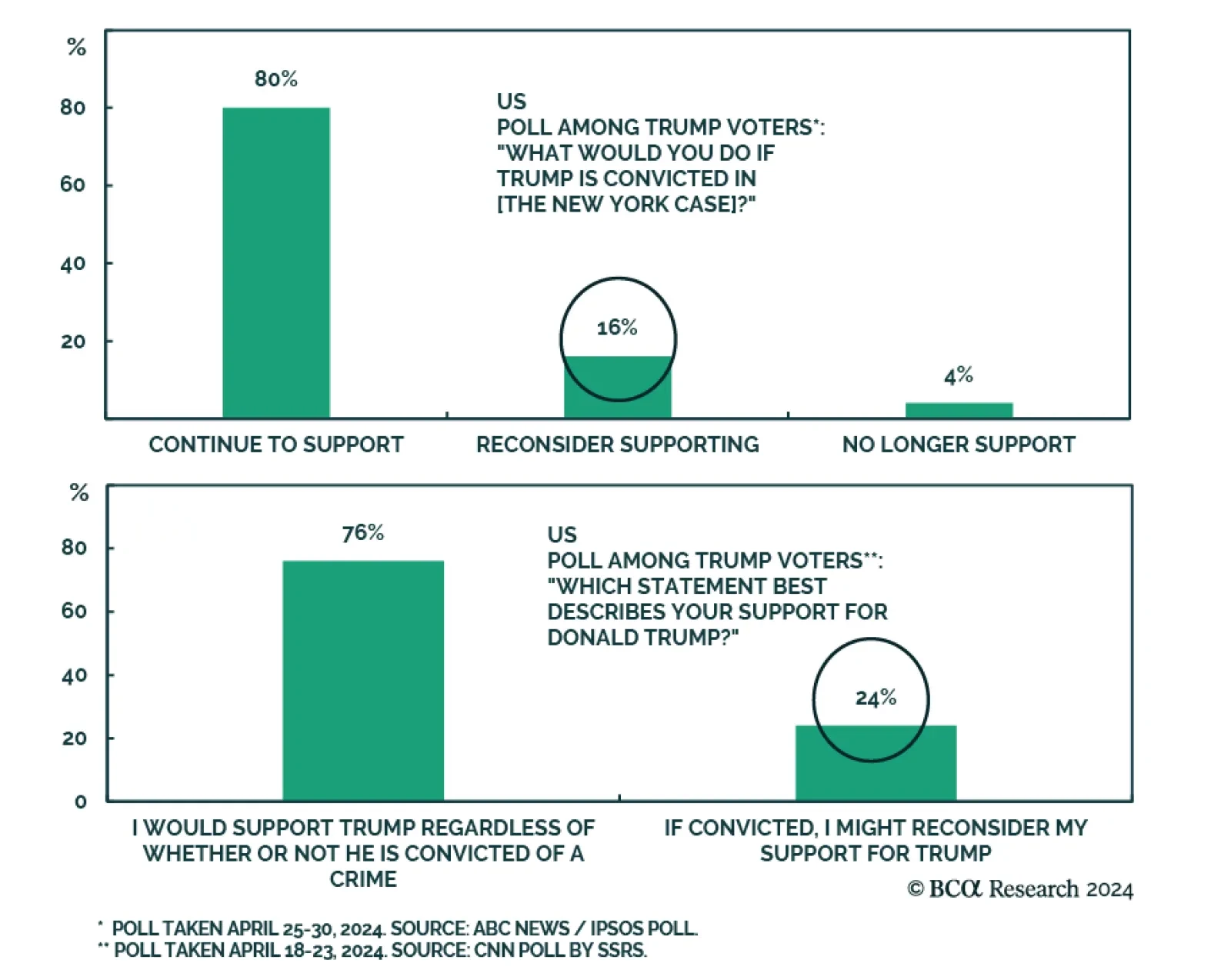

According to BCA Research’s US Political Strategy service, Trump’s conviction will not be a game changer in the upcoming Presidential election. President Trump was convicted of 34 felony charges by a 12-person jury…

