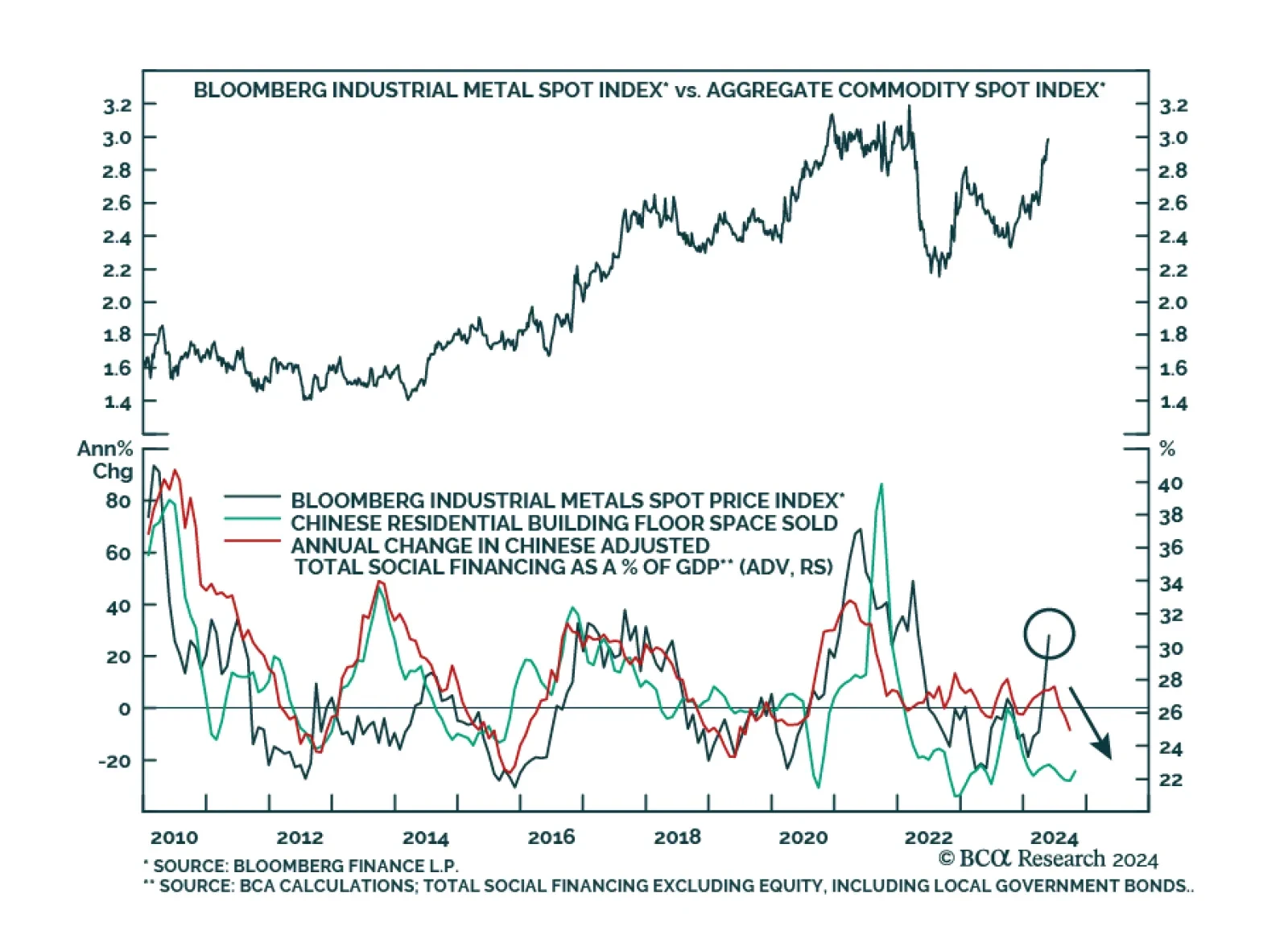

Industrial metals have outperformed the broad commodity complex this year and raced above the broad commodity complex even more meaningfully since the beginning of April. Our Commodity and Energy strategists have highlighted…

