Economy

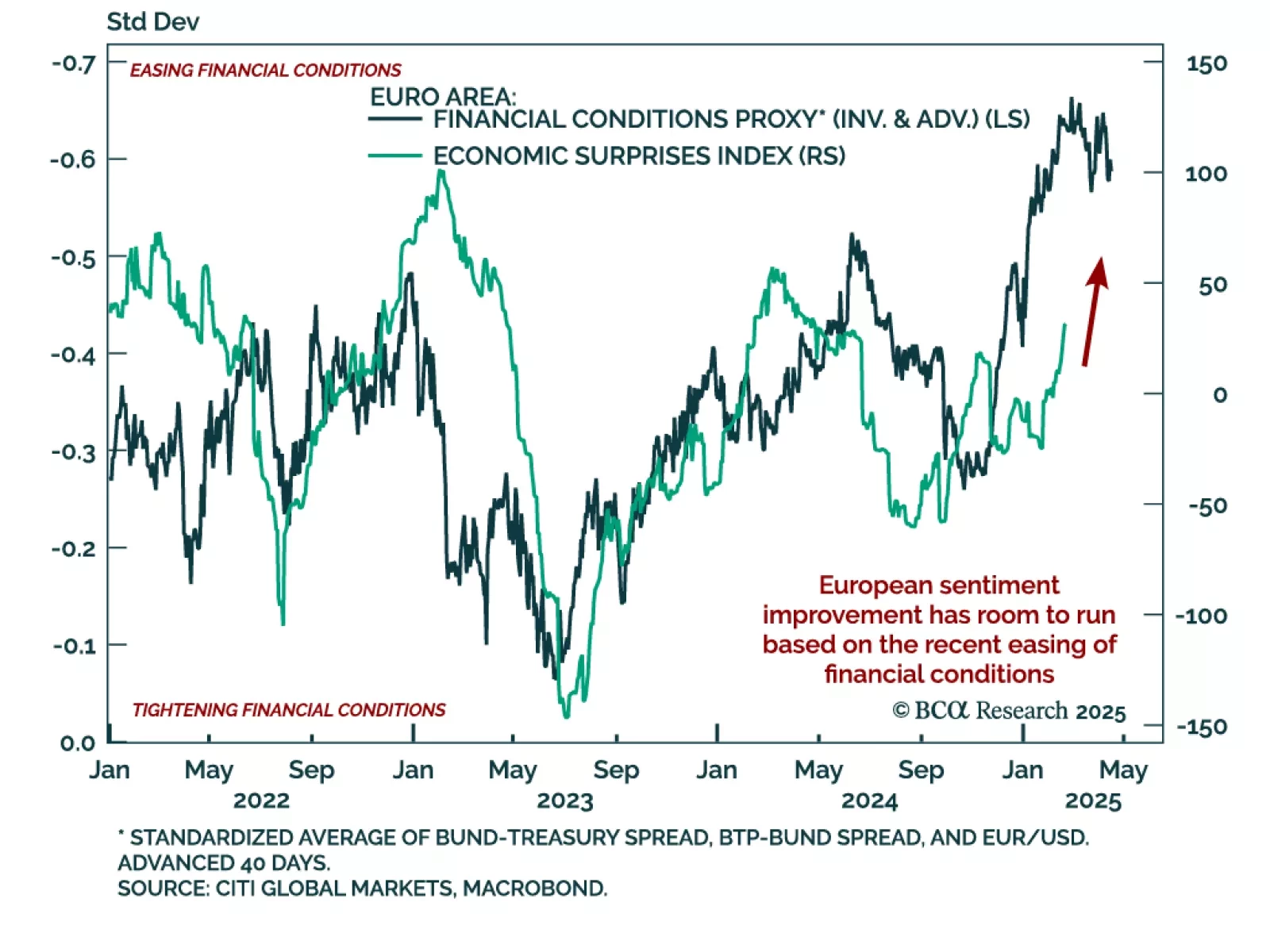

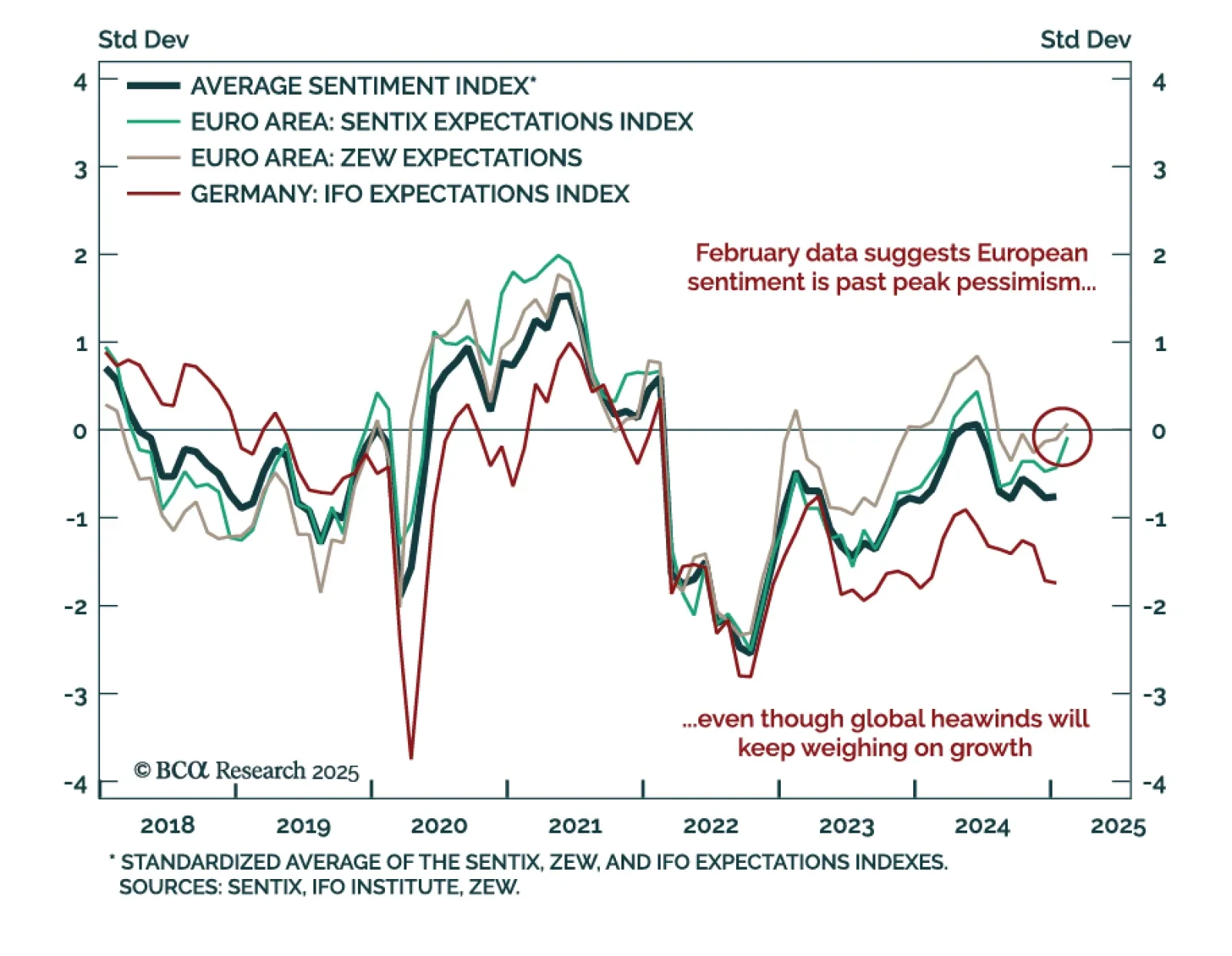

A nascent theme in the latest data is the broad improvement in European sentiment. The February Sentix and ZEW surveys both improved, and flash estimates for European consumer confidence beat estimates, ticking up to -13.6%. Confidence remains low, but…

In this webcast, Dhaval will give an update on his key views for 2025. The discussion will include:

Why the US is heading into ‘mini stagflation’.

Why the BoJ must hike interest rates, and the global consequences.

The outlook for global bond yields and the dollar.

The latest advances to our complexity analysis and indicators.

