Economy

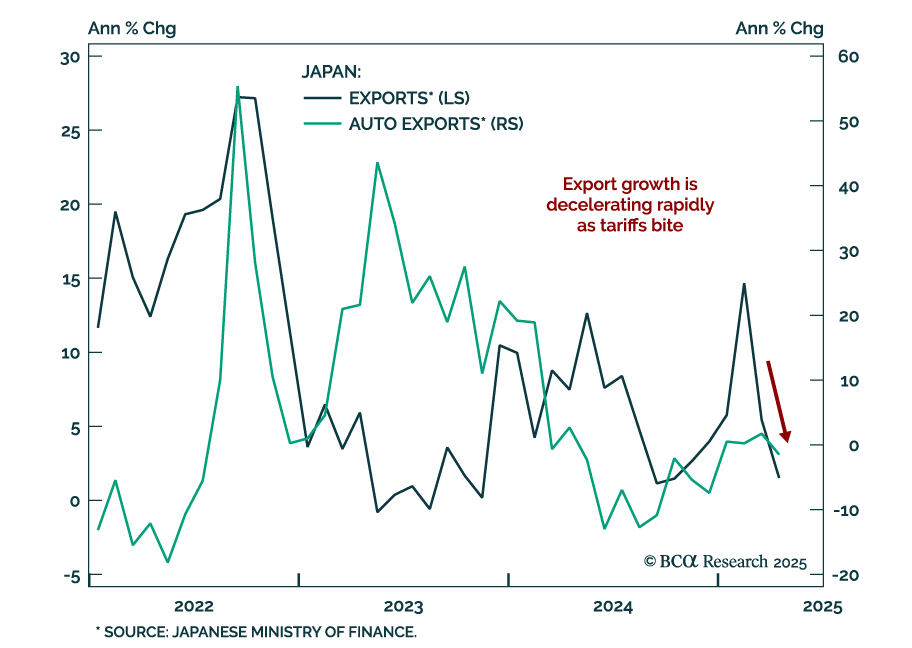

Japan’s export growth slowed materially in April as shipments to the US, Japan’s largest export destination, fell 1.8% from a year earlier. Japan has yet to make a trade deal with the US. Japanese export growth slowed to 2% from 4% in March, which aligns…