Euro Area CPI accelerated for the first time this year from 2.4% y/y to a faster-than-expected 2.6% y/y in May. Preliminary estimates also suggest that core CPI accelerated from 2.7% y/y to 2.9% y/y, against expectations of a…

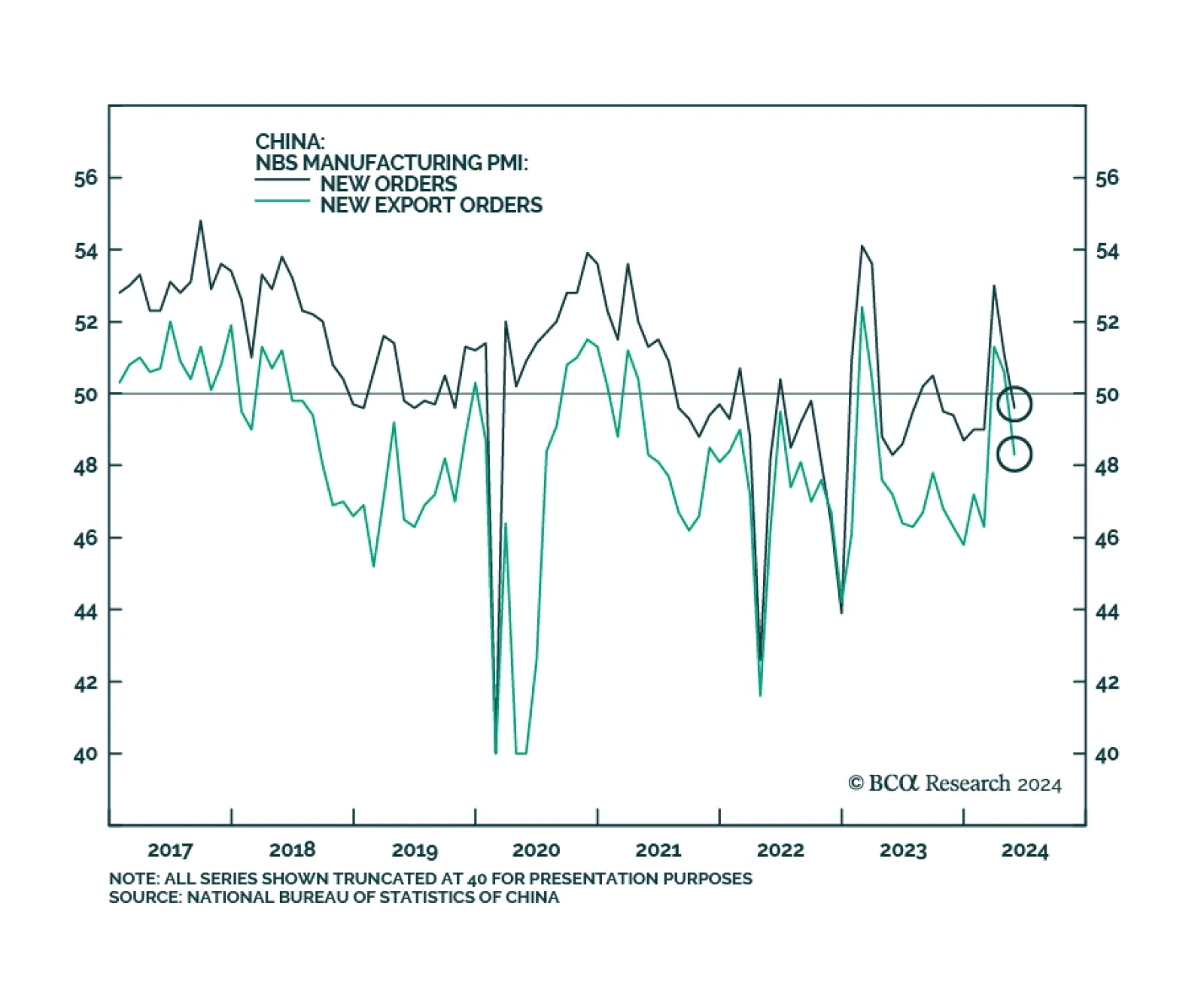

Chinese PMIs from the National Bureau of Statistics (NBS) disappointed in May. The manufacturing PMI contracted in May (49.5), breaking a two-month expansion streak and disappointing expectations of continued growth. Meanwhile…

