Economy

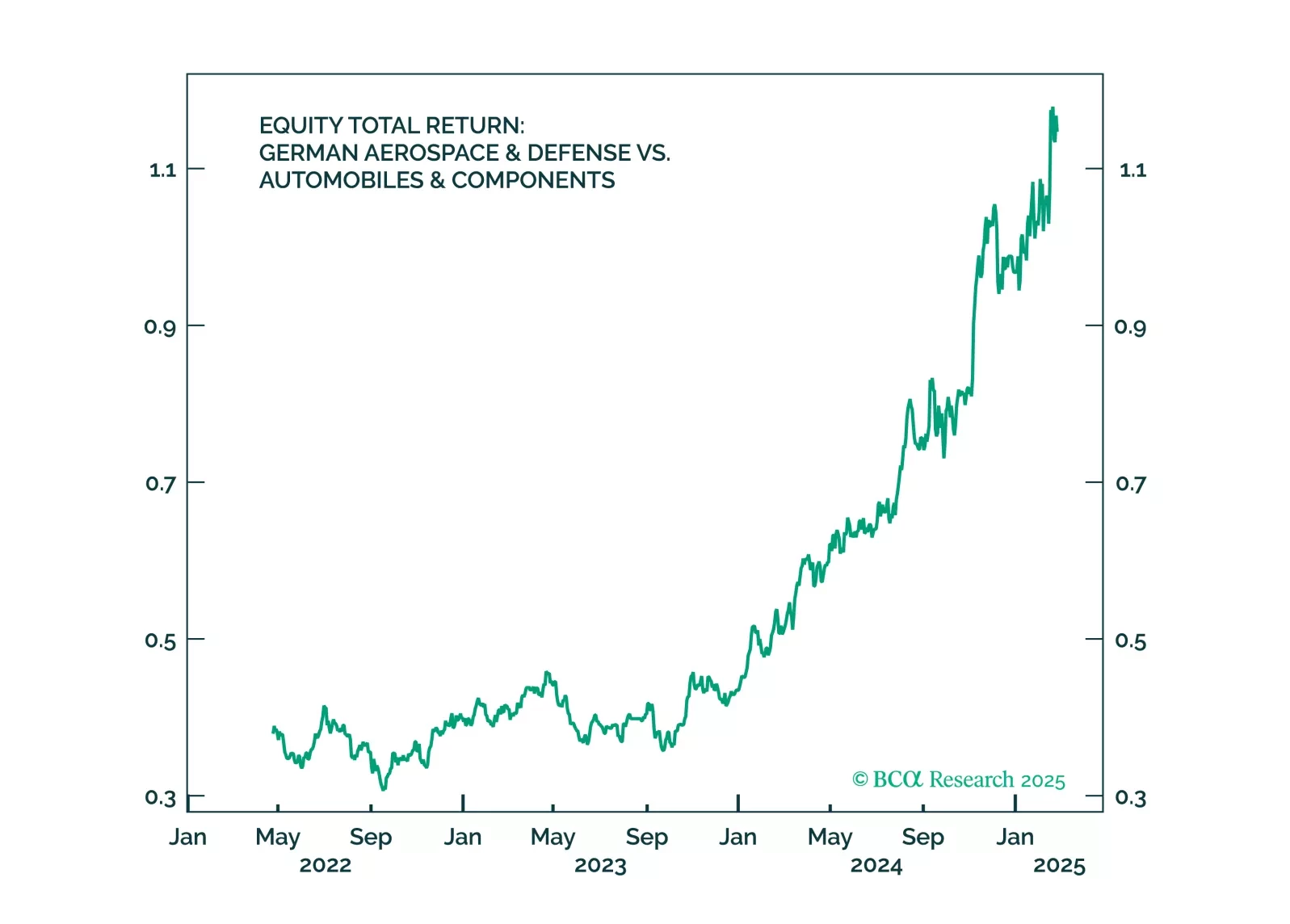

Trump’s ceasefire talks are positive for Germany – and so was the German election result. But Trump’s tariffs will hit Germany soon. Investors should use near-term volatility to increase exposure to Germany.