When the bull market will end.

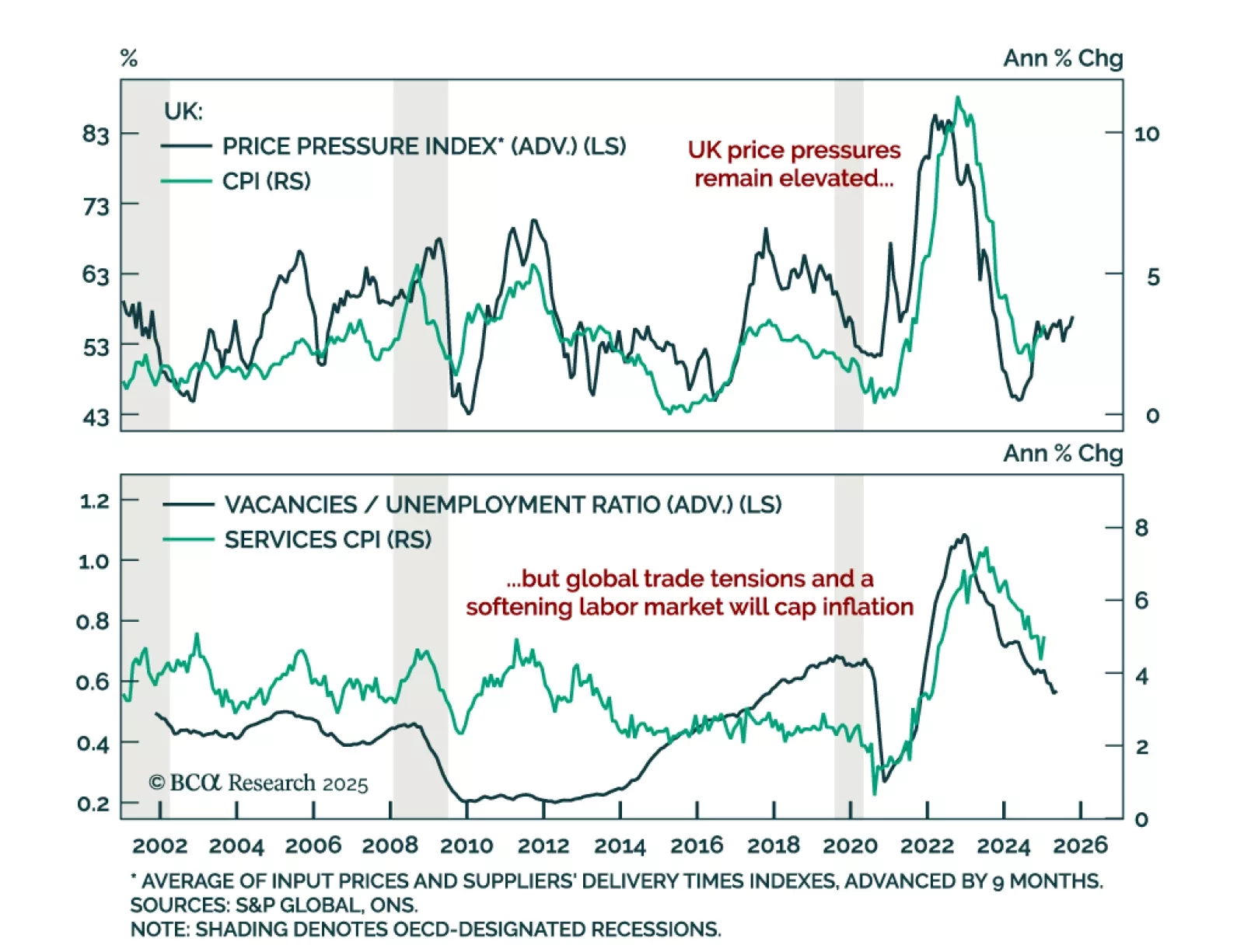

The January UK CPI was slightly hotter than expected. Headline inflation beat estimates, rising to 3.0% y/y from 2.5% in December. Core inflation also jumped but was in line with expectations at 3.7%. Services were strong, albeit slightly lower than expected…

