Economy

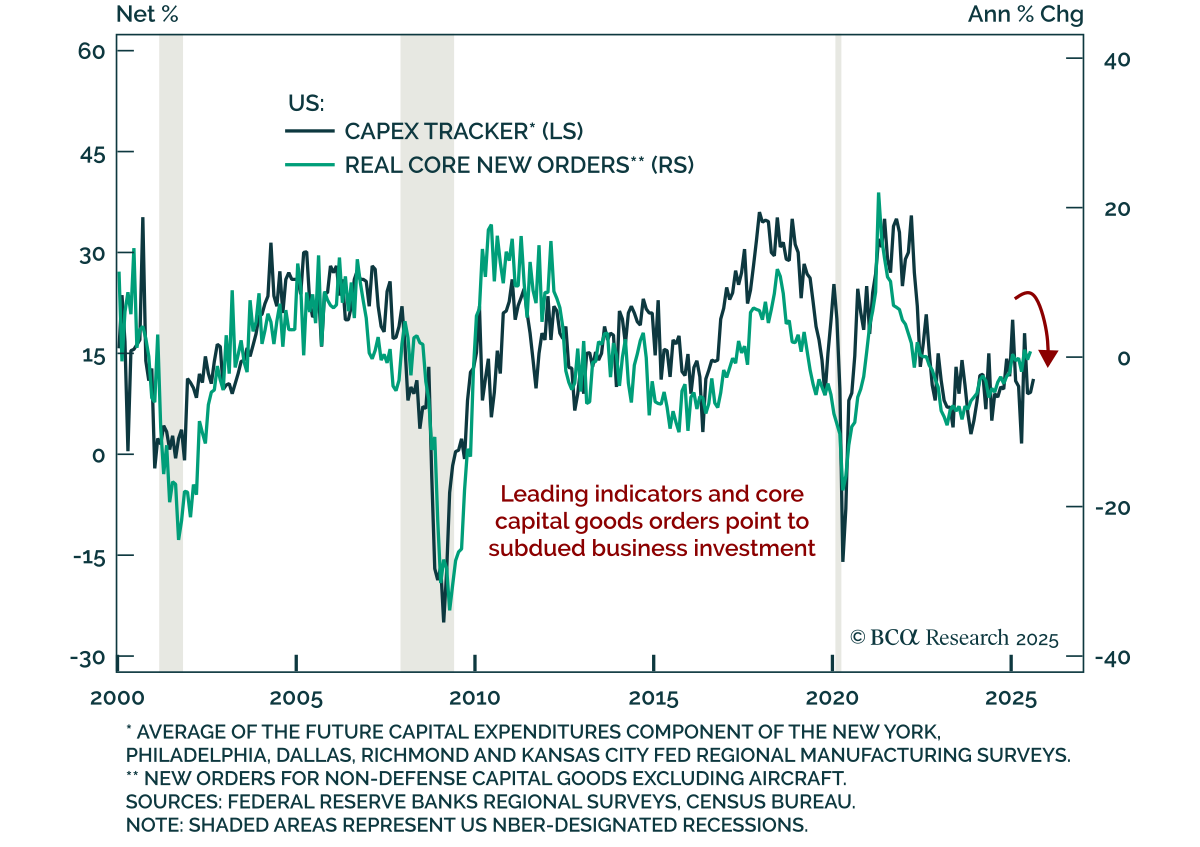

July US durable goods orders rebounded, but investment signals remain subdued and favor duration and tech. Orders fell 2.8% m/m after a 9.4% June drop, better than expected. Core measures excluding volatile components were stronger, with nondefense…

Australia’s July CPI surprise does not justify the aggressive easing priced, keeping us underweight ACGBs. Headline inflation accelerated to 2.8% y/y from 1.9% in June, with trimmed mean rising to 2.7% from 2.1%. Despite the rebound, inflation remains…