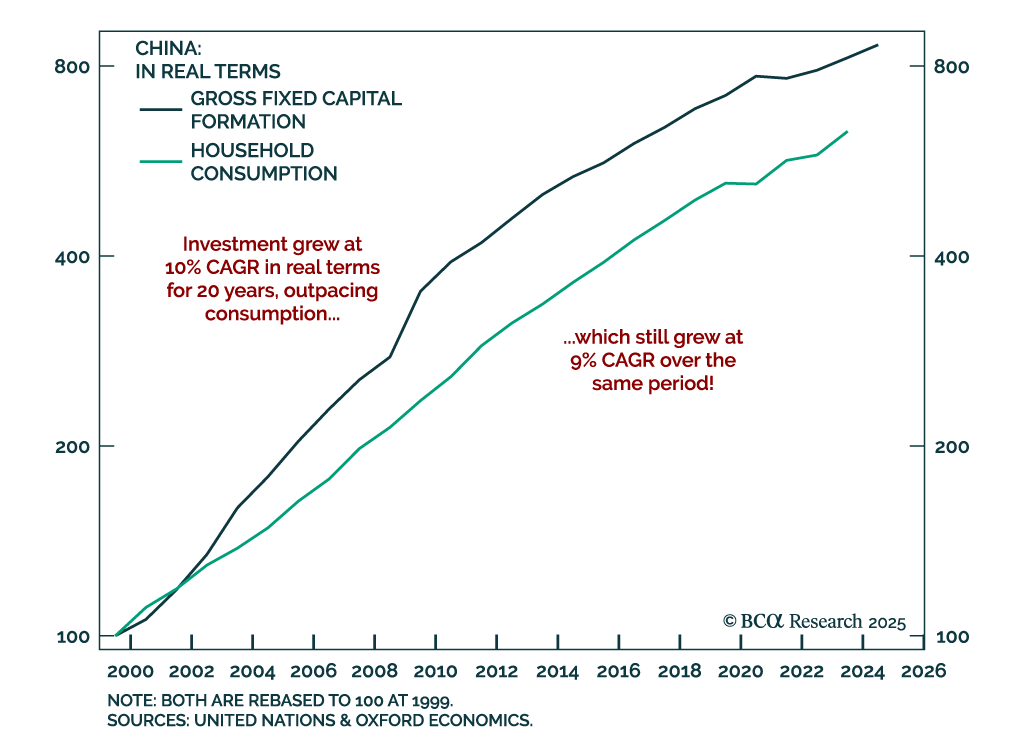

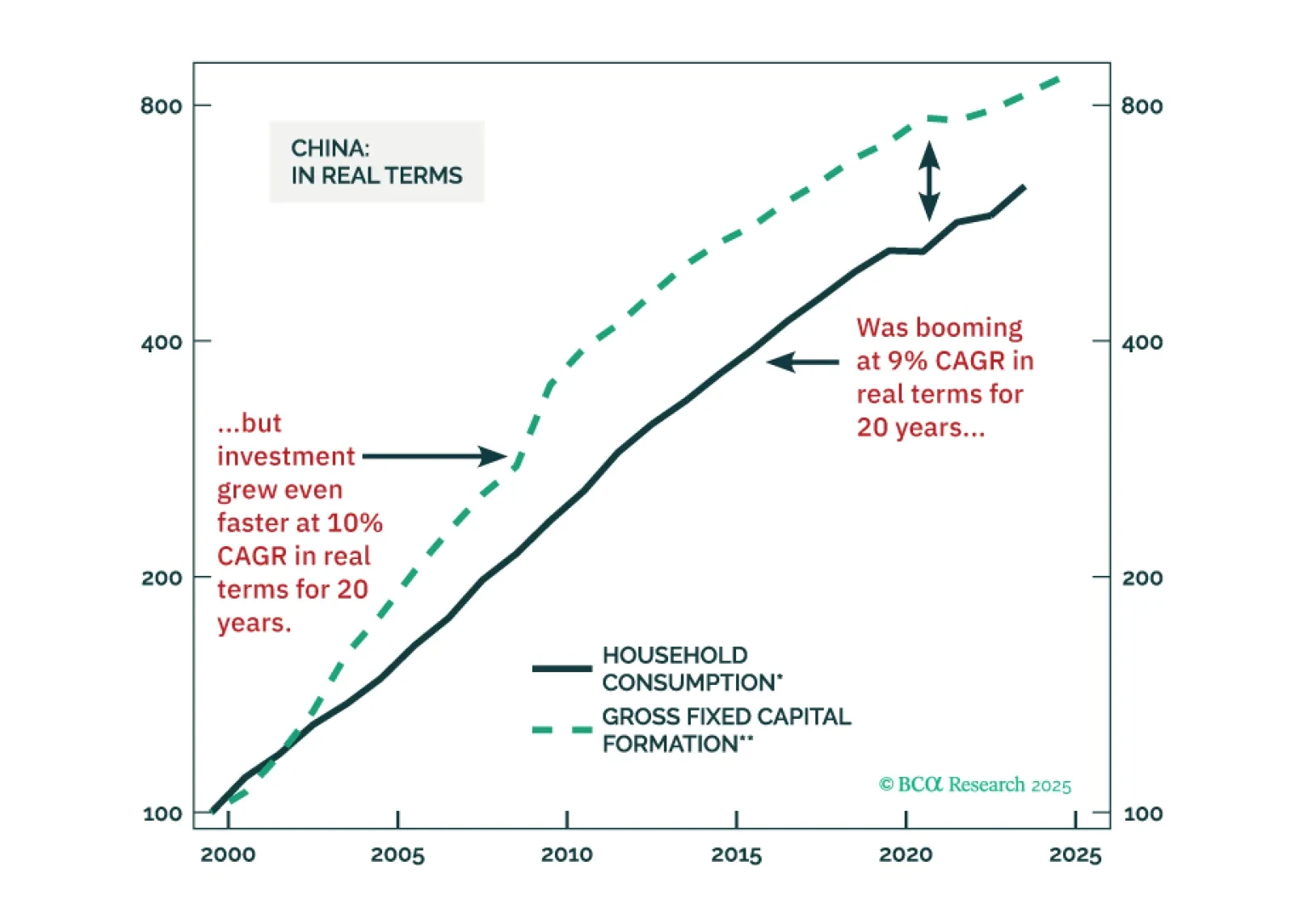

Our EM strategists warn that China’s overinvestment problem has no quick fix, keeping deflationary pressures in place and limiting upside for Chinese equities. Excessive domestic investment, driven by aggressive credit creation, is at the heart of China’s…

