Economy

The January NFIB Small Business Optimism Index decreased more than expected to 102.8 from 105.1. After reaching near all-time highs in the wake of the election, expectations pulled back somewhat as uncertainty took center stage. The decline was…

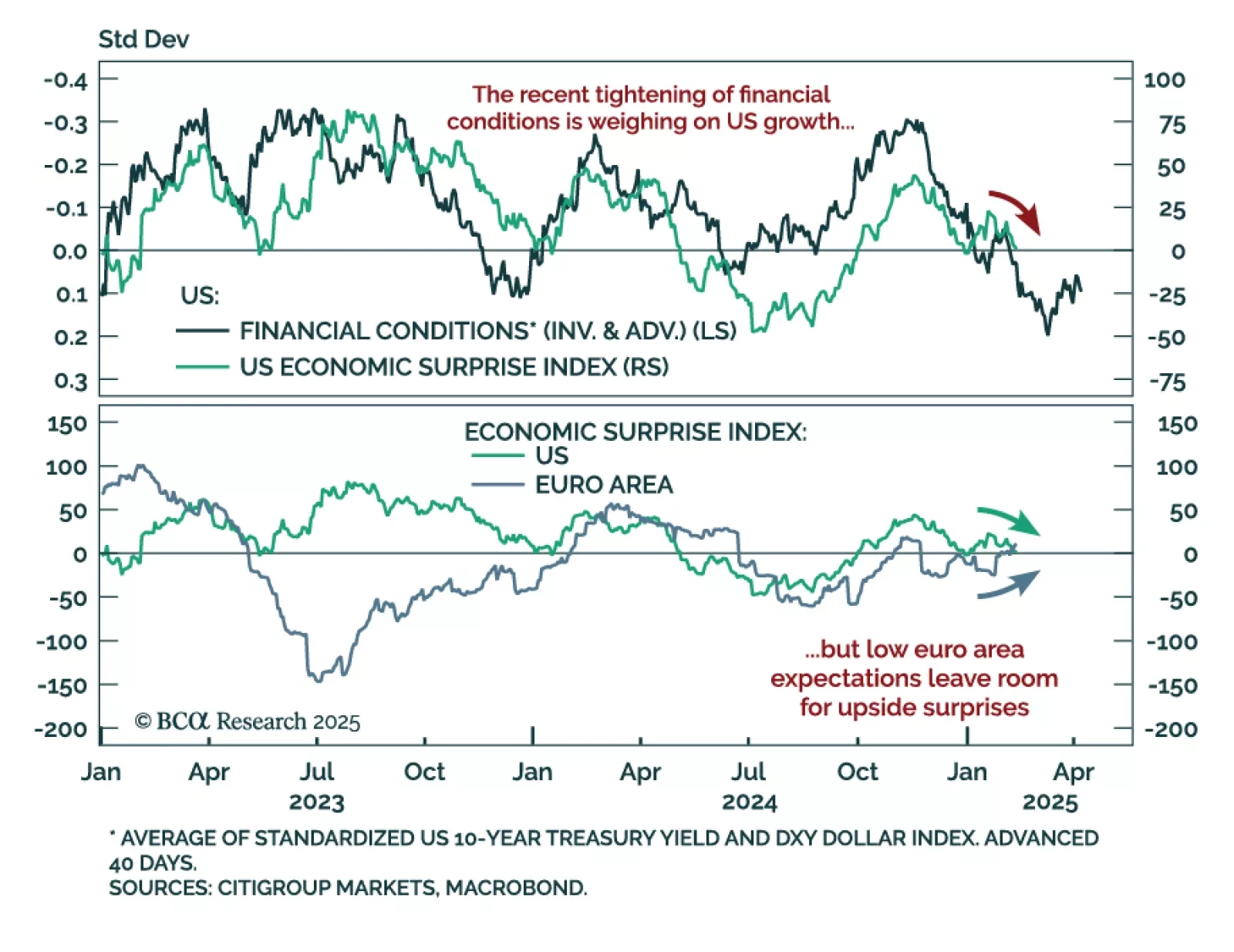

While geopolitics captured the latest headlines, Eurozone economic surprises have turned positive, while those in the US are on the verge of turning negative. Global economic surprises hinge on expectations and realized data, and they play a…