We do not subscribe to the Goldilocks scenario in which price pressures continue to ease while economic growth remains robust. We expect that softening labor demand will eventually hinder consumption as wage and payrolls growth…

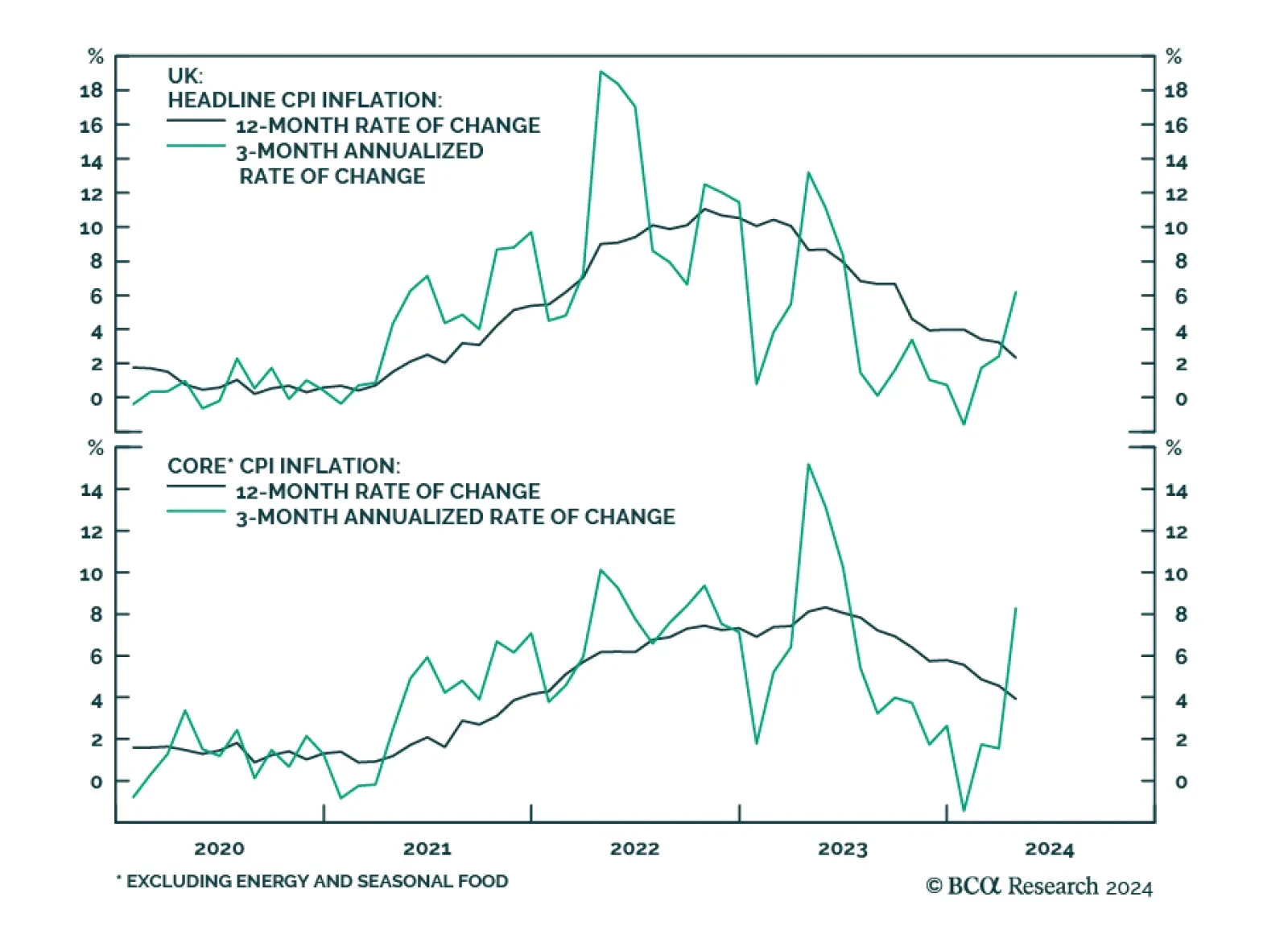

The UK CPI release surprised markets to the upside across the board on Wednesday. Headline CPI increased 2.3% year-on-year, above expectations of 2.1%. Core surprised to the upside as well, moderating from 4.2% to 3.9%y/y, less…

