Economy

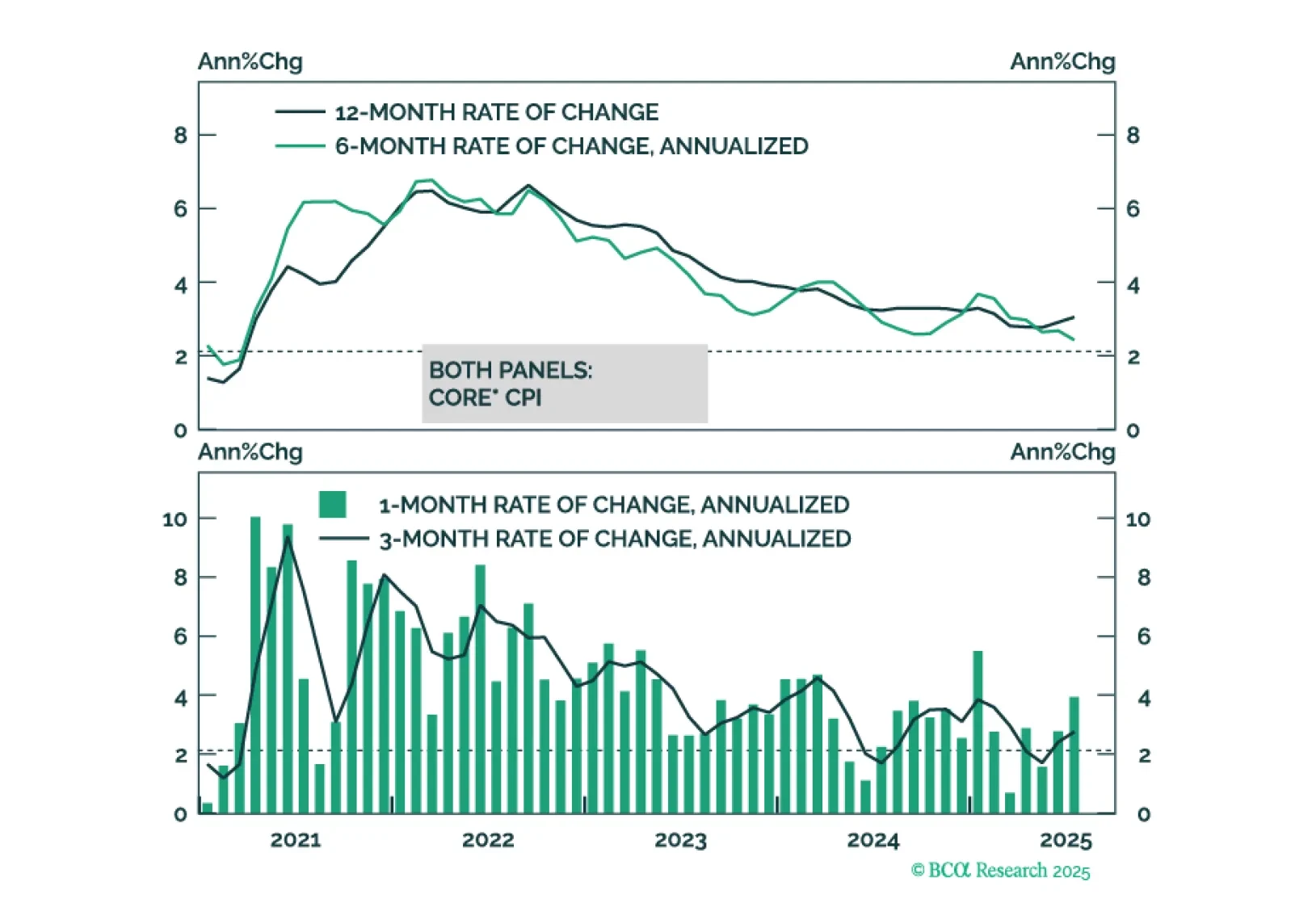

This morning’s CPI report marginally tips the scales in favor of a September rate cut.

