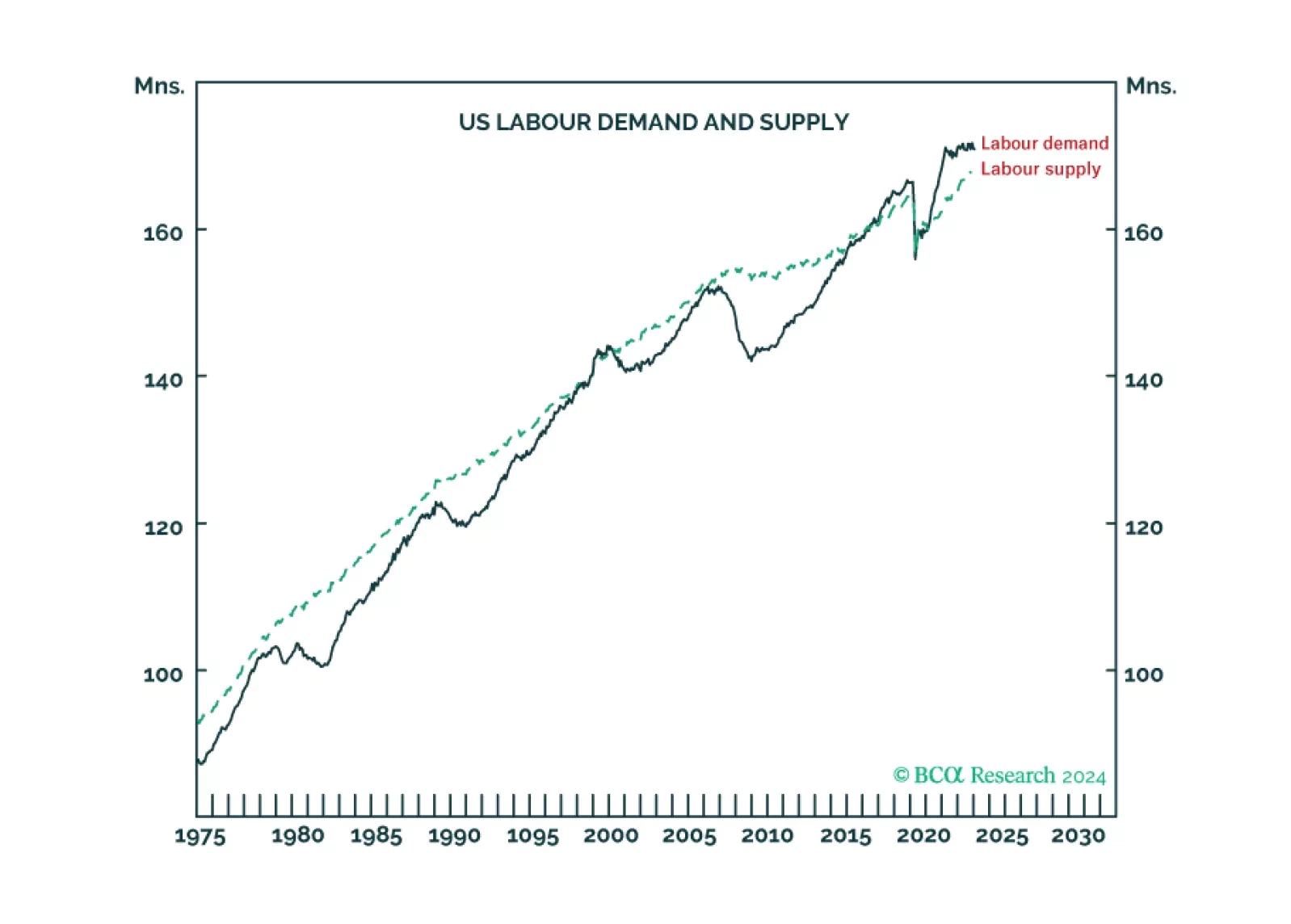

For the first time in at least fifty years, US labour supply is running well below labour demand, meaning the US economy is ‘inverted’. We discuss how and why the economy inverted, and what it means for recession, inflation, and…