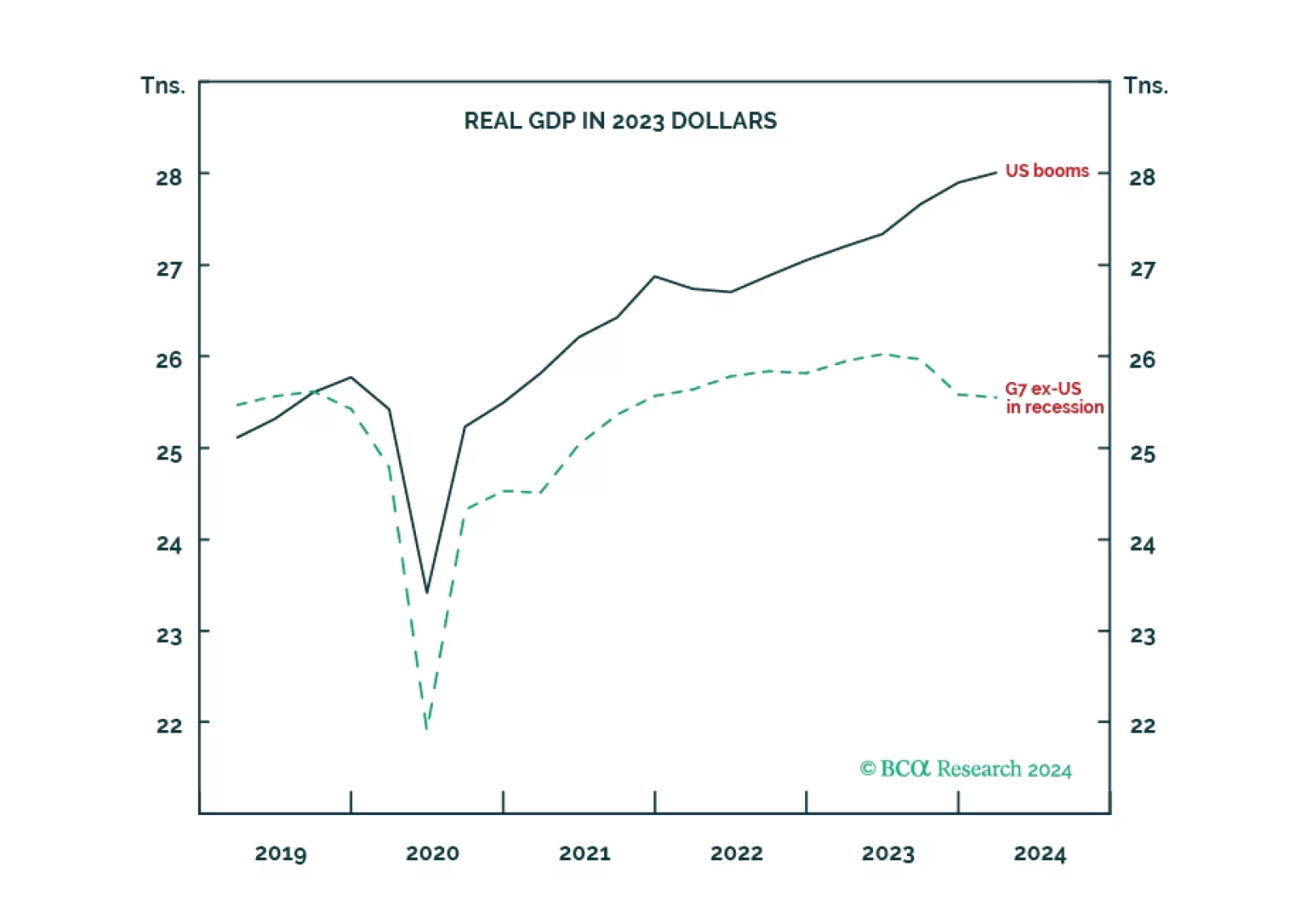

The economic schism in the world economy, between the non-US developed economy in recession and the US in strong growth, is unprecedented during our lifetimes. Now the schism will continue in reverse, as the non-US developed economy…