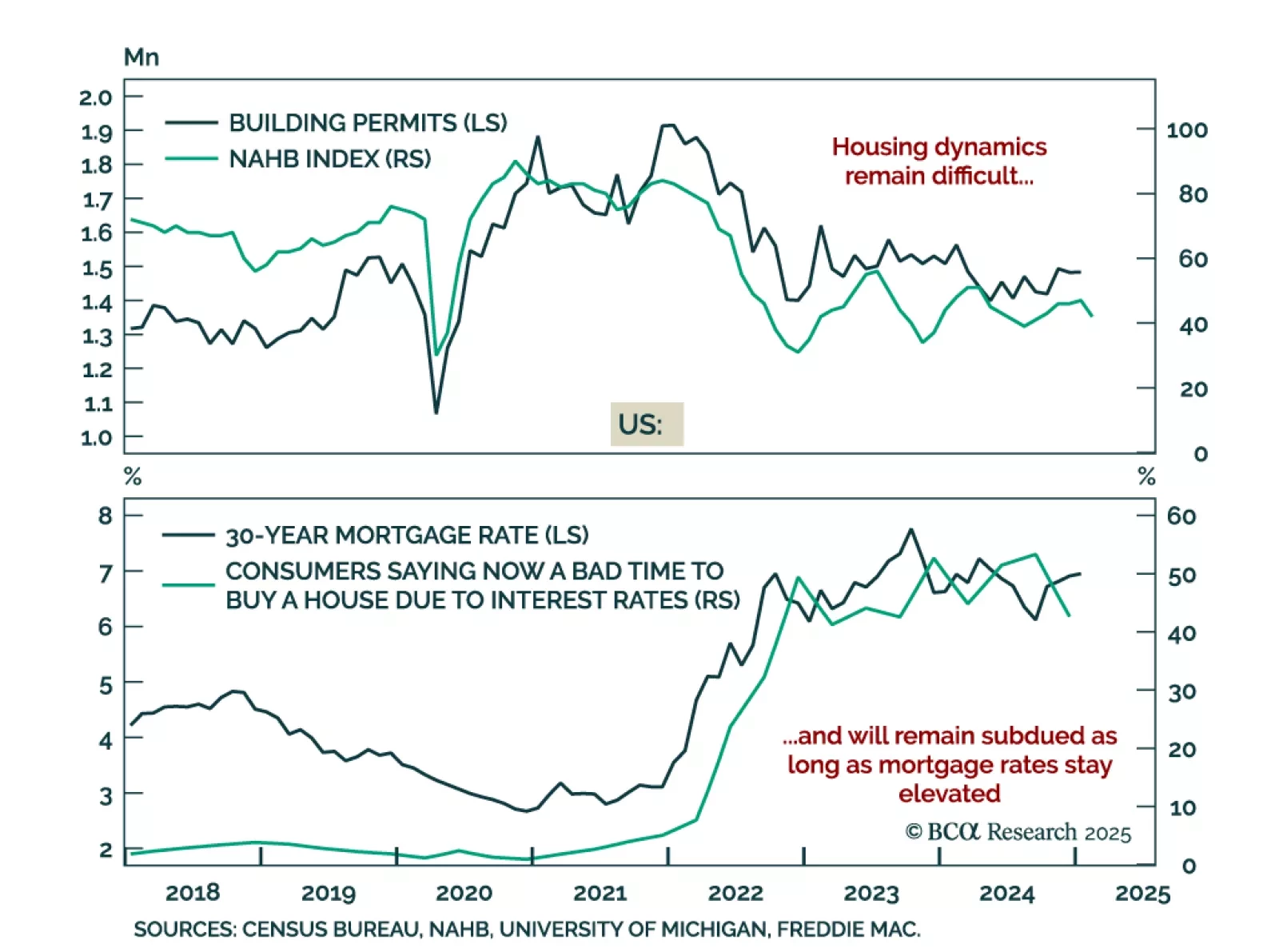

US January housing data disappointed, with housing starts falling 9.8% m/m after expanding 16.1% in December. The February NAHB Housing Market Index also weakened, falling to 42 from 47 in February. Building permits were the one positive surprise, growing…