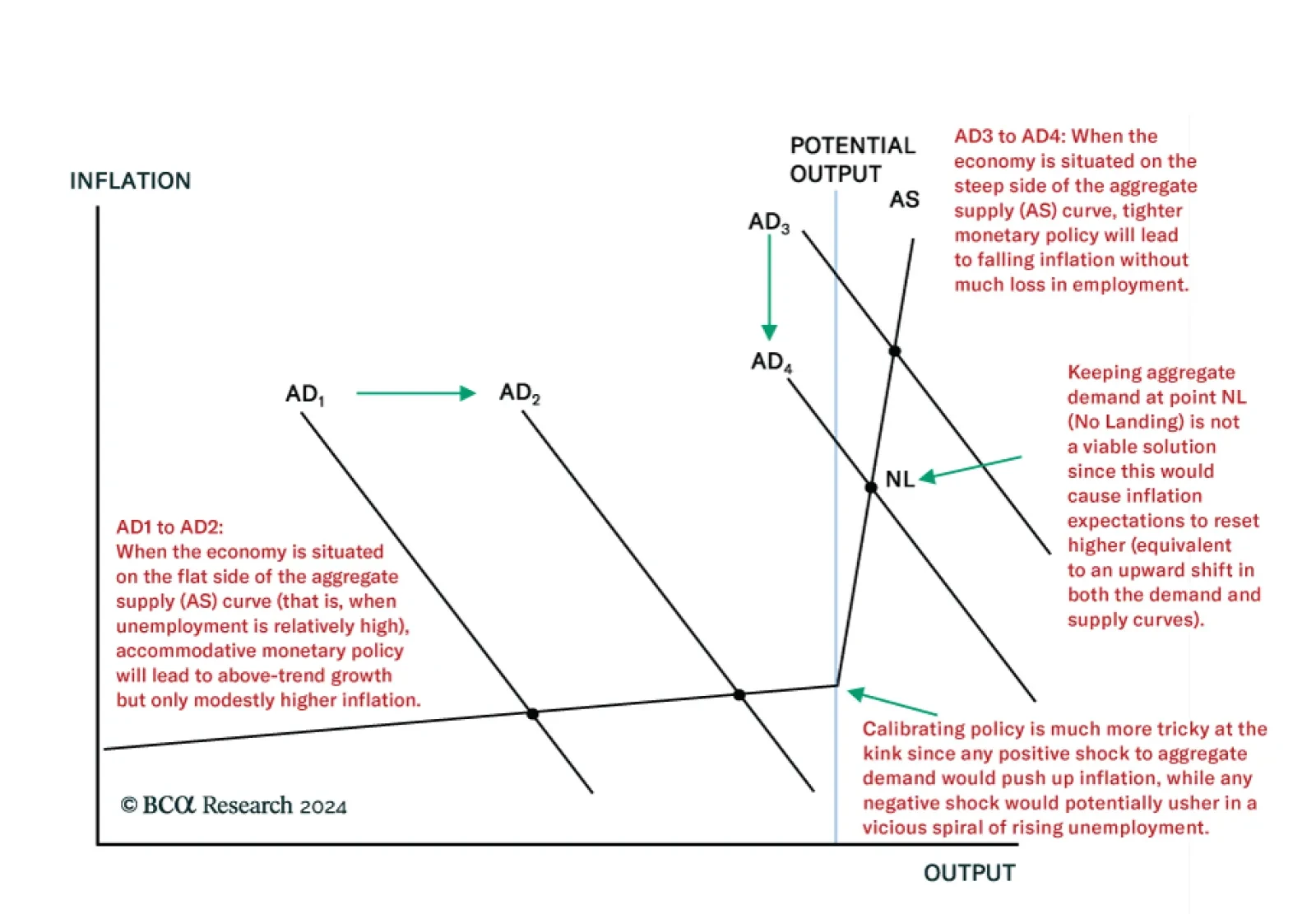

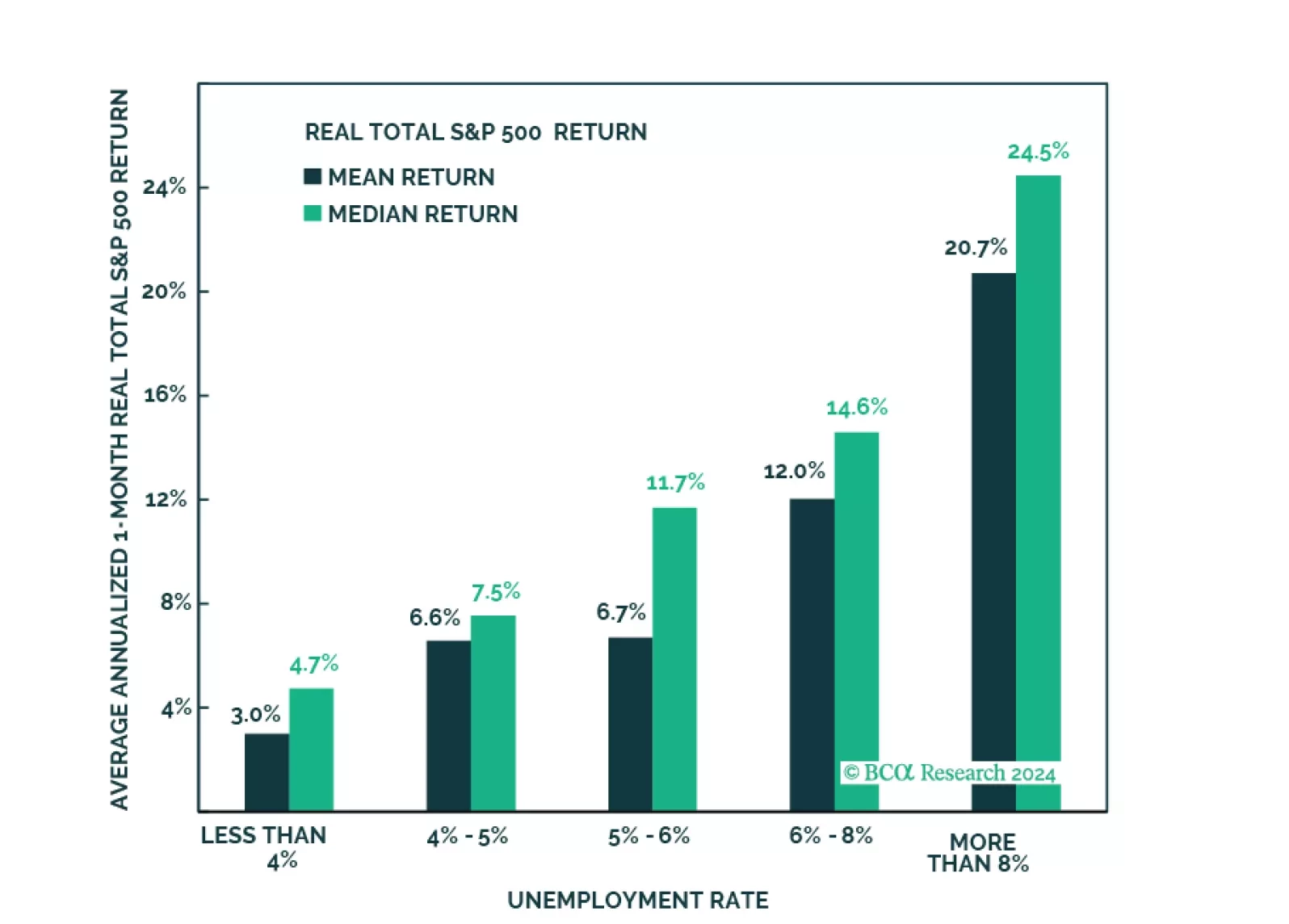

According to BCA Research’s Global Investment Strategy service, the wave of inflation that the US experienced over the past three years cannot be safely repeated. The unemployment rate is a highly mean-reverting series:…

The US equity rally has recently stopped narrowing with the gap between the market cap-weighted and equal-weighted indices for the S&P 500 stabilizing over the past month. Indeed, this has coincided with a shift in market…

