Economy

Our Portfolio Allocation Summary for June 2026.

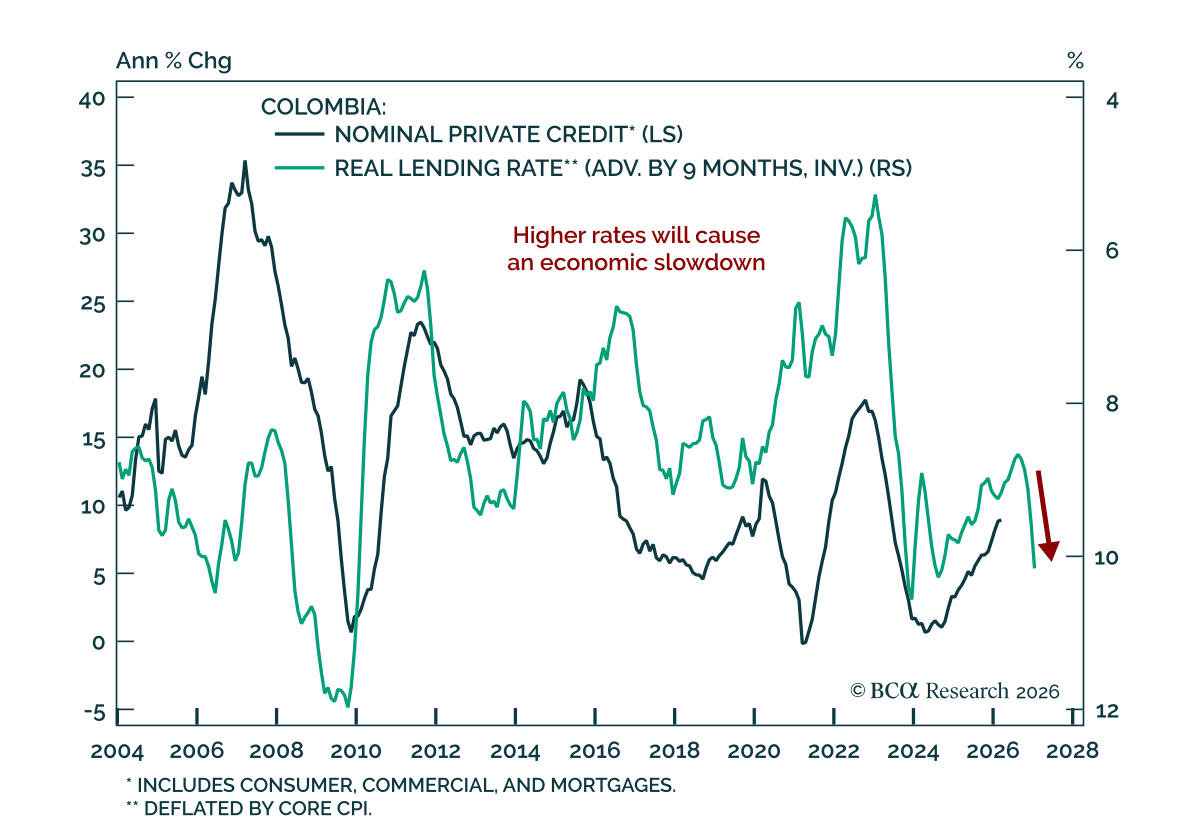

Our EM strategists view the rally in Colombian assets as being on borrowed time and recommend using near-term strength to reduce exposure. Colombia displays the markings of an attractive comeback story, with high interest rates, elevated oil prices, and a…

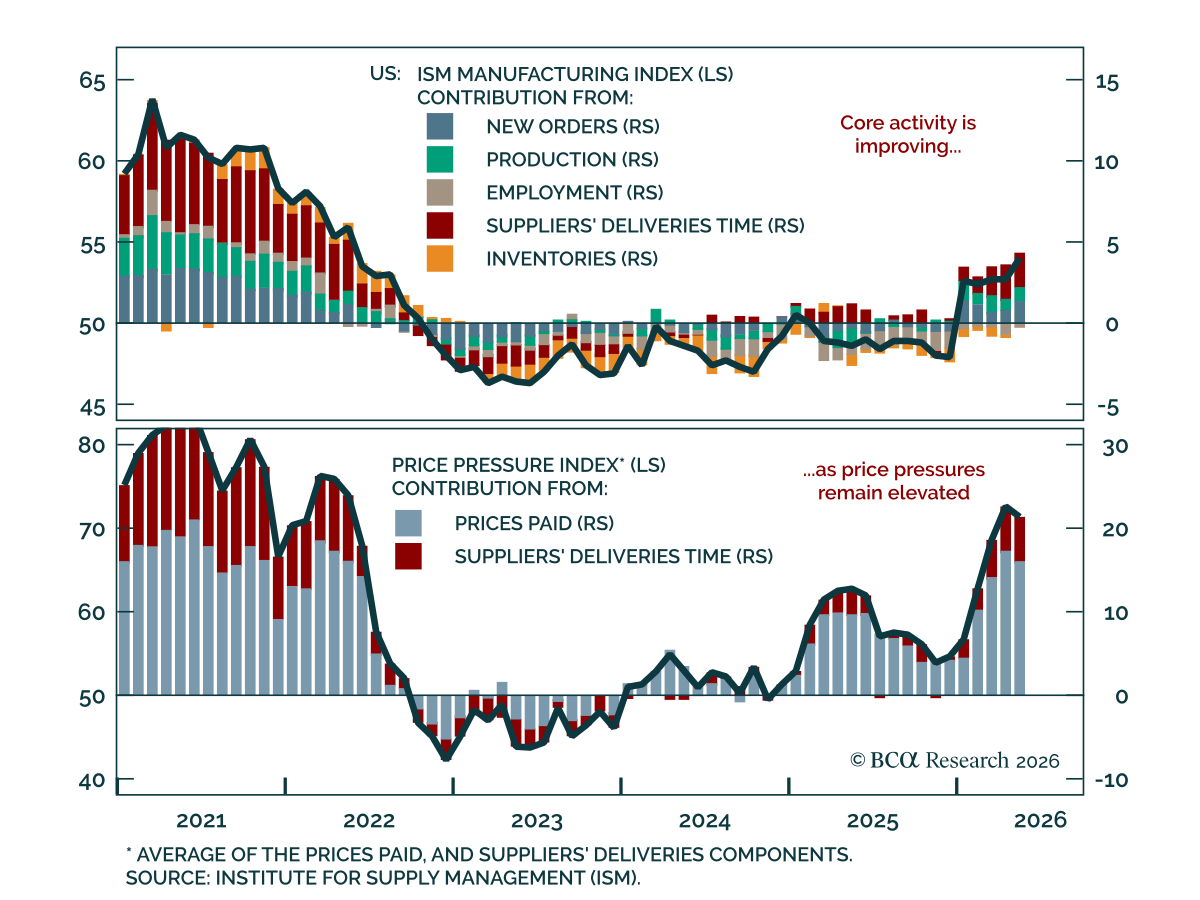

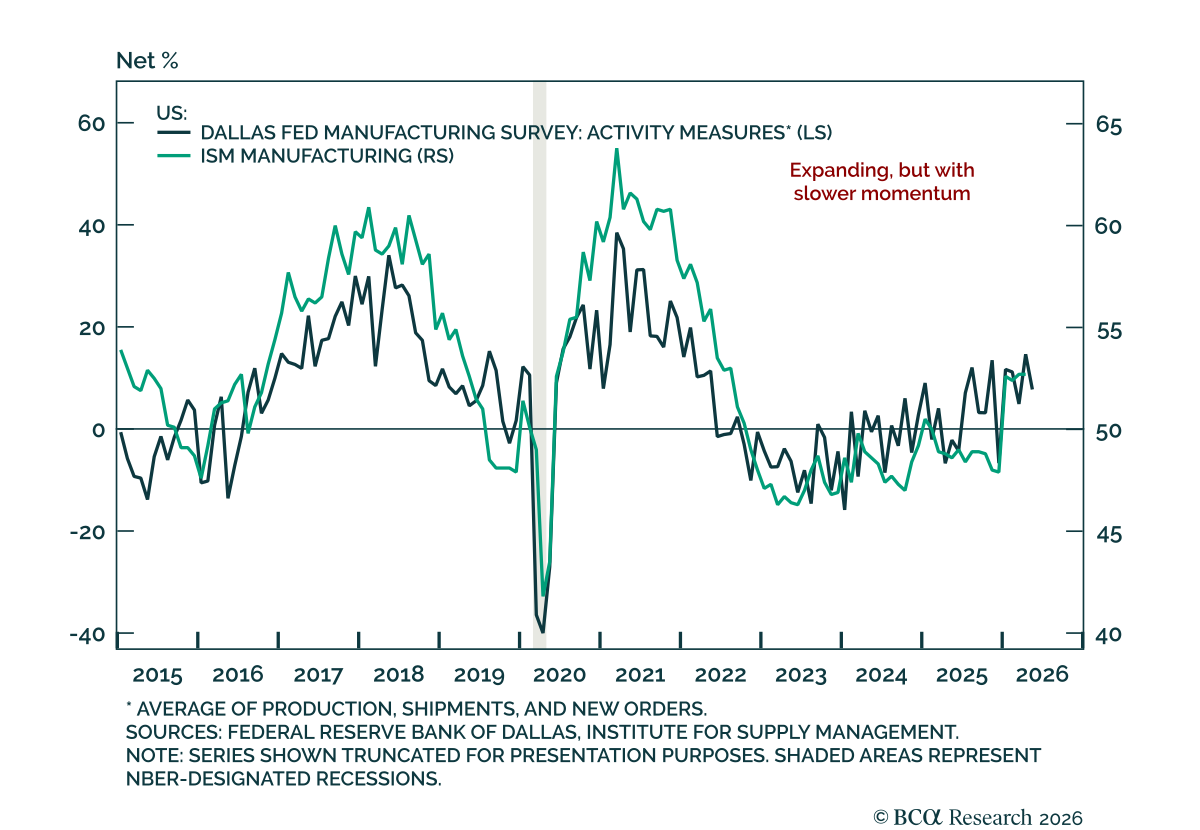

May’s US ISM Manufacturing report reinforces improving activity alongside persistent price pressure, highlighting continued inflationary impulse and hawkish risks to US monetary policy. The headline index came in at 54, above the market expectation of 53,…

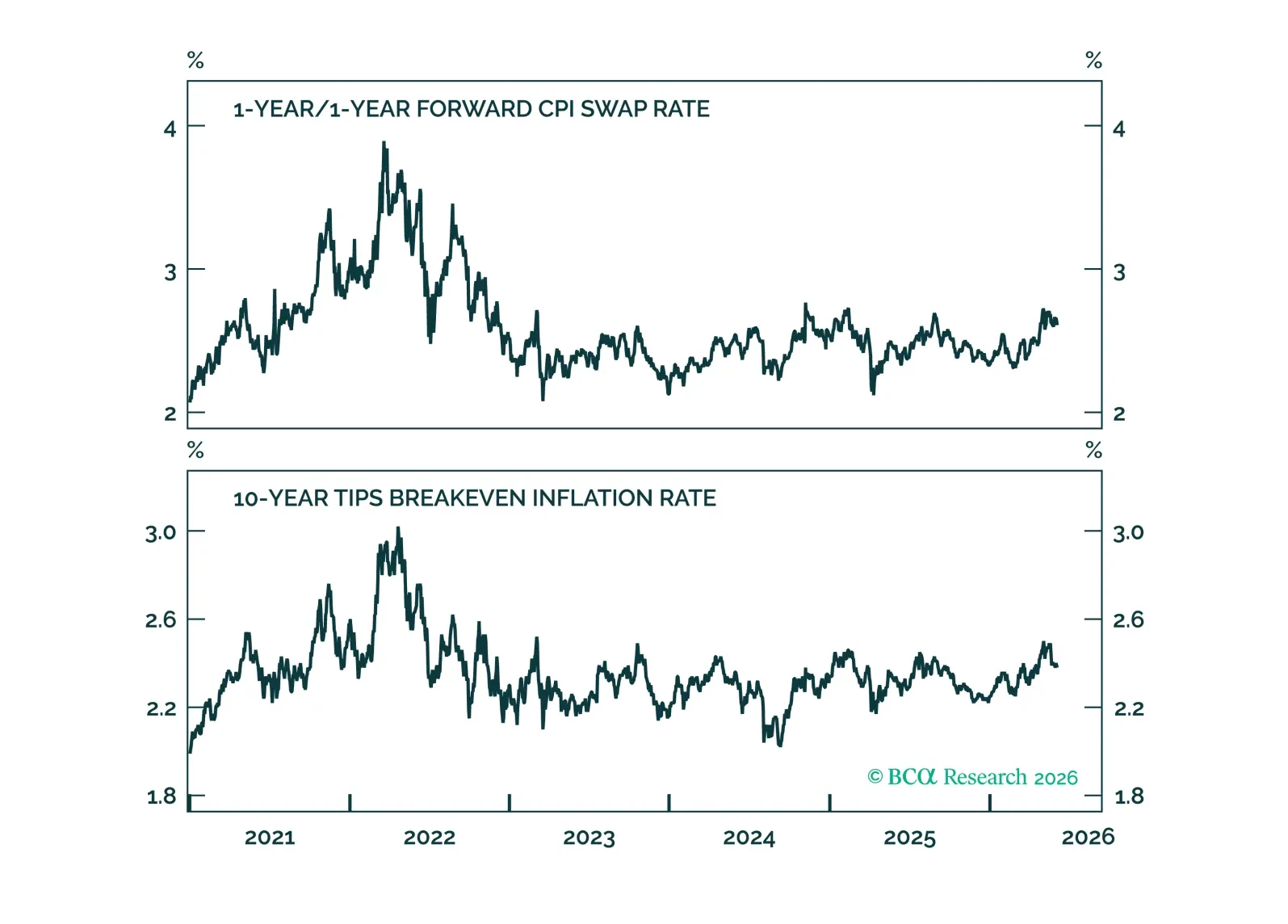

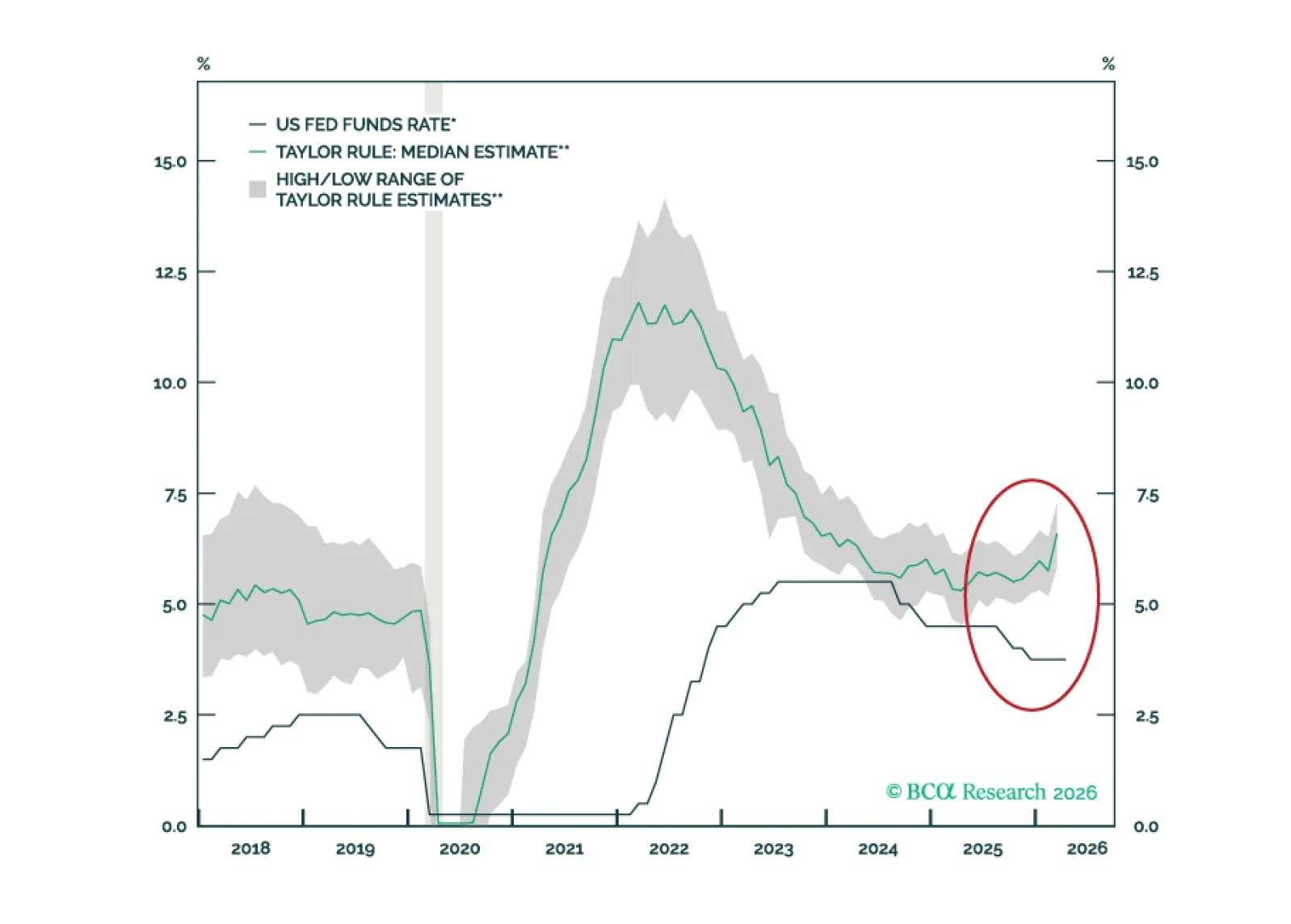

In Section II, Jonathan explores whether Kevin Warsh's appointment as Fed Chair signals a return to Greenspan-era, rules-based monetary policy.

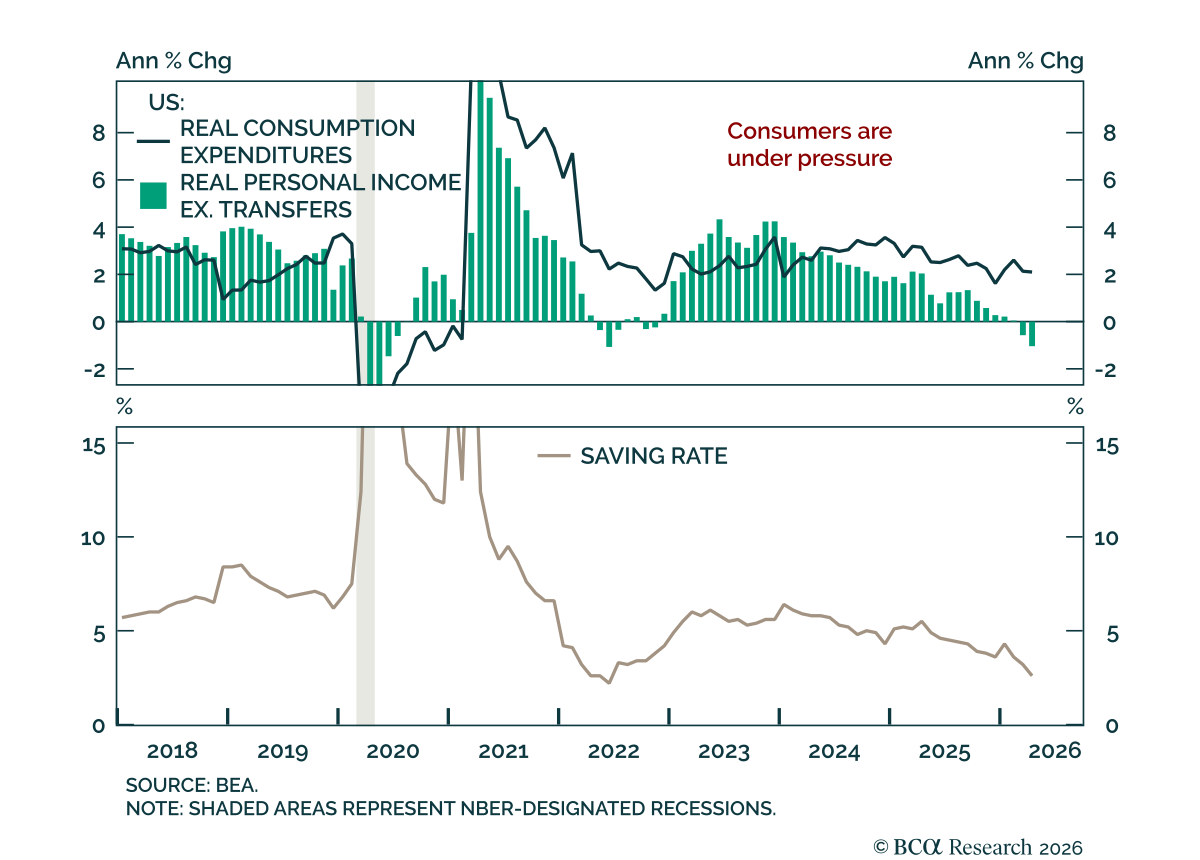

US demand is cooling as income growth falls behind spending. Q1 real GDP was revised down by 0.4 percentage points to 1.6%, mainly on weaker consumer spending and inventory investment. The April Personal Income & Outlays report confirms the softer…

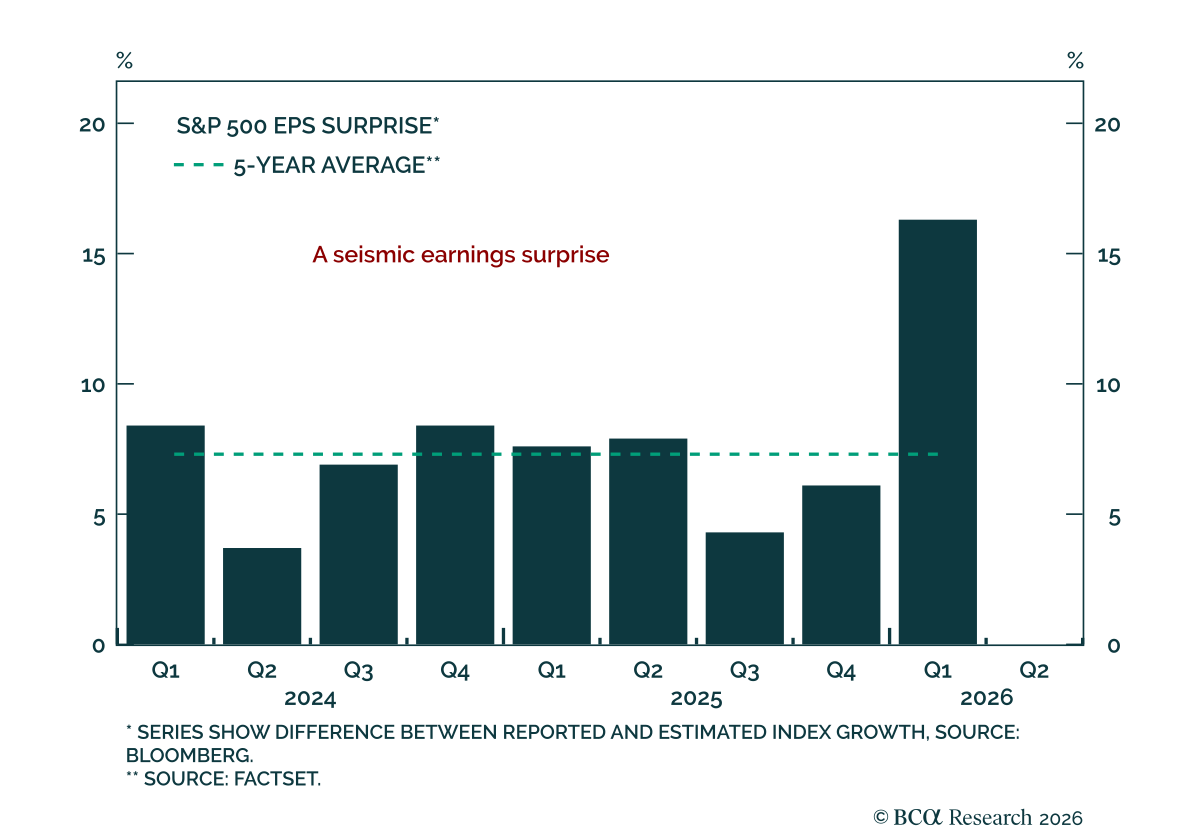

Our US Investment strategists remain constructive on the US economy as there is no evidence of overheating or looming stagflation. The S&P 500 has risen for eight straight weeks, supported by strong earnings. With 94% of constituents reporting, this…

The Dallas Fed survey points to Texas manufacturing continuing to expand in May, but with slowing momentum. The production index fell 10 points to 9.4, signaling an average pace of output growth rather than a broad acceleration. The softer tone showed up…

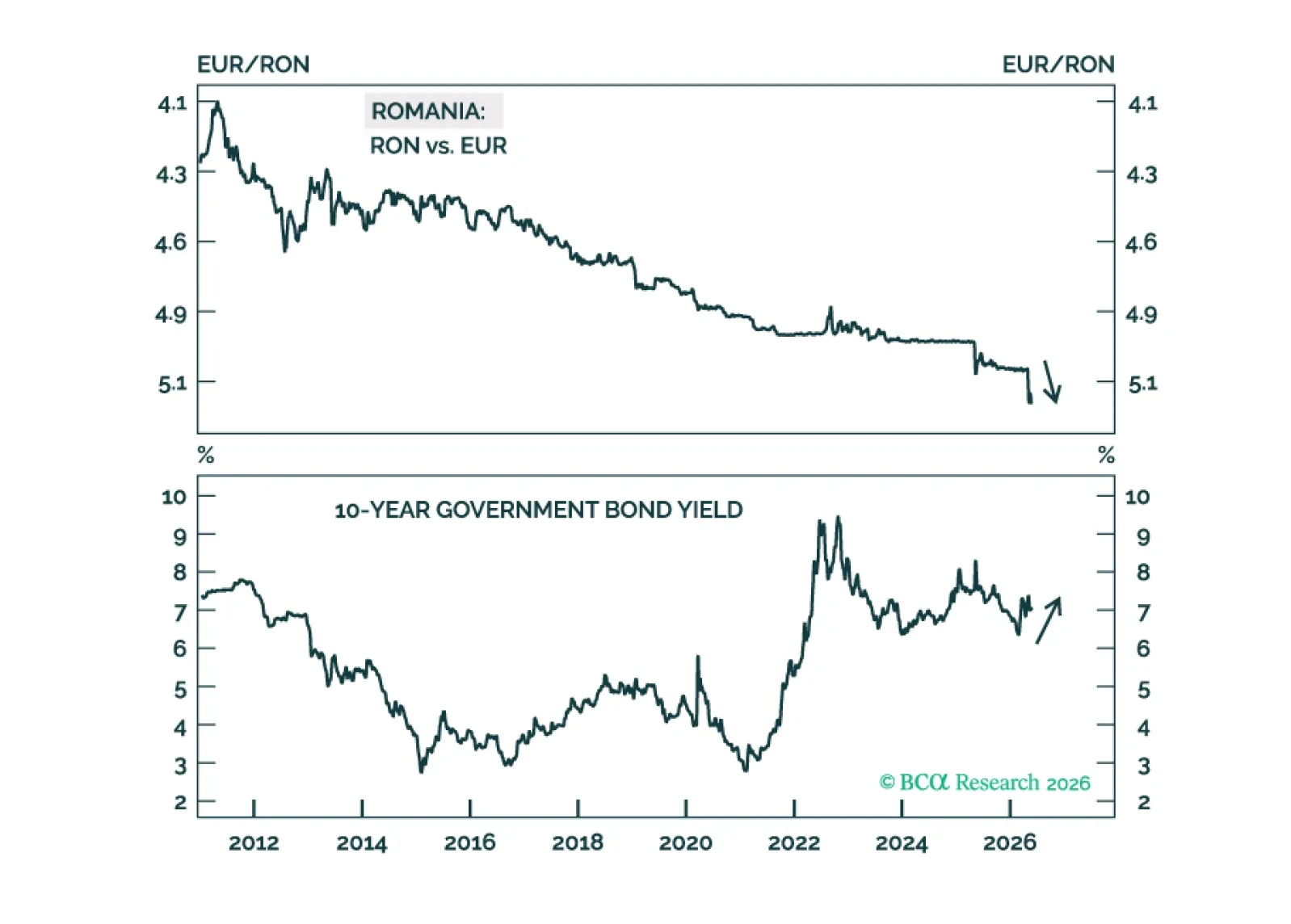

In Romania, large fiscal and current account deficits, high inflation, negative real rates, an overvalued exchange rate, and deteriorating growth point to budding currency devaluation. Investors should short the Romanian currency versus the euro and underweight Romanian local bonds, equities, and sovereign credit.

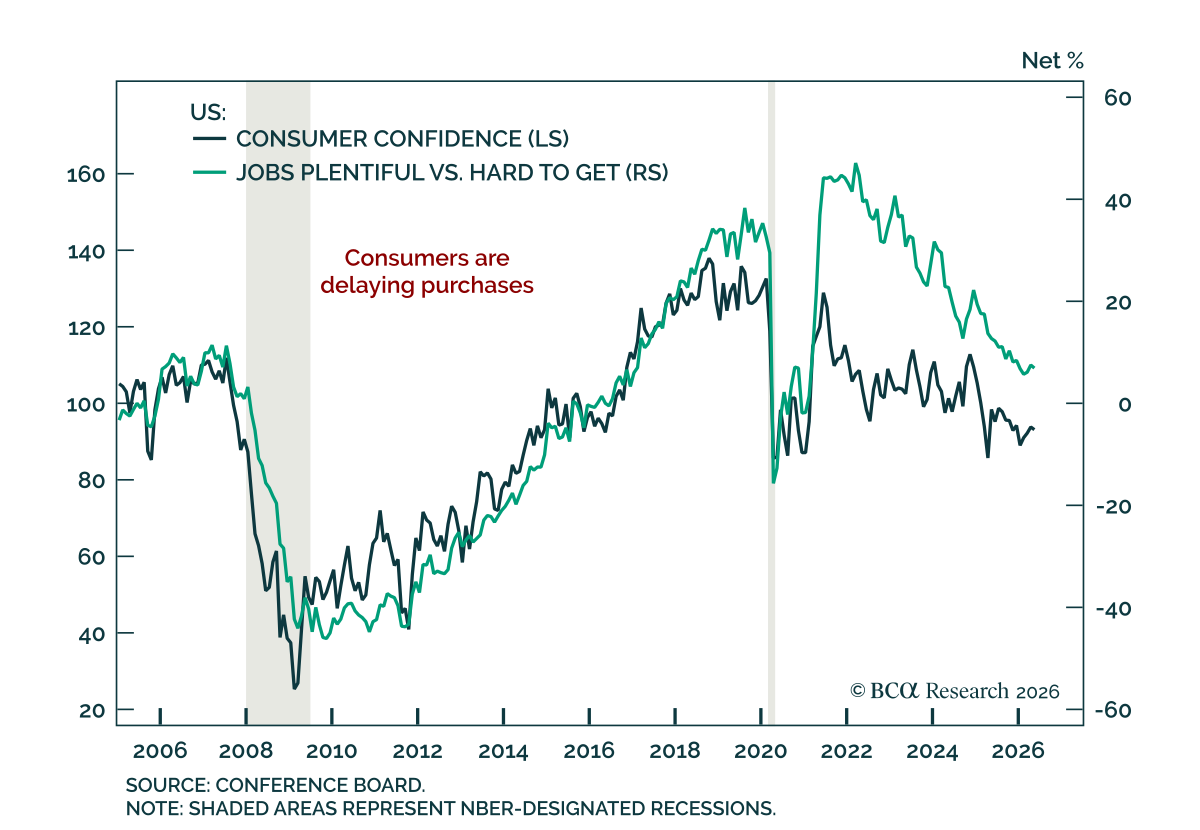

US consumer confidence softened marginally in May as high oil prices kept inflation pressure in focus. The Conference Board Consumer Confidence Index slipped to 93.1 from an upwardly revised 93.8 in April, but still came in slightly above…

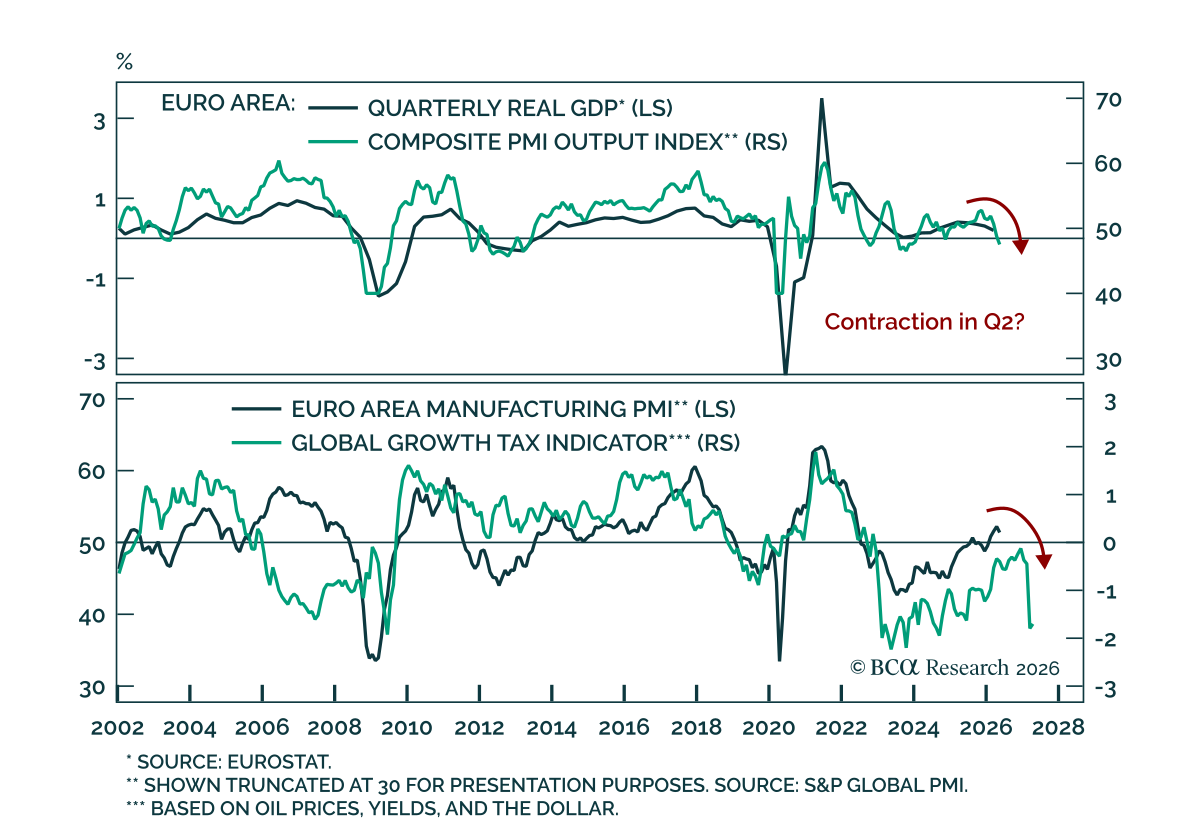

Our European strategists argue Europe is shifting from stagflation toward recession. Growth is weakening rapidly, labor markets are softening, and limited fiscal space leaves the economy exposed to renewed inflationary pressures, especially…