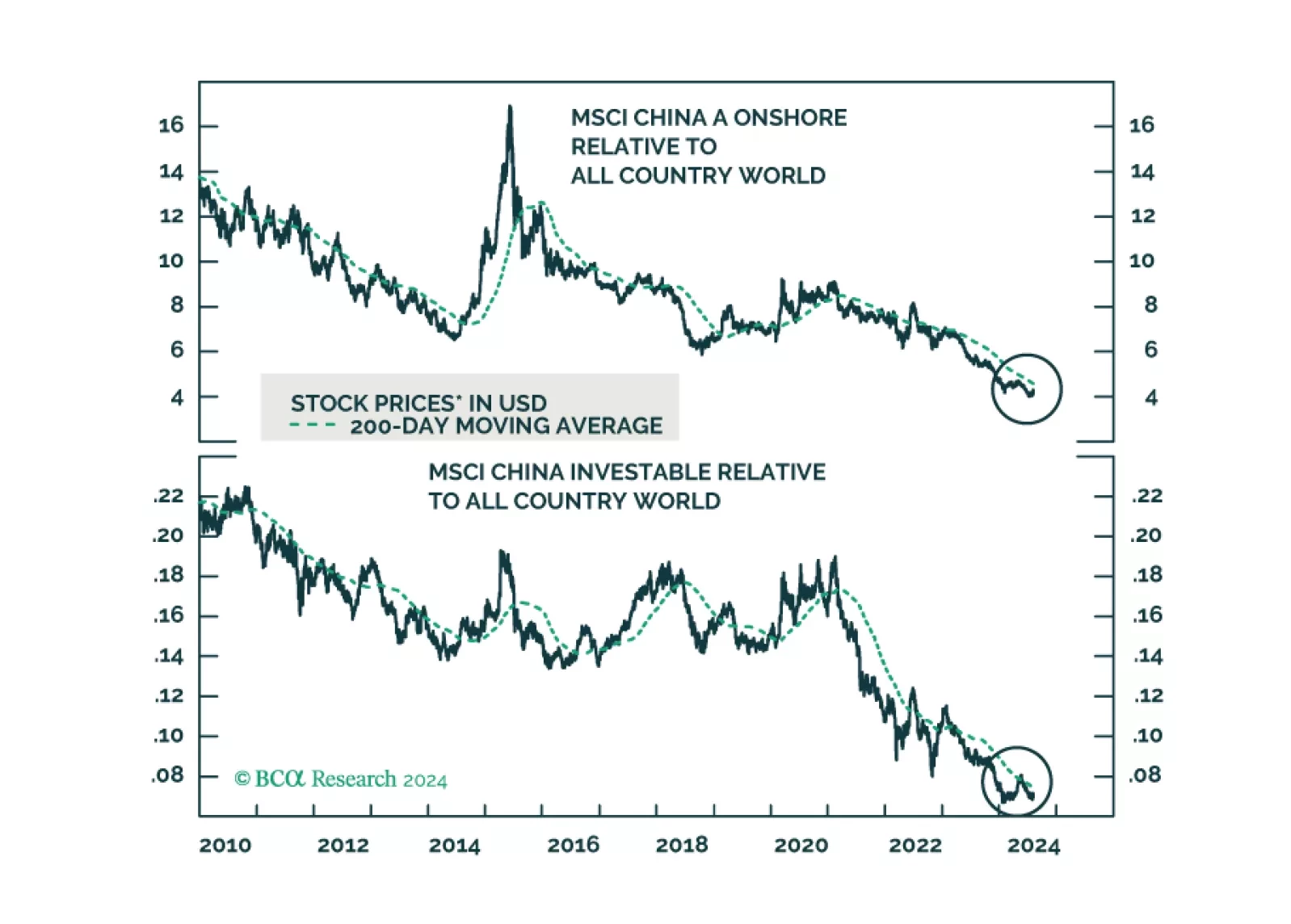

The prices of multiple financial assets have failed to break above their technical resistances. When this occurs, a breakdown ensues. In brief, global risk assets remain vulnerable. We are upgrading Chinese onshore stocks from neutral to overweight and offshore ones from underweight to neutral within EM and global equity portfolios.