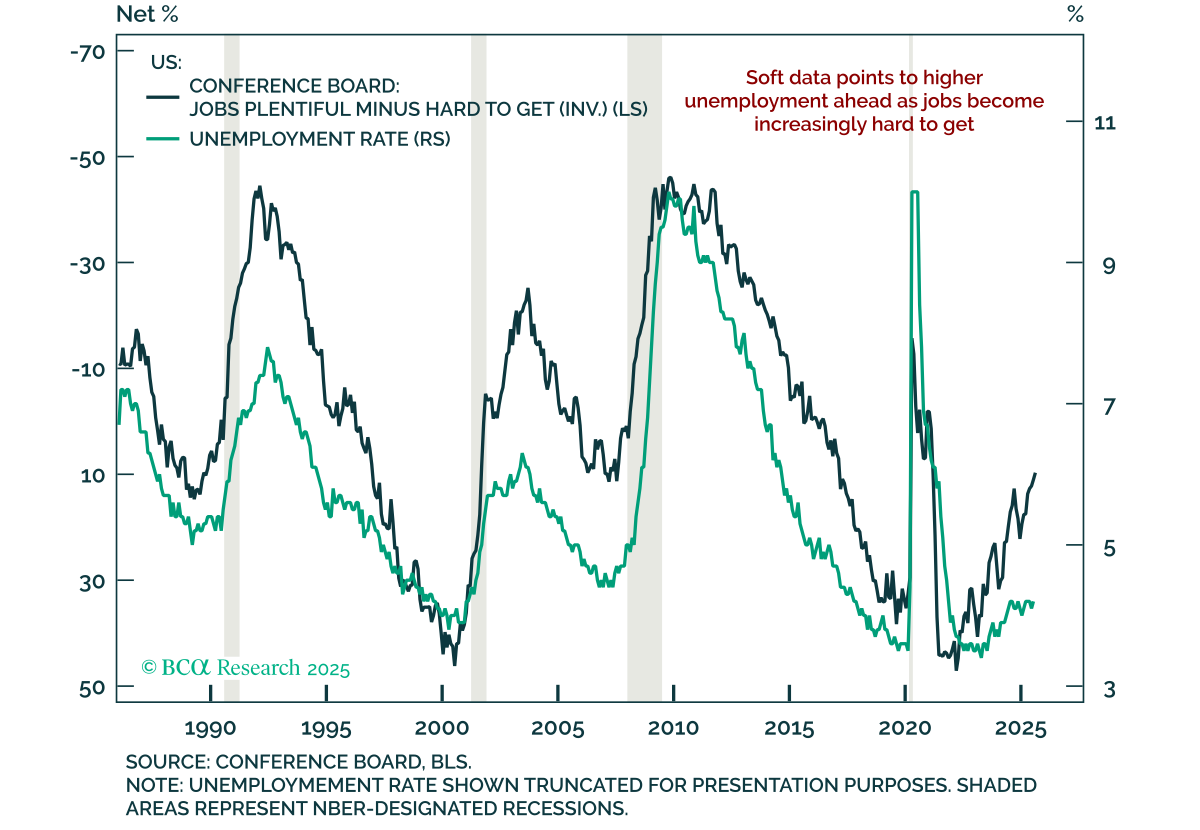

Mixed consumer confidence data and weakening labor signals argue for a modestly defensive stance. The August Conference Board Consumer Confidence Index beat expectations but fell from an upwardly revised 98.7. The present situation component edged lower…

