Economy

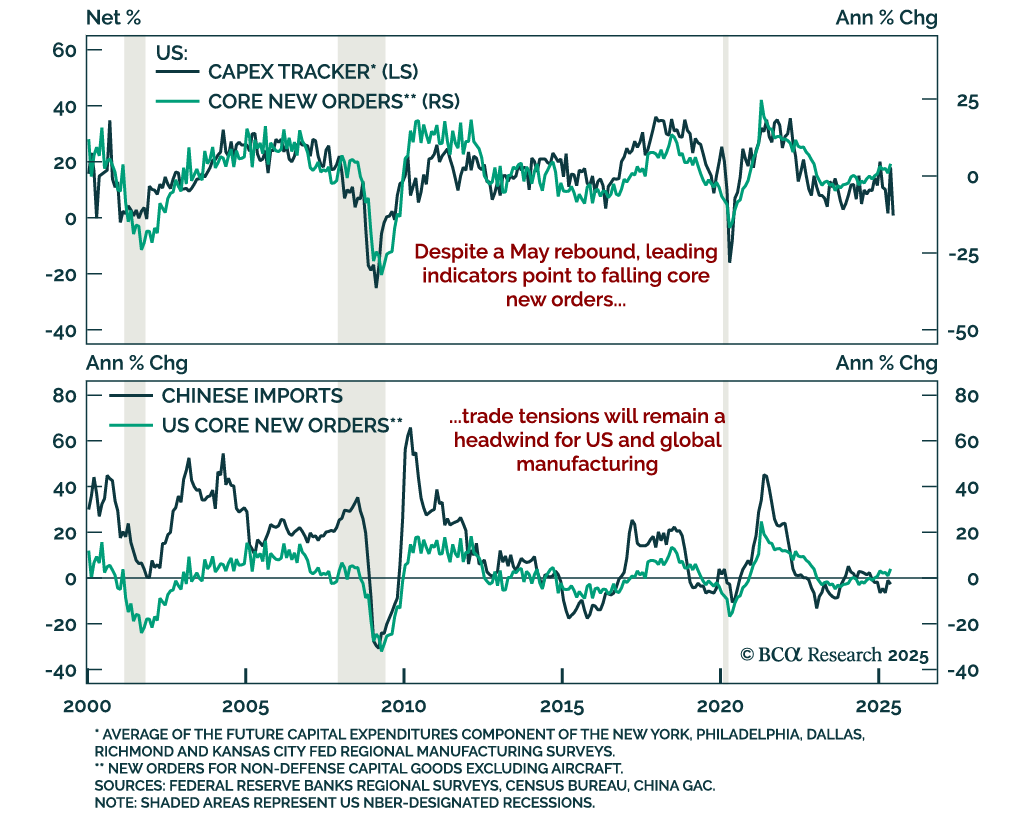

Headline strength in US capital goods orders is unlikely to last, reinforcing our defensive stance and preference for steepeners. New orders for core capital goods (nondefense ex-aircraft) rose 1.7% m/m in May, beating expectations after a 1.5% drop in April.…