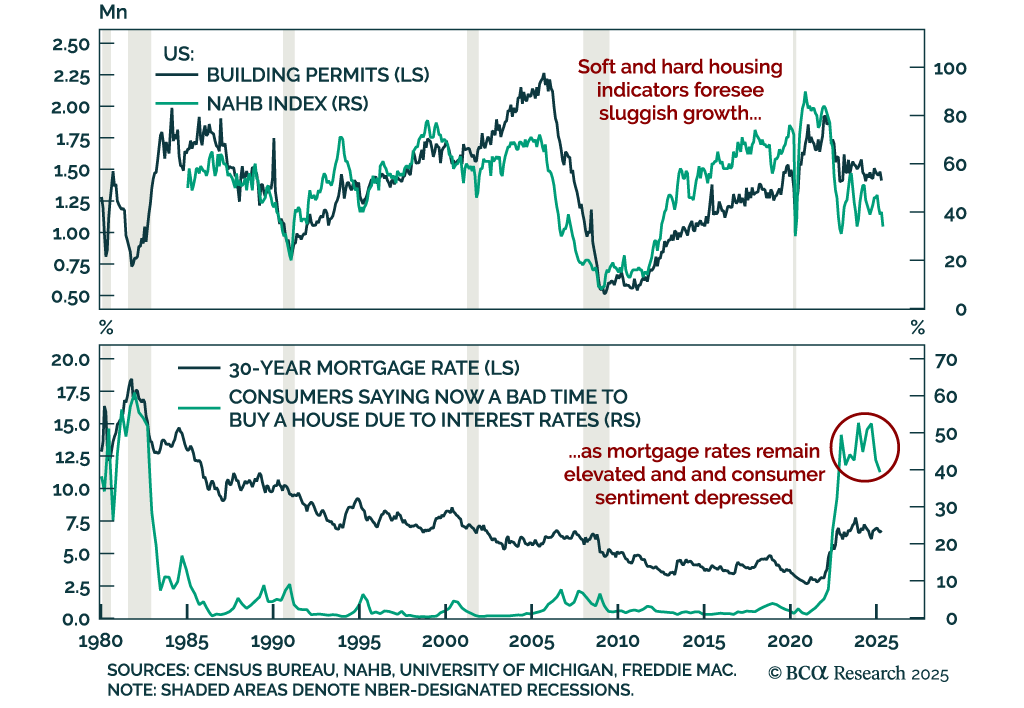

Weak April housing data and deteriorating builder sentiment reinforce our defensive stance, as recession risks remain underpriced. Housing starts rose at a 1.6% m/m annualized rate, missing expectations. Similarly, building permits, a leading indicator of…