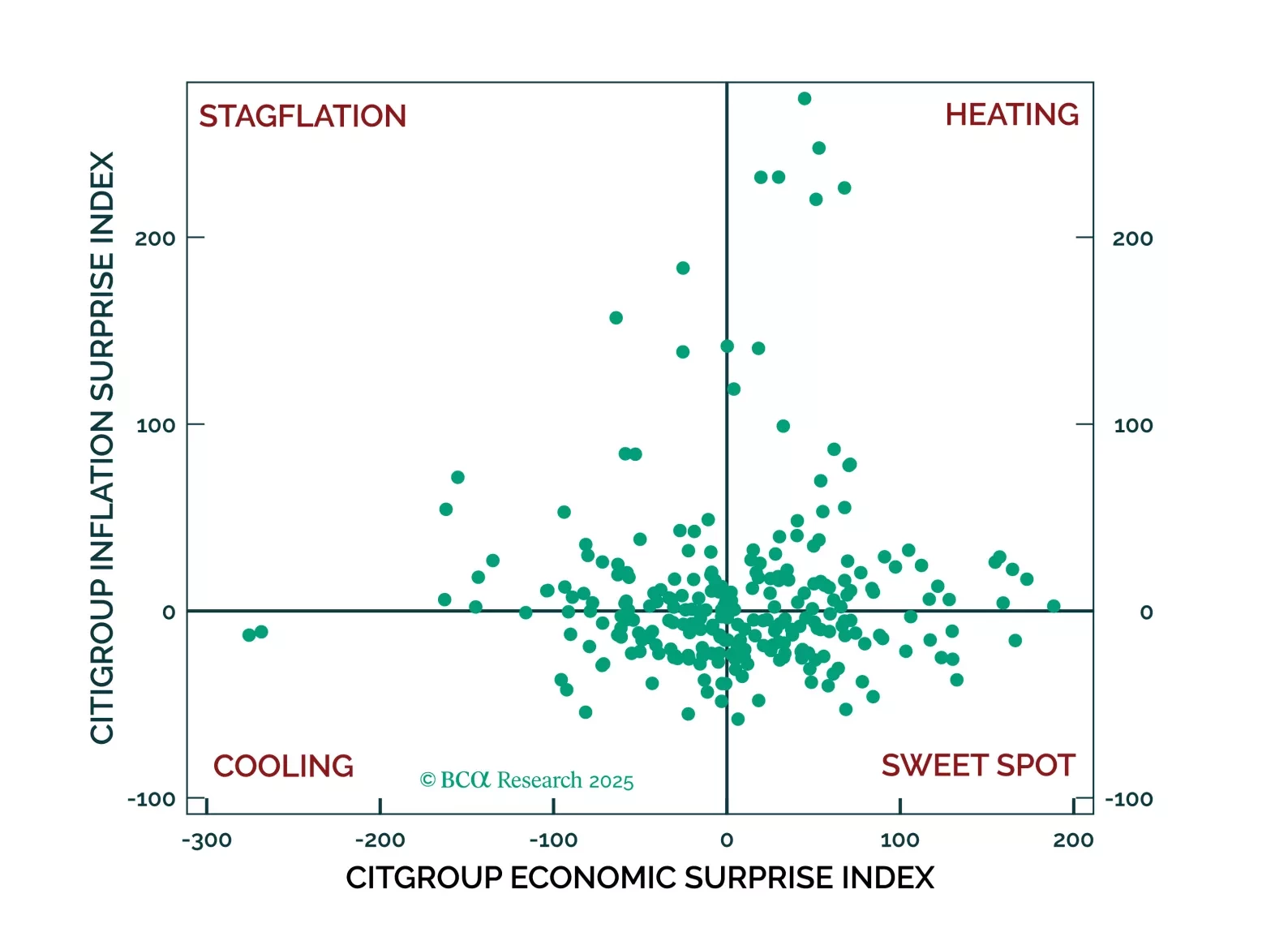

We introduce a systematic approach to investing based on the combination of three macroeconomic variables: economic, inflation, and monetary policy surprises.