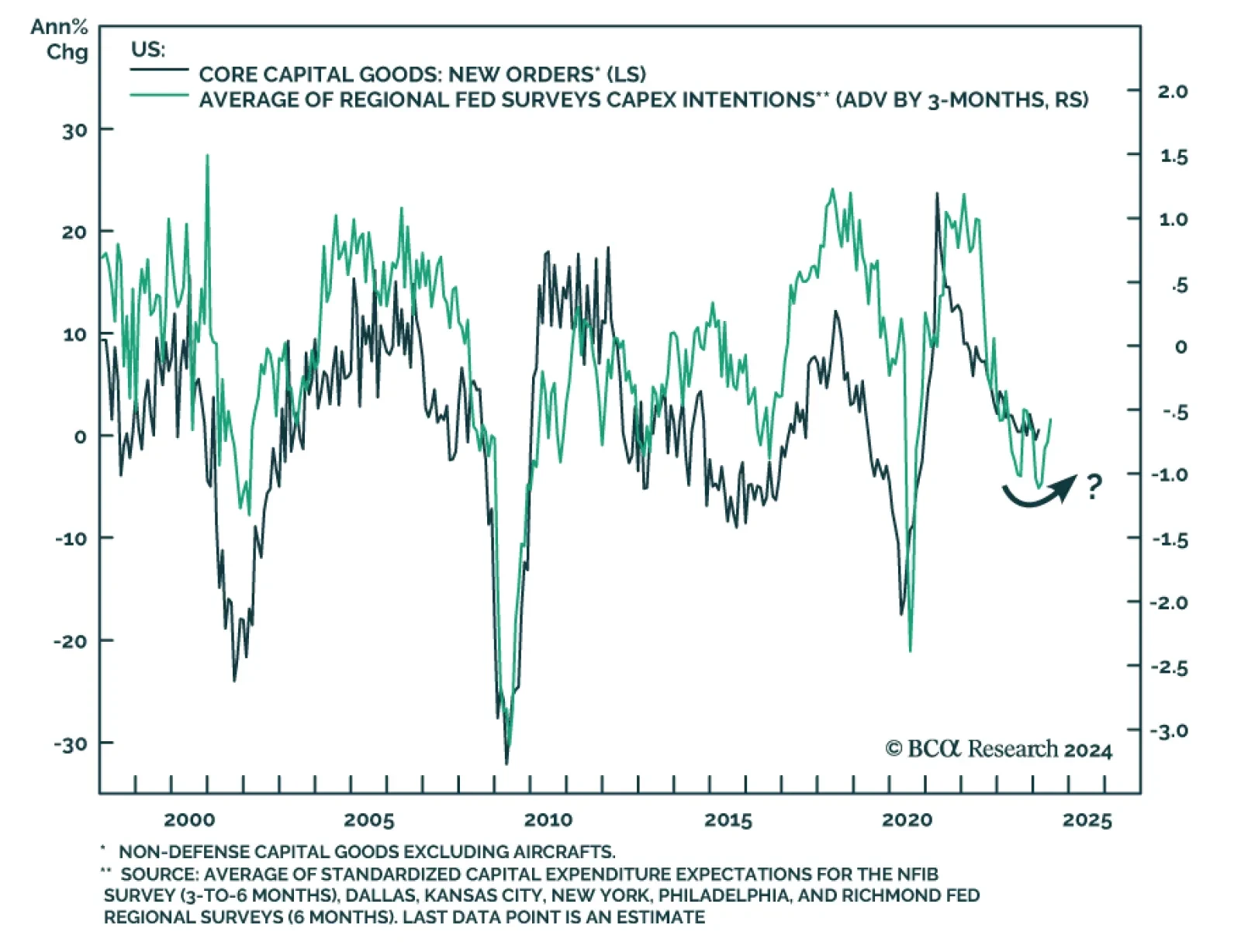

US durable goods orders delivered a positive signal for the business spending outlook. The 1.4% increase in new orders for durable goods in February marks the first expansion in three months and beat expectations of a 1.0%…

