Economy

European equities have some short-term support, but global growth risks will cap gains. Our Chart Of The Week comes from Mathieu Savary, Chief European Investment Strategist. Mathieu sees probable but limited upside for European equities in the near term. His…

Our Portfolio Allocation Summary for May 2025.

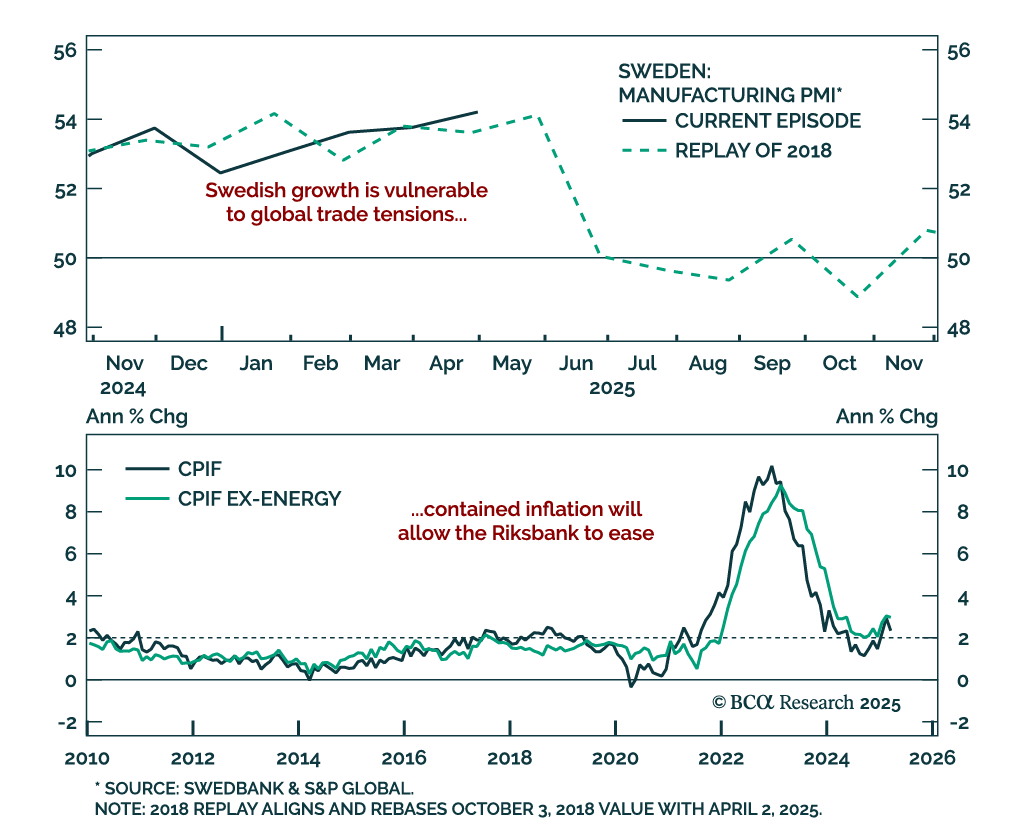

The Riksbank’s cautious stance sets up a dovish pivot, reinforcing our long Swedish bonds view and SEK fade vs. USD. The central bank held rates at 2.25% for the second time this year, with Governor Thedéen describing policy as well-balanced despite rising…

The inflation divergence between the US and Eurozone drives our call to stay long US duration. Inflation, typically a lagging indicator, blends slow-moving labor pressures with fast-moving supply drivers. The COVID inflation spike was a rare fusion of both,…

