Economy

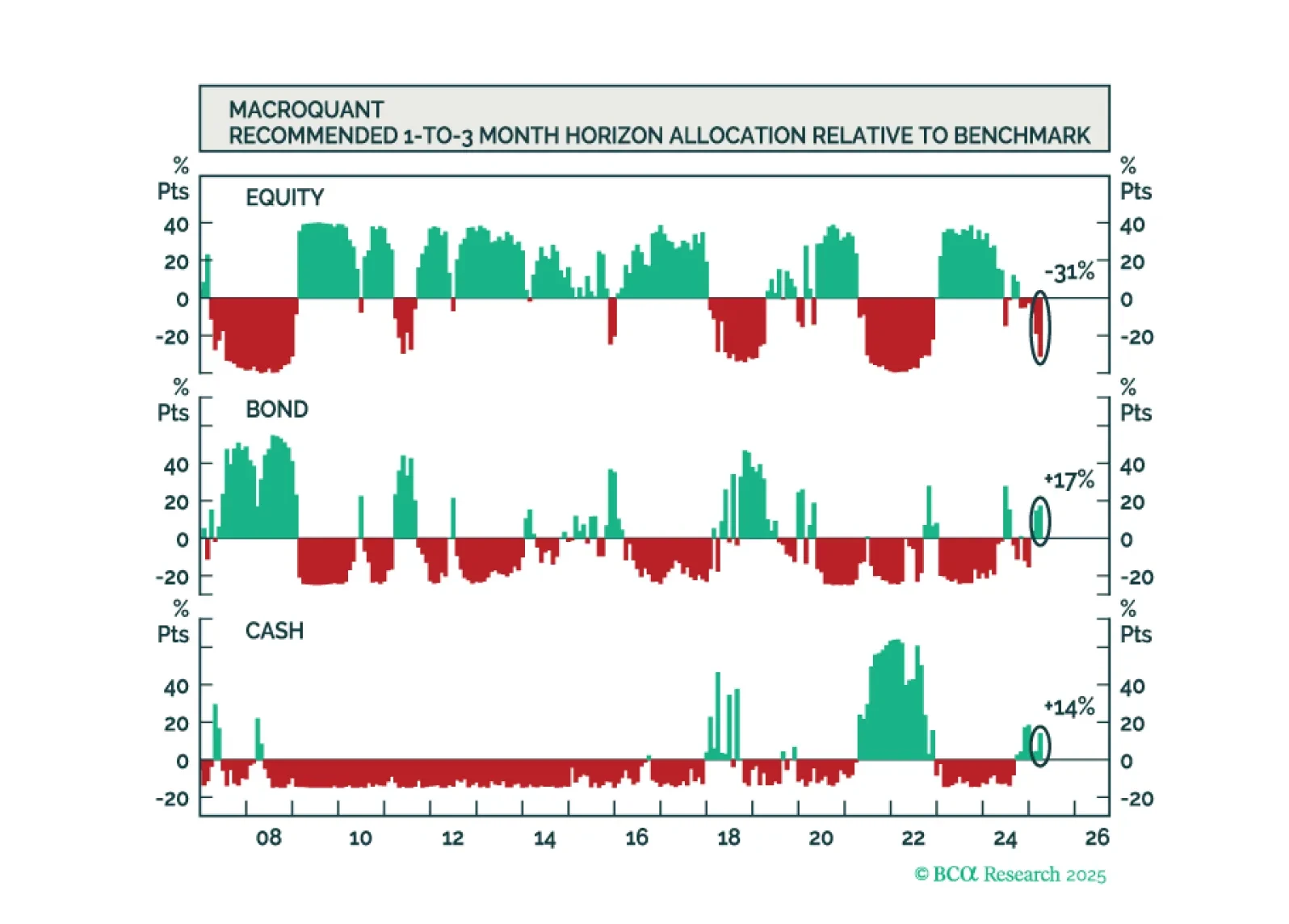

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

MacroQuant sees the risks to US growth as being to the downside and the risks to inflation as being to the upside. Such a stagflationary brew justifies an underweight on stocks.