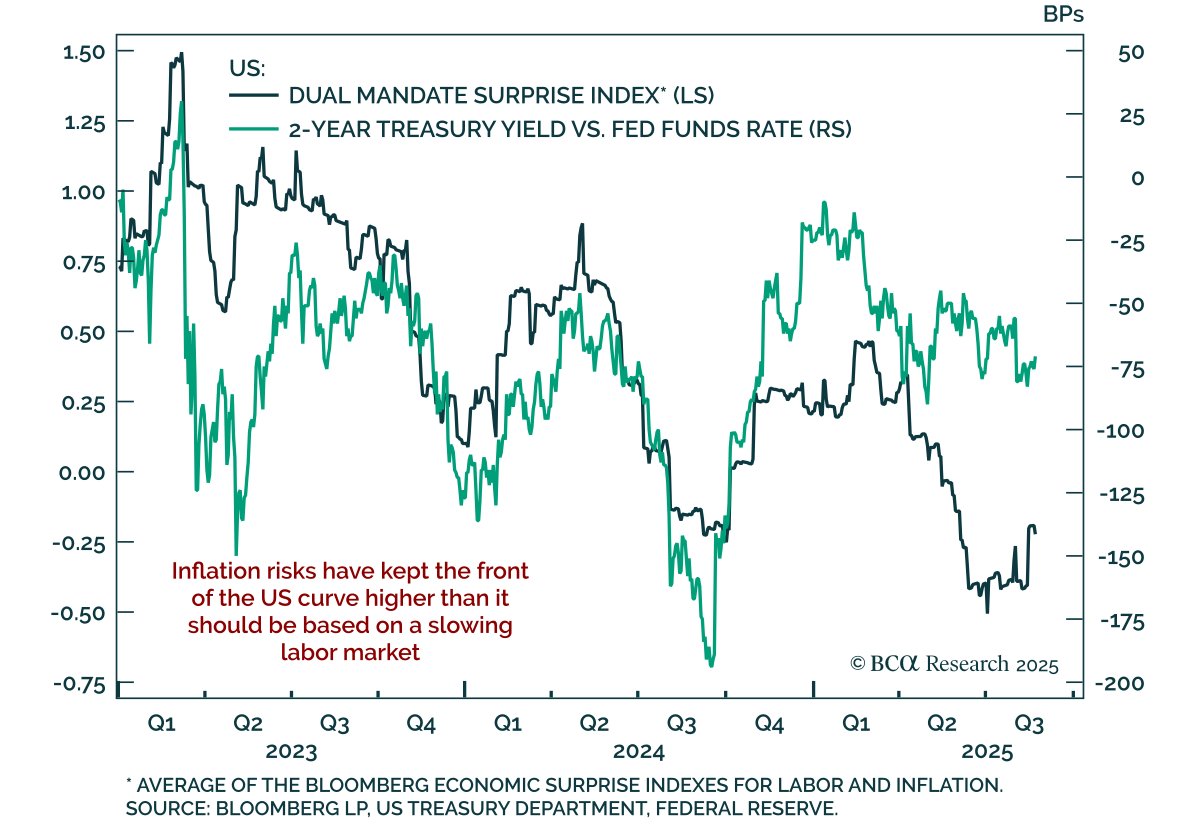

Powell’s Jackson Hole speech was misread, and points to cautious dovishness. Some commentators called it hawkish, others suggested the Fed abandoned its 2% target. Neither is accurate. Central bank communication is rarely binary; it operates across…

