Economy

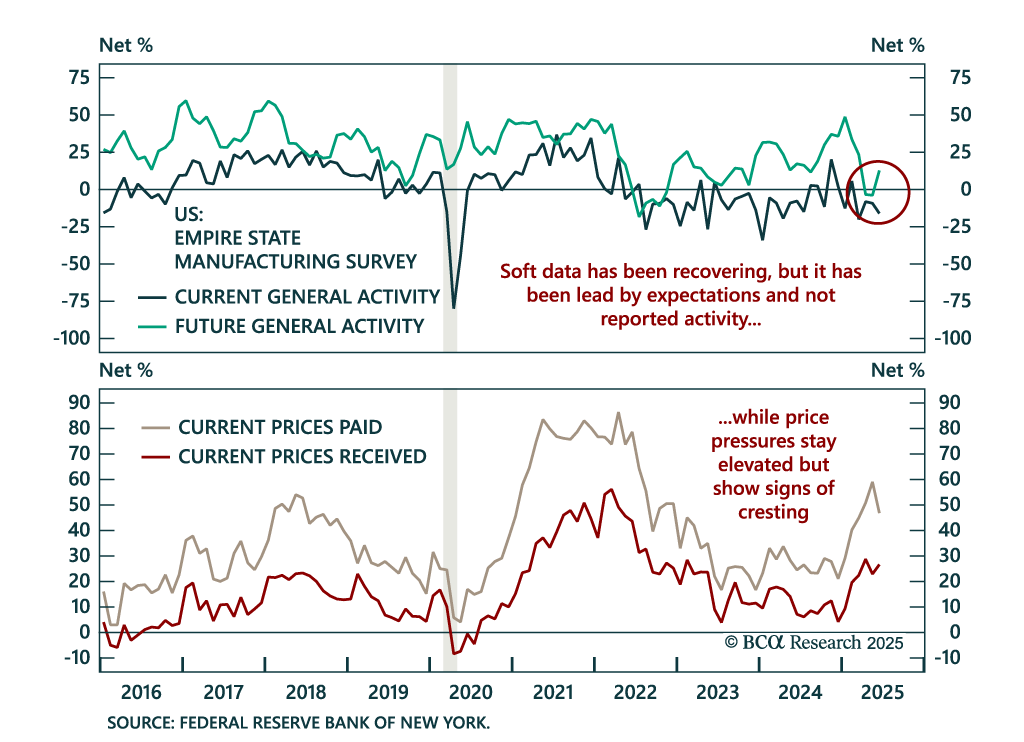

Worsening manufacturing data reinforces our defensive stance as expectations rebound but observed activity continues to deteriorate. The June Empire State Manufacturing Survey fell to -16.0 from -9.2, well below estimates. Expectations rebounded, but the…

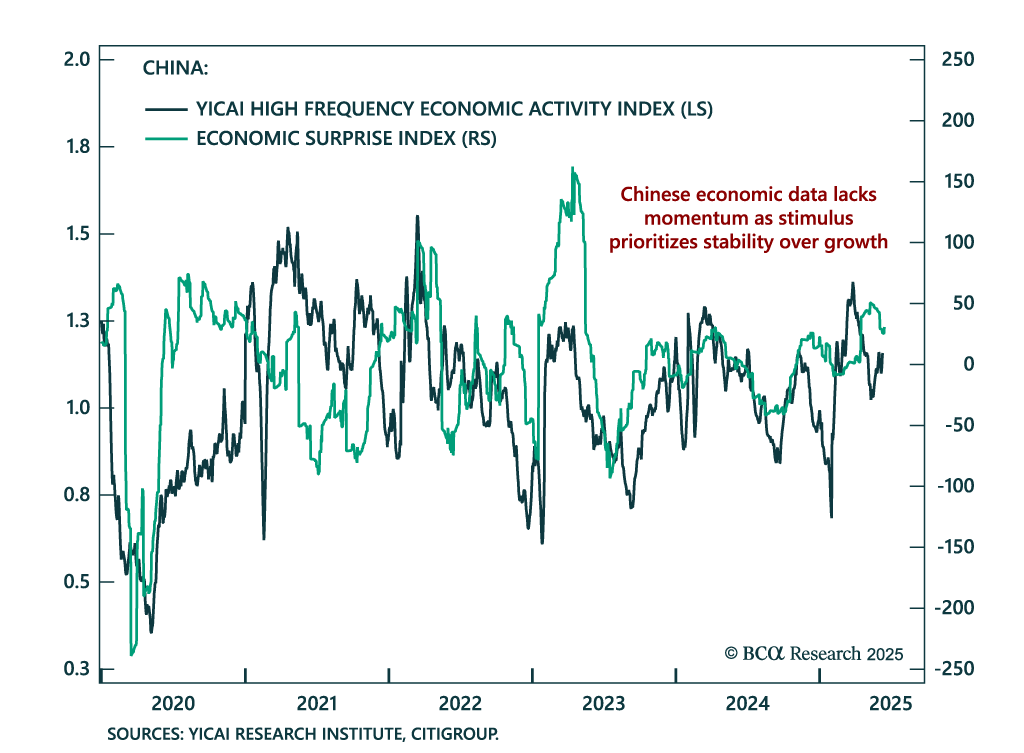

Household data beat in May, but China’s macro story remains fragile, reinforcing our overweight in local government bonds. Traditional supply-side activity decelerated, with industrial production and fixed asset investment both weaker, while retail sales and…

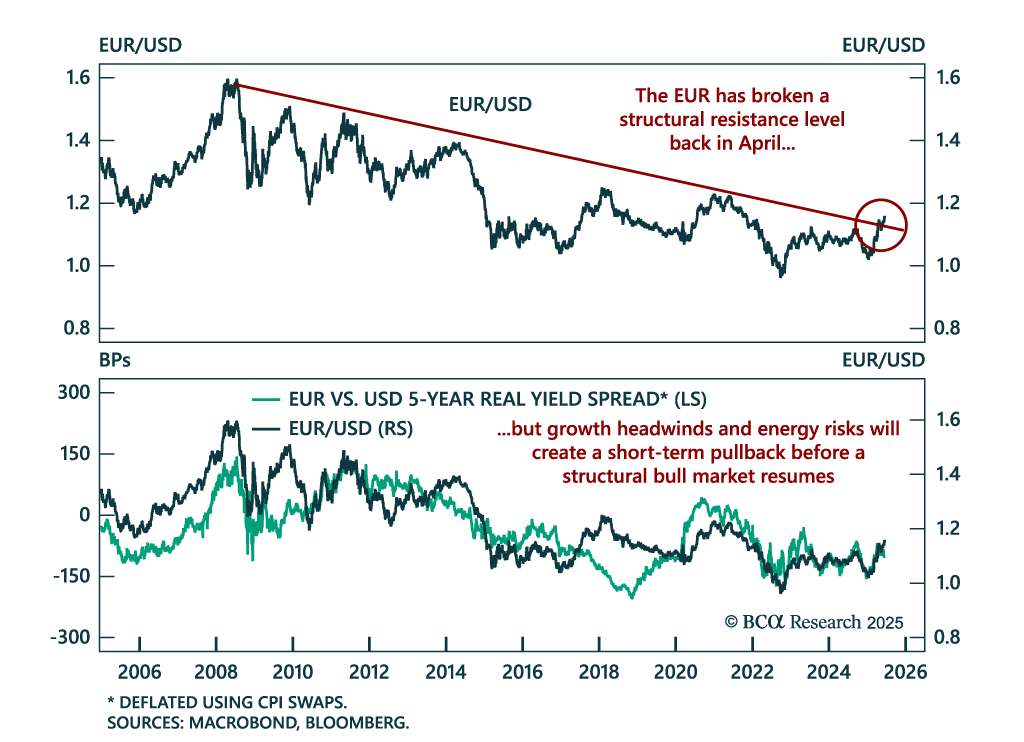

Short term euro upside is limited despite a structural bull case, as fragile growth, easing ECB policy, and geopolitical risks cap further gains. EUR/USD broke above structural resistance in April amid optimism over German stimulus and US political…

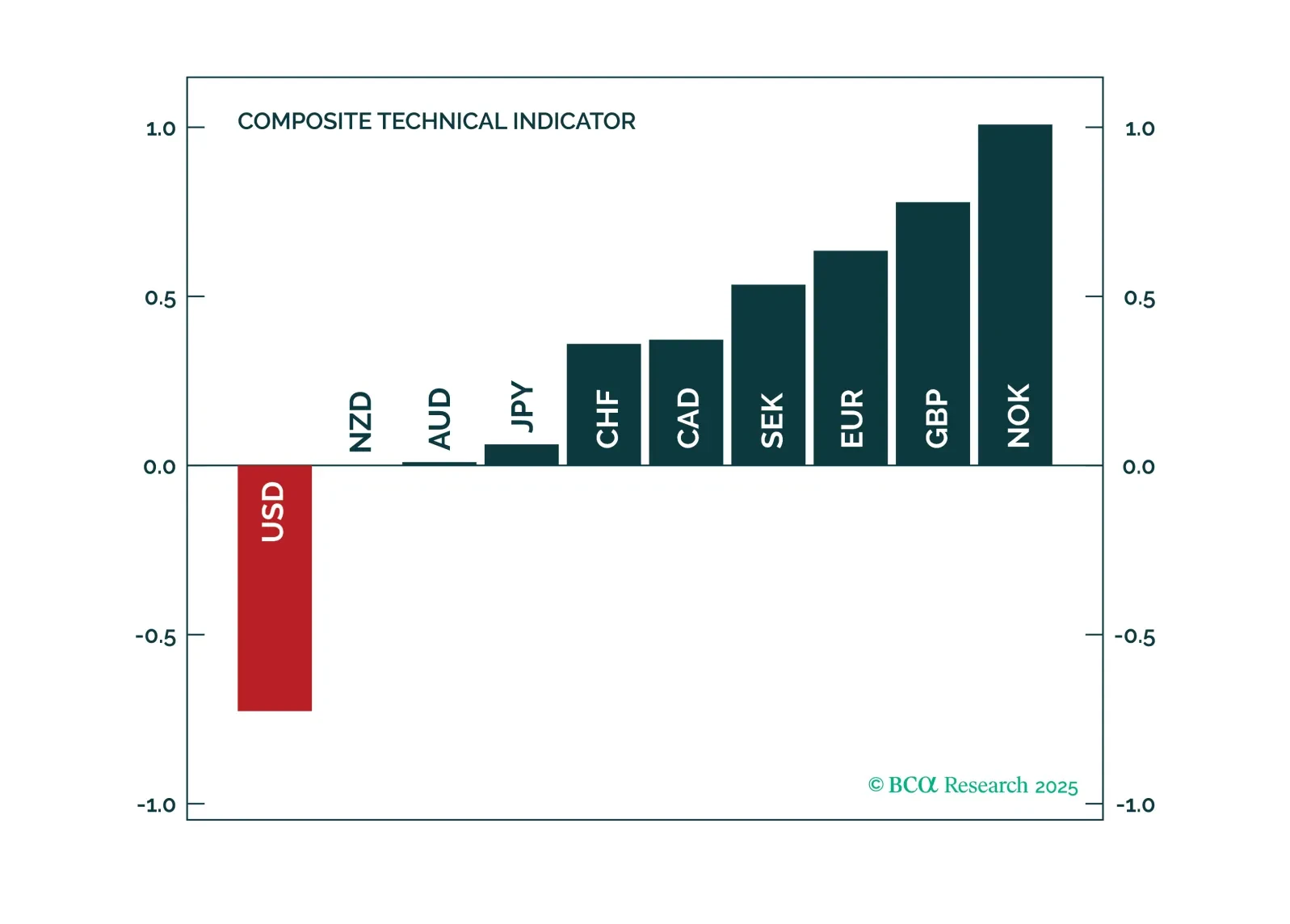

In this FX note, we provide a rationale for why it is important to pay attention to technical indicators, while still keeping your eyeball on the structural factors that drive currencies. This report answers the following questions: 1. Should you buy or sell the USD over a three-to-six month period from the pure lens of our proven technical indicators and 2. What are the best tactical cross trades among currencies.

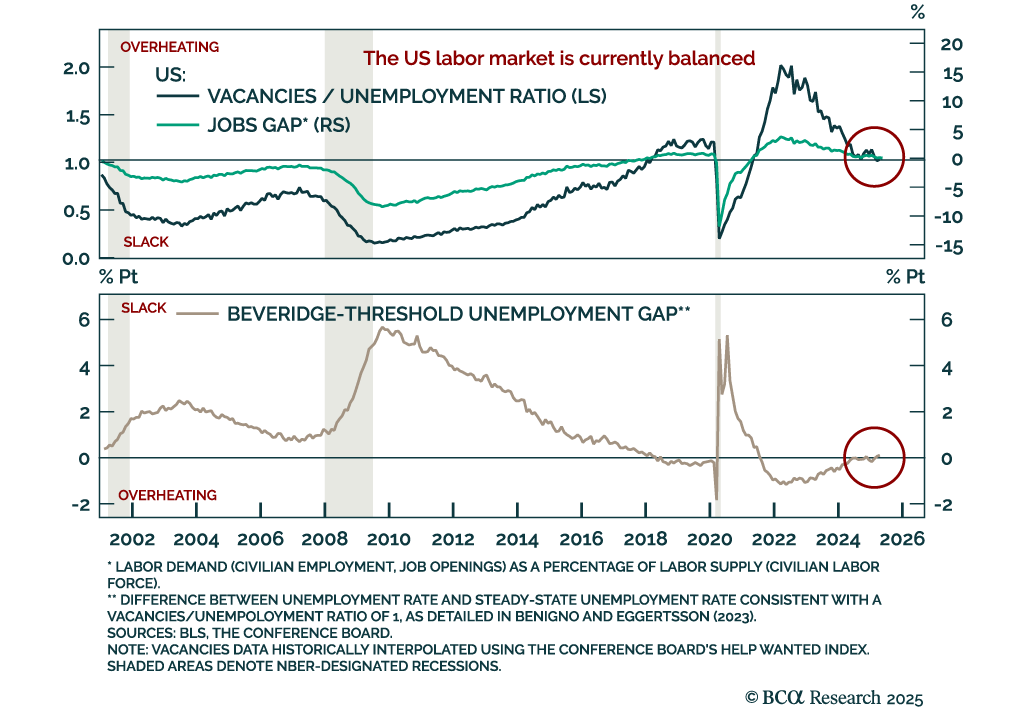

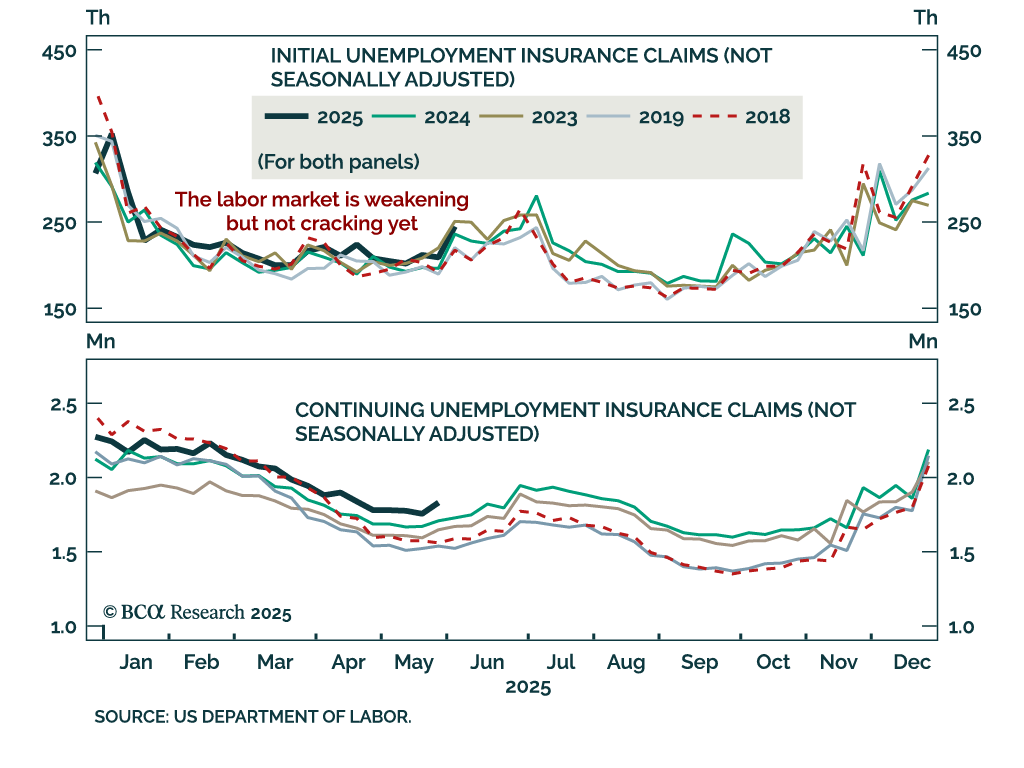

The US labor market appears balanced but at a pivotal point, with further weakness likely to prompt a shift to maximum defensiveness. After running the hottest since the 1960s, the labor market has gradually cooled. That rebalancing sparked a brief growth…

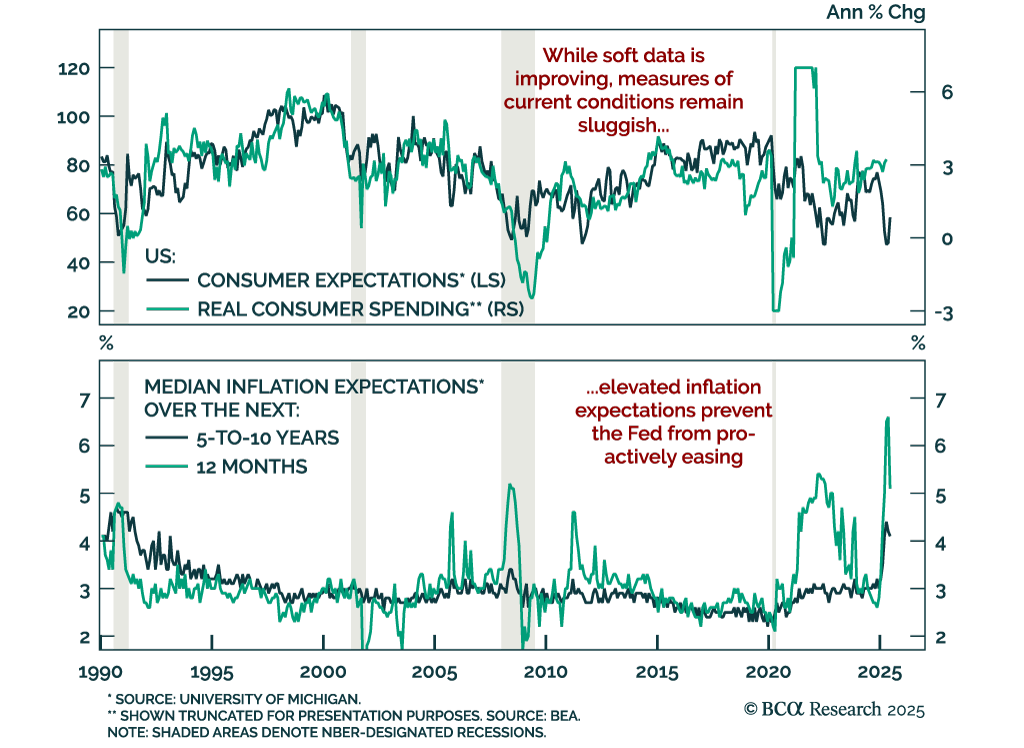

While consumer sentiment is rebounding, sticky inflation expectations and slowing growth warrant staying long duration and steepeners. The preliminary June University of Michigan Consumer Sentiment Index surprised to the upside, rising to 60.5 from 52.2.…