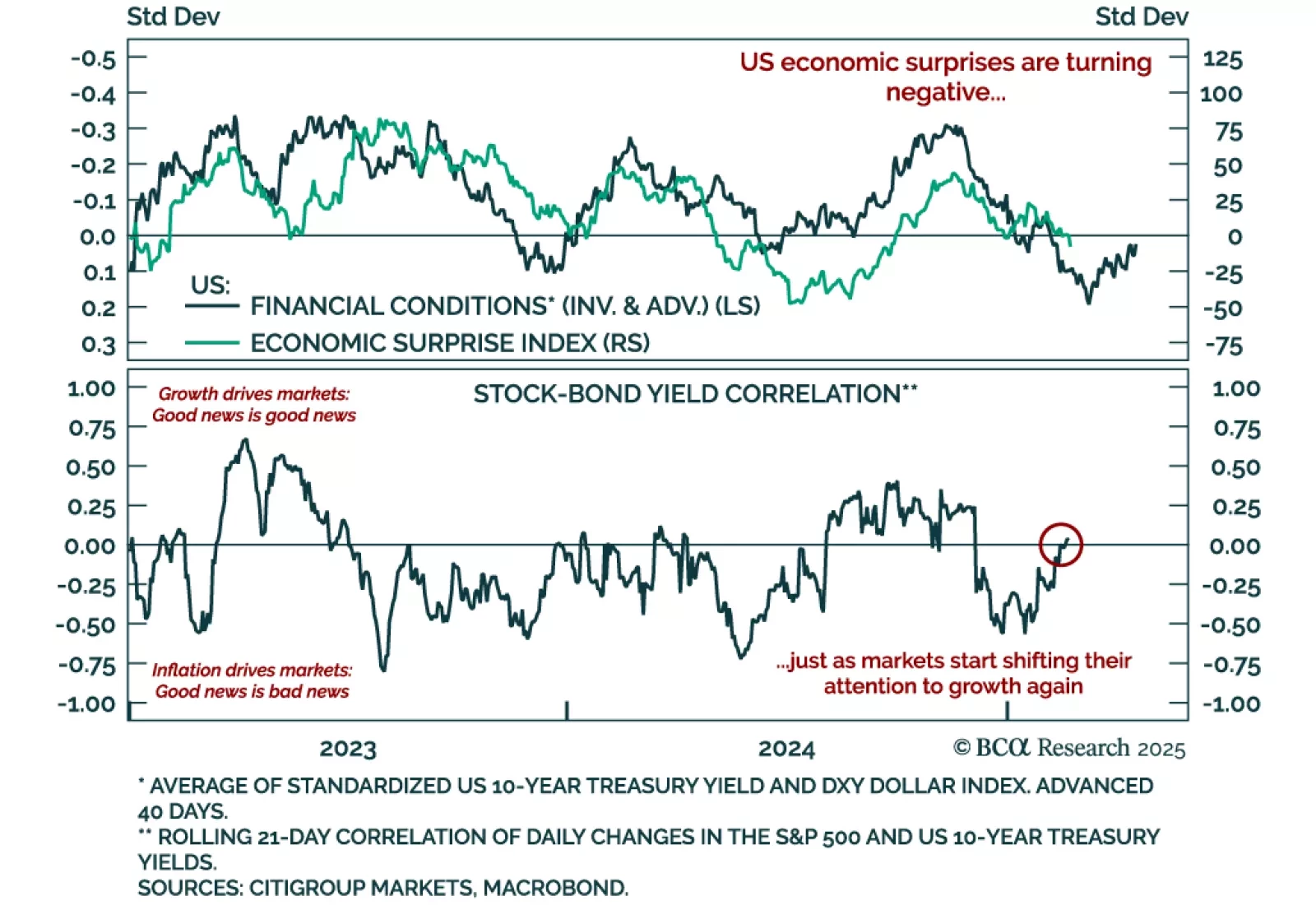

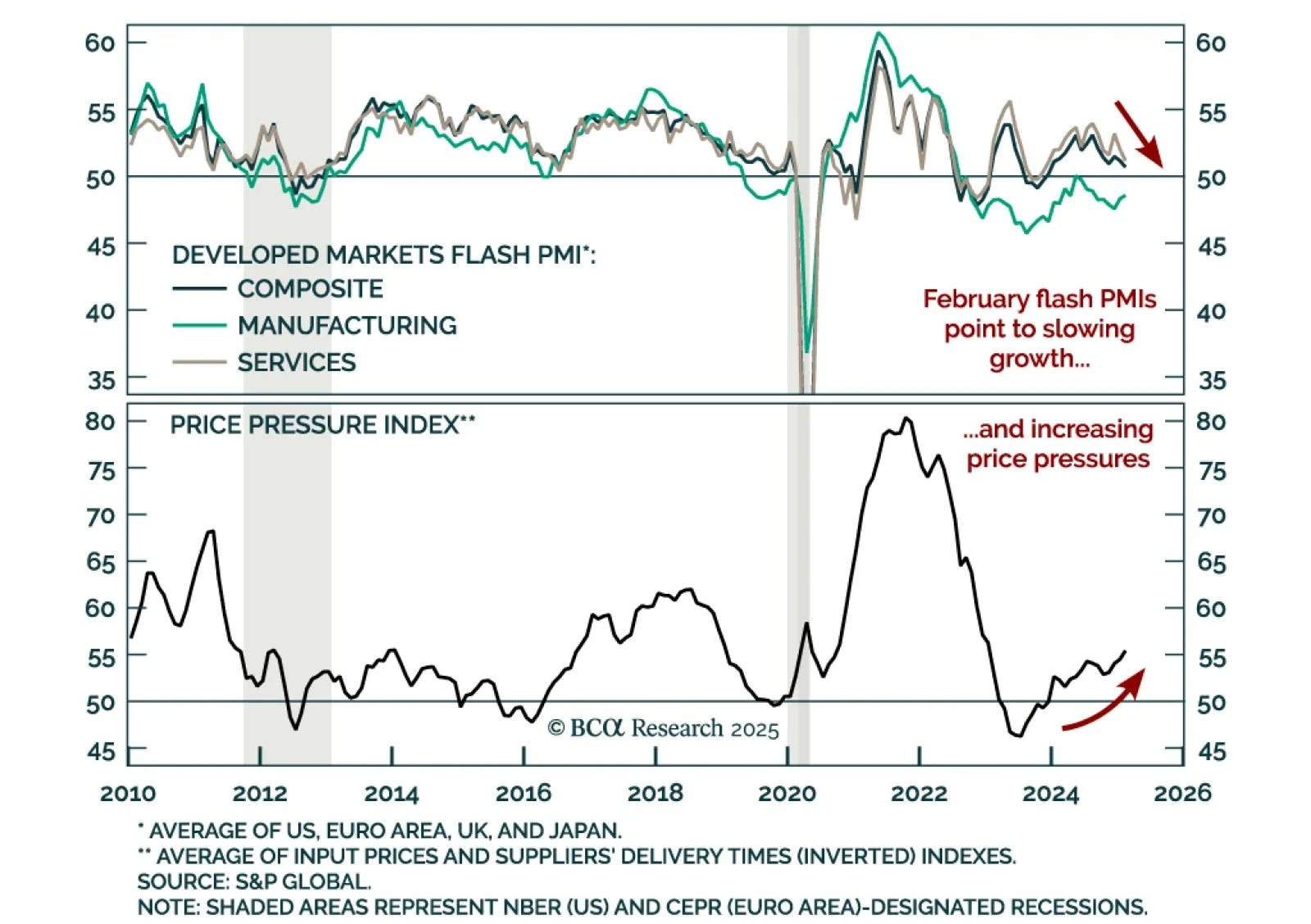

US growth has slowed in recent weeks. This can be seen in the weaker data on retail sales, consumer confidence, services PMIs, and a swath of housing releases (notably starts, existing home sales, homebuilder confidence, and stock prices). It can also be seen in the decline in GDP tracking estimates. The Atlanta Fed's GDPNow model projects growth of 2.3% in Q1, down from a peak of 3.9% on February 3. The Citi US Economic Surprise Index has also dipped into negative territory.

