Economy

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

Downward pressure on the pound will rise in the coming months. Inflation will go up, so will bond yields. It’s time to book profits on Egyptian domestic bonds.

This report analyzes China’s persistent deflation, which is rooted in supply-side forces. Consumption support will be slow and incremental, keeping deflationary pressures elevated for the next 6–12 months.

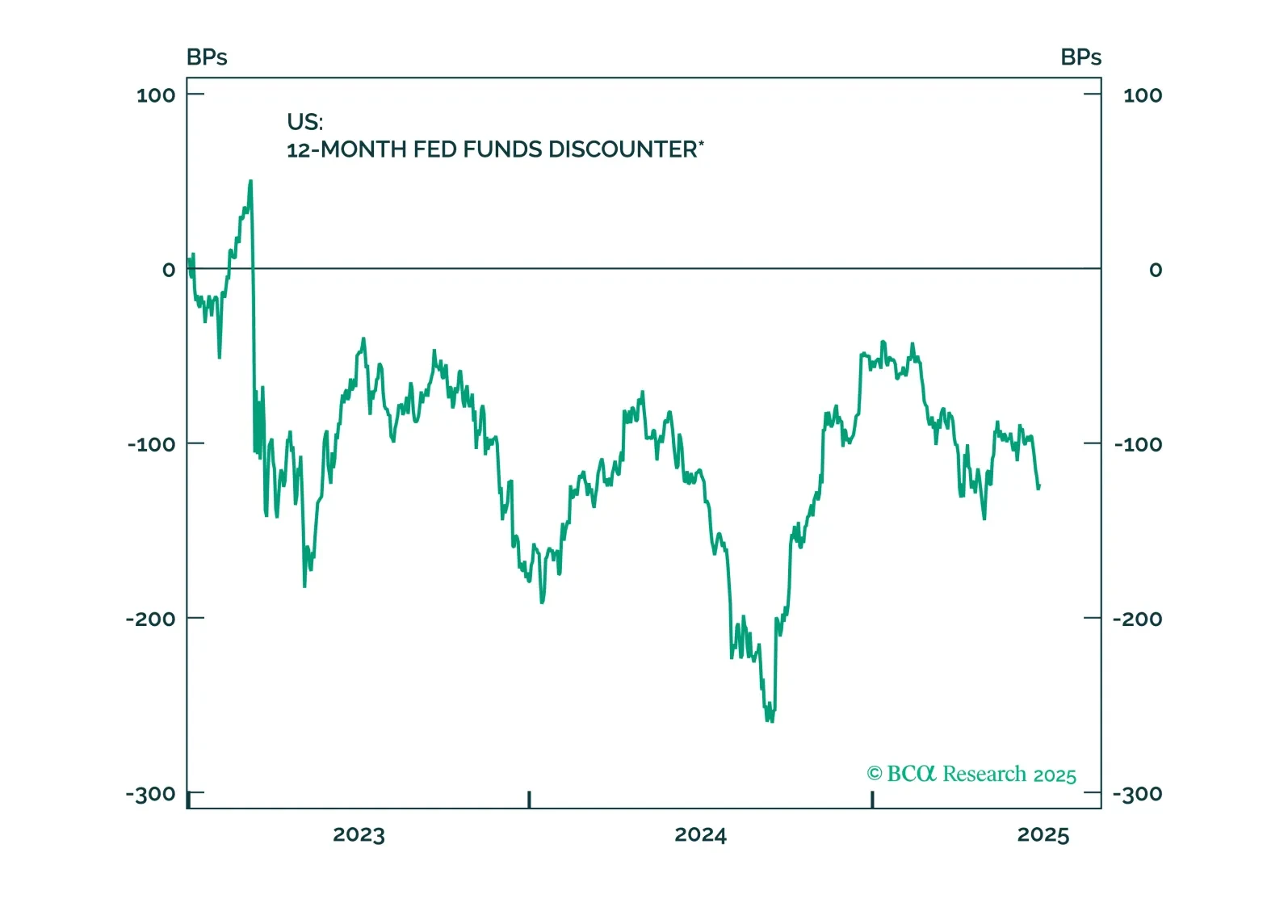

Monetary policy is about to become a powerful tailwind to the already bullish brew that includes Trump’s repeated step-downs from a global trade war, irrelevant geopolitical risks in the Middle East, and a fiscal policy that is no longer as alarming to the bond markets as the raft of campaign promises appears to be. Investors should hesitate to get overly bearish either bonds or stocks. However, we remain uber USD bears.