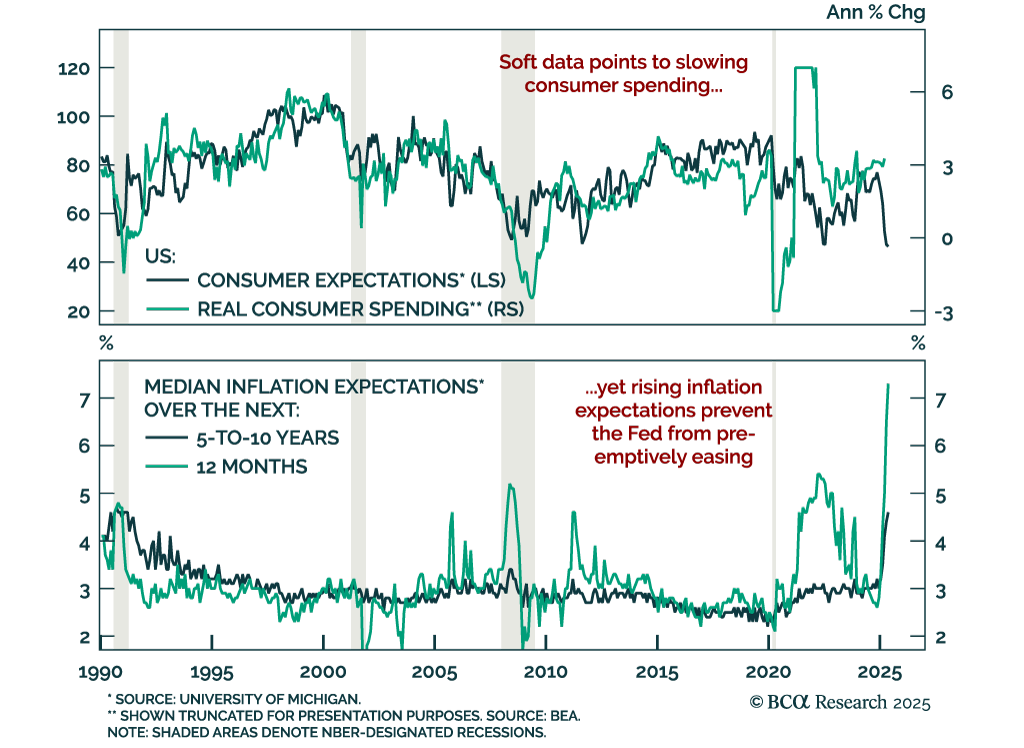

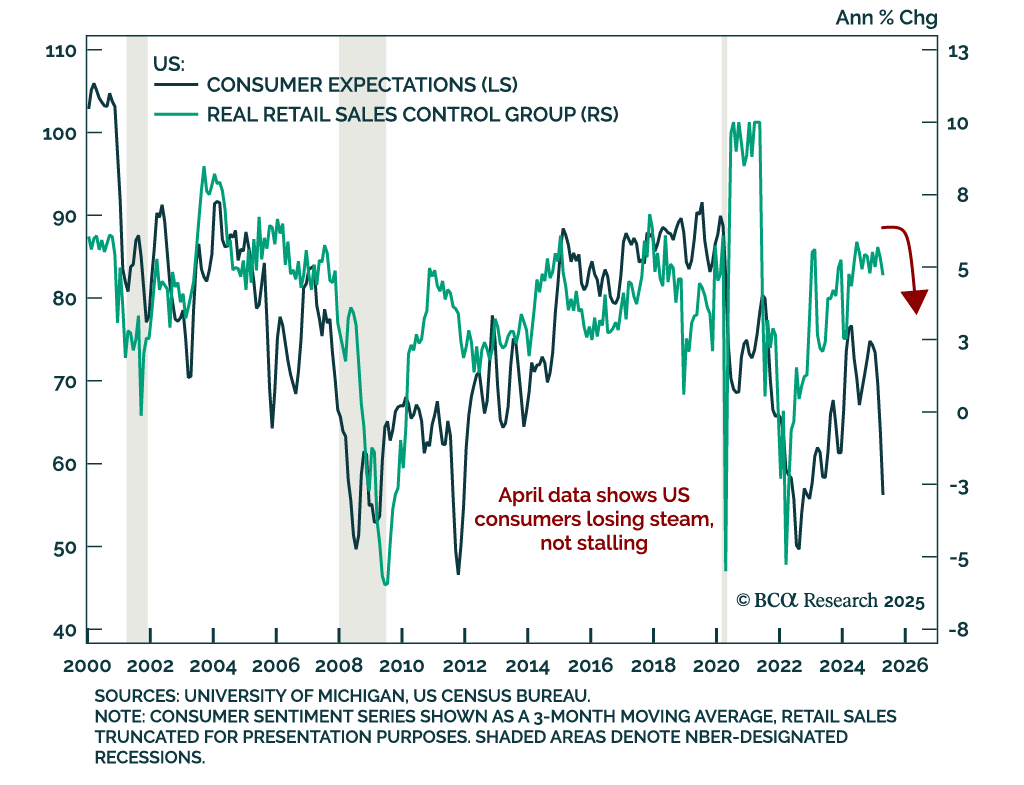

Deteriorating US consumer sentiment and surging inflation expectations add to growth concerns and reinforce our long-duration bond stance. The preliminary May University of Michigan Consumer Sentiment Index missed expectations, falling to 50.8 from 52.2. The…