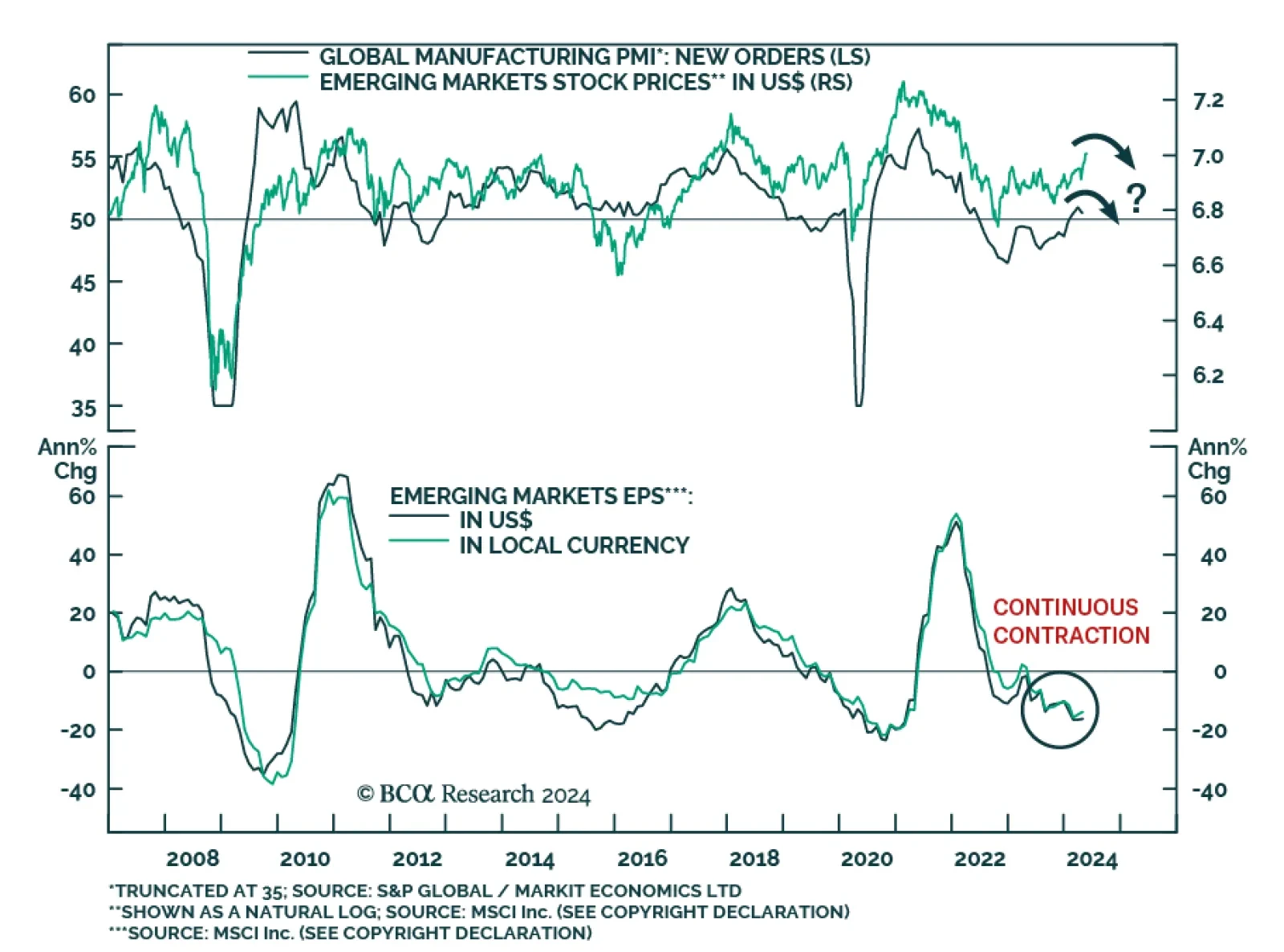

Emerging market stocks have outperformed their global counterparts by 4 percentage points in USD terms since February according to MSCI indices. They have gotten a boost from the bounce in the global manufacturing cycle. The MSCI…