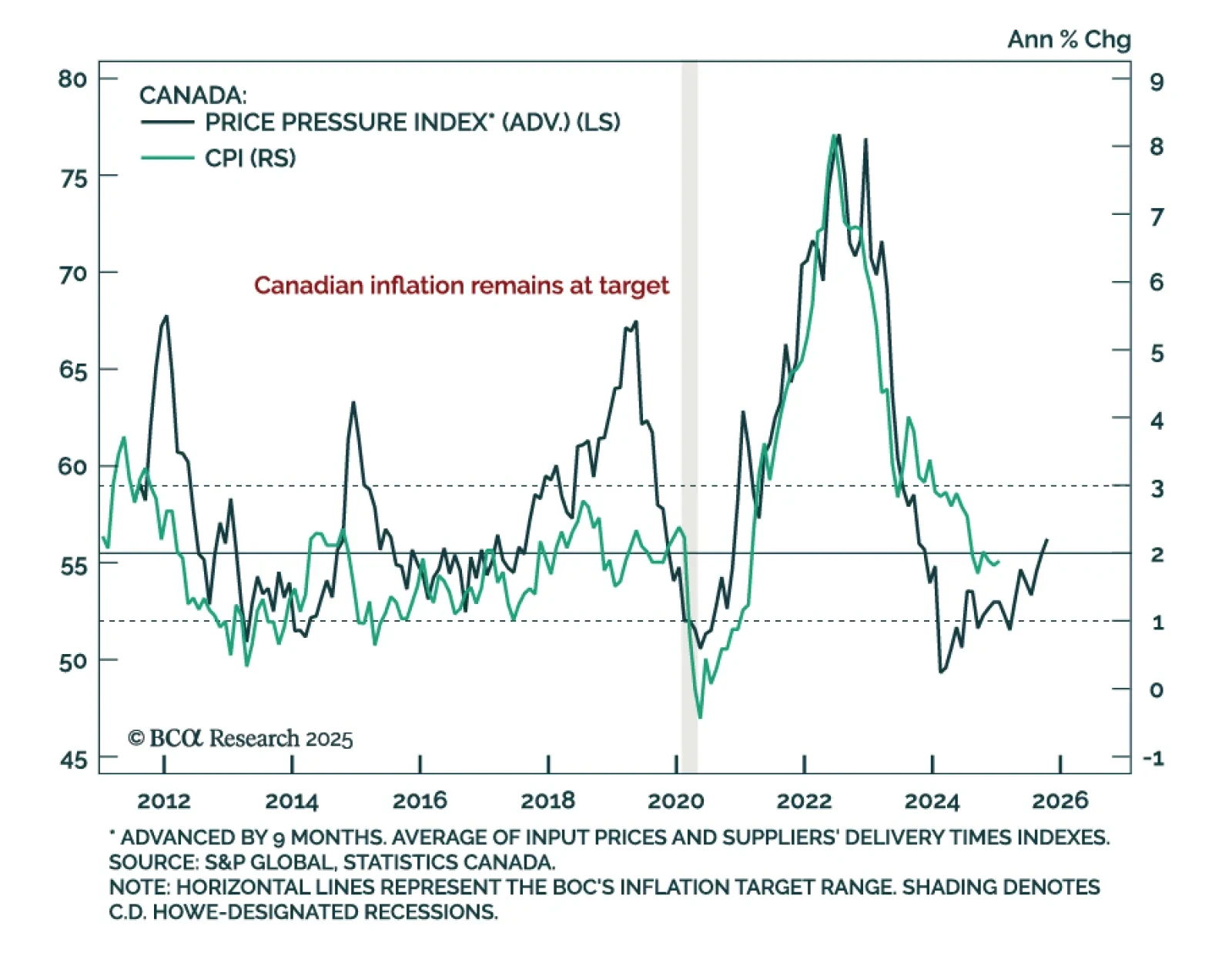

January Canadian headline inflation was in line with estimates at 1.9% y/y. The Bank of Canada’s core measures were slightly hotter than expected, rising to 2.7%, near the top of the Bank of Canada’s 1%-to-3% target range. Canadian inflation remains…