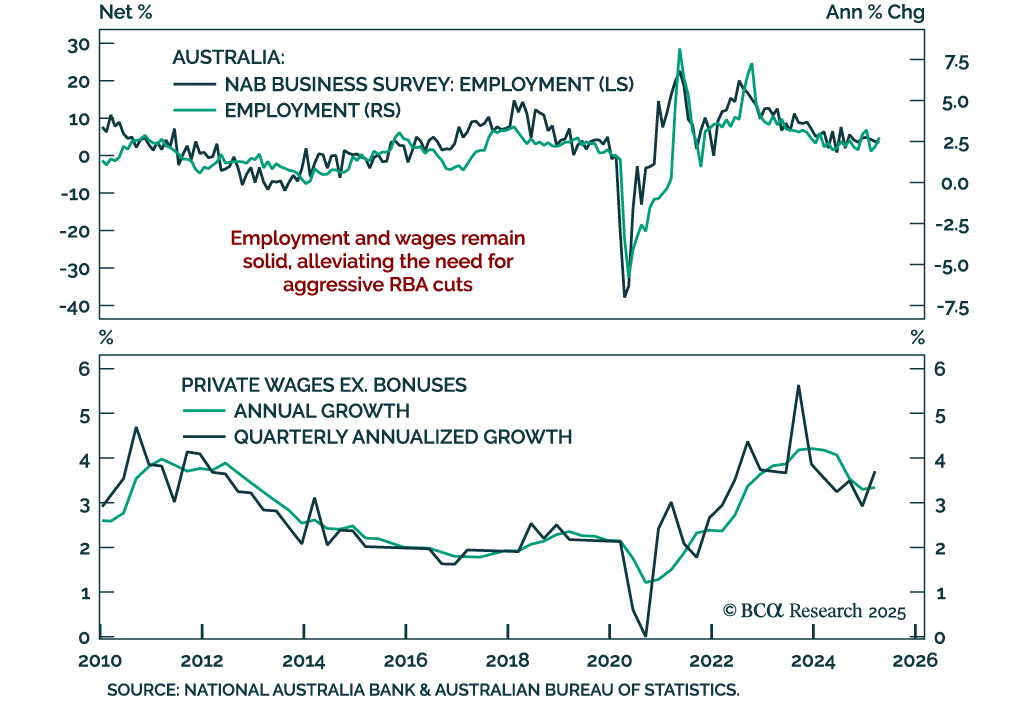

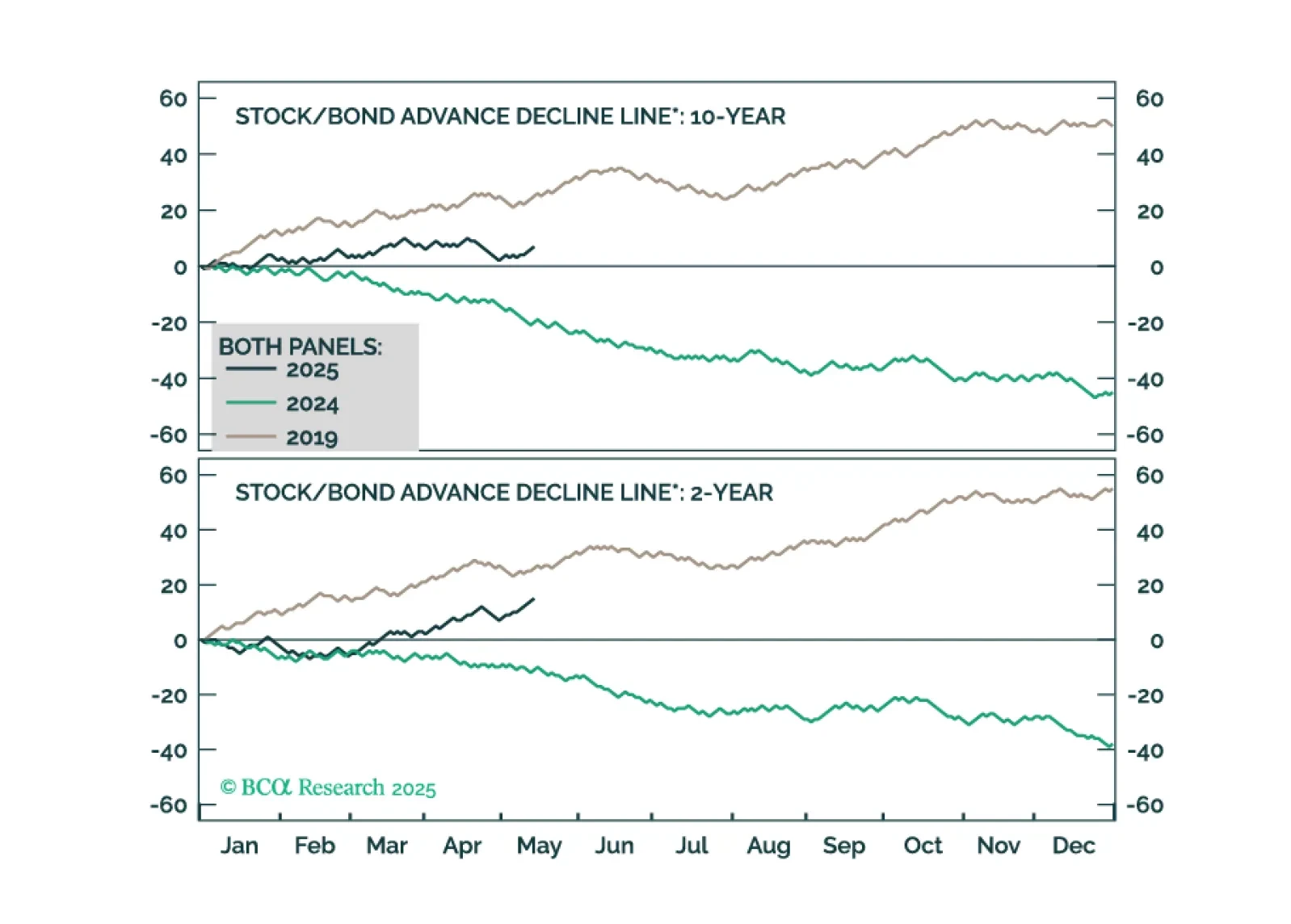

A strong Australian labor market is limiting the scope for RBA easing, reinforcing our underweight on Australian government bonds. Our Chart Of The Week comes from Robert Timper, strategist in our Global Fixed Income Strategy team. The April NAB business…

The prevailing narrative around the world is that Chinese households are not spending enough and that China has overly relied on exports for economic growth. Some parts of this conjecture are incorrect. The primary economic imbalance in China is neither inadequate consumption nor outsized exports. The main economic excess is overinvestment.