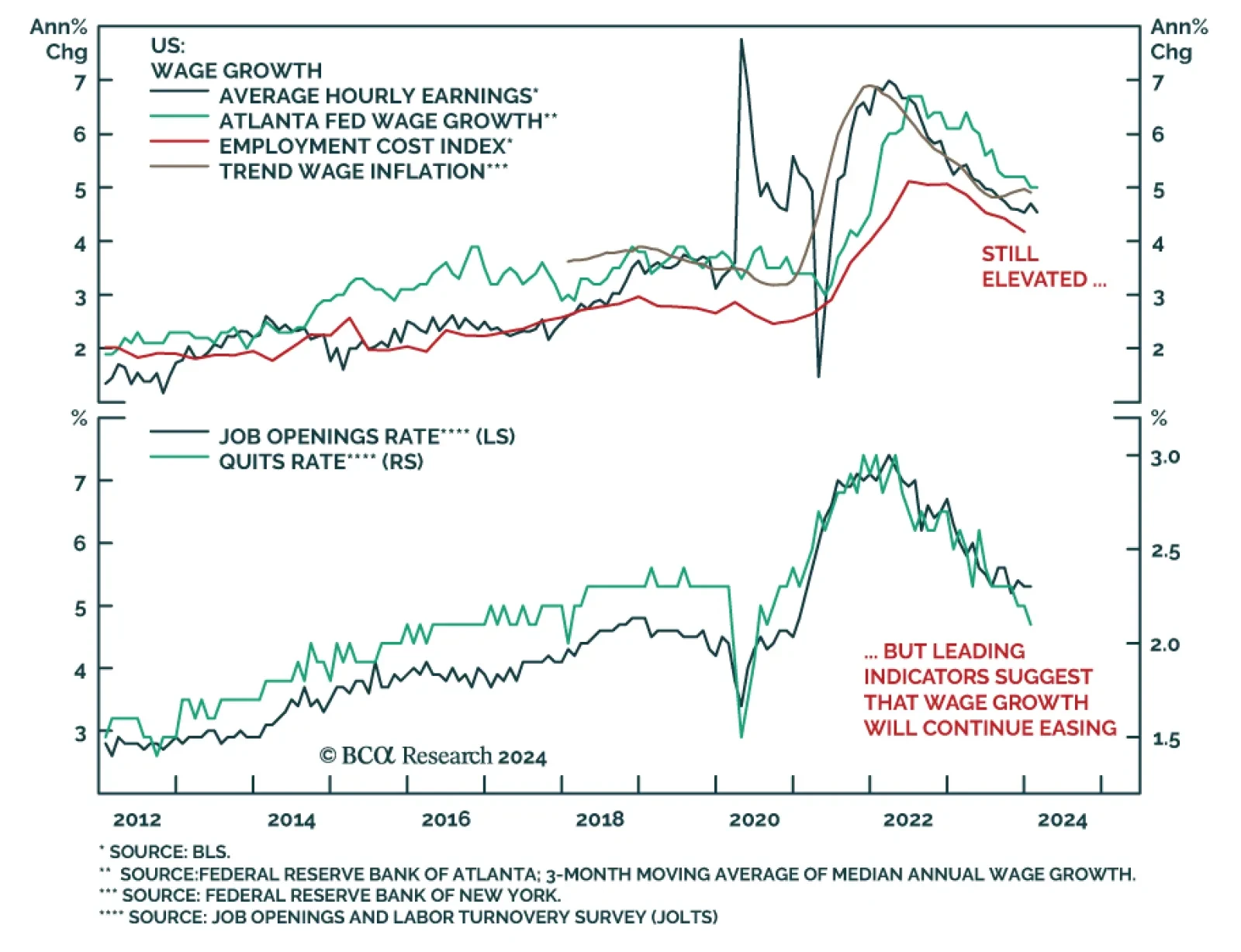

In Fed chair Jay Powell’s opening remarks at last week’s press conference, he noted that wage growth has been moderating and that FOMC participants expect a continued rebalancing of the labor market to help ease price…