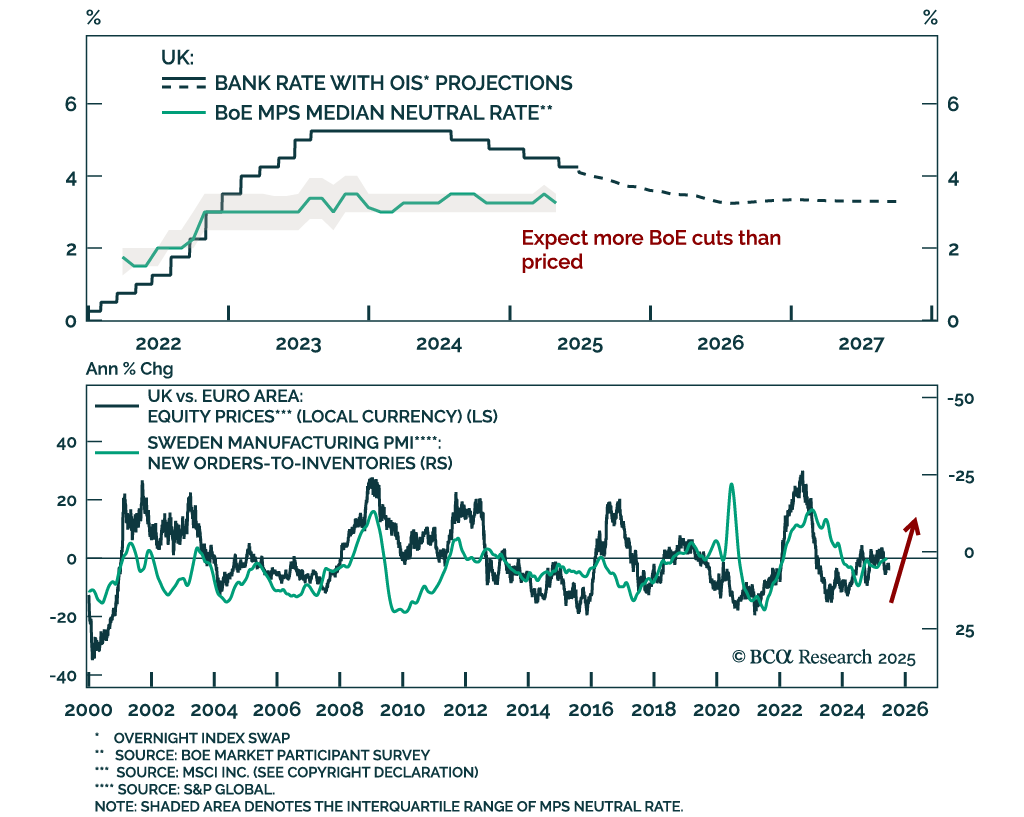

Our Global Fixed Income, FX, and European strategists expect aggressive BoE easing amid disinflation and labor market weakness, supporting an overweight in Gilts and UK equities versus the euro area. While UK productivity remains sluggish, a recovery in labor…

Deflationary pressures and weak core Europe growth support CE3 bond longs as rate cuts loom. The Czech and Hungarian central banks held rates steady at 3.5% and 6.5% this week, following Poland’s earlier decision to keep rates unchanged at 5.25%. While citing…

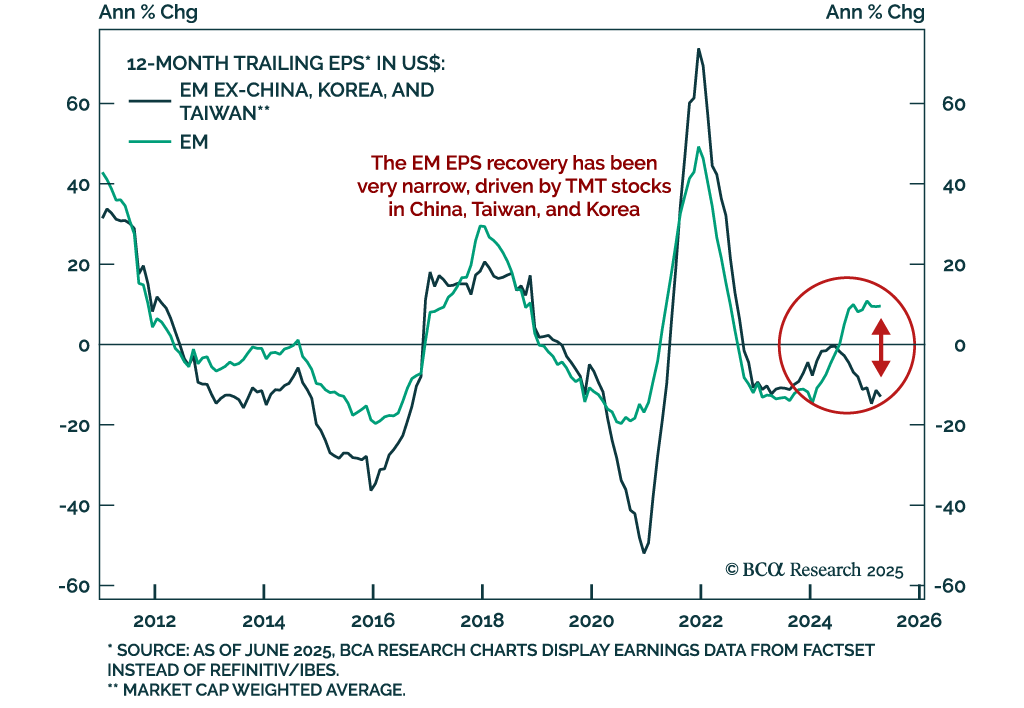

BCA’s EM strategists remain downbeat on EM equities despite a bearish US dollar view, citing profit headwinds and limited valuation support. The ongoing EM earnings recovery has been narrowly concentrated in TMT sectors across China, Taiwan, and Korea,…

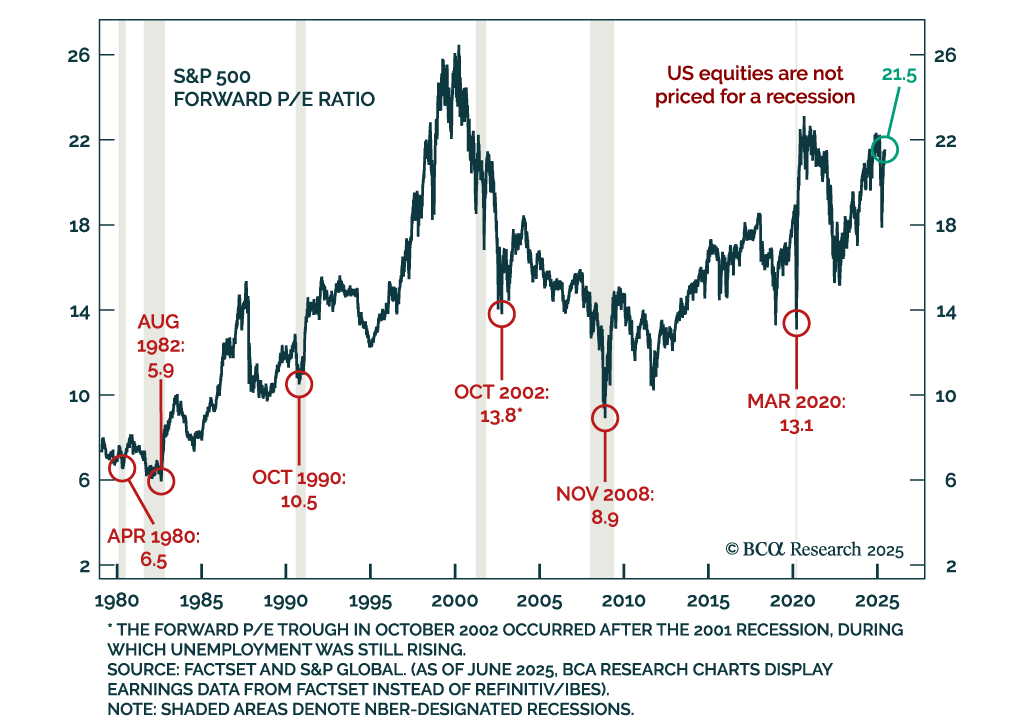

Geopolitical risks and fragile margins reinforce a defensive allocation stance, as oil shocks and high US equity valuations pose growing downside risks. At this month’s Views Meeting, our strategists discussed the potential fallout from an Iran-Israel…

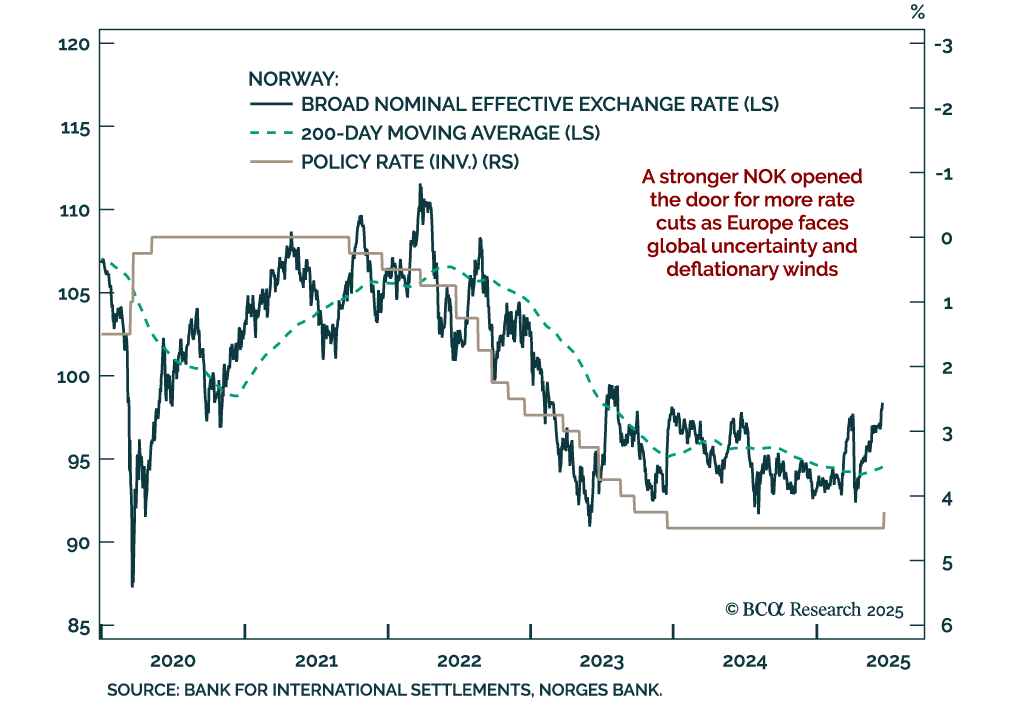

A stronger Norwegian krone has opened the door to more rate cuts, making Norwegian government bonds more attractive. Our Chart Of The Week comes from Jeremie Peloso, European Strategist. With its surprise 25 basis point cut, the Norges Bank made its first…

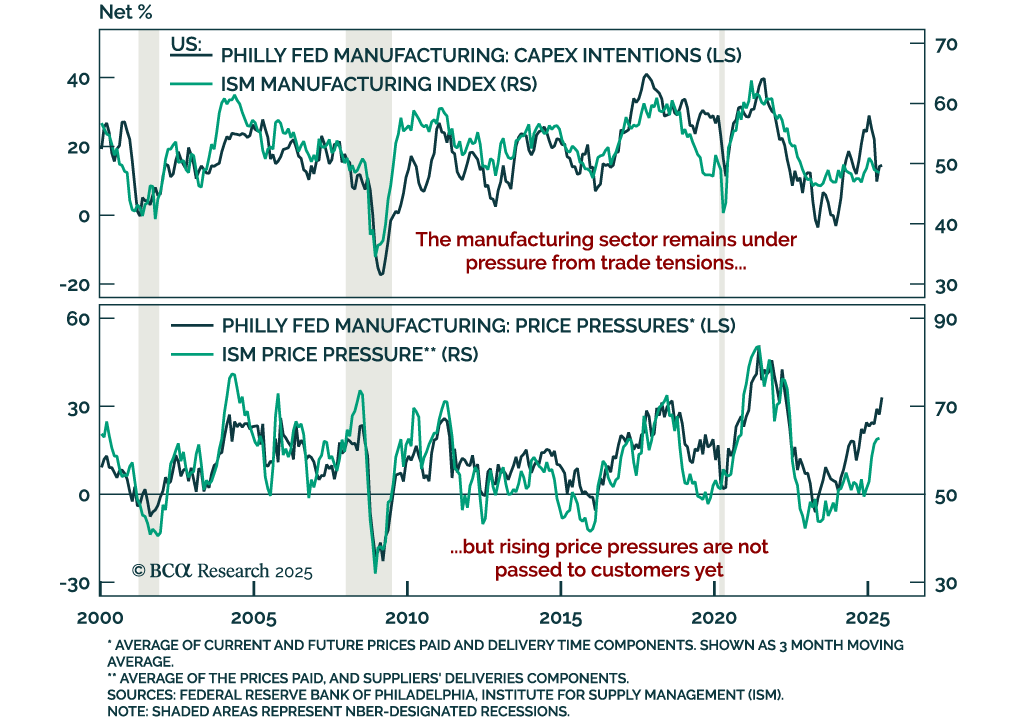

Worsening manufacturing momentum supports a long duration stance as recession risks remain elevated. The June Philly Fed survey came in below expectations, unchanged at -4.0. While shipments increased, new orders decelerated and employment measures fell.…

In this Insight, we highlight our strong conviction trades based on the central bank meetings held by the Bank of England, the Norges Bank, the Swiss National Bank and the Riksbank.