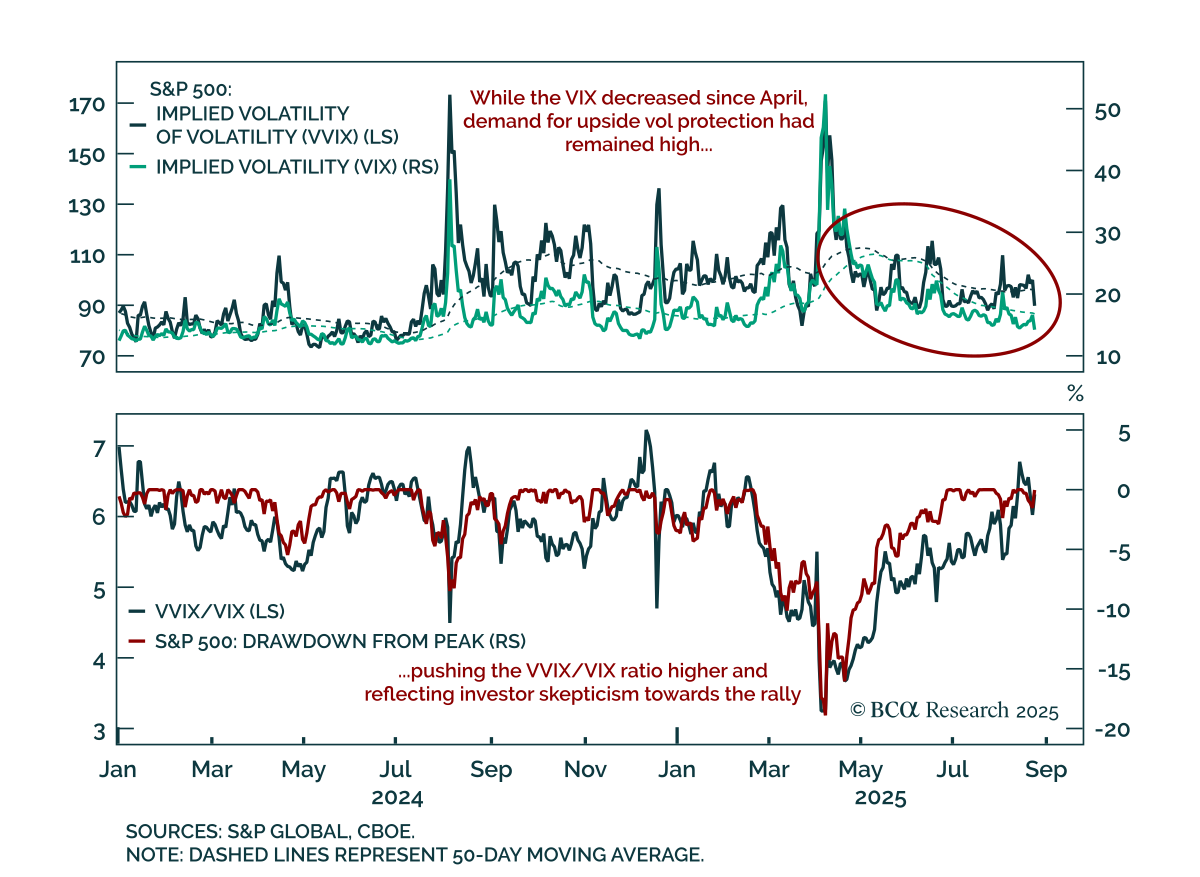

The post-Liberation Day rally has broadened, reducing skepticism and strengthening the case for US outperformance versus Europe. The S&P 500’s climb to all-time highs has been unusually smooth, compressing realized volatility and pulling the VIX…