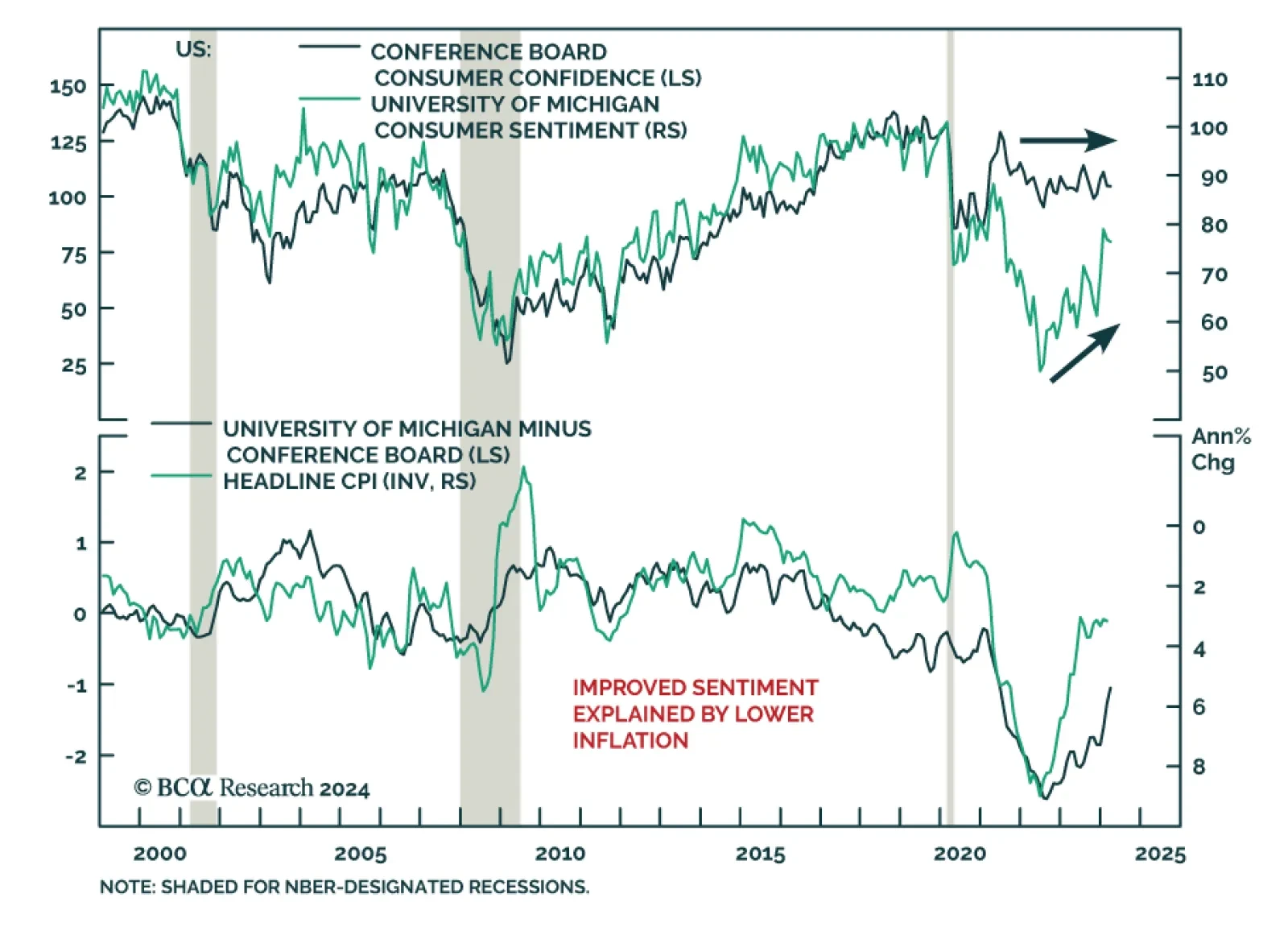

The Conference Board’s gauge of US consumer confidence came in at 104.7 in March – broadly unchanged from a downwardly revised 104.8 in February and below expectations of an improvement to 107. The Expectations Index…

In this Strategy Outlook we examine why, contrary to popular perception, the odds of a global recession over the next 12 months are rising not falling.