US Q1 GDP was revised lower from 1.6% q/q annualized to 1.3%. Notably, the downward revision to personal consumption was higher than expected, from 2.5% q/q annualized to 2.0%. Investment and government spending were revised…

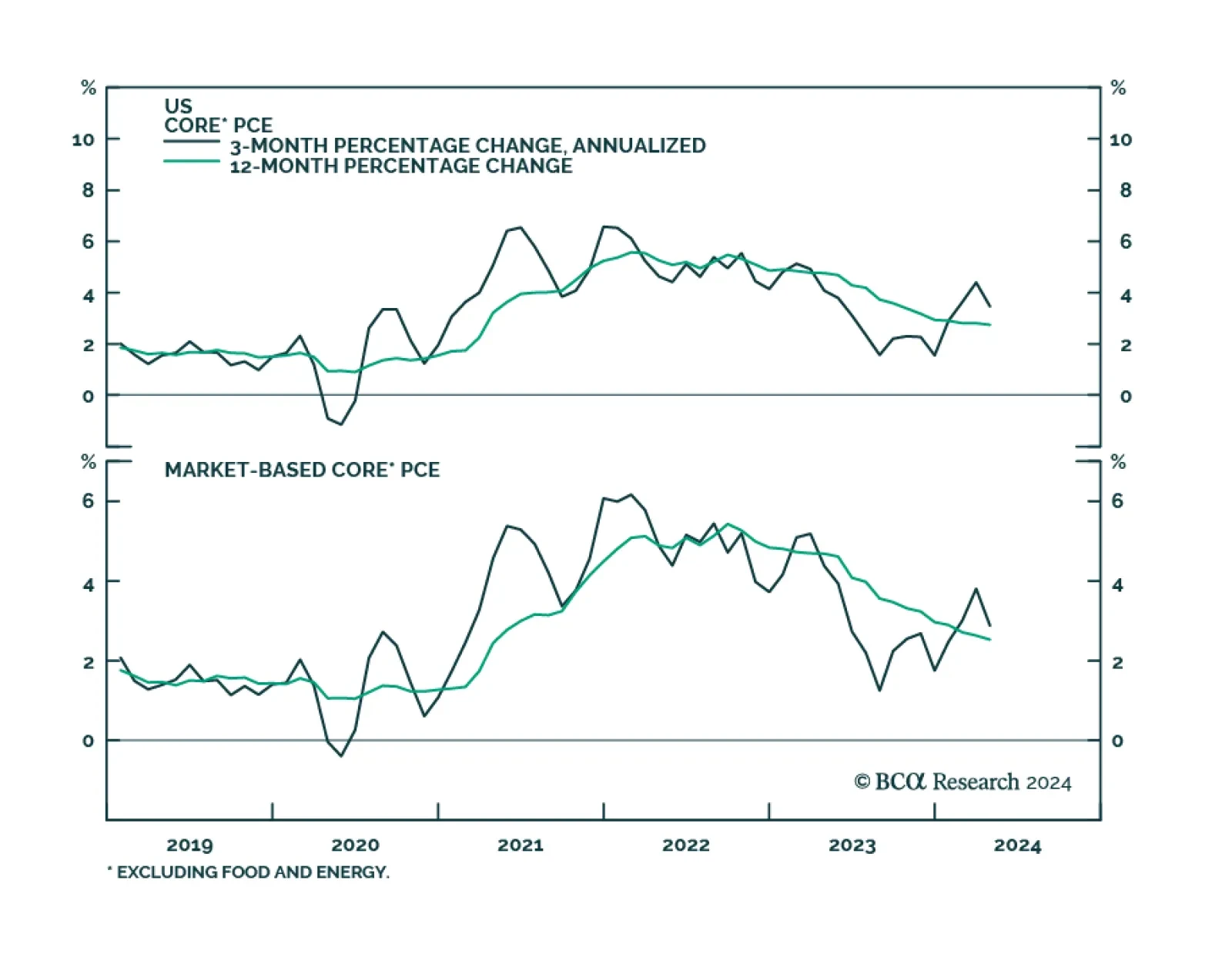

US nominal personal income growth decelerated from 0.5% m/m to 0.3% m/m in April, in line with expectations. However, nominal personal spending surprised to the downside, and contracted 0.1% m/m in real terms. Core PCE –…