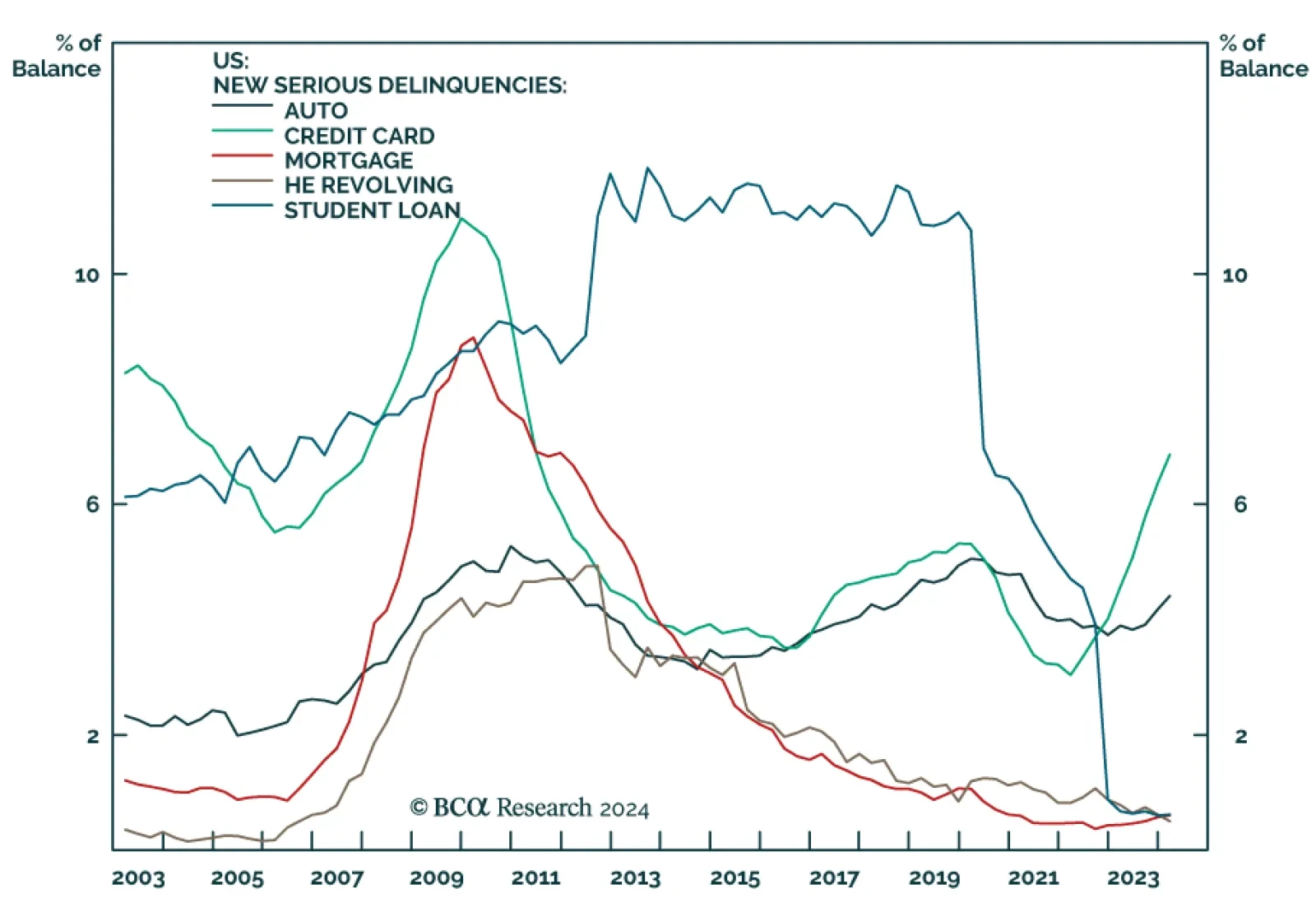

The New York Fed Quarterly Report on Household Debt and Credit indicates that US household debt rose 1.1% q/q in Q1 to $17.7 trillion. Higher mortgage, home equity loan and auto loan balances drove the bulk of the Q1 increase,…

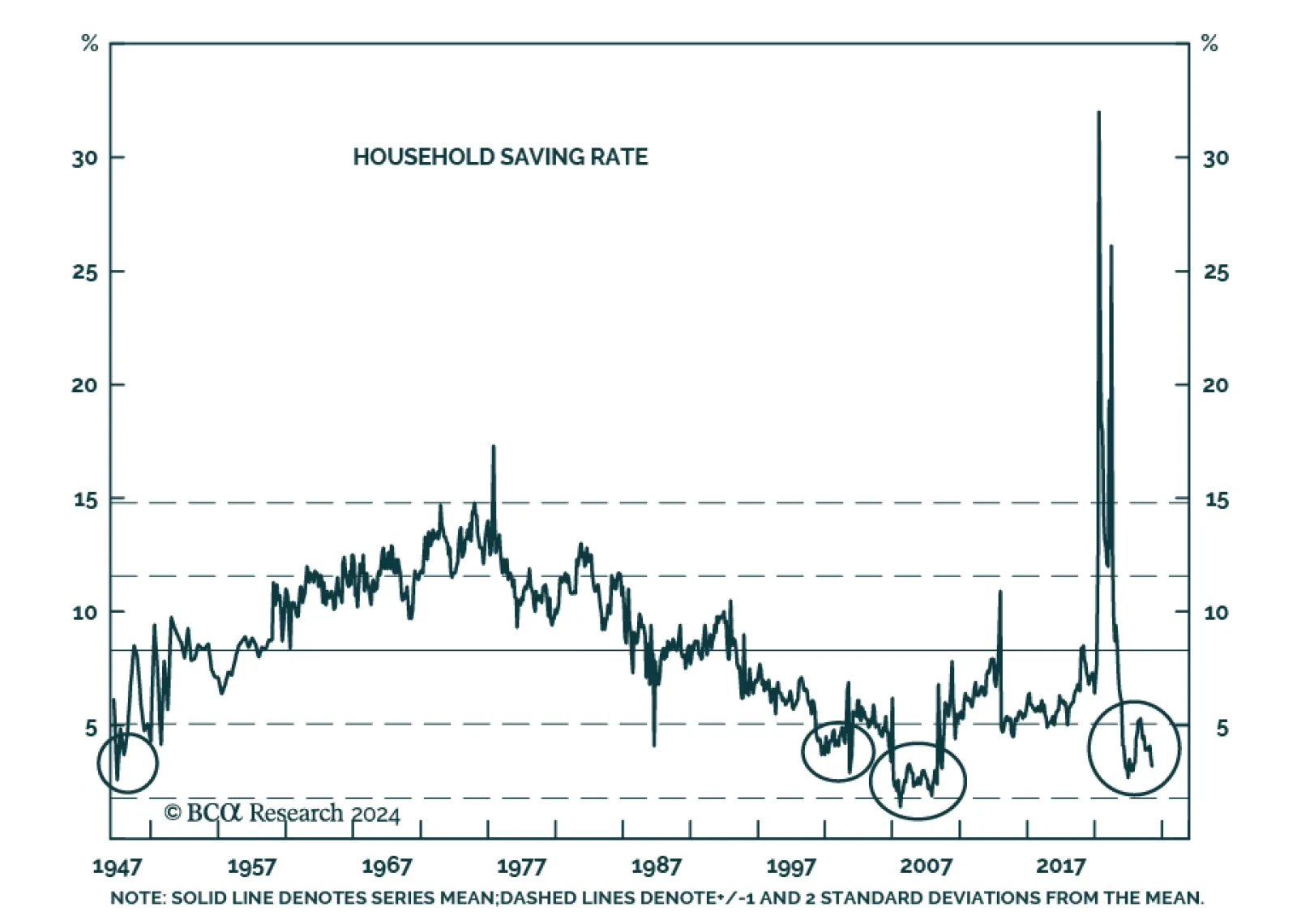

Our US Investment strategists have used the savings rate as a proxy for households’ willingness to spend. Its persistent decline suggests that consumers have been spending their pandemic-era excess savings and our…