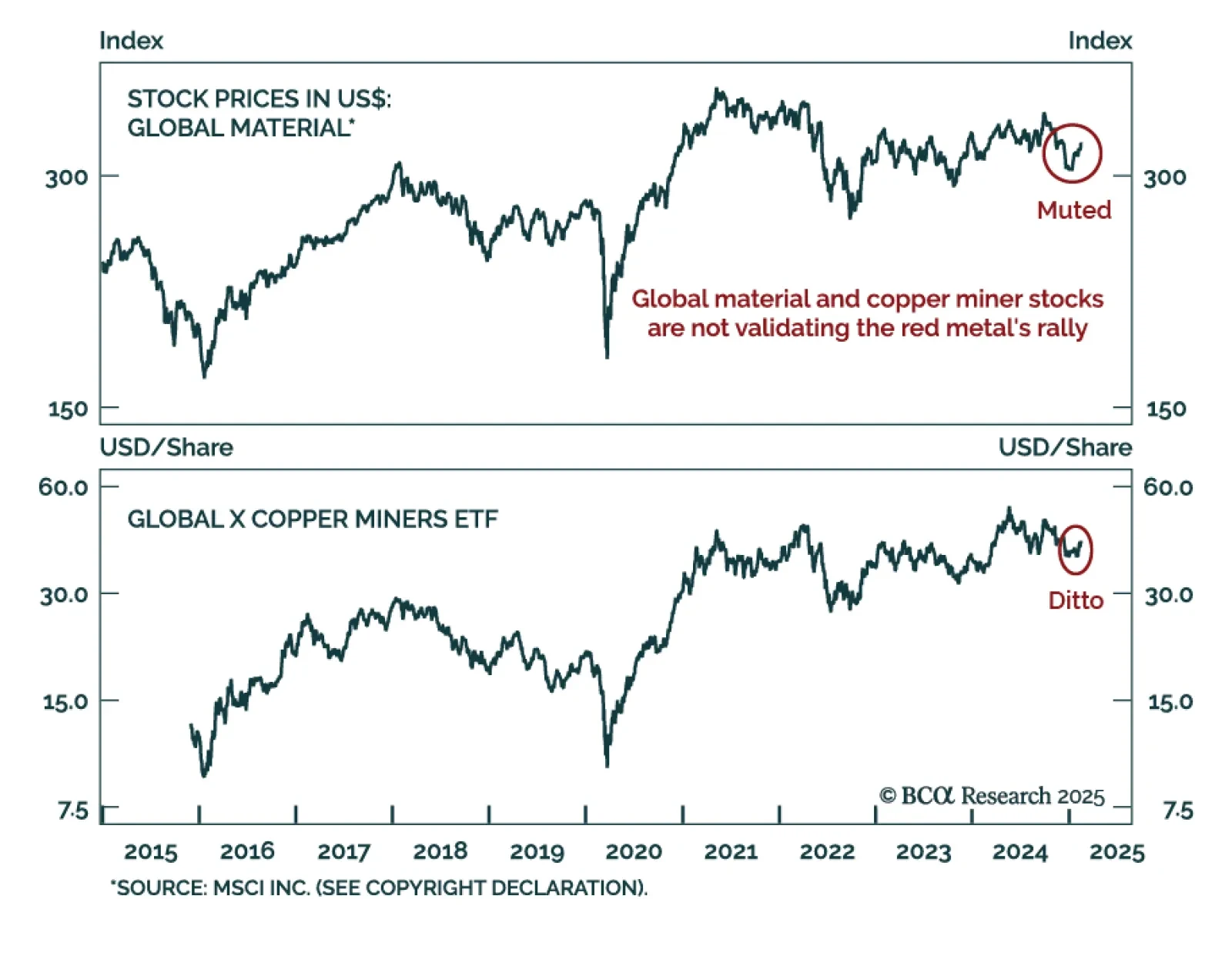

Our Emerging Markets and Commodities strategists explored the dislocations in metals markets as tariffs fears led to physical flows to the US and price spikes. US import tariffs on gold, silver, platinum, and copper are unlikely because their…

The February ZEW index for Germany and the eurozone beat estimates, with the expectations component rising to 26.0 from 10.3 a month prior. The current situation assessment also improved, although it remains deeply negative at -88.5. The improvement…