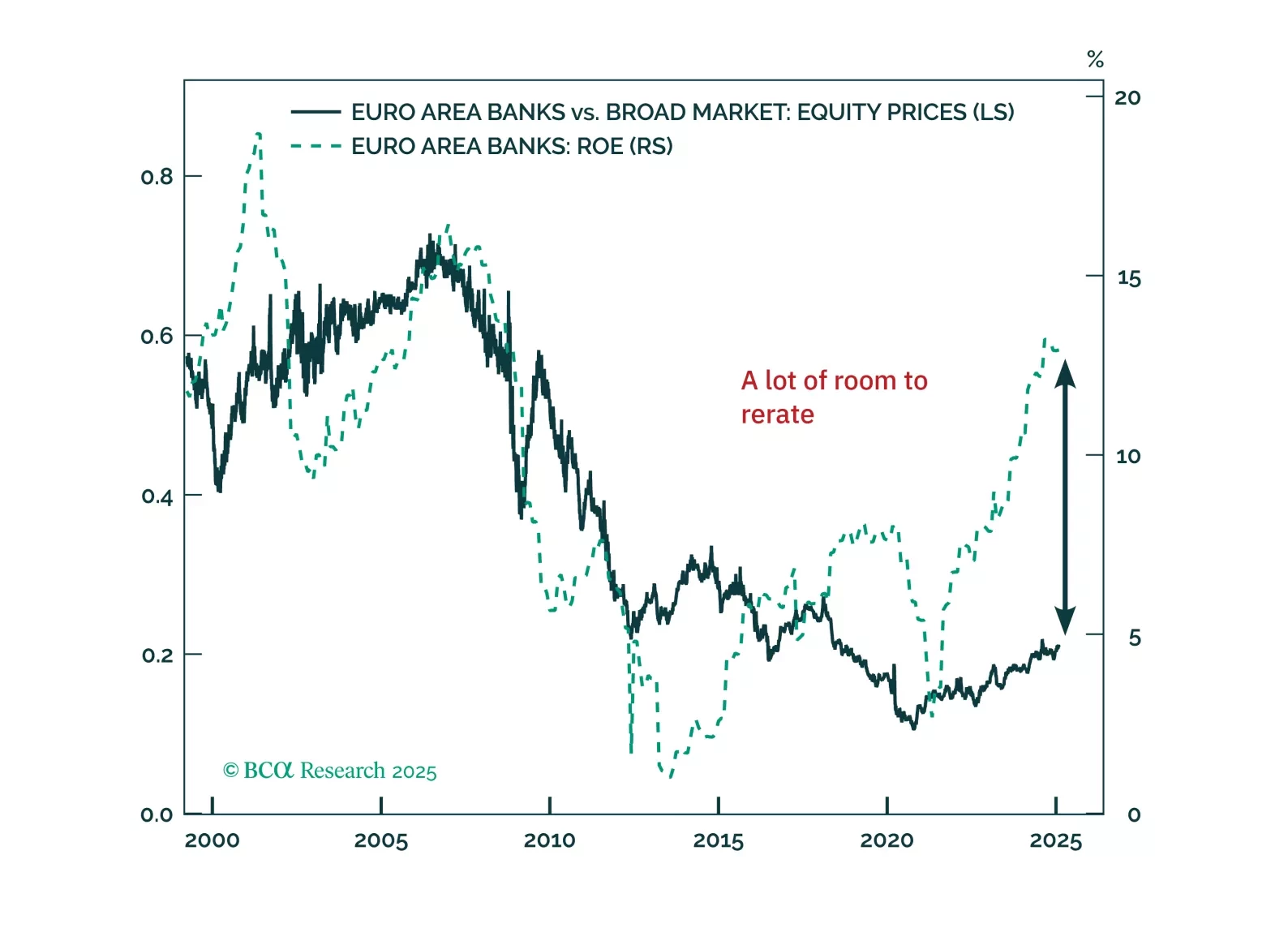

Eurozone banks have quietly outpaced the Magnificent 7—can they keep winning? With strong balance sheets, rising profitability, and structural tailwinds, European lenders still offer value despite short-term risks. Meanwhile, German equities continue to defy expectations, but is a near-term pullback on the horizon?