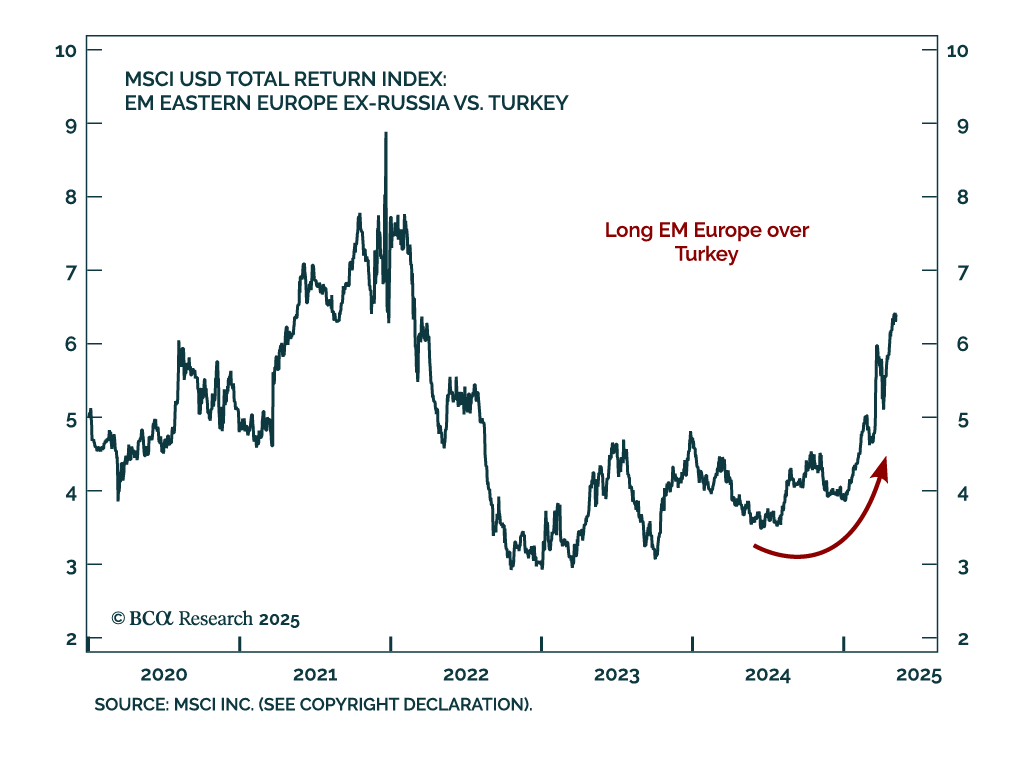

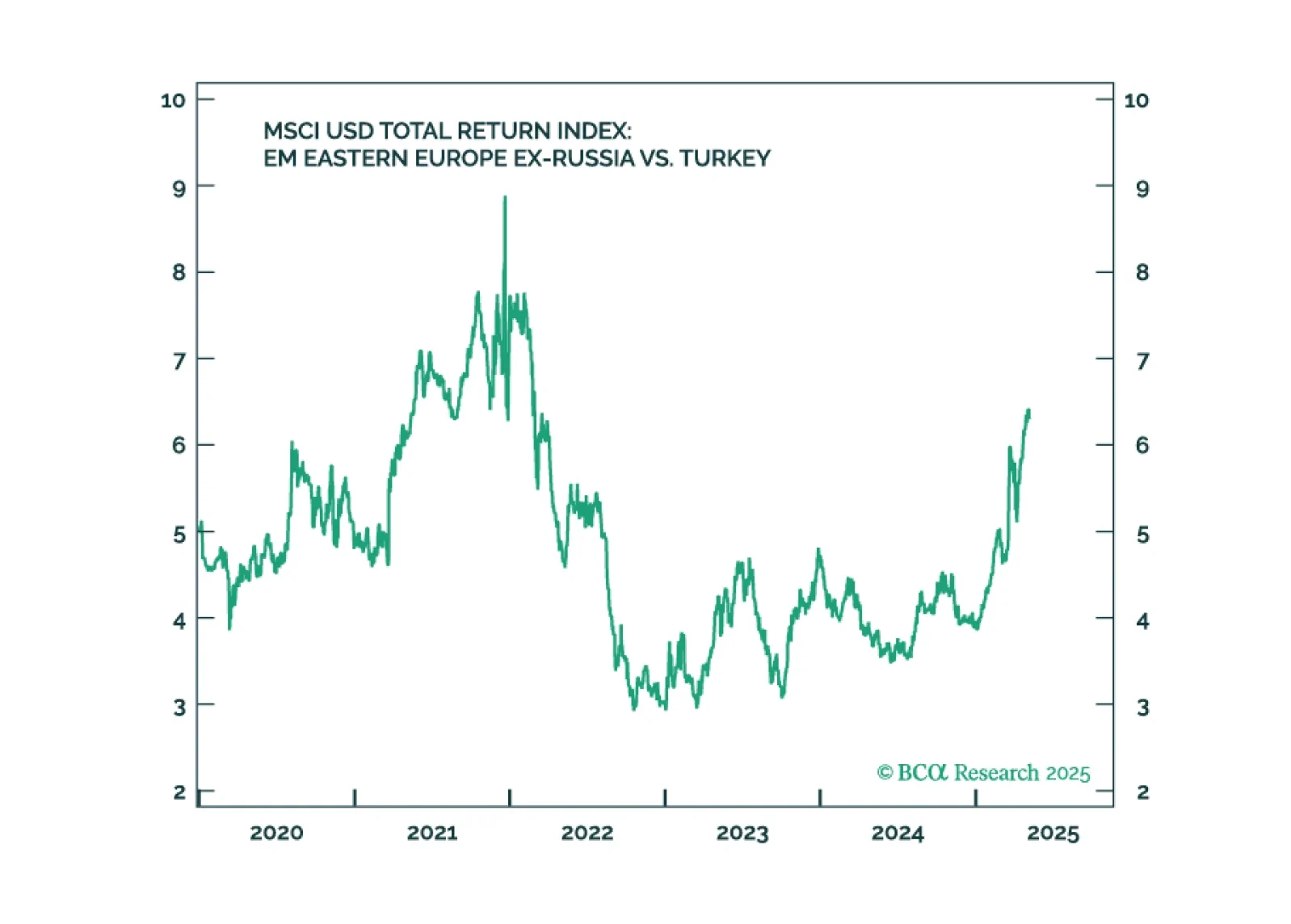

Our Geopolitical strategists recommend underweighting Turkish assets. Erdogan’s weakening rule, rising social unrest, and eroding governance are deepening Turkey’s macro deterioration. Inflation will stay sticky as odds of new government spending rise, and…