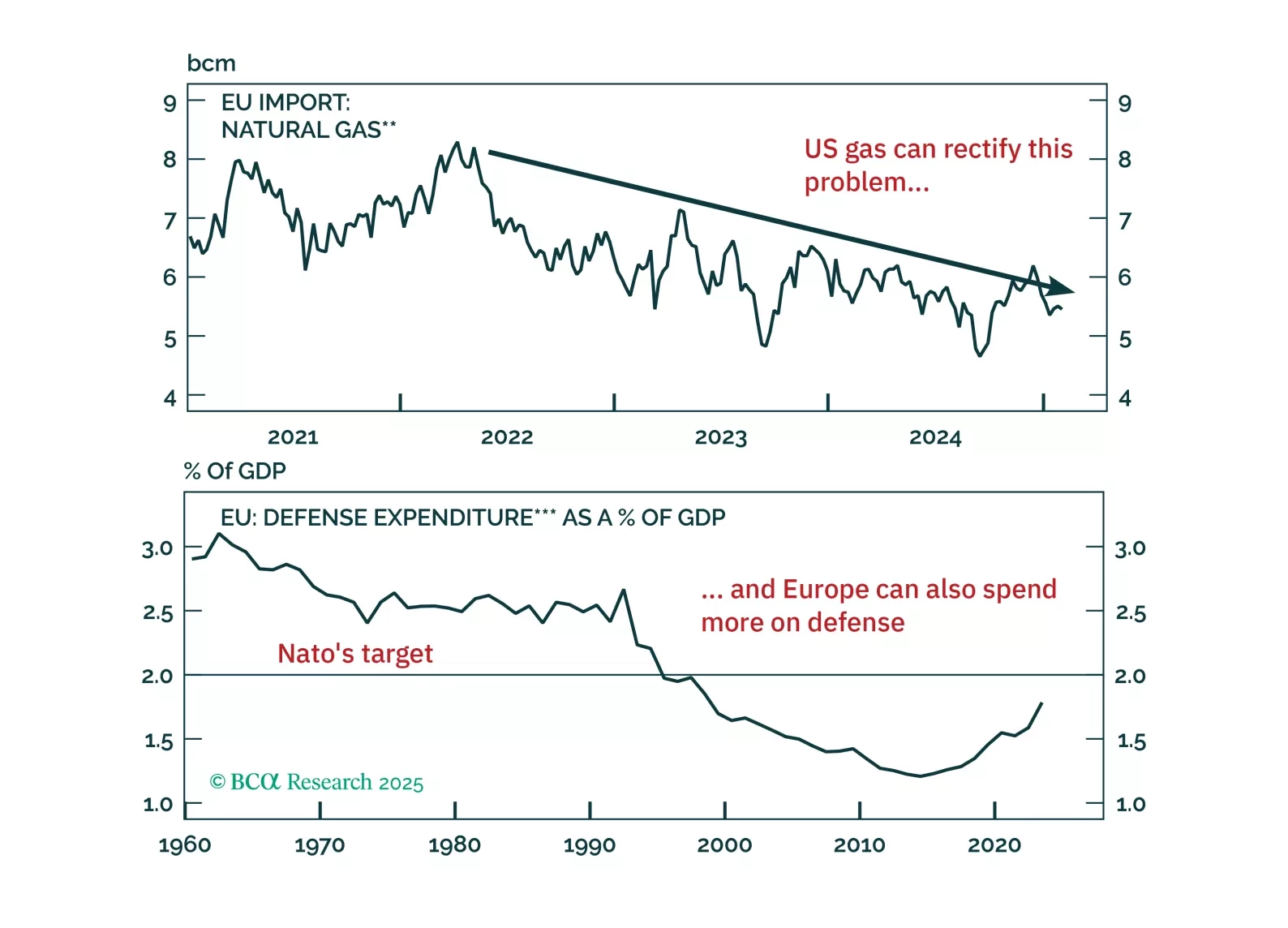

Our European strategists evaluate the looming threat of US tariffs on Europe, as it is President Trump’s next trade target after Canada, Mexico and China. While a deal centered on European energy imports and defense spending is likely, uncertainty will remain…

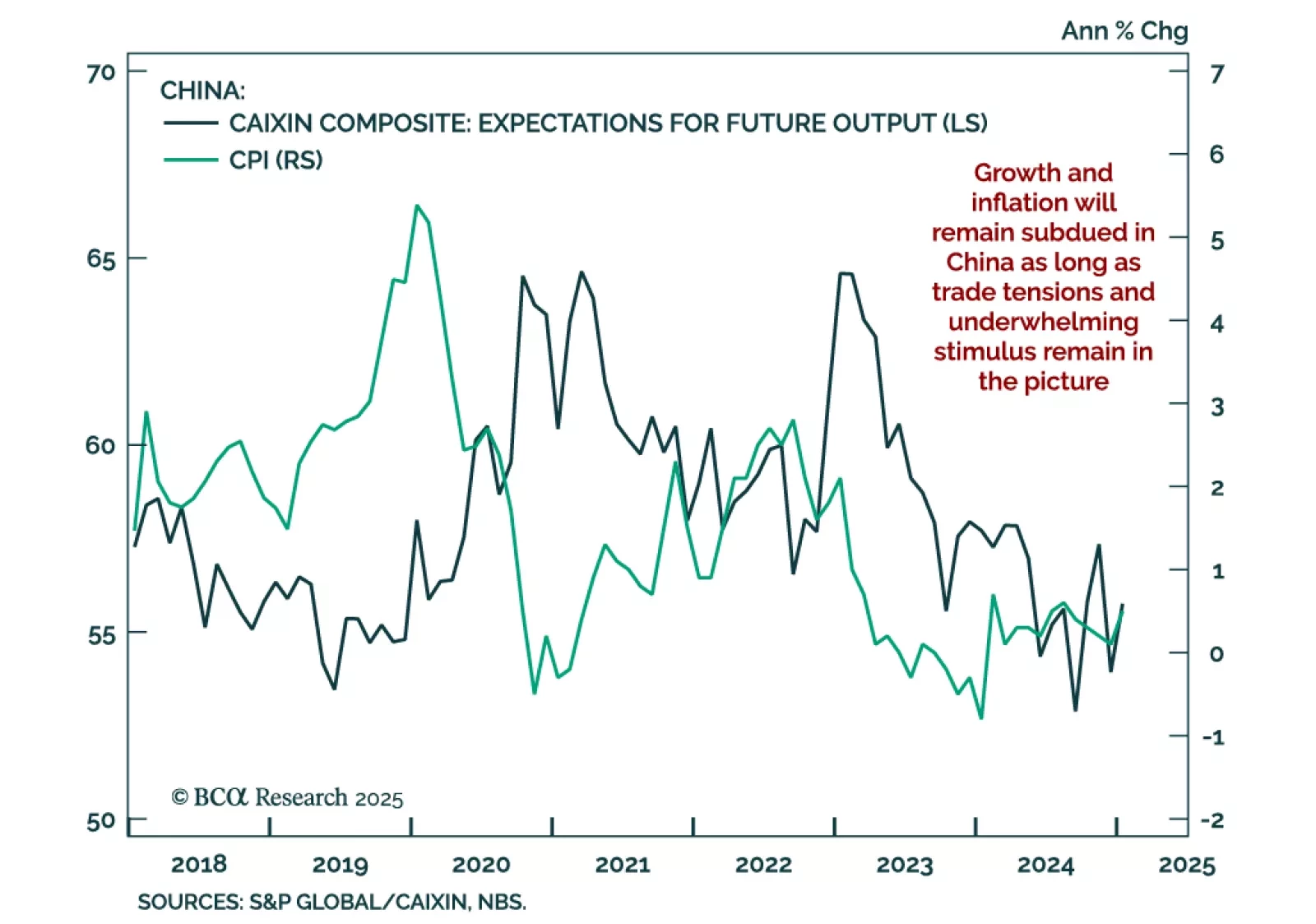

China’s January consumer prices rebounded to 0.5% y/y, and producer price deflation was unchanged at -2.3%. China’s first quarter data tends to be distorted by the Chinese New Year, as its variable dates shift consumption peaks around without a clear pattern.…

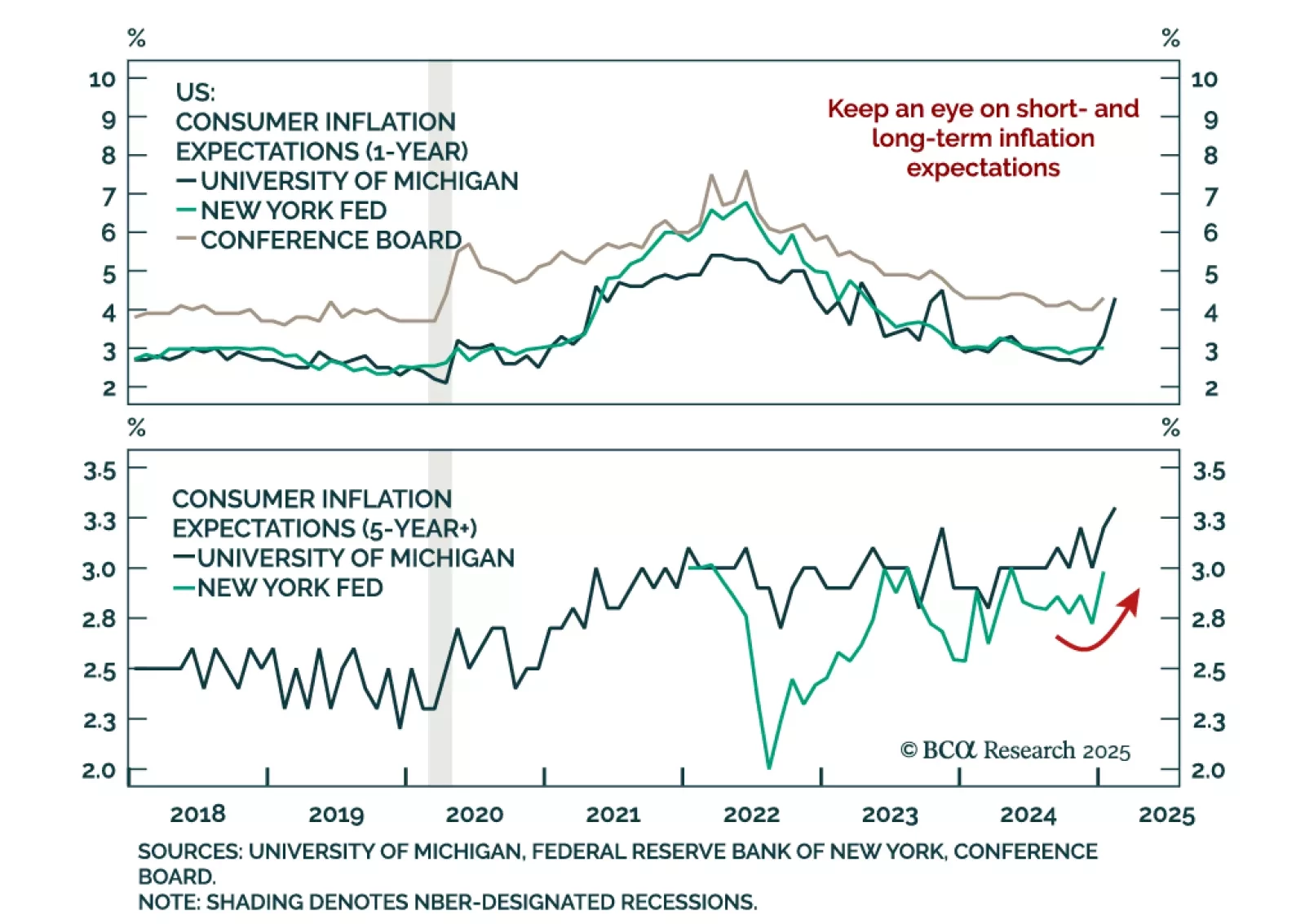

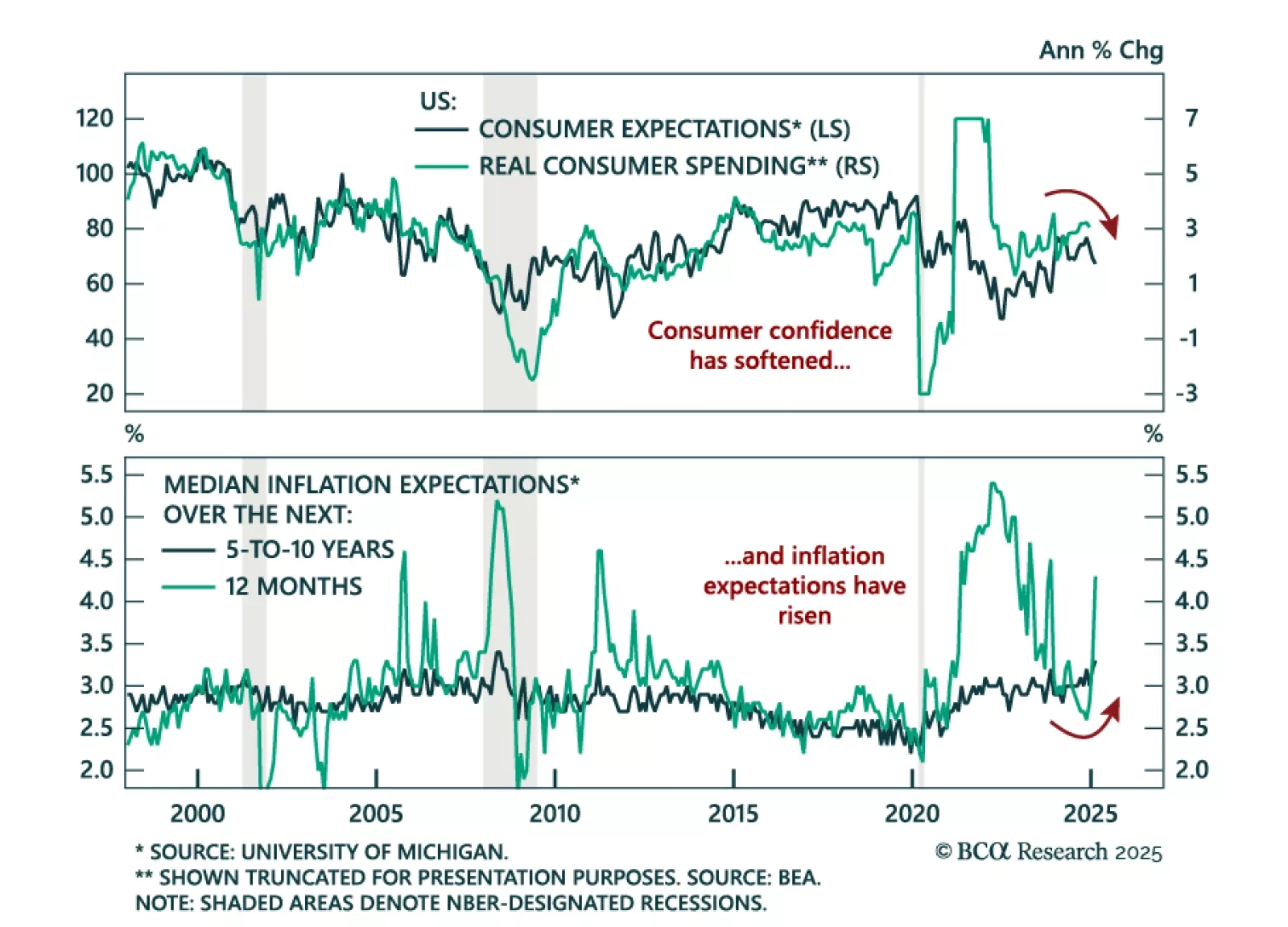

The New York Fed’s Survey of Consumer Expectations’ 1-year and 3-year inflation expectations were unchanged in January. Five-year ahead expectations however increased, as did expectations for staples inflation, while spending expectations…

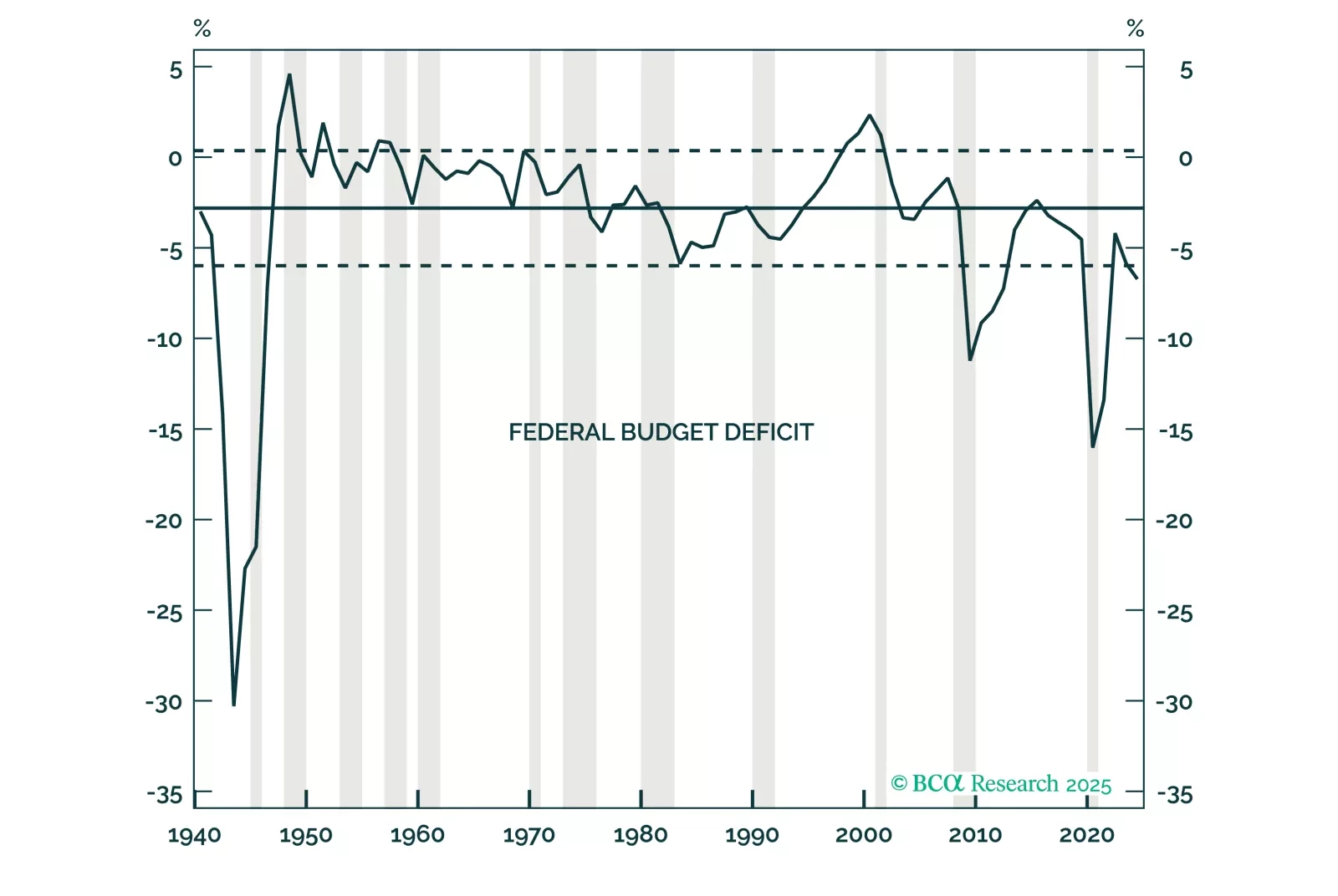

The 3-3-3 plan pitched by Treasury Secretary Scott Bessent will need several improbabilities to break its way if it is to meet its goals. We think it is much more likely that the plan will disappoint. Defensive asset allocations will outperform once it becomes clear that 3-3-3 will fall short, but we are currently neutral across the board because the disappointment may be months away.

The preliminary February University of Michigan Consumer Sentiment Index missed estimates, falling to 67.8 from 71.1 in January. The decrease came from both expectations and the assessment of current conditions. Measures of 1-year and 5-10 year inflation…

Our Emerging Market strategists published a follow-up piece to their Bessenomics note where they assess the new Treasury Secretary plan’s impact on markets. Lower interest rates are central to Bessenomics. The Trump administration is expected to pressure…

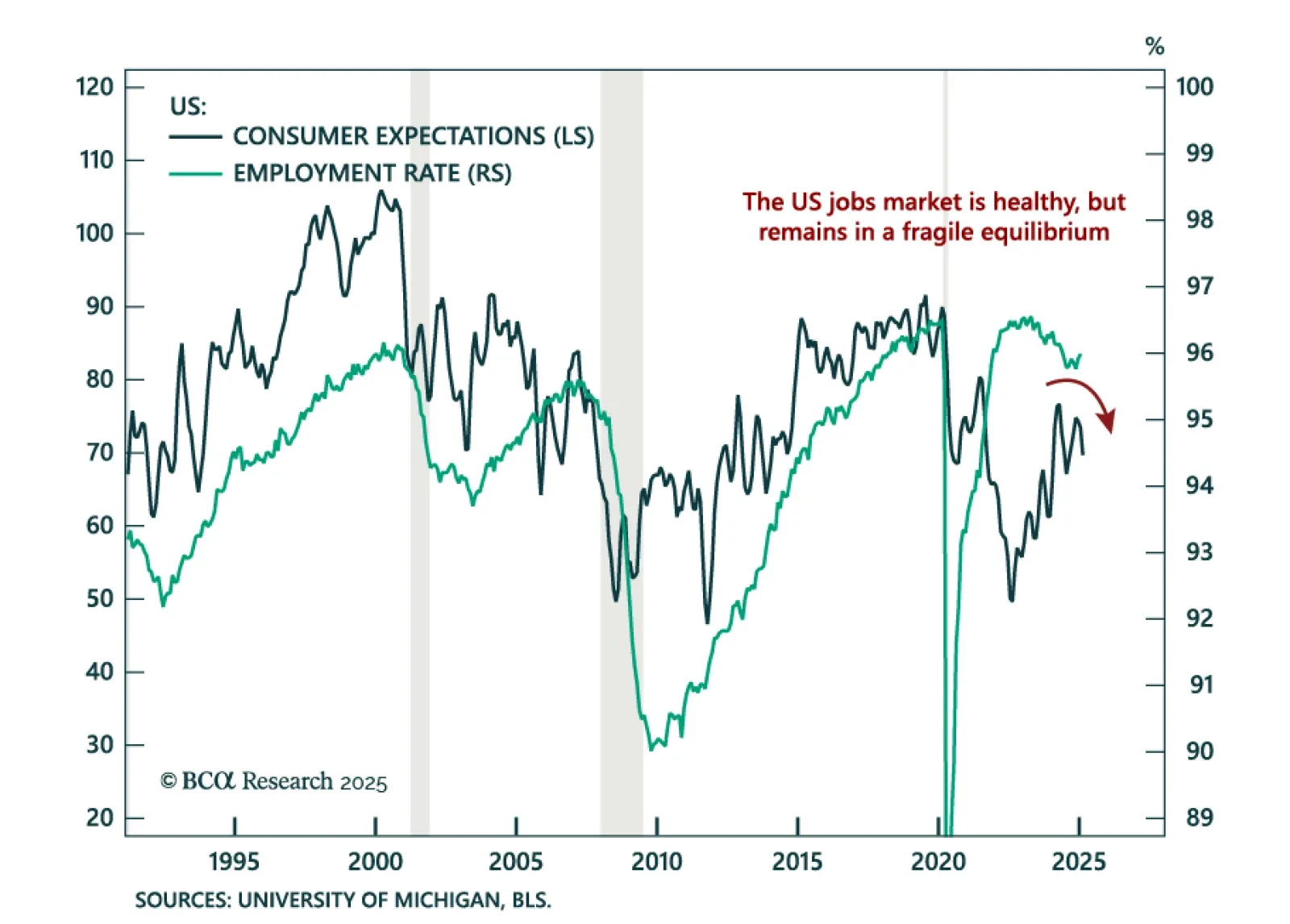

The January US jobs report was solid, reflecting a healthy labor market. Payrolls rose by less than expected at 143k, down from an upwardly-revised 307k in December, leaving the 3-month moving average at 237k. The unemployment rate ticked down 0.1% to 4.0%…

Europe is about to become President Trump’s next target. The good news: a US/EU trade war will be short as common ground to achieve a deal exists. The bad news: European assets remain at the mercy of heightened uncertainty. How should investors position themselves in this tricky context?