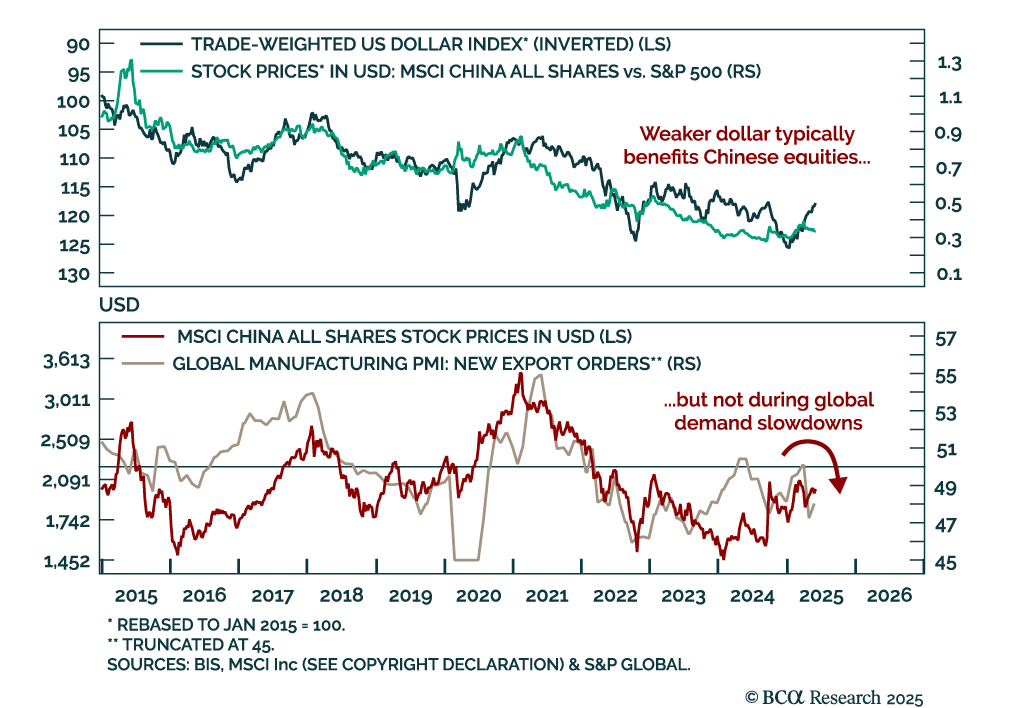

BCA’s China Investment strategists see limited upside for Chinese equities and favor bonds, as trade tensions ease but domestic headwinds persist. This week’s US-China trade talks in London lowered the risk of near-term escalation or new retaliatory tariffs,…