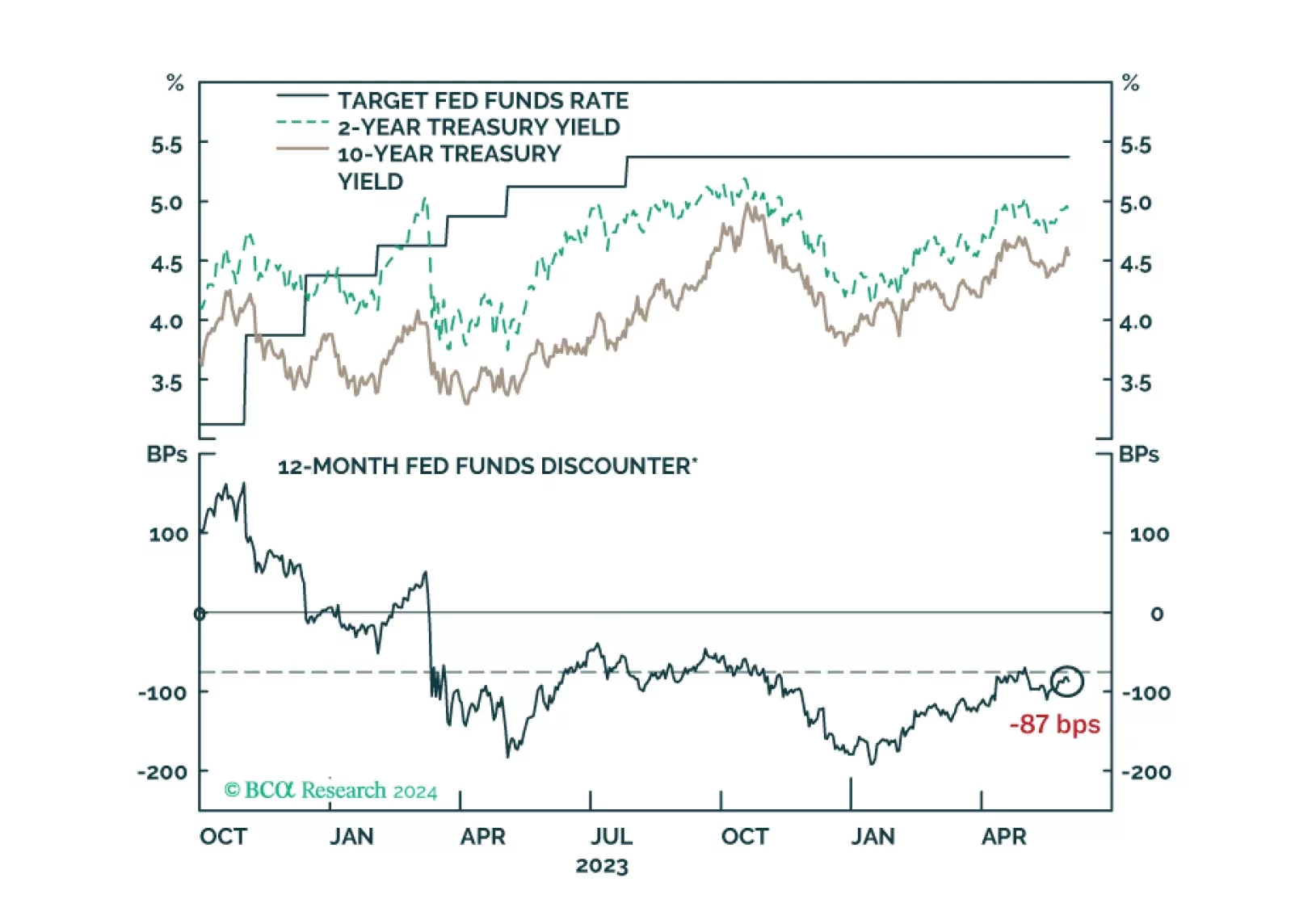

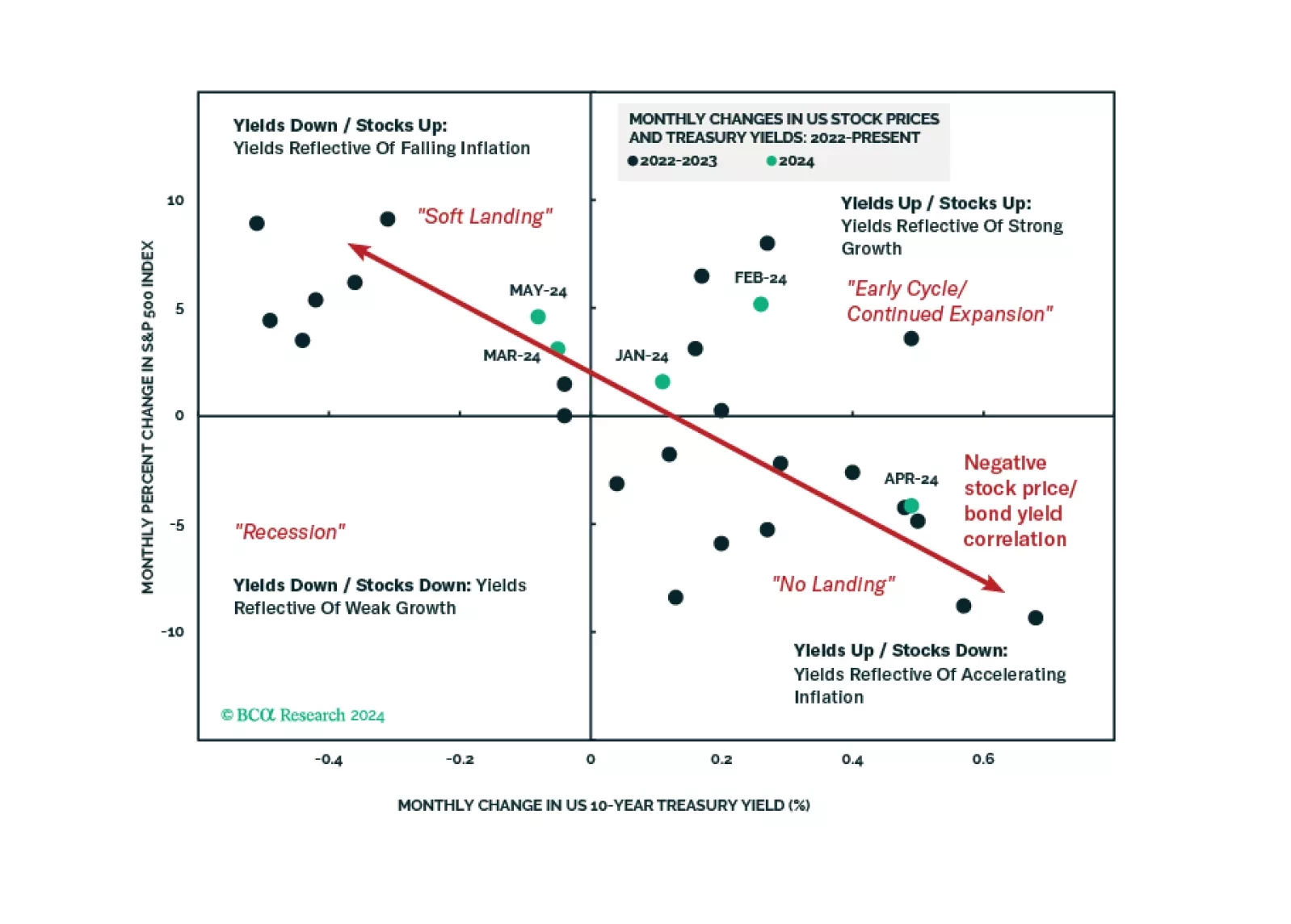

We comment on whether Treasury market valuation is sufficiently attractive to get long bonds and consider some of the common arguments for why yields may yet make new highs.