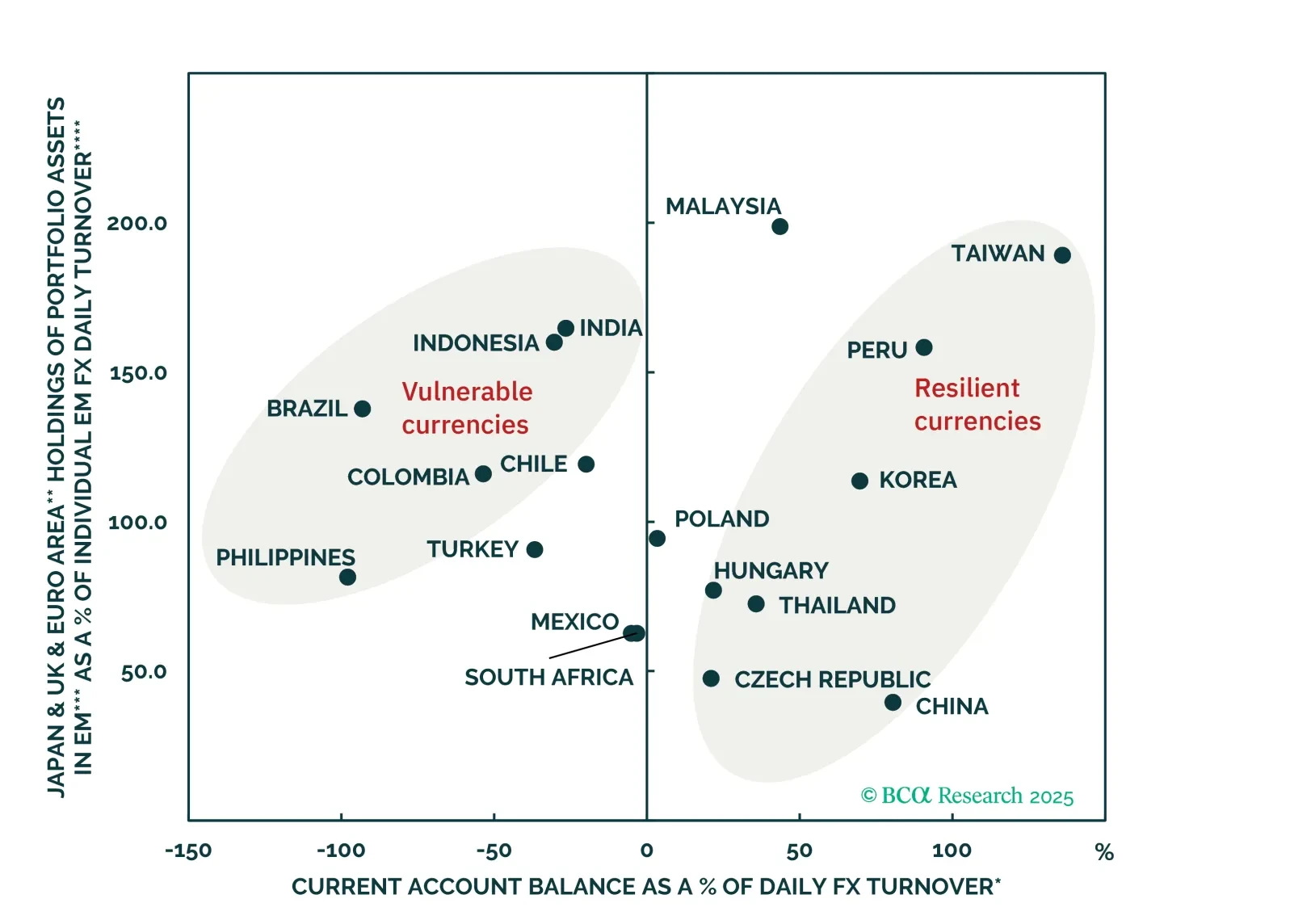

Despite widespread investor optimism Brazil’s currency outlook is challenged by a toxic mix of poor external, fiscal, and macro fundamentals. Expect BRL to underperform most EM peers.