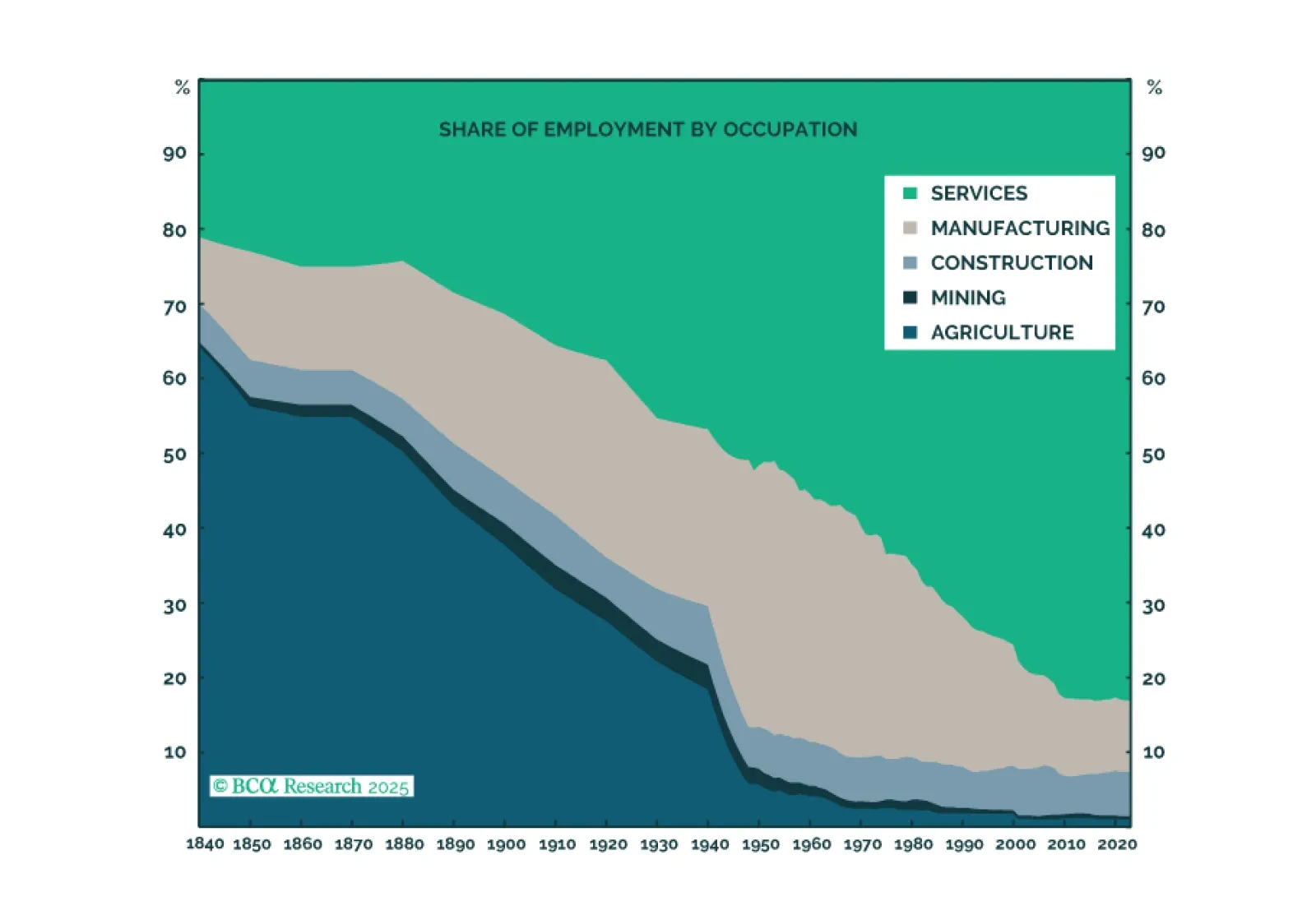

Provided that humanity can overcome the existential risks posed by AI, real incomes will rise. Although most workers will ultimately gain from the transition to an AI-dominated economy, the biggest winners will be those who control the land and the natural resources beneath it.

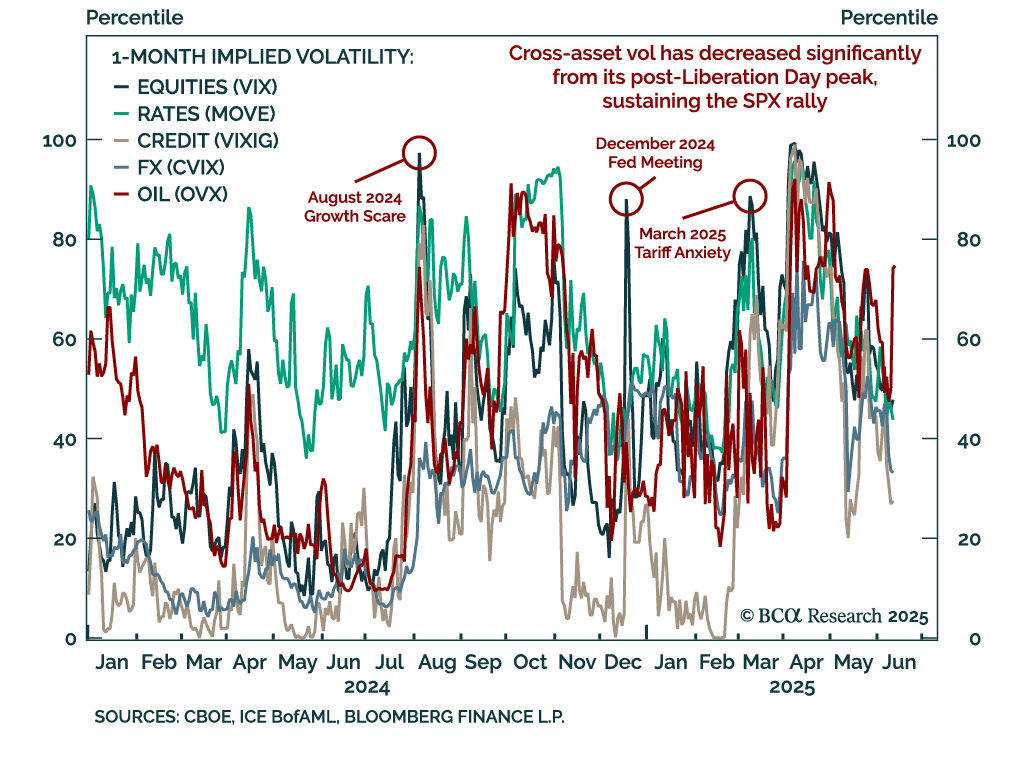

The S&P 500 has breached 6000 and may retest all-time highs, but we would not recommend chasing the rally. Risk assets have shrugged off recession fears, with stress indicators like the VIX, SKEW, and VVIX still subdued, signaling limited demand for…

Further labor market deterioration would trigger a shift to maximum underweight in equities. While soft indicators have markedly deteriorated, hard labor data remains relatively resilient, though it has clearly weakened. The labor market is still in…