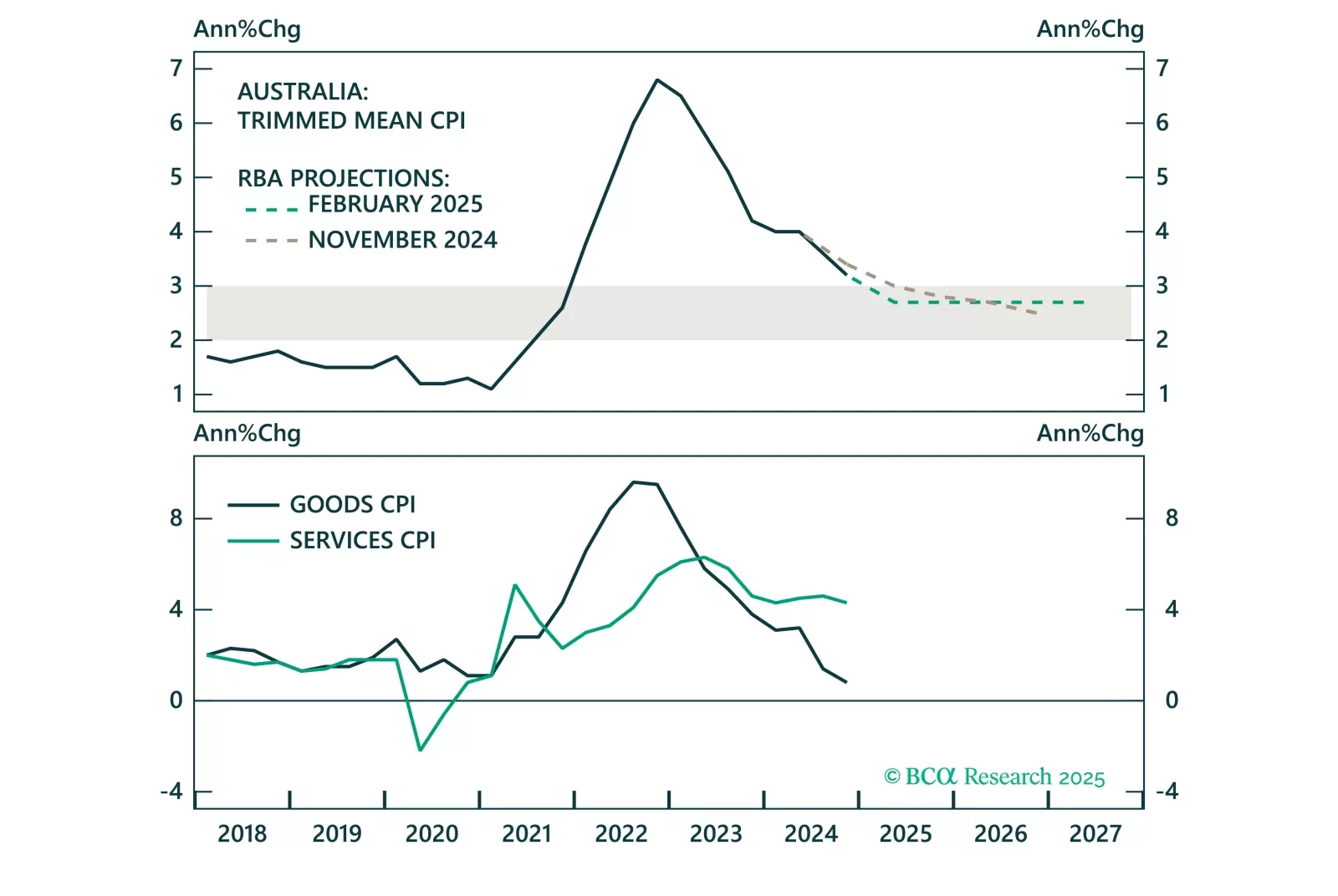

Overnight, the RBA cut the cash target rate for the first time since 2022, marking the beginning of the policy easing cycle in Australia. However, the RBA will proceed cautiously with further rate cuts, given a tight labor market and still elevated services inflation. This will keep Australian government bond yields elevated versus global yields, benefitting the Australian dollar.

Ryan will outline the value proposition in US bonds and discuss the main factors that will determine the direction of yields over the next 6-12 months, including: