Economy

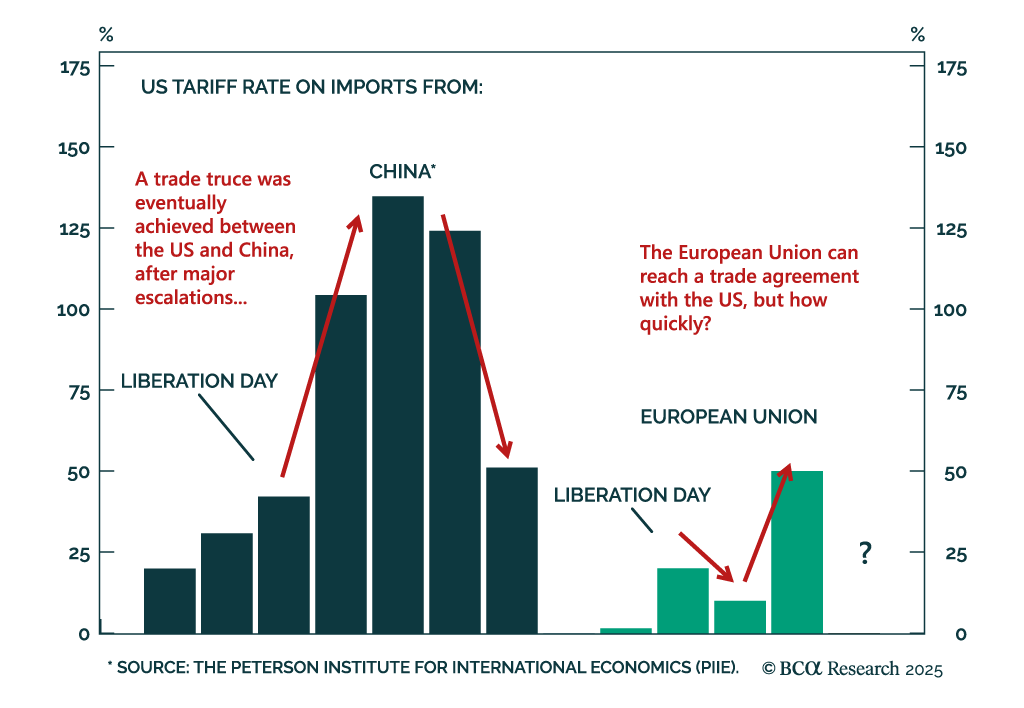

Last Friday, President Trump announced new 50% tariffs on imported goods from the European Union (EU), effective June 1st, and threatened US company Apple with 25% tariffs unless it made iPhones in the US. Global stock markets reacted negatively to the news,…