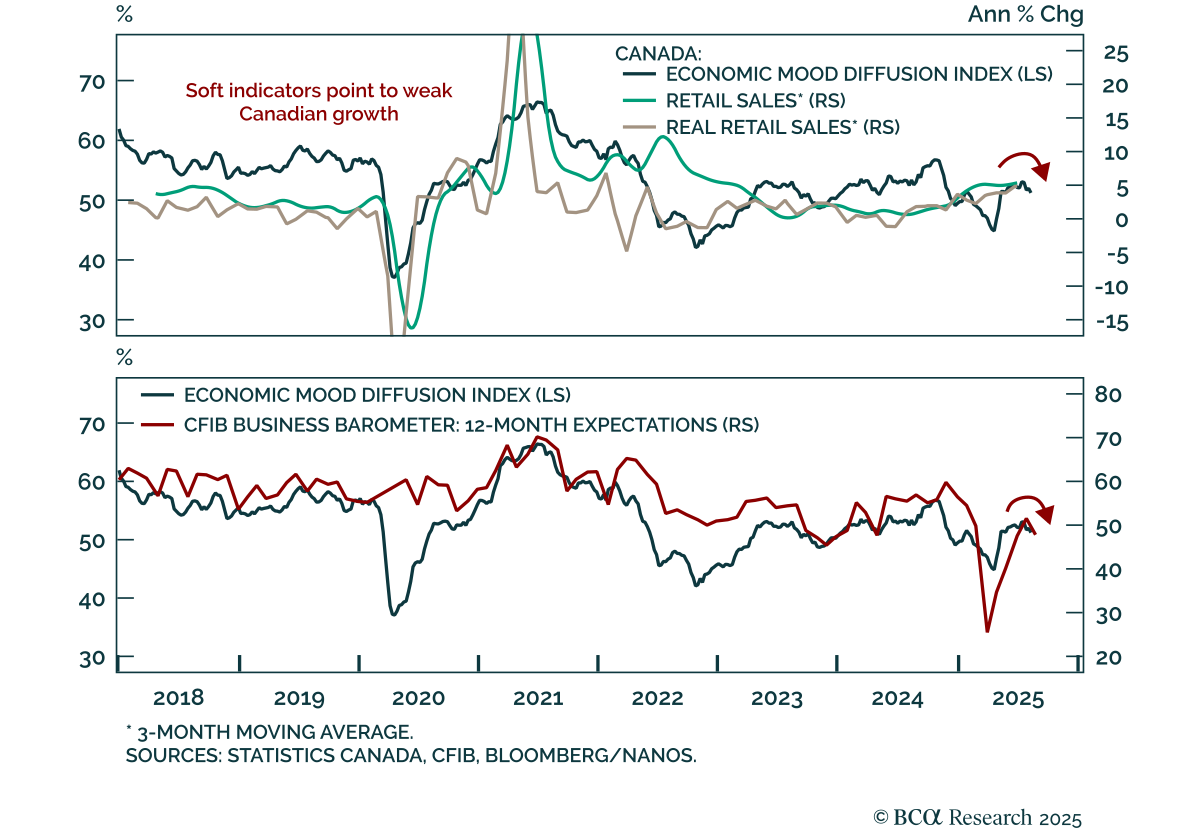

Canada’s fragile growth backdrop reinforces the case for more BoC easing than markets price. June retail sales rose 1.5% m/m, in line with expectations. Excluding autos, sales were stronger at 1.9%. However, the advance estimate for July points to a 0.8%…