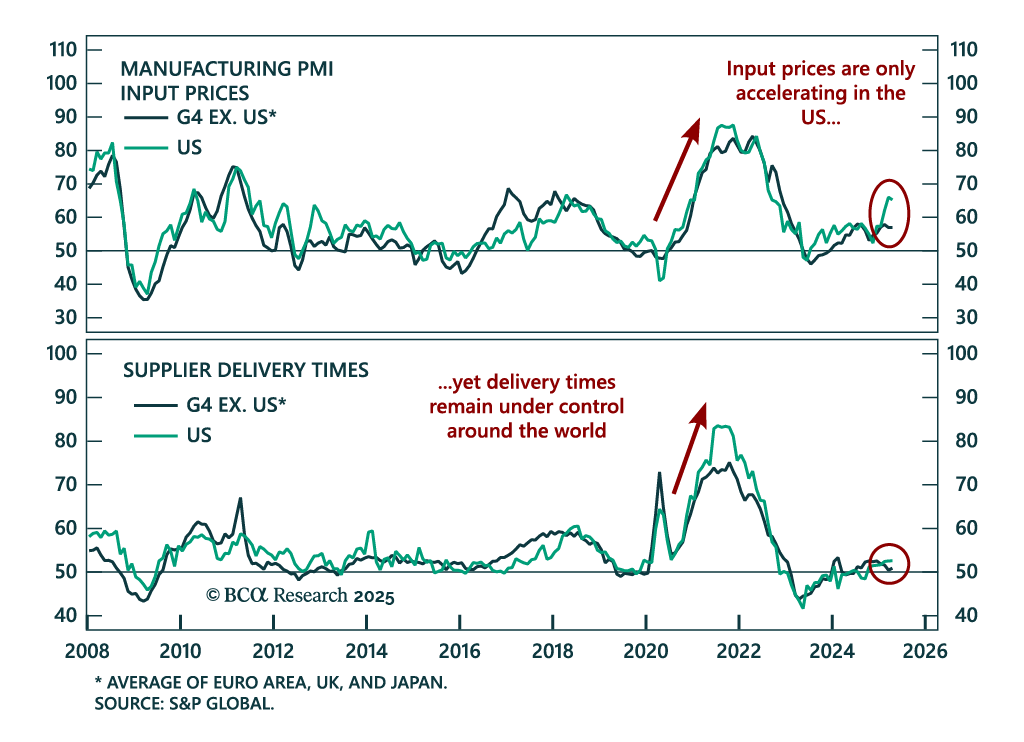

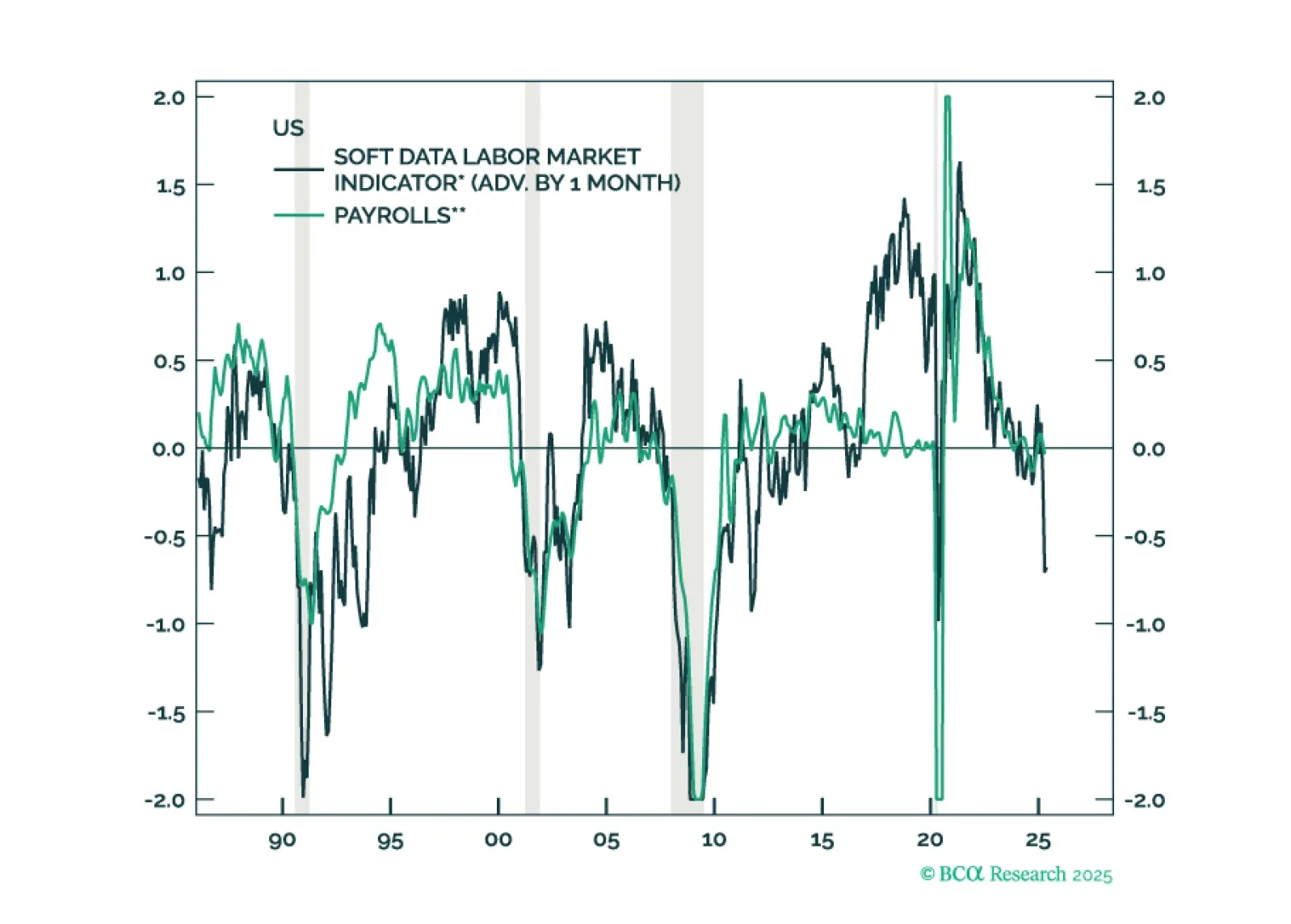

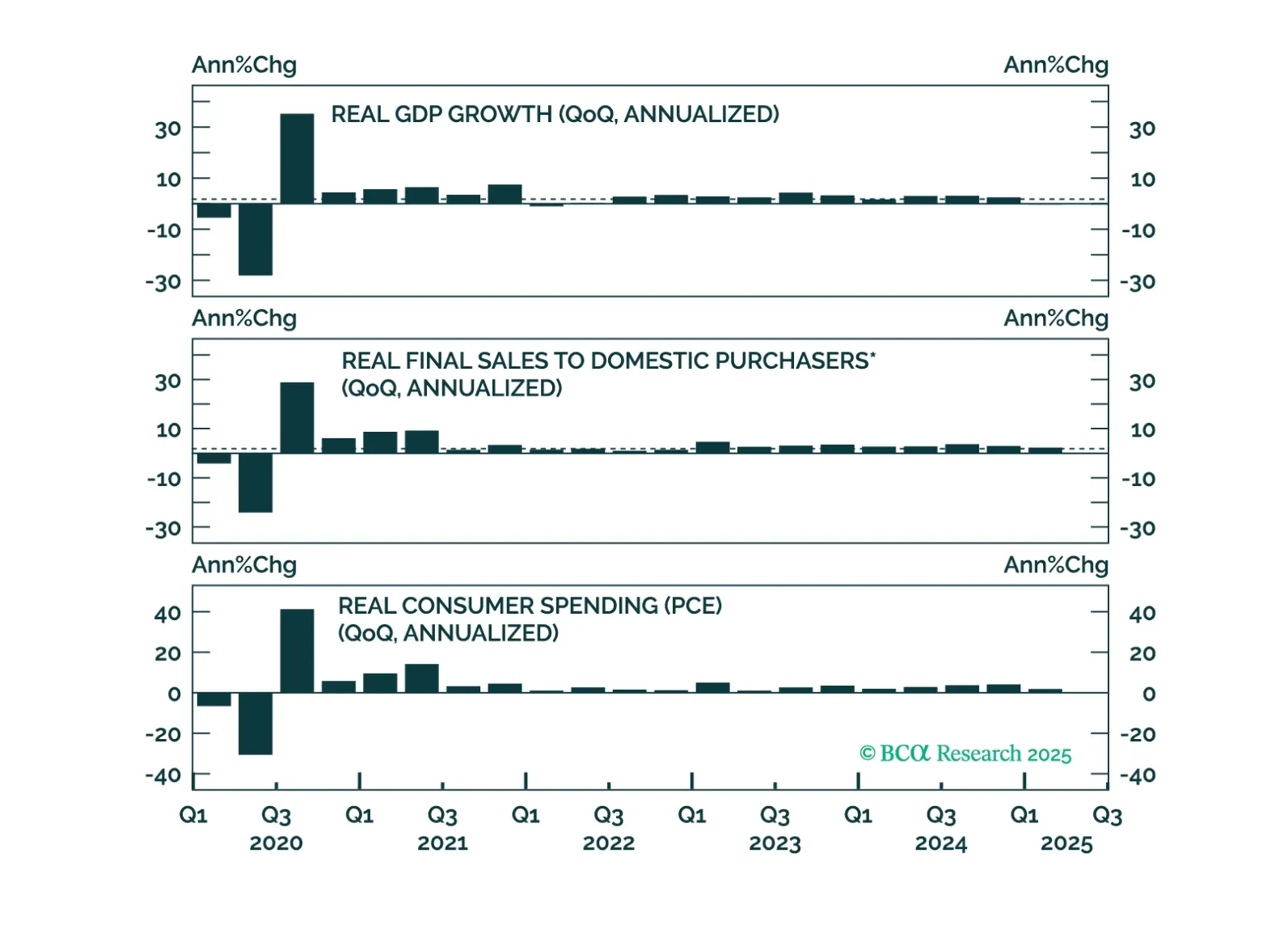

It may take several months for the tariff shock and policy uncertainty to filter through the real economy, but survey-based data are already sending a warning. Equities have priced in a lot of good news, and investors are too sanguine about the risk of a US recession.

Erdogan's rule continues to decline. Social unrest will persist, governance will erode, and the macro backdrop will deteriorate further. We recommend underweighting Turkish assets.