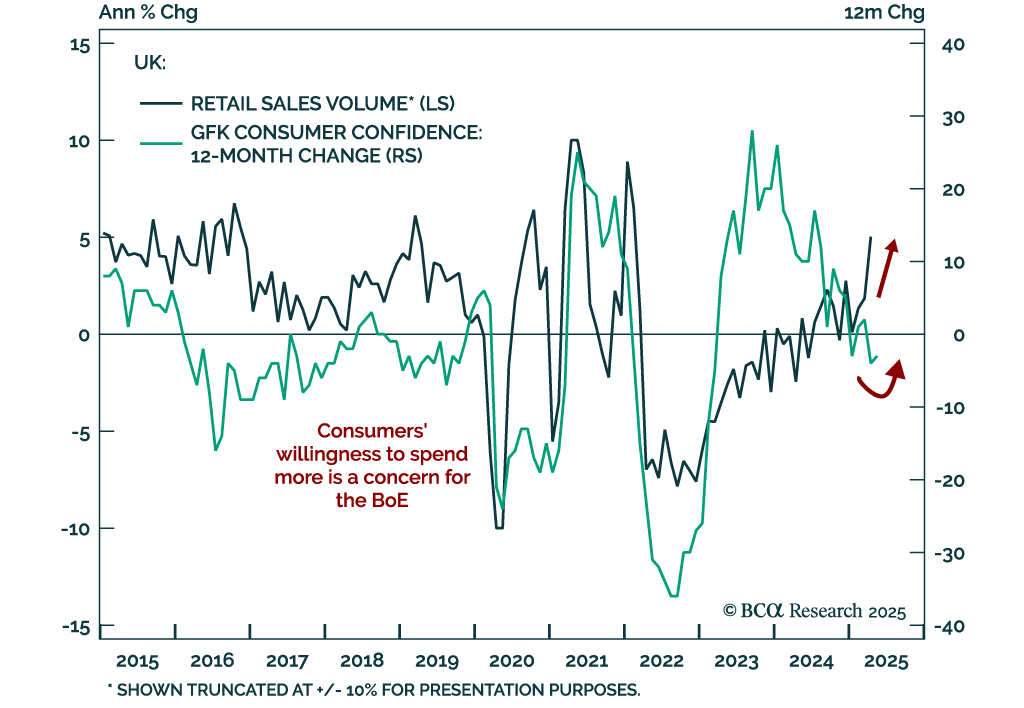

The rebound in UK retail sales and consumer confidence surprised to the upside, and suggests that the re-acceleration in inflation observed earlier this week may not be transitory. UK retail sales rose 1.2% m/m in April from 0.1% m/m, significantly…

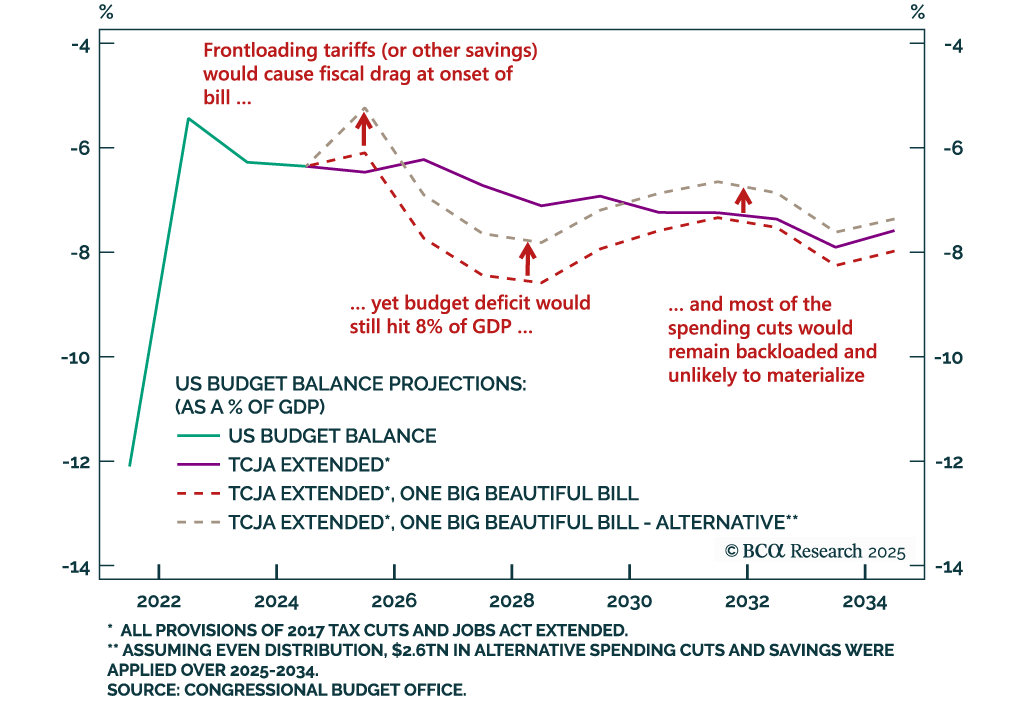

President Trump’s signature bill is surprising to the upside with budget deficits, as predicted by our Geopolitical Strategists. Some form of the bill is guaranteed to pass, no matter how many tries it takes. The bill will cut taxes more than…

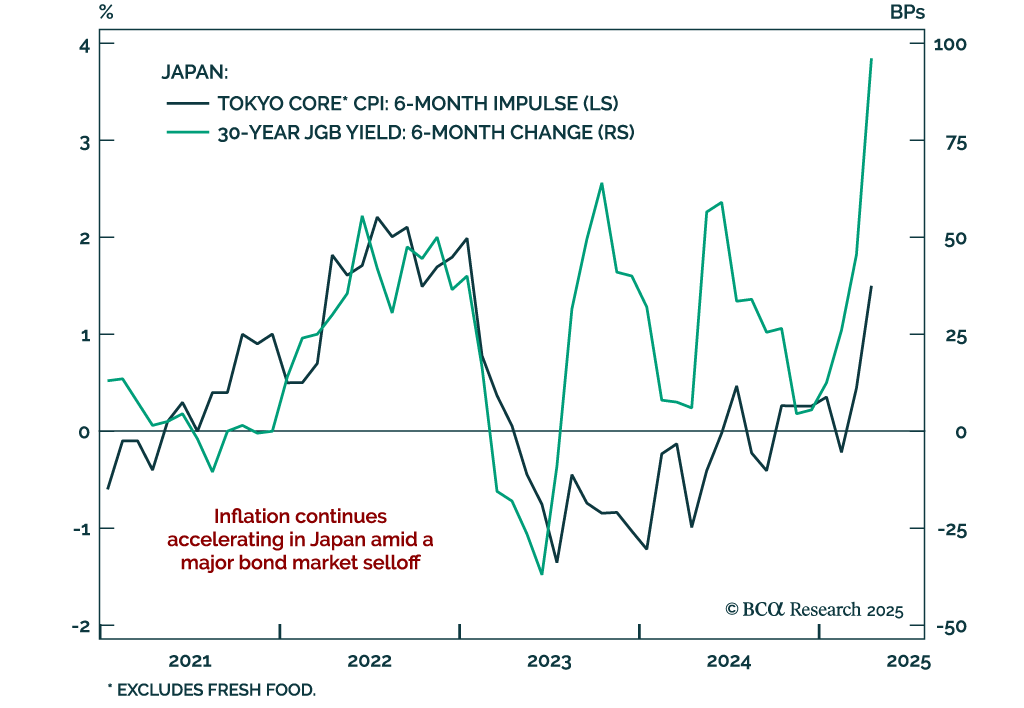

Tokyo CPI surprised to the upside in April, signaling that Japanese inflation shows no sign of deceleration and putting the Bank of Japan (BoJ) in a complicated position. Investors should remain maximum underweight in JGBs and overweight in…

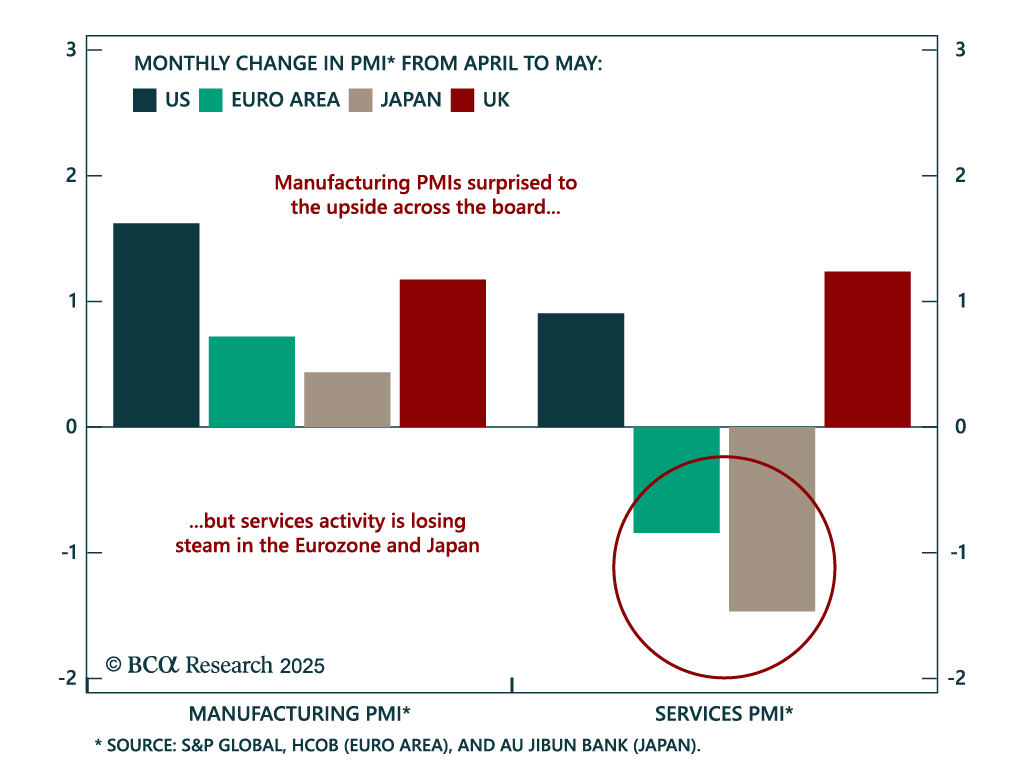

May PMIs confirm the improvement in confidence due to fewer concerns about US tariffs. Manufacturing flash PMI numbers showed resilience. The services activity PMI is more of a mixed bag.The US composite index beat estimates, increasing to 52.1 from 50.6,…

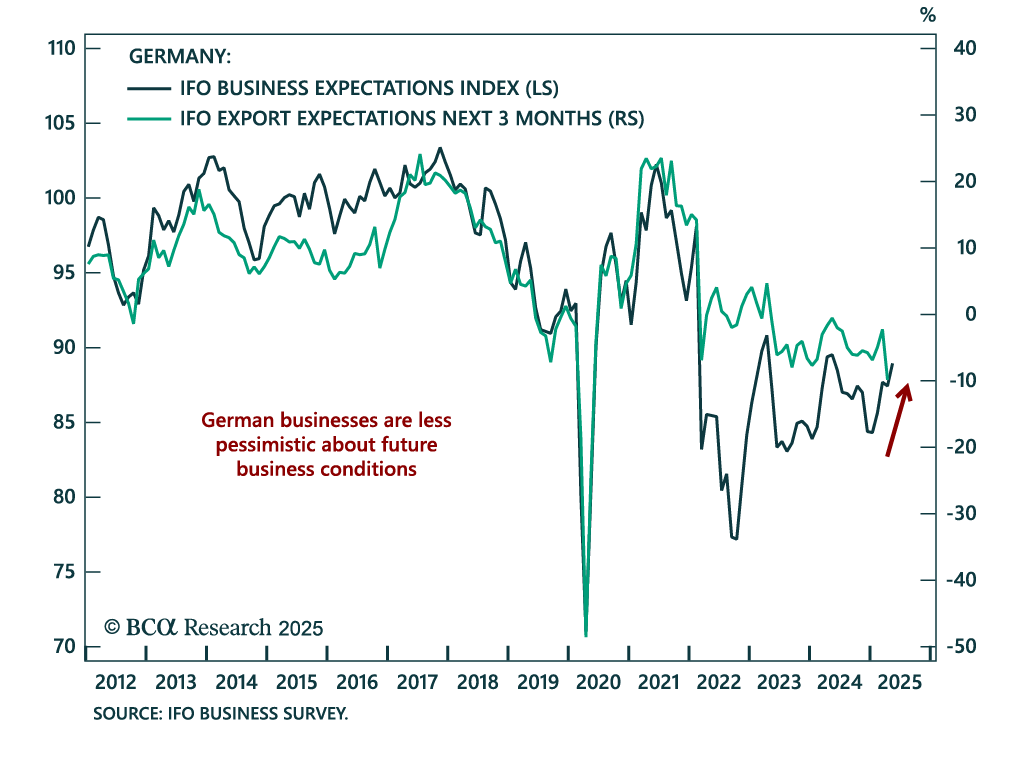

Business sentiment improved slightly in May, corroborating the message from other soft-data indicators of Eurozone business activity, which remain weak but are not plummeting. The increase in the future expectations index to 88.9 from 87.4 a month…

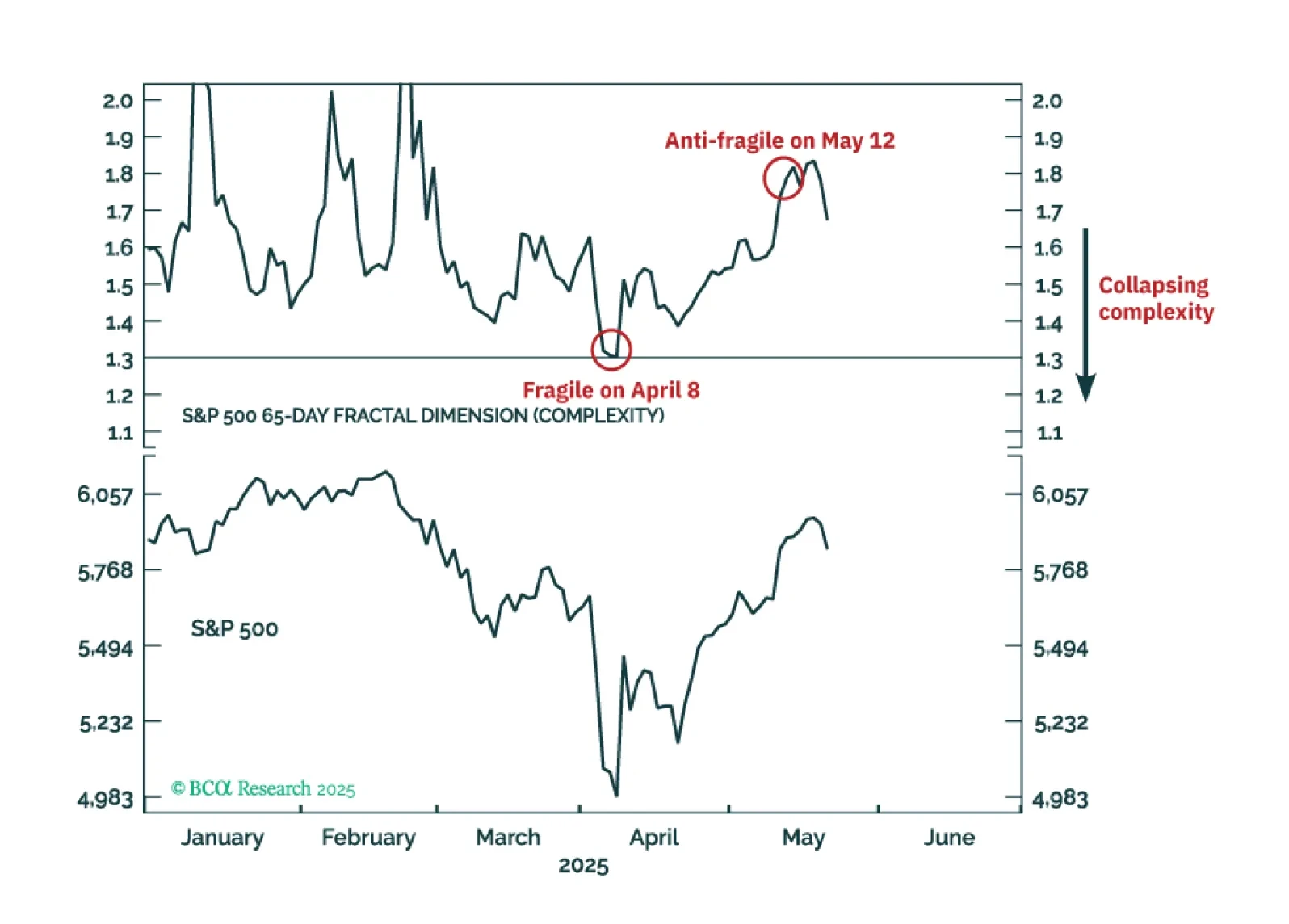

Right now, the major stock and bond markets are more ‘anti-fragile’ than fragile, and the Joshi rule recession indicators signal that a US recession is not imminent. This justifies a neutral, or default, tactical weighting to both stocks and bonds until a major market does become fragile, or until recession risk elevates. The one major price trend that is fragile is the 65-day selloff in the US dollar, which justifies a tactical overweighting to the dollar.