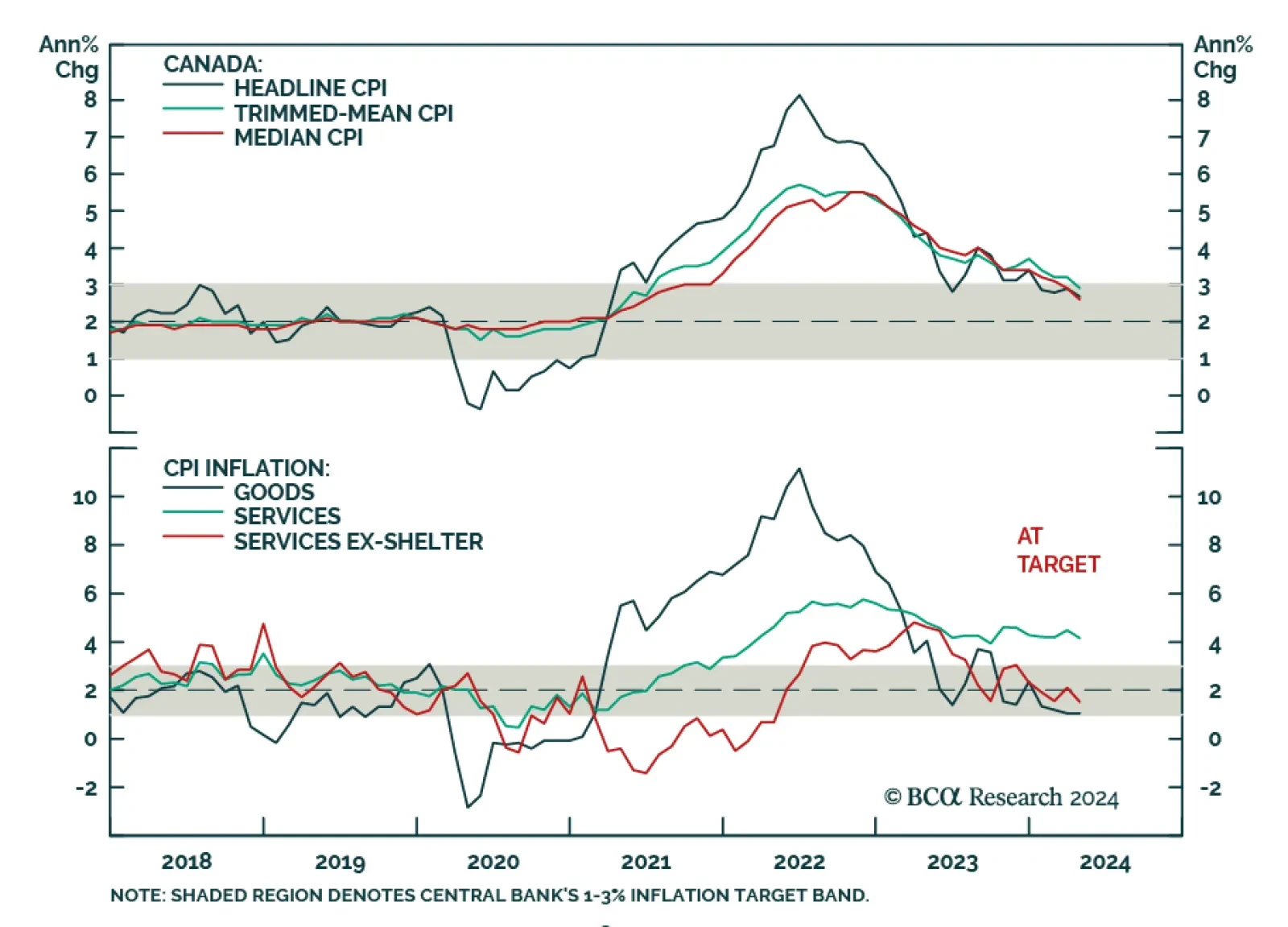

Canada’s headline CPI inflation decelerated in April from 2.9% y/y to 2.7% y/y. Notably, core median CPI eased from 2.9% y/y to a softer-than-anticipated 2.6% y/y and core trimmed-mean CPI ticked lower from 3.2% to 2.9…