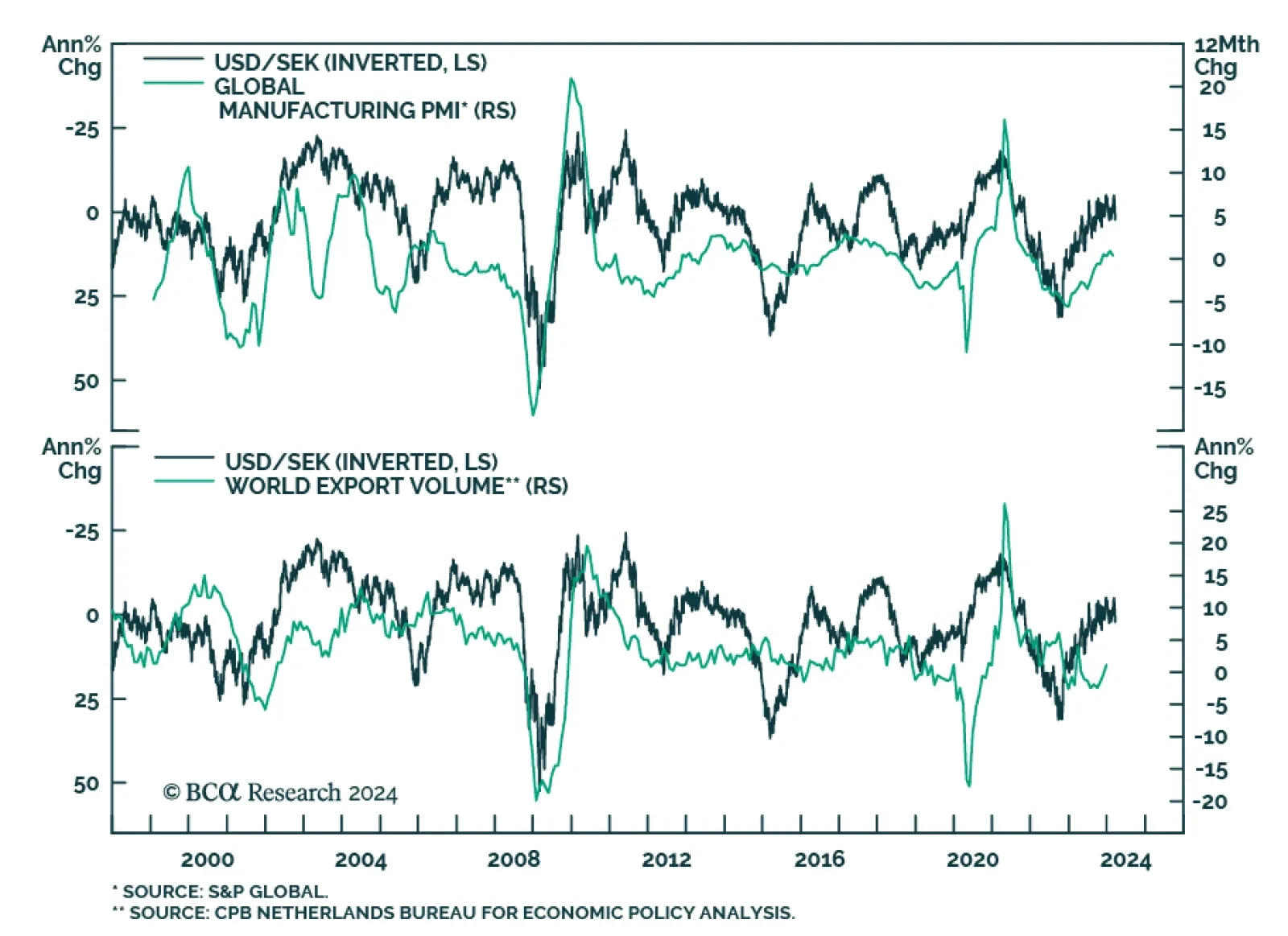

Swedish economic data is usually good at sniffing out the outlook for global growth. Looking at a broad swath of indicators, from domestic conditions to barometers of external demand, our colleagues from BCA’s Foreign…