UK inflation surprised to the upside in April. Headline inflation rose to a 15-month high of 3.5%, from 2.6% the month before. Core inflation also surprised above estimates, printing 3.8% vs. 3.4% in March. Services inflation climbed to 5.4% from 4.7%. Higher…

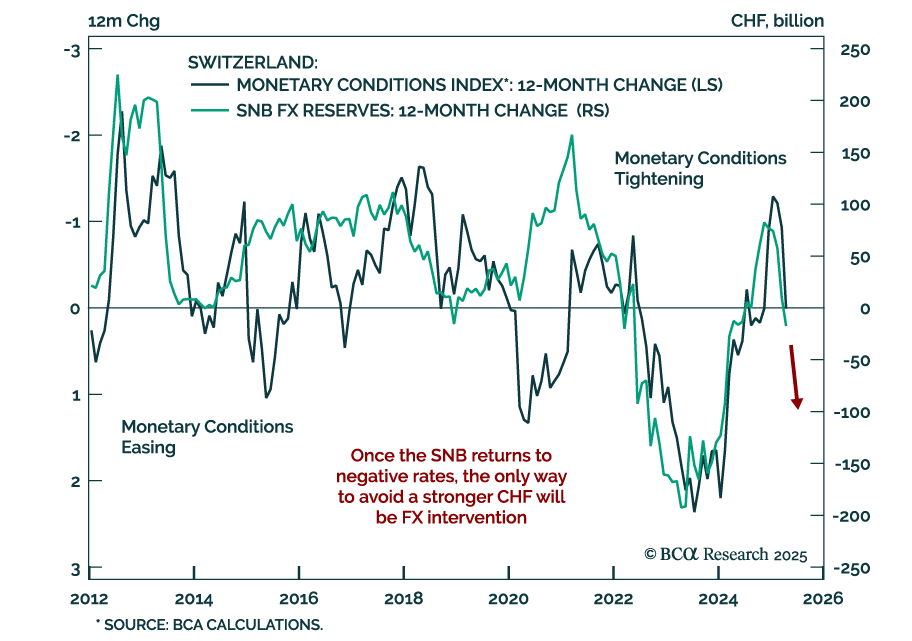

Swiss National Bank will have to resort to negative interest rates and FX intervention before year-end. Swiss inflation fell to 0% year-over-year in April, or the lower end of the SNB’s 0%-2% target range, and the continued strength in the Swiss Franc…

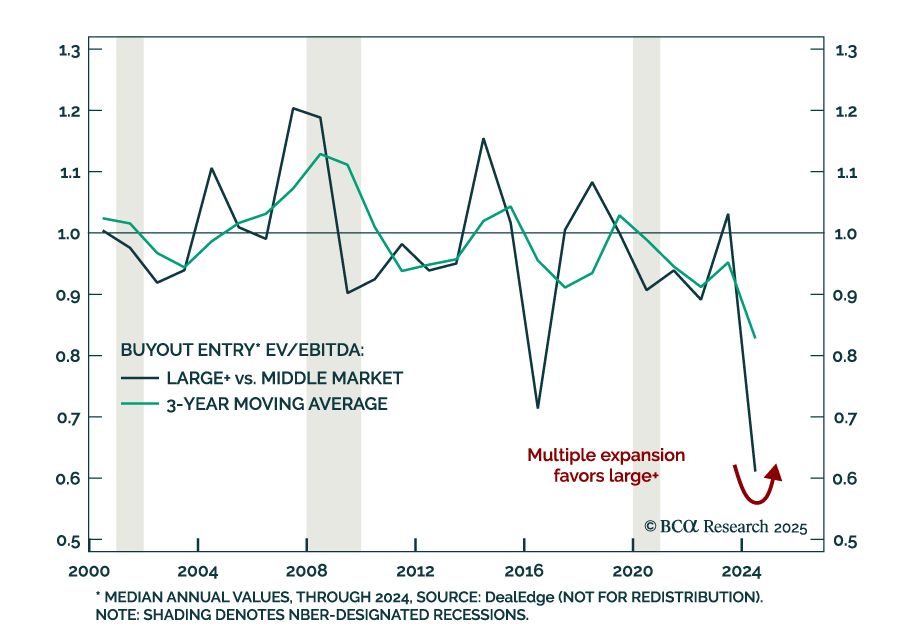

Our Private Markets & Alternatives team’s latest update to return expectations for Global Buyout yields a modest increase in projected returns, including the expectation of a greater multiple expansion tailwind in the Large+ segment. The team…