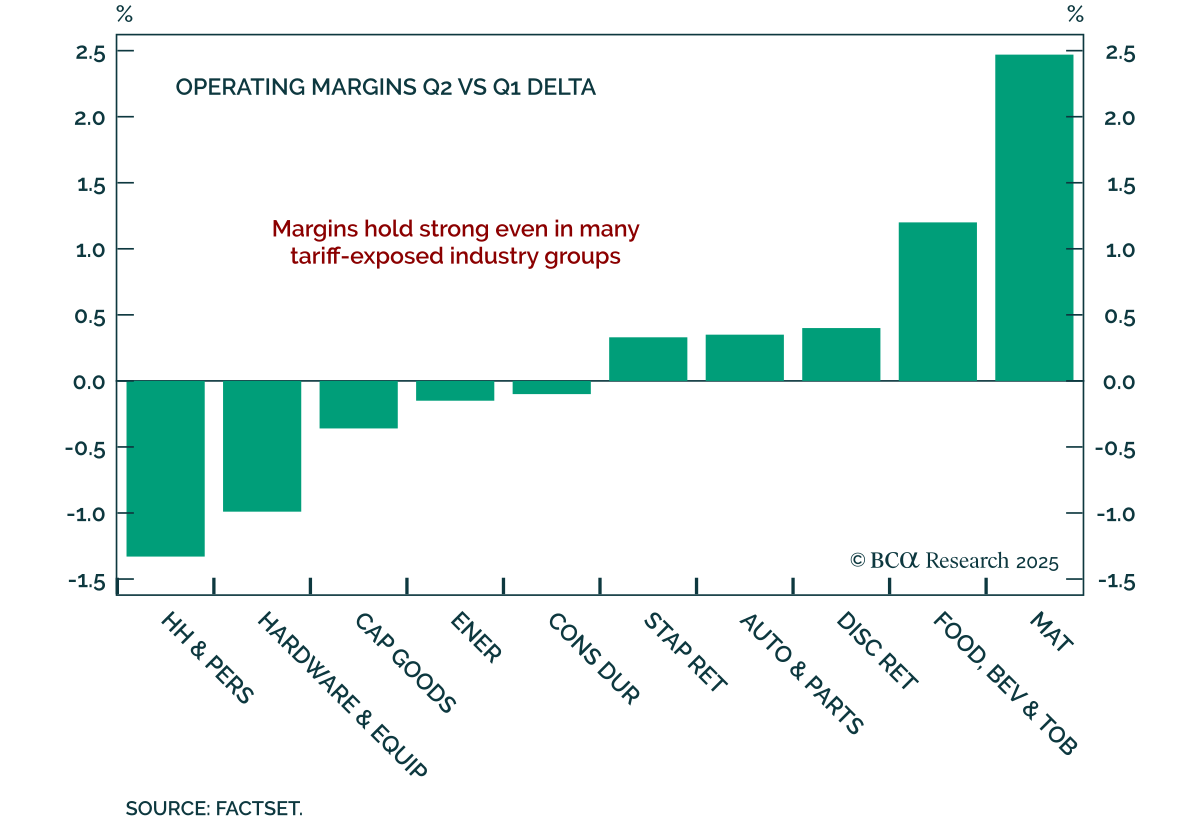

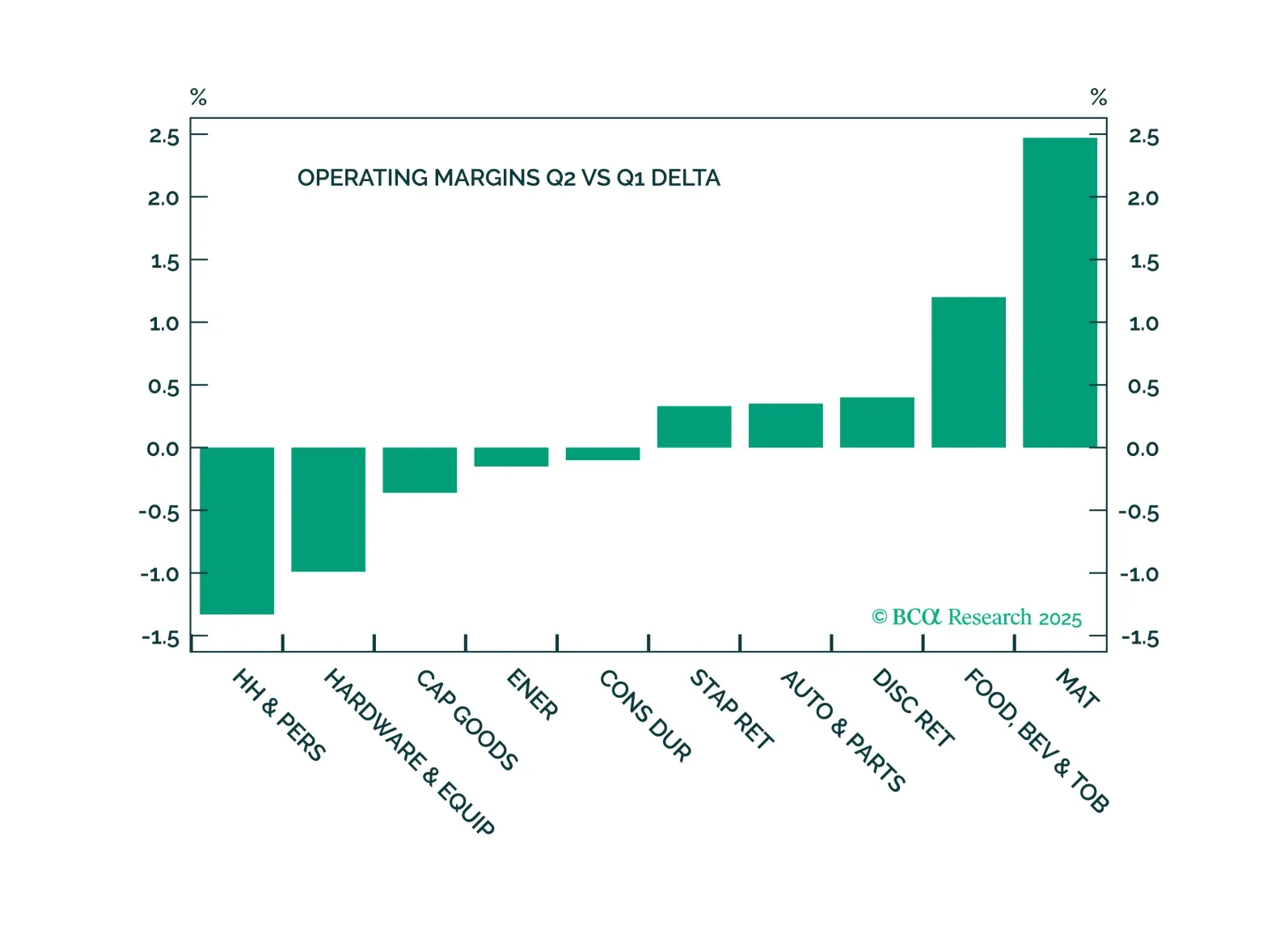

The Q2 earnings season delivered solid earnings and sales growth and resilient margins, reassuring investors that corporate America remains in good health and is capable of navigating economic uncertainty while mitigating the impact of new trade levies. The outlook is generally positive, but with one important caveat: The full effect of tariffs has yet to materialize.