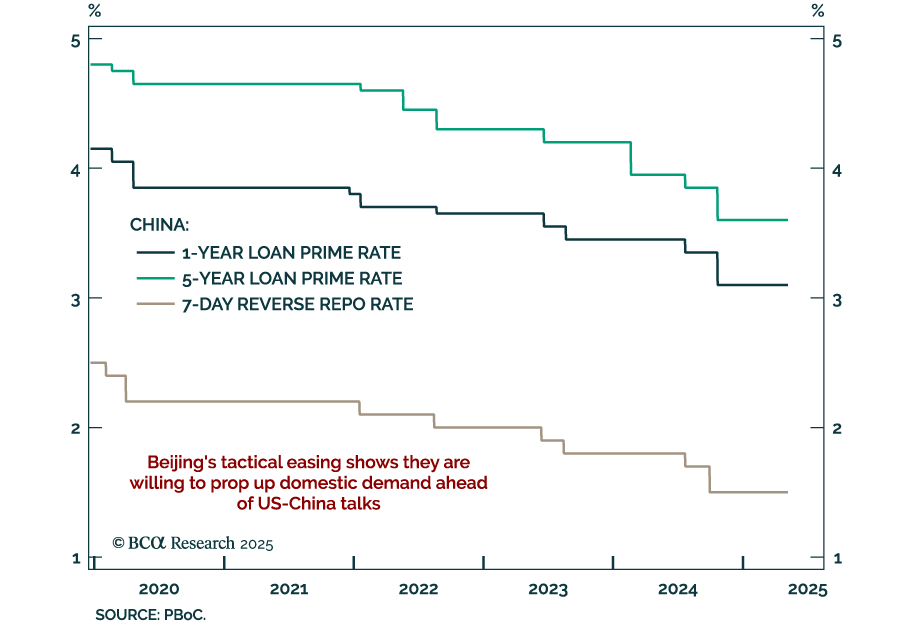

The PBoC’s latest easing aims to cushion growth risks and strengthen Beijing’s position ahead of US trade talks. In a rare pre-announced decision, China’s central bank cut its policy rate by 10 bps and the reserve requirement ratio by 50 bps, delivering…

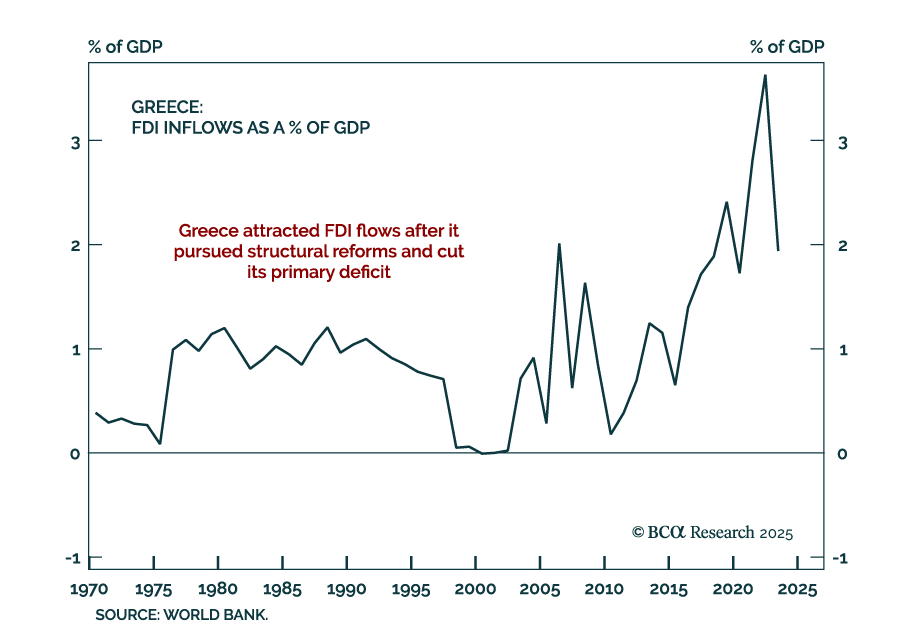

Our GeoMacro strategists remain negative toward US equities as President Trump’s efforts to limit the foreign investments of US firms will undercut their competitiveness. FDI brings clear strategic and financial gains, both for the investing firms…

The Fed held rates steady this afternoon, and the timing of its next move will be dictated by whether the tariff shock to inflation is transitory or more long lasting.