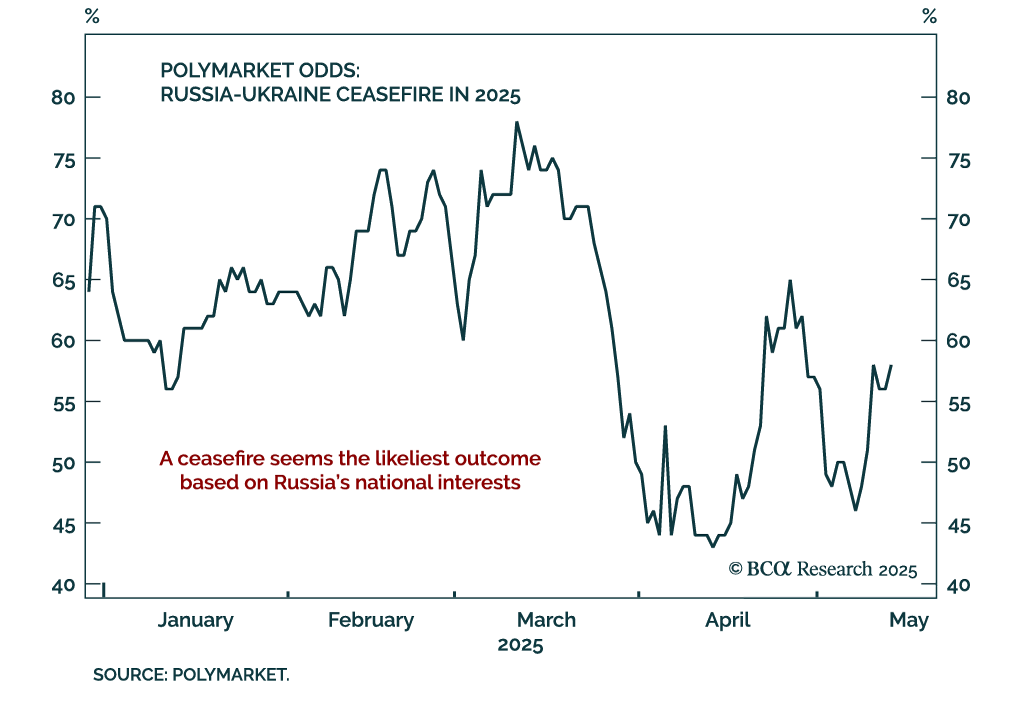

Our Geopolitical strategists expect a Ukraine ceasefire as Russia’s economic weakness compels Putin to shift focus from war to domestic stability. The likely outcome is not peace, but a frozen conflict that enables Russia to consolidate territorial gains…

April retail sales slowed, but signs of resilience in discretionary spending and labor data suggest US consumers are holding up. Headline retail sales rose 0.1% m/m, above expectations but decelerating from the upwardly revised 1.7% March gain. Core sales…

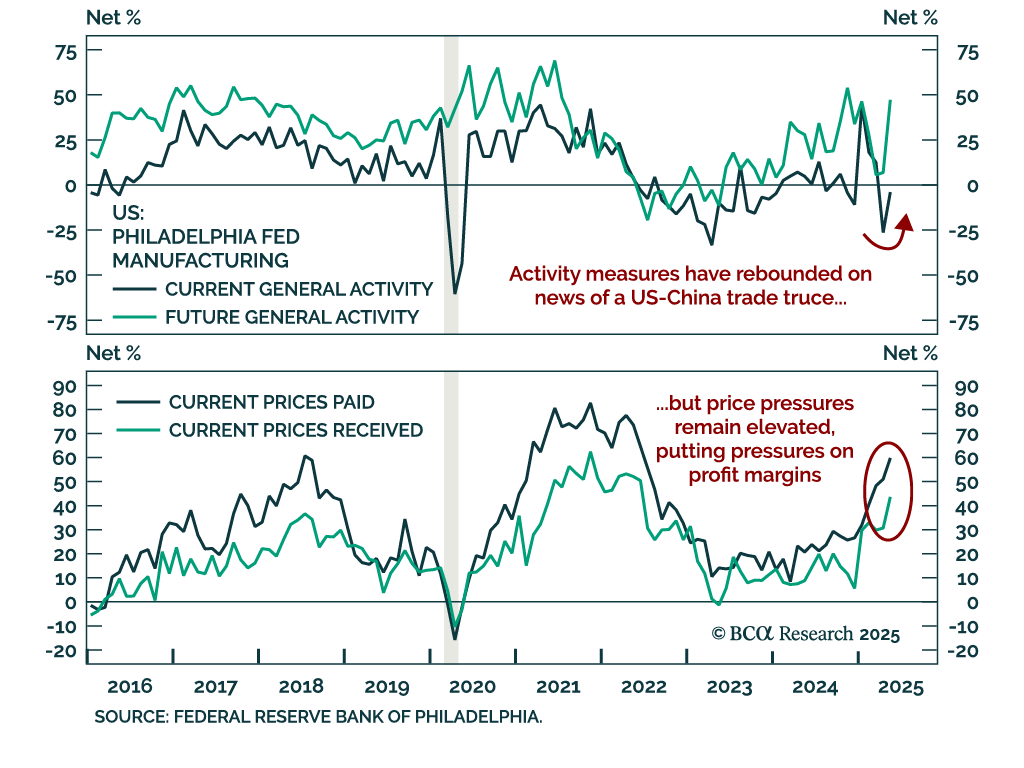

The US-China trade truce lifted short-term manufacturing sentiment in May, but margin pressures persist, reinforcing the case for defensive, domestic-focused equity positioning. The Empire and Philly Fed regional manufacturing surveys delivered a split signal…

Tariff front-running behavior makes the April hard economic data difficult to interpret, but we take the strong reading from Food Services spending as a signal that the US consumer has not yet buckled.