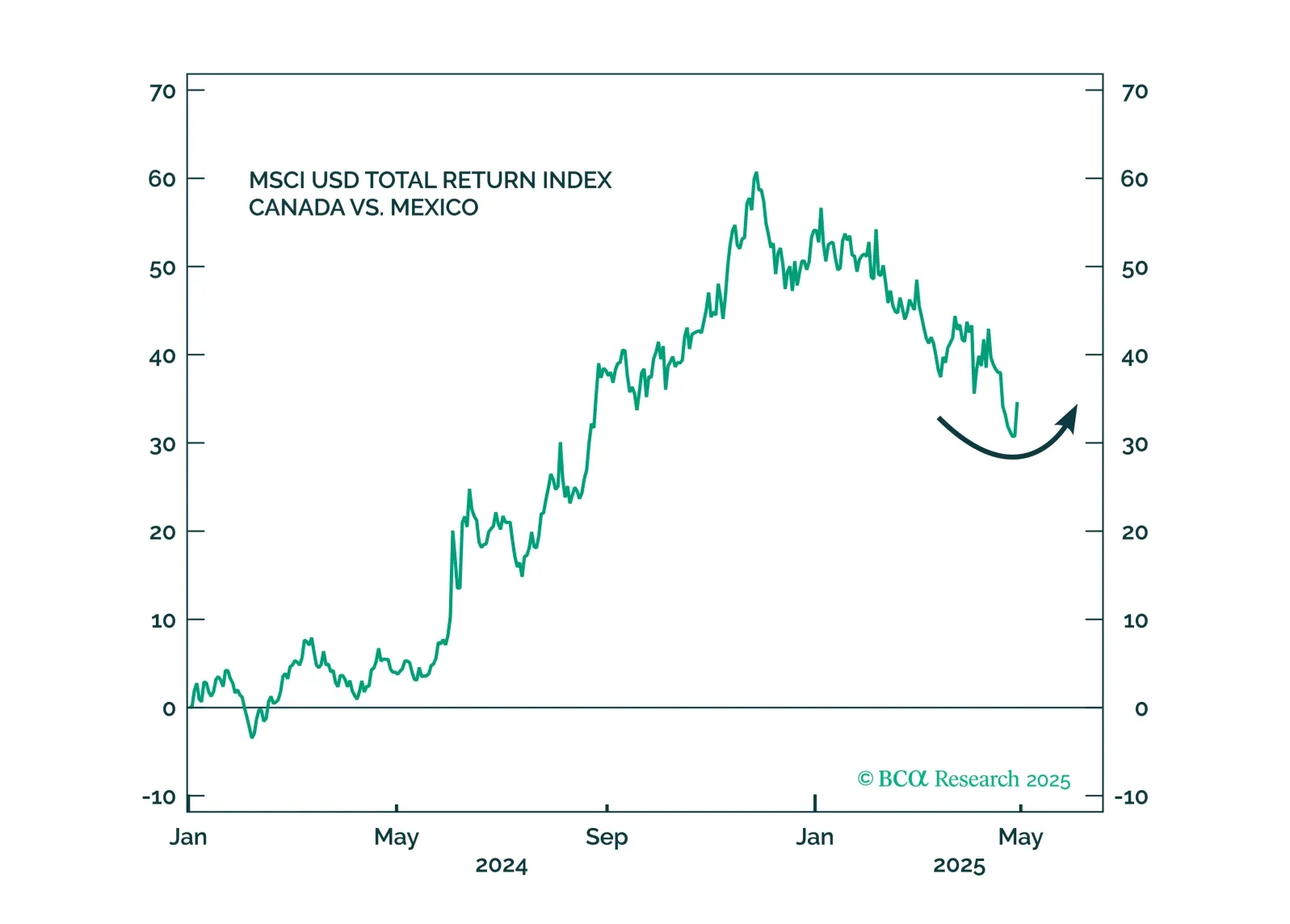

The US and Canada will resolve their trade dispute quickly, leading to a North American deal and better prospects for future relations, as well as for other US trade deals around the world. But even as tariff threats decline, the US economy will slow, weighing on its neighbors. Canada will fare better than Mexico.