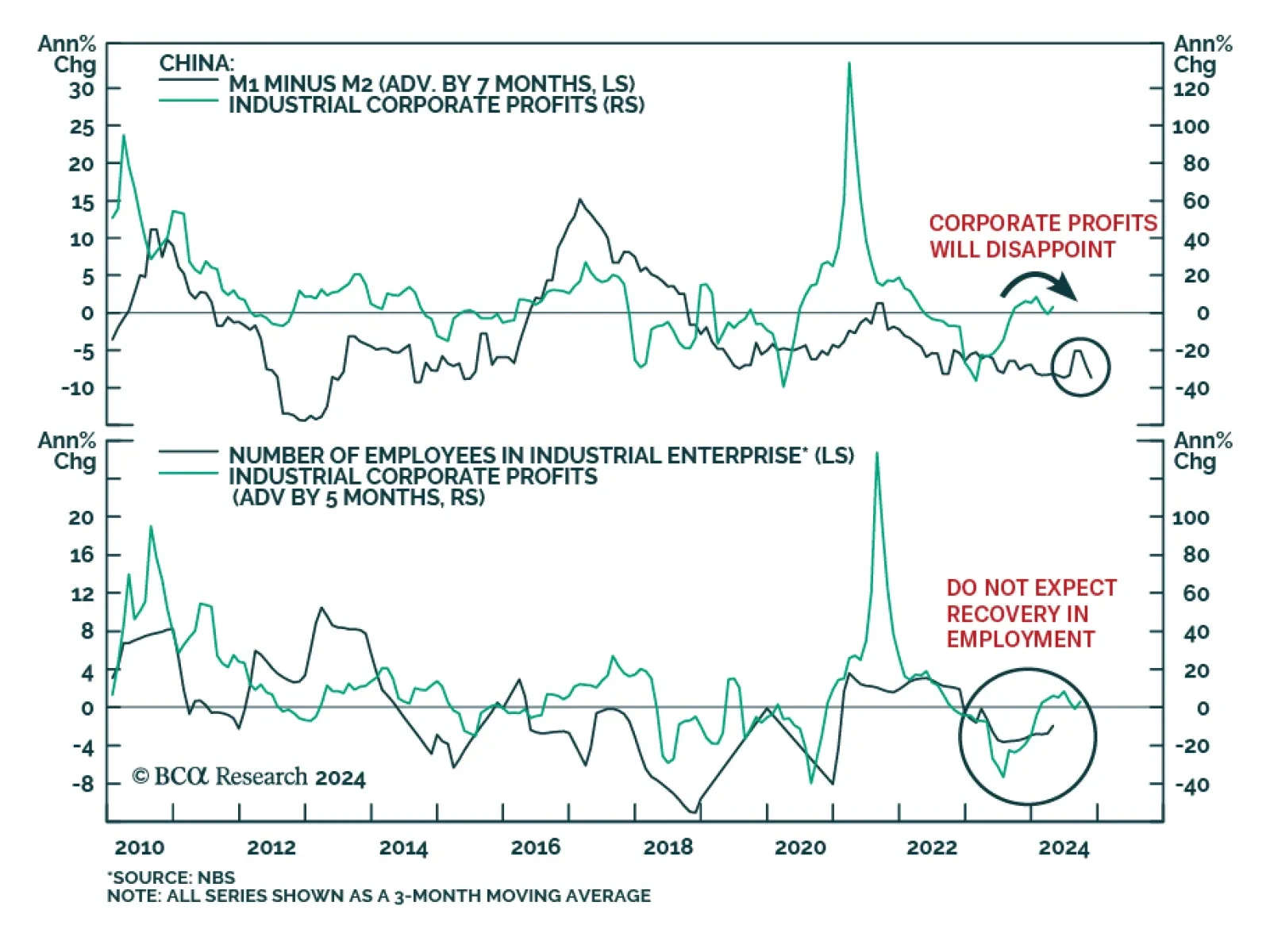

As in many other countries, China’s cyclical consumption growth is primarily driven by labor market conditions, income, and borrowing. BCA Research’s China Investment Strategy service maintains the view that these…