China's cyclical and structural headwinds will likely undermine Beijing’s initiative to accelerate urban migration over the next five years.

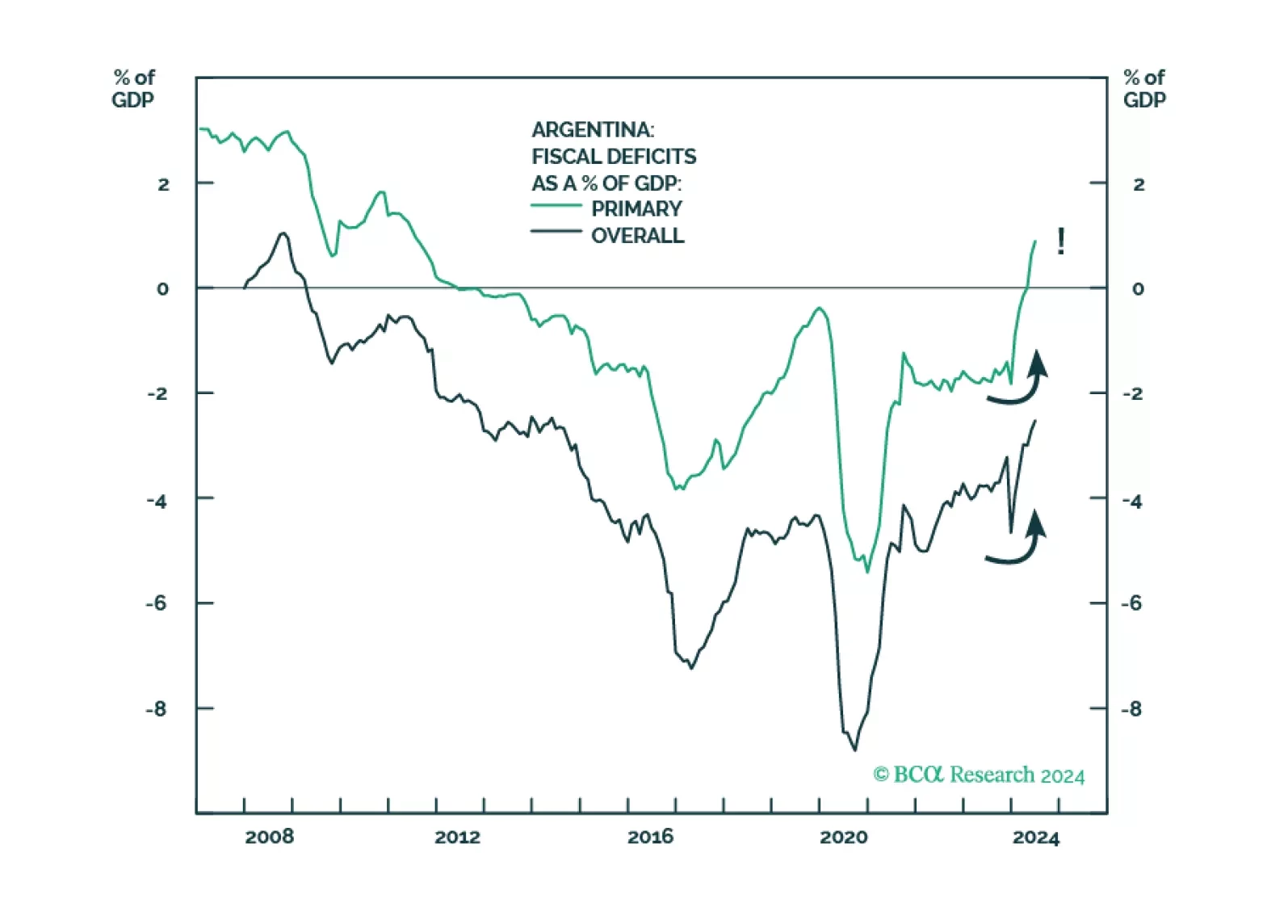

GeoMacro team partners with BCA’s Emerging Markets Strategy to examine political reforms in Argentina. Our colleague Juan Egaña argues that the time is not right to go long Argentinian assets and that Buenos Aires must avoid the mistakes of the Macri era: opening to foreign capital flows too soon without addressing structural macro imbalances. However, the Milei administration is on the right path with potentially global implications.