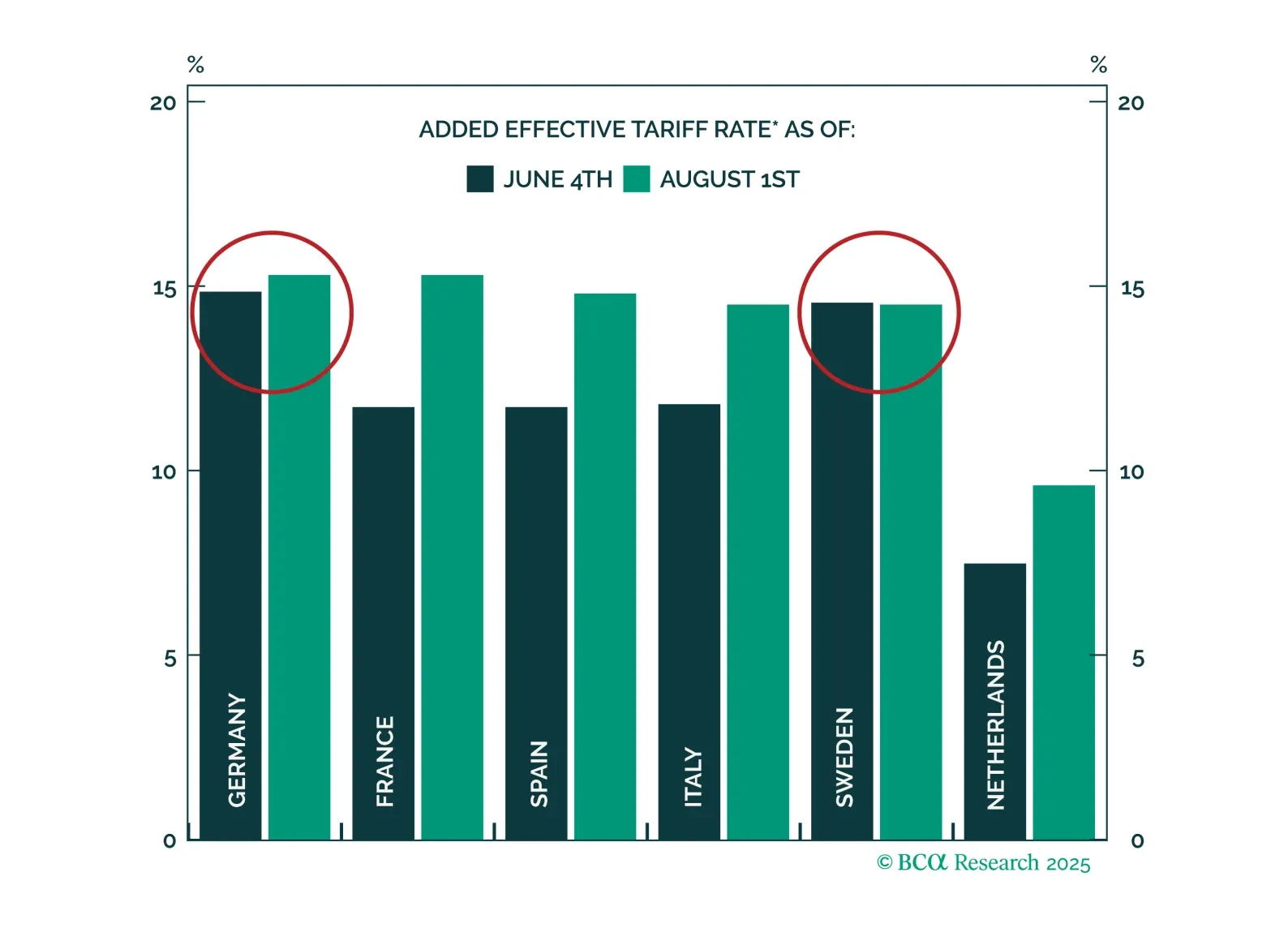

US tariffs will not derail the low-inflation economic recovery underway in the Euro Area. Investors should overweight European equities, focusing on parts of the market more insulated from tariffs.