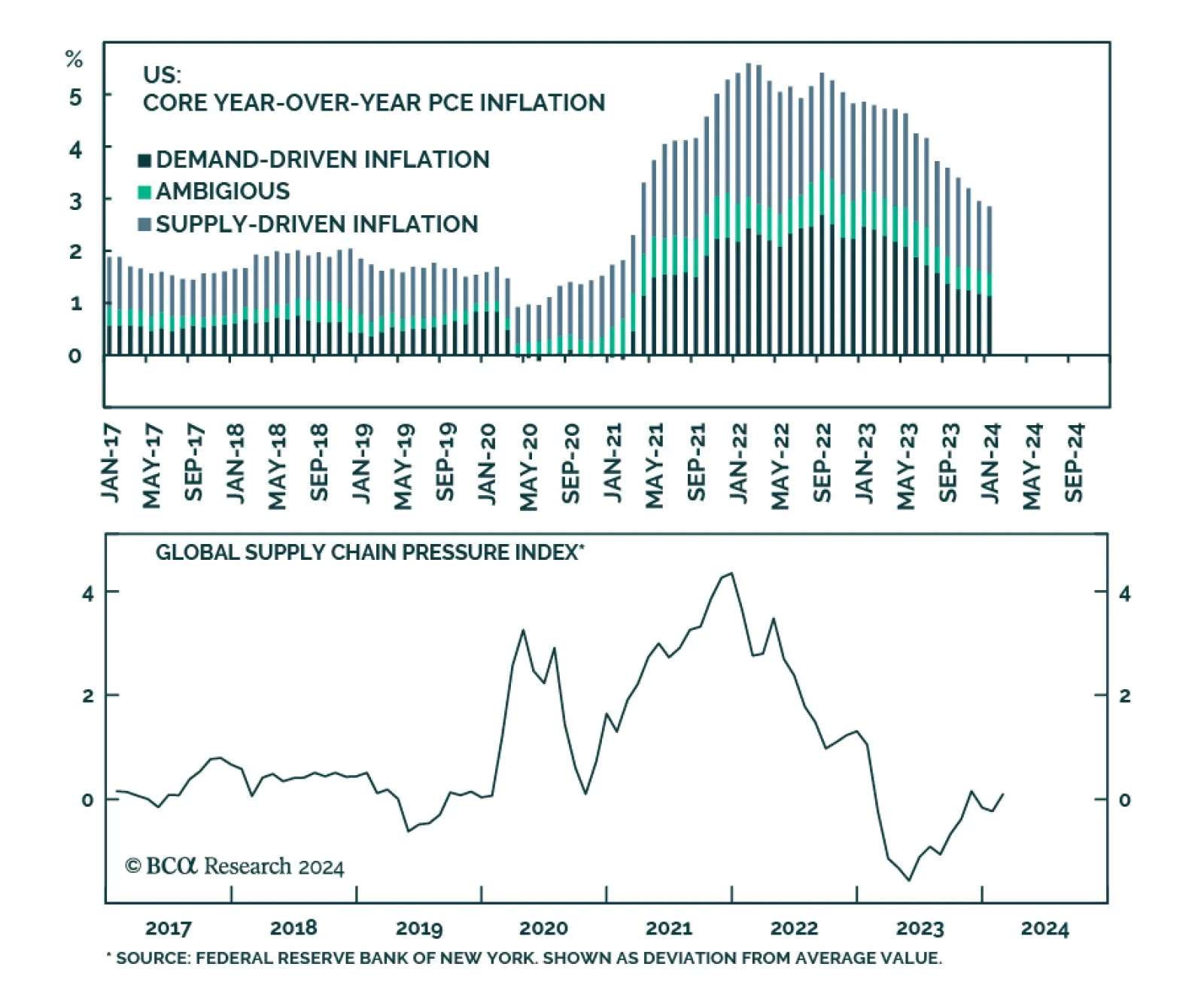

Both supply- and demand-side forces contributed to the inflation surge in 2021/2022. According to the San Francisco Fed’s estimates, the contribution of demand-side forces to annual core PCE inflation jumped from -0.09…