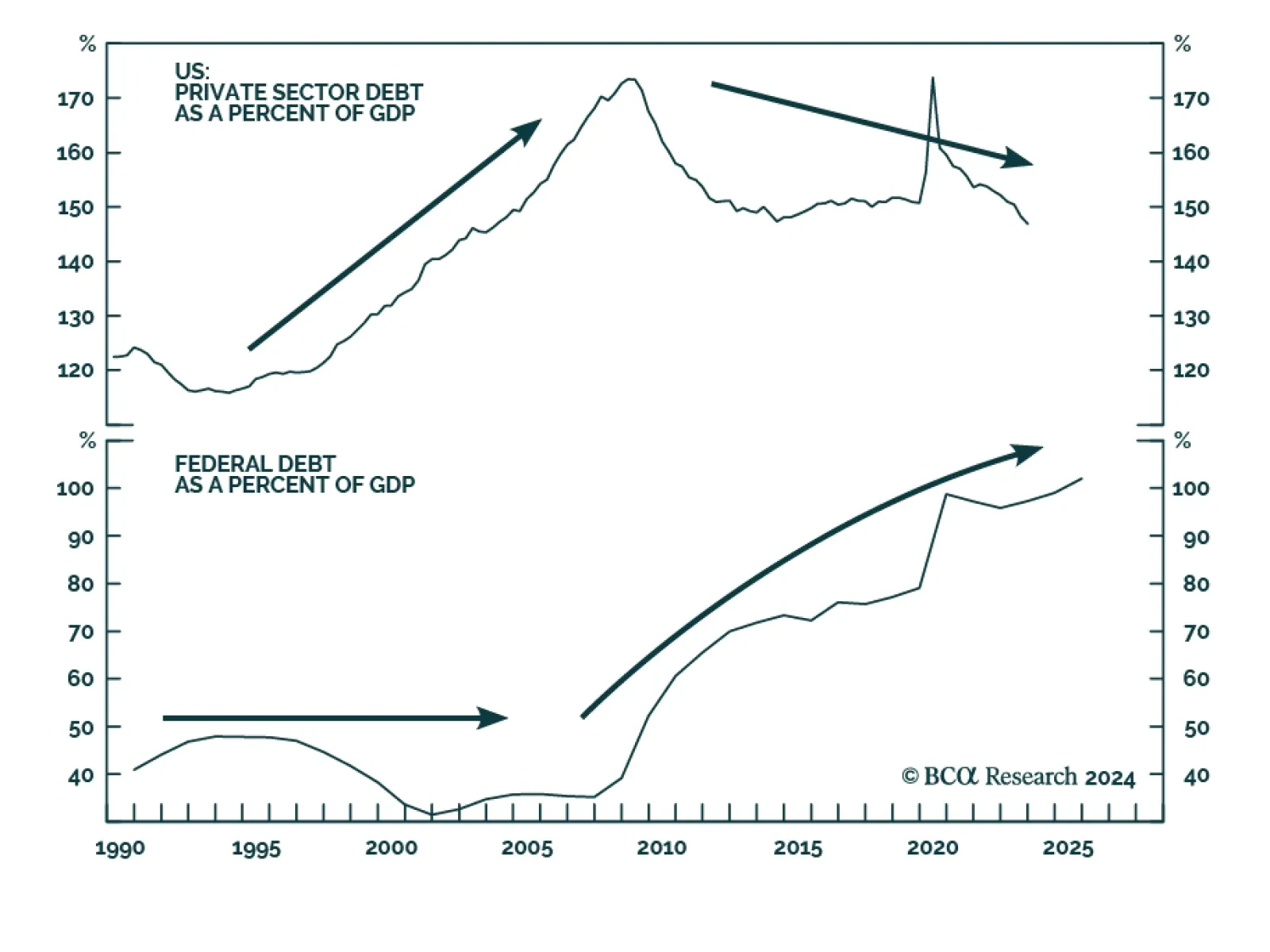

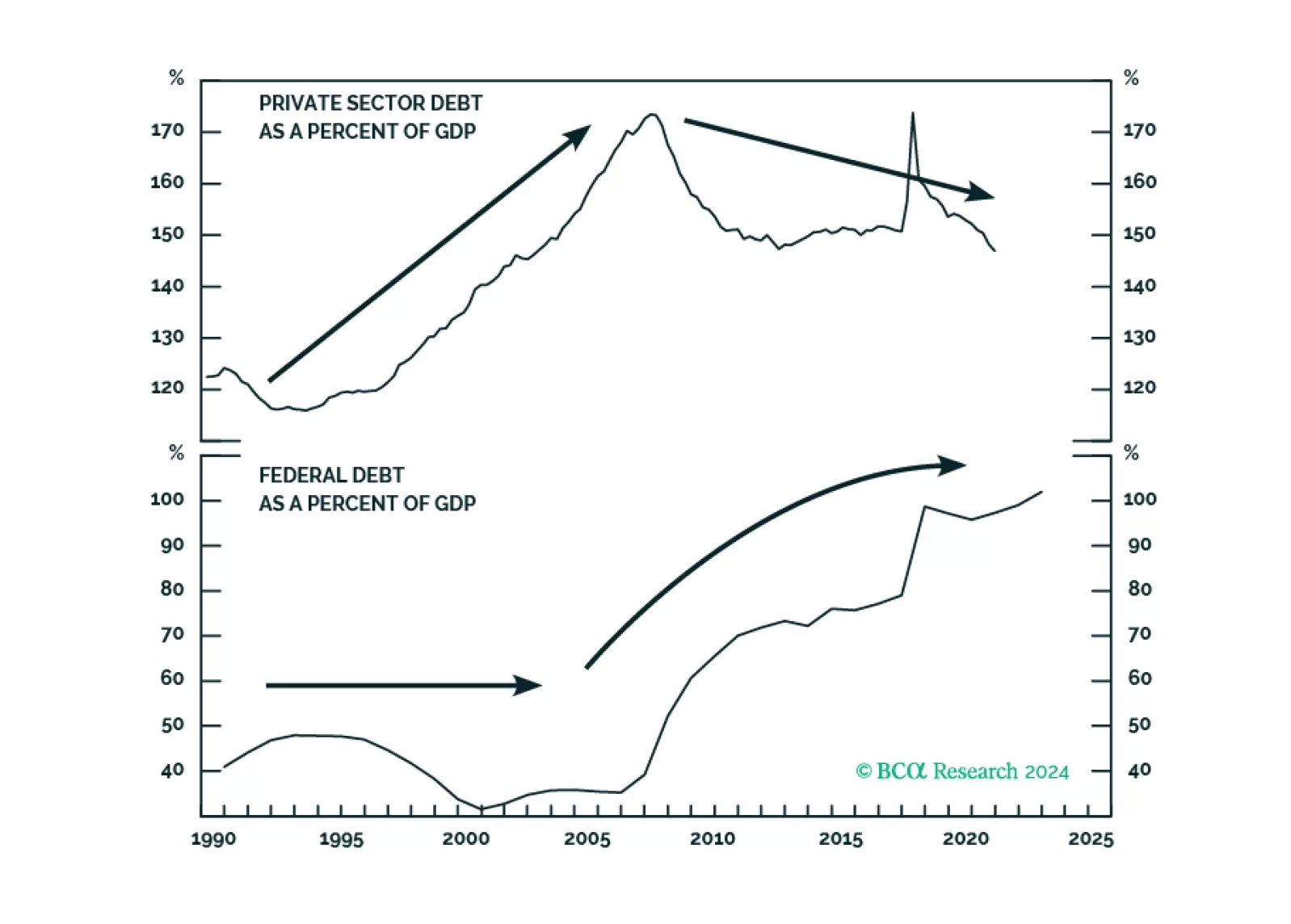

BCA developed the Debt Supercycle thesis in the 1970s to characterize the postwar surge in private sector indebtedness. Because rising debt burdens increased economic vulnerability, policymakers were forced to pursue increasingly…

In Section I, we argue that global investors have been lulled into a false sense of security concerning the resiliency of the US economy. Tight monetary policy means that something must change for a recession to be avoided, and…