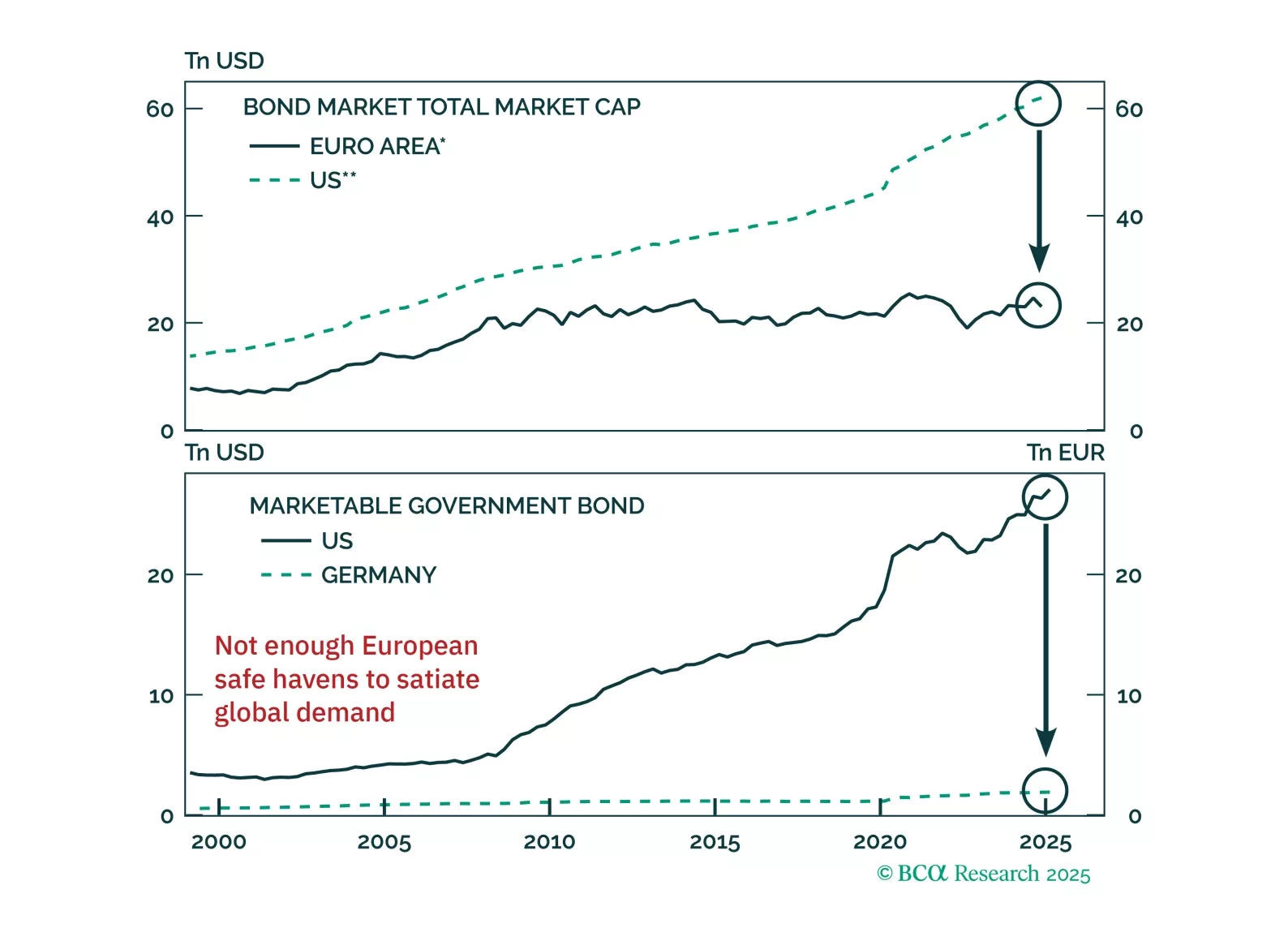

Are bunds the new Treasurys? The euro and German debt are gaining favor as safe havens, but markets may be overplaying the shift. Our latest report dissects what's durable, what's not, and how to trade the dislocation.