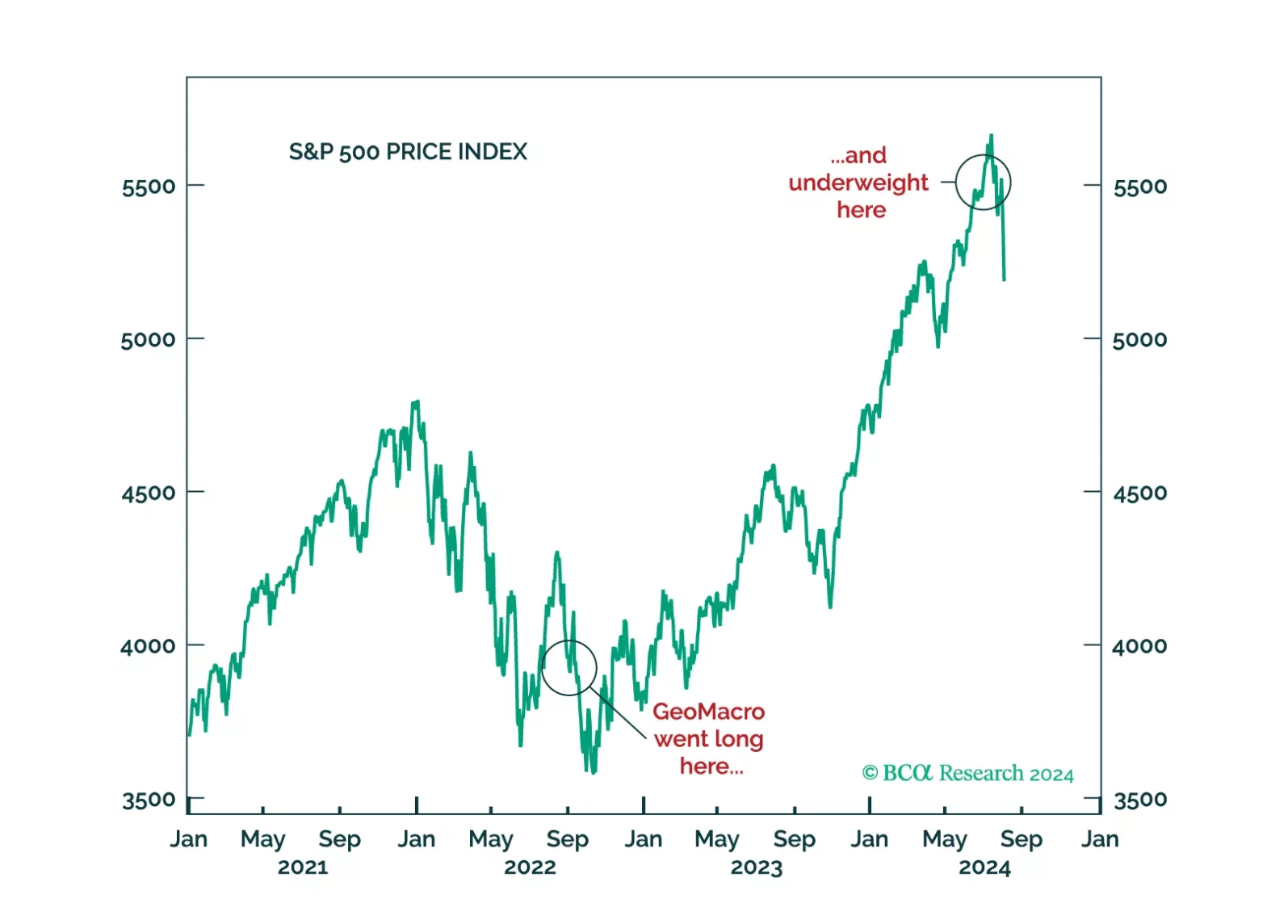

The decision by GeoMacro team on July 2 to short USDJPY and underweight equities has proven to be prescient. We still do not like the market setup from here on out. A recession would, obviously, be negative for risk assets. But even if investors avoid that scenario, the transition from cash- to leverage-driven growth is unlikely without a significant Fed rate-cutting cycle.