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability.…

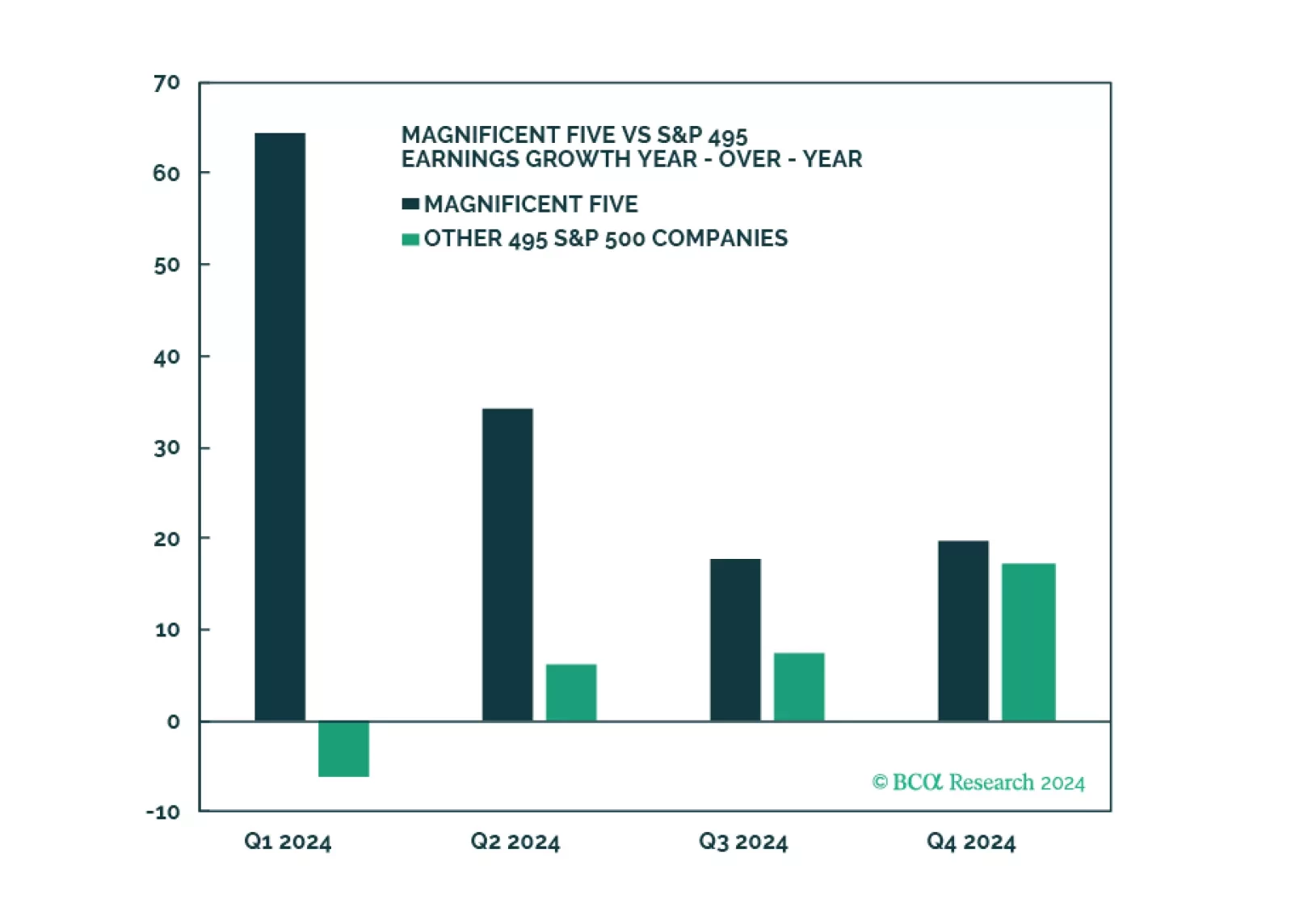

Q1 Earnings and sales growth were strong, but the devil is in the details: Without the Magnificent Five, earnings growth for the index would have been negative. On a positive note, margins have stabilized, and earnings growth is…