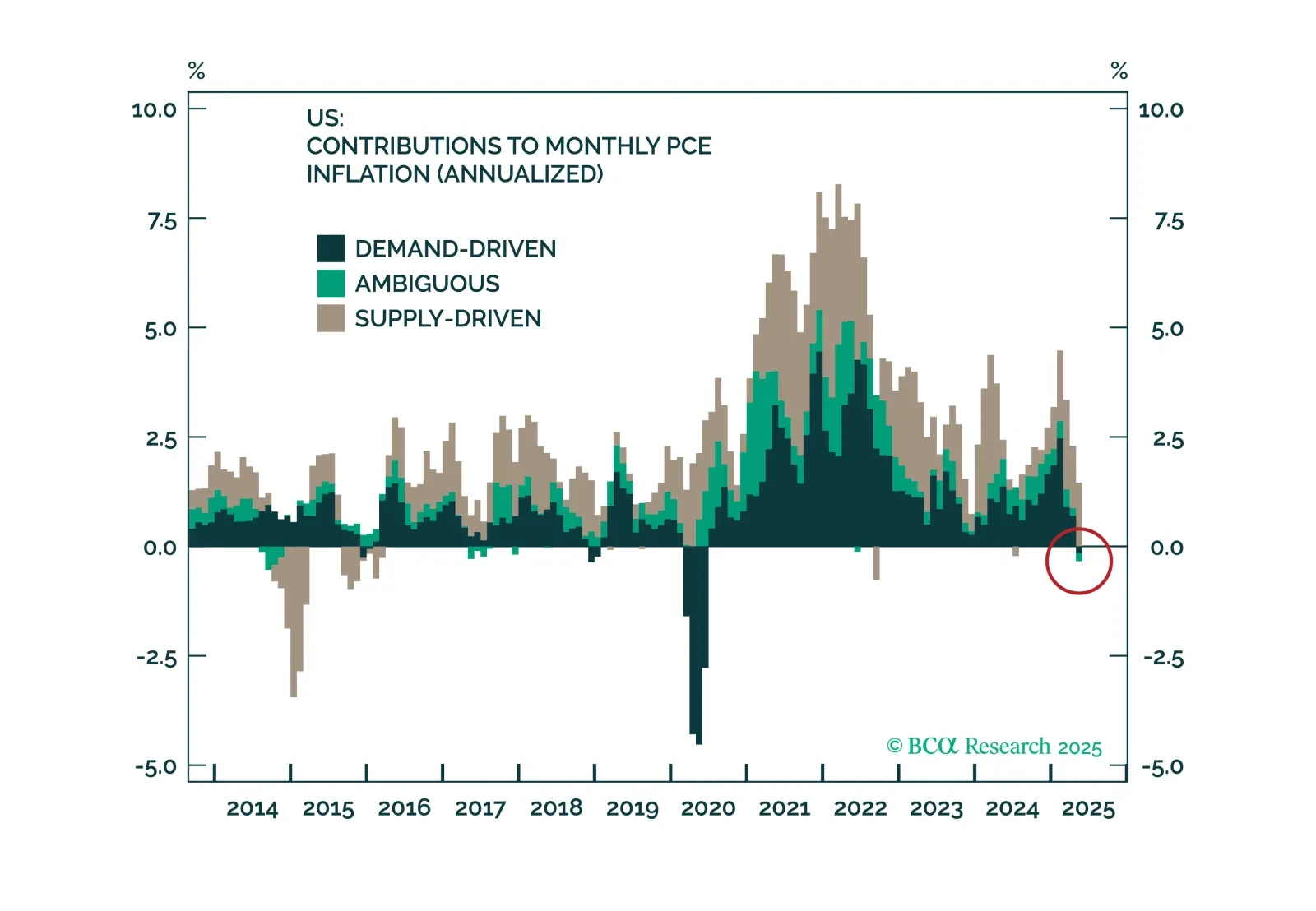

The US economy is not in recession, but is suffering from a post-pandemic stimulus hangover. The cure: lower interest rates. We expect the Fed to start lowering rates, which will benefit both equities and bonds. We upgrade stocks to neutral and downgrade cash to underweight. We also upgrade duration to overweight. The US dollar will continue to weaken, so favour Europe and China within equities.