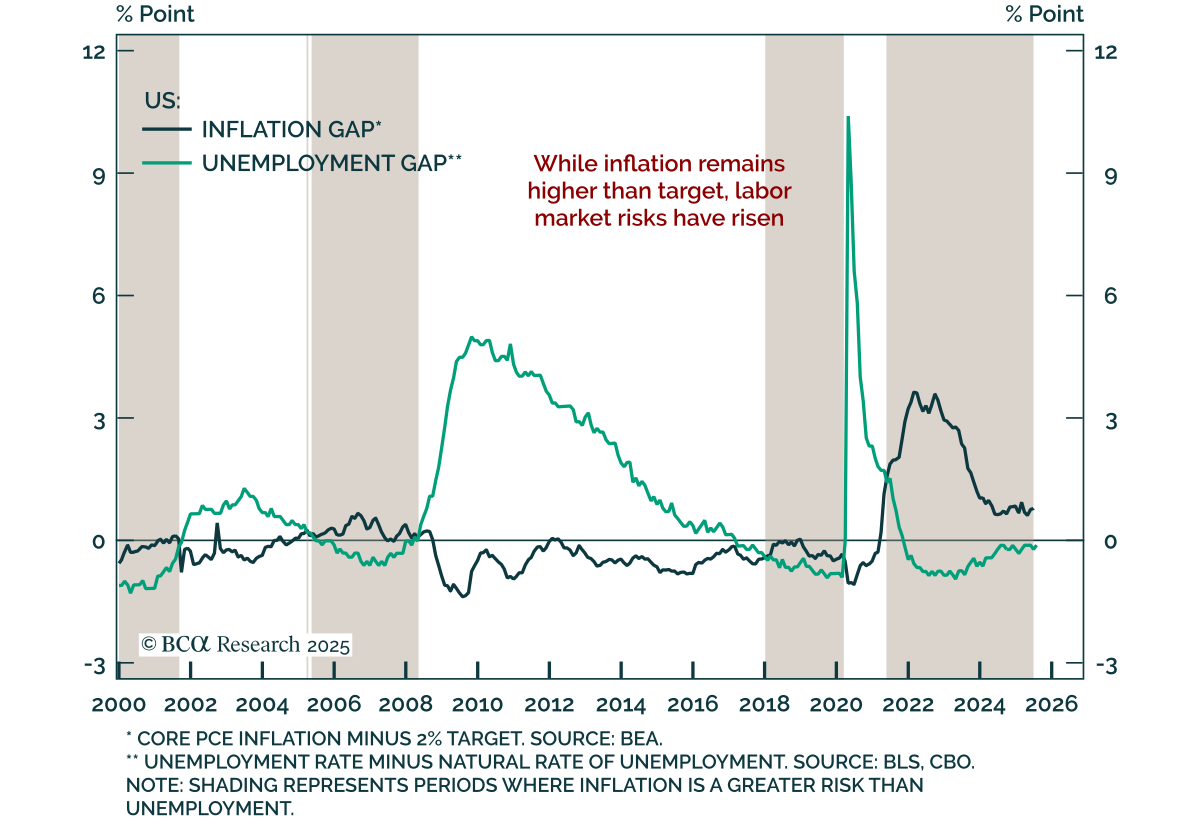

Powell’s final Jackson Hole speech signaled a dovish tilt, opening the door to a September cut. The Fed is under pressure to balance unemployment and inflation risks, with the FOMC split between “proactive” doves and “reactive” hawks. Recent data have not…

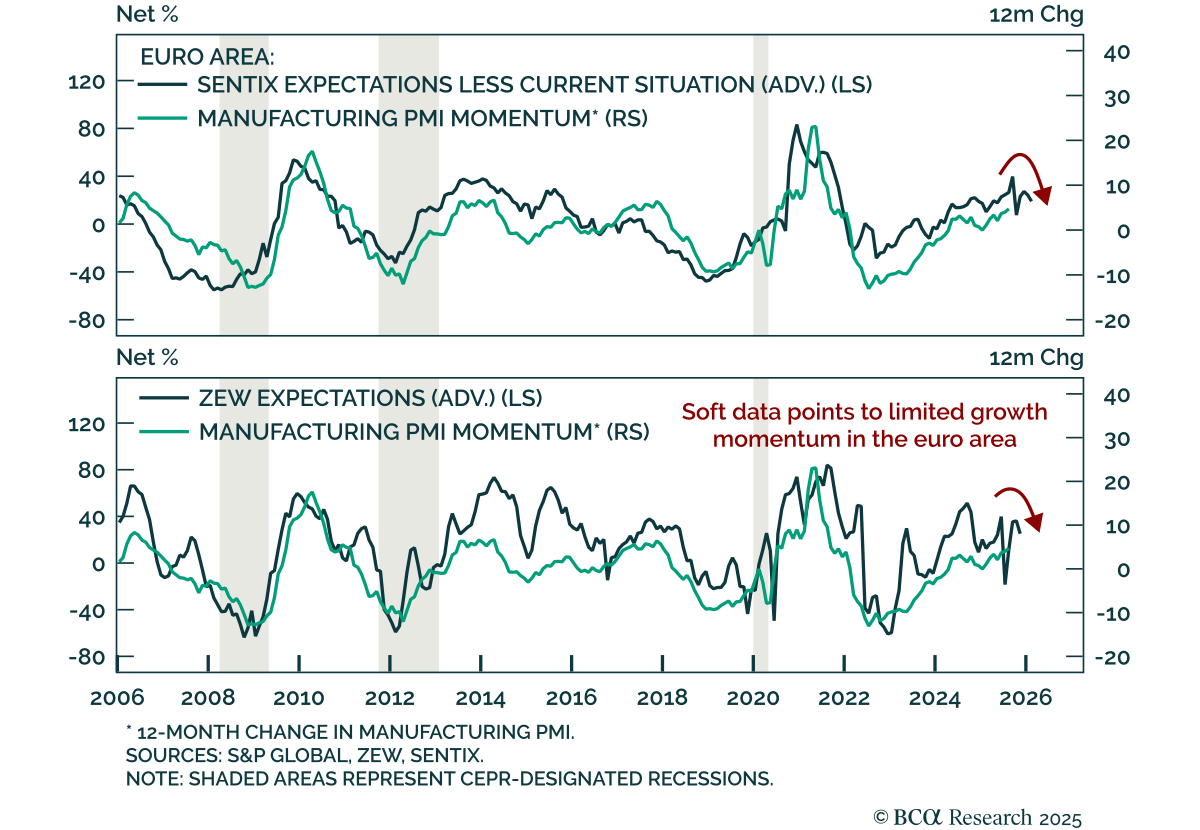

Although Euro area PMIs beat expectations in August, the growth outlook remains weak. The composite index rose to 51.1, driven by manufacturing returning to expansion at 50.5 from 49.8. Meanwhile the services PMI slipped 0.3 points to 50.7. The readings…

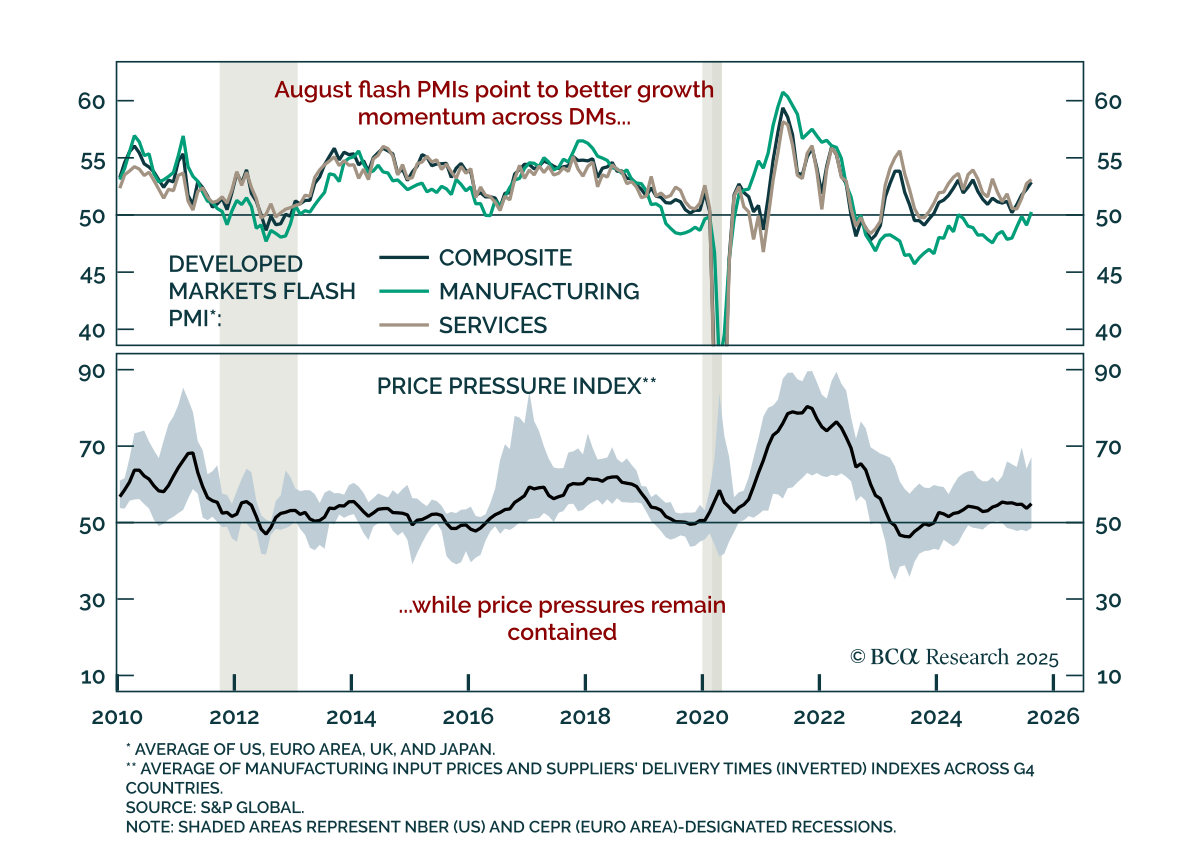

Flash August PMIs show tentative global momentum yet growth remains weak. The composite PMI improved in both the US (55.4 vs. 55.1) and euro area (51.1 vs. 50.9), with manufacturing moving into expansion for the first time in 18 months. US manufacturing…

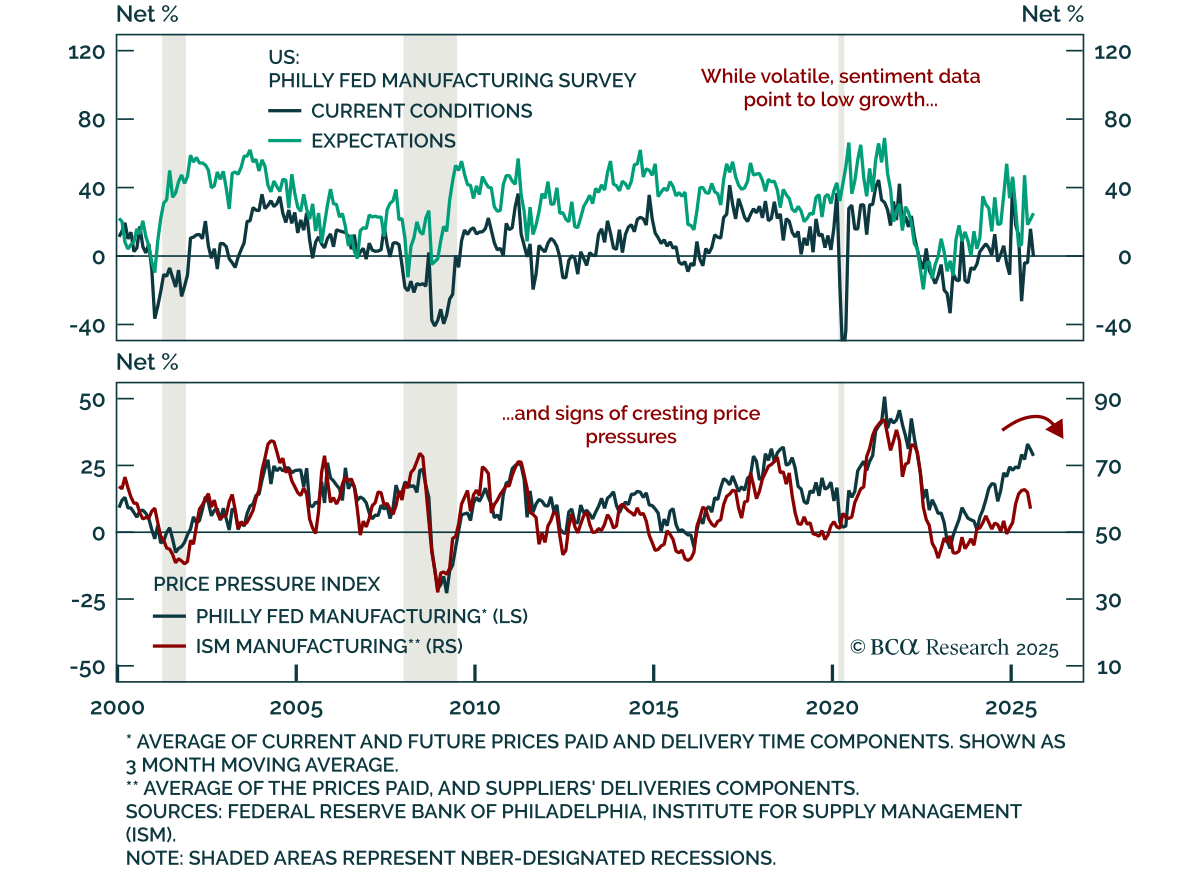

The Philly Fed’s August dip confirms persistent US manufacturing weakness and sends a disinflationary impulse. The index fell to -0.3 from 15.9 in July, with shipments, employment, and new orders all declining, the latter slipping into contraction.…