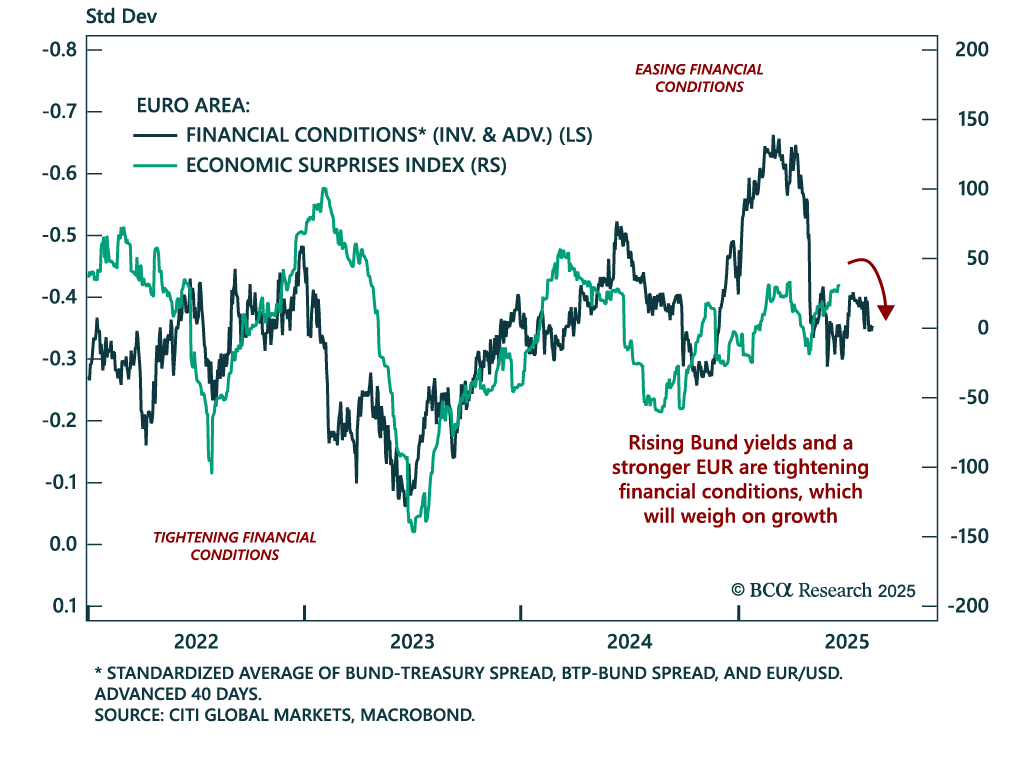

Tightening financial conditions, deflationary headwinds, and rising geopolitical risks argue for short-term caution on European assets. European equities have outperformed in 2025, with the EURO STOXX 50 beating the S&P 500 and EUR/USD moving higher. This…

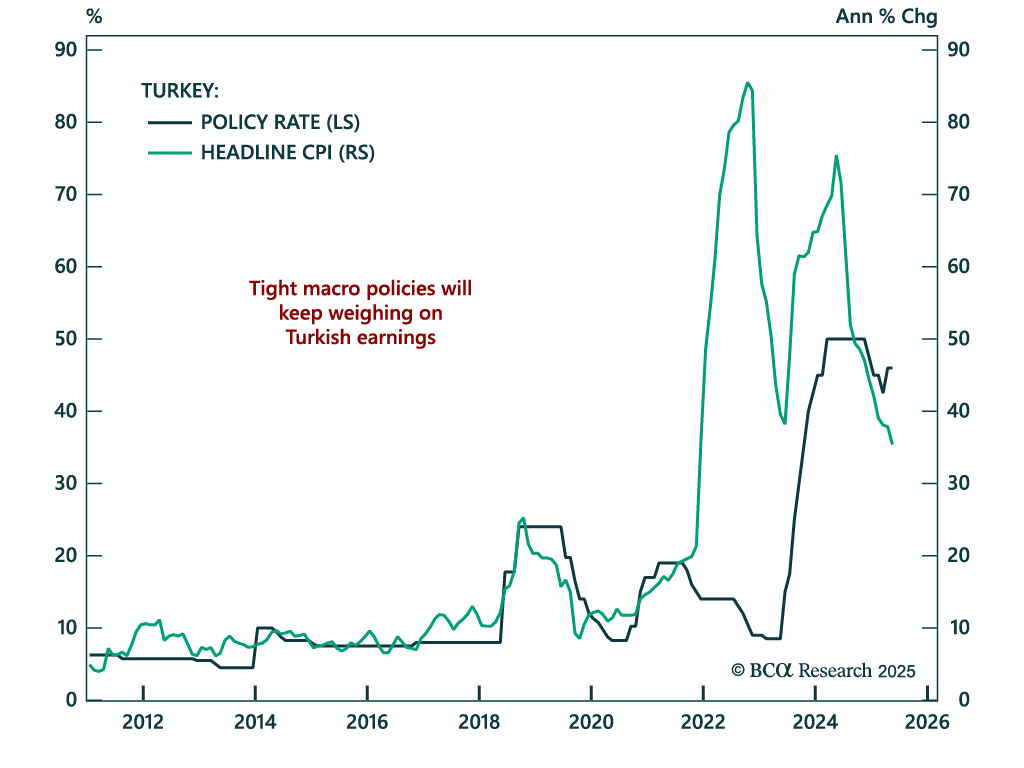

Turkey’s tight policy stance will weigh on growth and earnings, reinforcing our bearish view on Turkish equities. The central bank held rates at 46% and maintained a hawkish bias, consistent with efforts to bring inflation down from 35% to single digits.…